PFE - Pyxis Oncology: Cashed Up And Entering The Clinic

2023-03-27 07:32:43 ET

Summary

- PYXS has initiated dosing with PYX-201 in a phase 1 study, with preliminary results due in early 2024.

- PYXS expects to initiate dosing in a phase 1 study of PYX-106 in Q2'23, which could add additional readouts to the 2024 calendar.

- PYXS trades very cheaply and an argument could be made for entering the stock ahead of any initial data from PYX-201, to capture a potential run-up.

Pyxis Oncology (PYXS) is a biotech based in Cambridge, Massachusetts, with two therapeutics in the clinic that have potential in various cancer types. The stock reached a recent low in December 2022 and is up around 100% since; this article takes a look at the company's prospects.

PYXS makes progress

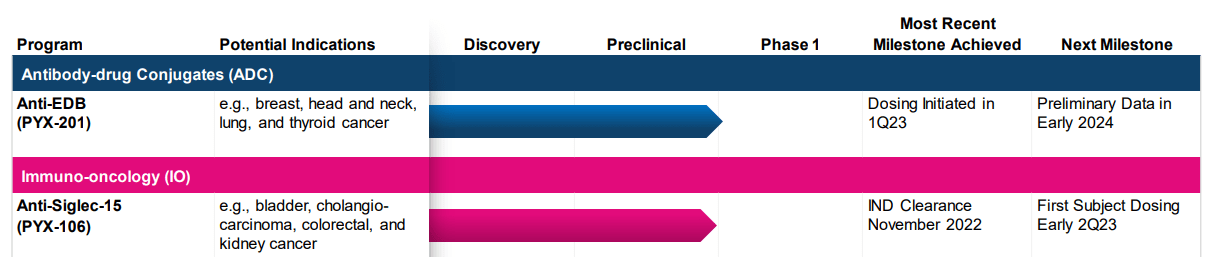

The obvious event that has played a role in the turnaround of PYXS is the entry into the clinic of their antibody-drug conjugates [ADC], PYX-201 and their immunotherapy candidate PYX-106. On December 1, 2022, PYXS announced that two Investigational New Drug [IND] applications had been cleared by the FDA. This means that their drugs PYX-201 and PYX-106 were free to enter the clinic.

The clinical component of PYXS's pipeline. (PYXS Corporate Presentation, March 2023.)

