PYXS - Pyxis Oncology: Catalysts Ahead Cash In Hand And An Acquisition Completed

2023-09-07 08:09:09 ET

Summary

- Pyxis Oncology completed an acquisition of Apexigen, adding to its pipeline and bringing in a drug called sotigalimab.

- Pyxis Oncology's pipeline includes PYX-106 and PYX-201, with preliminary data expected in late 2023 and early 2024, respectively.

- The company has a strong financial position with cash and investments of $144.1 million, enough to last into