{kind=link}

PYX-201

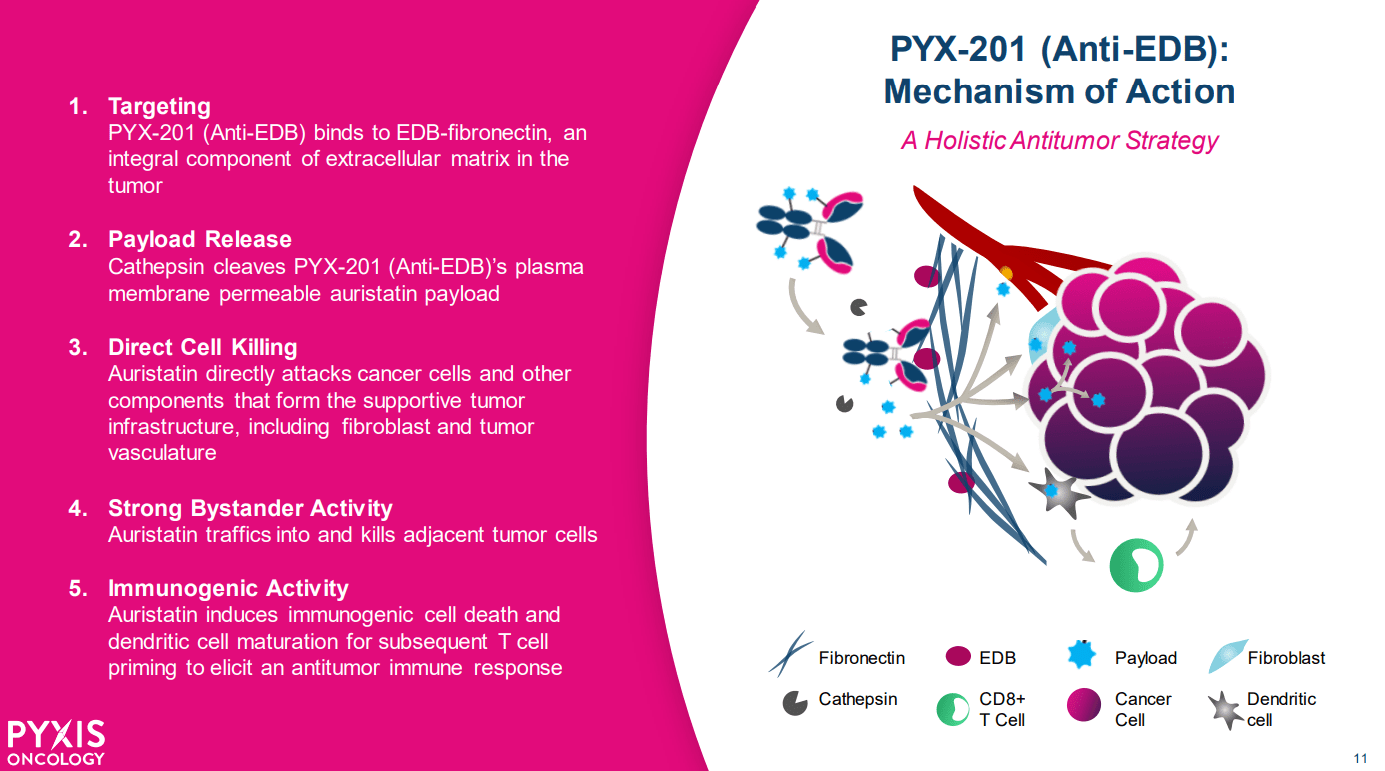

PYX-201 is an ADC directed against extra-domain B of fibronectin (EDB), with an auristatin payload. The idea is that EDB-fibronectin is found in and around tumors, where it promotes the growth of new blood vessels to supply the tumour, but not so much throughout the rest of the body.

PYX-201 Mechanism of Action (PYXS Corporate Presentation, March 2023.)

{kind=link}

On March 16, 2023, PYXS announced it had dosed the first patient in its phase 1 trial of PYX-201. The phase 1 trial will enroll patients with various cancer types and look at safety, toxicity, pharmacokinetics, pharmacodynamics and efficacy. We don't have any anti-tumor activity data yet, so there is little to go off in regards to PYX-201 specifically. The strategy of targeting EDB-fibronectin to selectively target cancers is not new however, and so there is at least some clinical data worth considering.

Other drugs targeting EDB-fibronectin

In 2008-2009, a UK biotech, then called Antisoma plc, ran a phase 1 trial of AS1409, a fusion protein containing interleukin-12 and an antibody targeting fibronectin (containing EDB). The idea was to harness the anti-tumor activity of interleukin-12 but direct it specifically to the tumor, where EDB-fibronectin is found, to enhance the efficacy of interleukin-12 and minimize its side effects. The phase 1 trial of AS1409 was small with only 11 melanoma and 2 renal cell carcinoma patients treated . Five patients achieved a best response of stable disease and a sixth achieved a partial response.

There was no further development of AS1409. Several of Antisoma's other drugs failed in clinical trials and in 2011 the company was forced to stop clinical trials of its various drugs to conserve cash. The company used its remaining cash to become and investment holding and management company rather than remain a biotechnology company. As such we can't say where AS1409 would have gone had Antisoma had the funds to develop the drug further. As such I won't say EDB-fibronectin isn't a good target for cancer therapeutics based on the fact that development of AS1409 was ceased.

For something still in development, there is Darleukin from Philogen S.p.A. (trading under PHIL on the Borsa Italiana exchange). Darleukin is a fusion protein of interleukin-2 and the antibody L19 (an antibody that binds EDB of fibronectin). In a 67-patient , phase 2 trial of Darleukin, there was a statistically significant benefit on overall response rate and median progression free survival of Darleukin added to dacarbazine versus dacarbazine alone in metastatic melanoma.

A separate, ongoing phase 2 trial of Darleukin, sponsored by Maastricht University, in metastatic non-small cell lung cancer with an estimated enrollment of 126 participants began in April 2019. That study, although open-label, does include a control group, with one group receiving standard of care plus radiotherapy, with the experimental arm receiving Darleukin plus radiotherapy. As the trial has an estimated primary completion date of December 2022, and an estimated study completion date of December 2023, we might see some results in 2023 which can provide another confirmation that targeting another molecule to a tumor with an EDB-fibronectin binding antibody is a viable strategy in cancer. Of course in the case of Darleukin, that molecule is interleukin-2, whereas with PYX-201 it is an auristatin payload, but looking at the work so far with anti-EDB antibodies, I can see why PYXS sees potential with PYX-201.

In PYXS's March 16 press release, the company notes that it expects preliminary data from its phase 1 study of PYX-201 in early 2024. That means a bit of a wait for investors, but perhaps PYXS will at least release some data in H2'23 on the pharmacokinetics and some sort of update on toxicity/safety (i.e., so far so good, dose escalation proceeding, etc.) even if there is no efficacy data supplied in 2023.

PYX-106

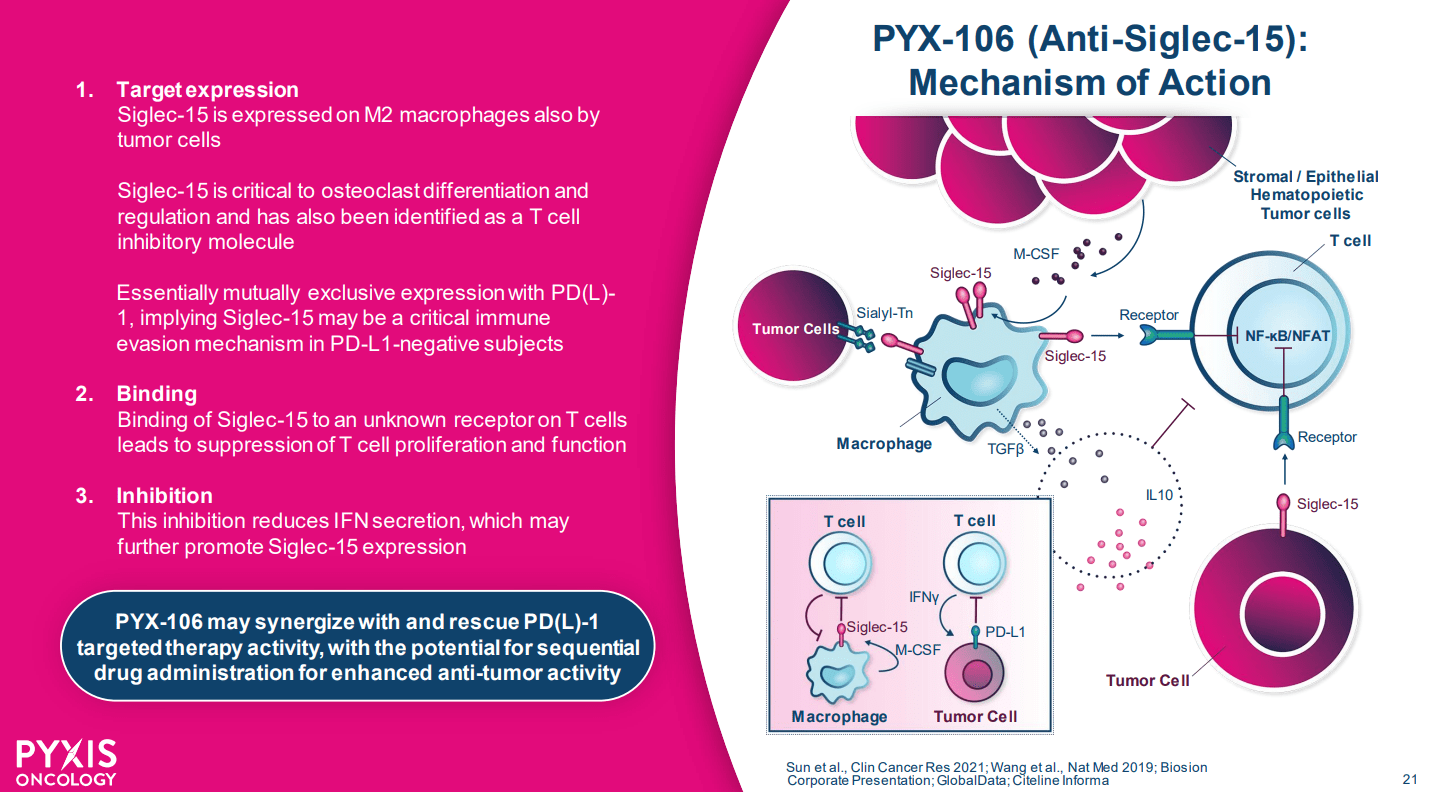

PYXS's other drug entering the clinic is PYX-106, an antibody against Siglec-15. The idea here is that Siglec-15, found on tumor cells and macrophages, binds a yet-to-be-identified receptor on T-cells to suppress activation of the immune system. As such, tumor cells can reduce immune system activation that might otherwise lead to tumor cell killing. Simply interfering with this process via PYX-106 then might allow the immune system to fight cancer more effectively.

PYX-106 Mechanism of Action. (PYXS Corporate Presentation, March 2023.)

{kind=link}

While we don't have any clinical data with PYX-106 to consider yet, what we do have is results from another antibody called NC318 developed by a company called NextCure ( NXTC ). While NXTC spent several years running trials on NC318, the company announced on November 3, 2022, that they would discontinue their development of NC318.

Based on current efficacy data, we have decided to discontinue our clinical development of NC318. We will continue to support Yale University through its ongoing investigator initiated trial of NC318 in combination with pembrolizumab in lung cancer patients...

Michael Richman, President and CEO of NXTC, November 3 , 2022.

PYXS's notes the apparent differences of their anti-Siglec-15 antibody (PYX-106) to NXTC's NC318, in terms of affinity, longer half-life and activity in some preclinical assays. PYXS licensed PYX-106 (previously BSI-060T) from Biosion Inc., for a $10M upfront license fee with Biosion eligible for milestones and royalties. As such preclinical work done by Biosion appears in a poster presented at the 2022 American Association for Cancer Research (AACR) Annual Meeting. Even if that PYX-106 has a 10-fold higher affinity for Siglec-15 than NC318, and a longer half-life, this might not result in much more compelling data from PYX-106. It is possible Siglec-15 isn't as promising a drug target as many would have hoped.

My feelings are similar regarding demonstrations of what appears to be superiority of PYX-106 to an NC318 analog in other assays (a study in mice, an ex vivo study with human blood cells) presented in that AACR poster and reproduced by PYXS in its corporate presentation. They provide a theory for why PYX-106 might succeed where NC-318 underwhelmed, but I think the market will have a "show me" attitude regarding Siglec-15 antibodies, even if PYX-106 looks like it might be a better anti-Siglec-15 antibody. Nonetheless given the theoretical potential of anti-Siglec-15 antibodies, I'm glad that PYXS is giving one a chance.

Financial summary

PYXS reported full year 2022 earnings on March 22, noting year end cash and cash equivalents of $180.7M and no debt. Net cash used in operating activities was $89.4M , which would suggest current funds should last PYXS to the end of 2024 or thereabouts assuming that rate of use remained constant. PYXS has guided similarly, noting it expects its cash to fund operations into H1'25. This is good news for investors as PYXS will be able to produce plenty of data before it has to raise cash again, an ideal scenario given the tough market conditions for biotechs currently.

As of March 21, there were 36,980,621 shares of PYXS outstanding, corresponding to a market cap of $81.7M ($2.21 share price). As such PYXS trades at about 45% of year end 2022 cash. I should briefly note a recent increase in holdings by Pfizer ( PFE ), while PFE now owns ~6M shares of PYXS, the recent Form-4 for 1.8M shares notes that these shares were issued as part of the license agreement between the two companies (PYXS licensed ADC technology from PFE).

Conclusions

With PYXS trading at less than half of cash, the market isn't putting a whole lot of value into PYXS's pipeline, and while I'm cynical on PYX-106, it might produce a few responses anyway, the way NXTC's NC318 did, and that could make market participants think PYXS has improved on NXTC's efforts. From a trading viewpoint then, there is a potential long thesis there, even if you're skeptical about PYX-106 long-term. Then there is PYX-201, which I'm less negative about, providing another shot on goal for the company.

With the potential of PYX-201 and PYX-106 to perform, or at least show something promising short-term, the idea that the stock might go up in the next six months to a year doesn't seem unreasonable to me, but that isn't the strongest bull thesis I've ever heard. That being said, PYXS still has plenty of cash runway, isn't in a tough position where it needs to raise, it can cut back development at any time to extend runway and focus on its favorite assets. Putting all that together then, I've rated PYXS a buy.

The risks of any long in PYXS are several fold, a few of which are worth discussing here. Firstly, if the company has to halt development of one of its drugs due a toxicity issue, the stock could trade down. Further, even if the safety profile of PYXS's drugs allow it to produce plenty of data, that efficacy data might underwhelm. Lastly, delays in producing data can cause speculators to exit, which could cause the stock to sell off.

For further details see:

Pyxis Oncology: Cashed Up And Entering The Clinic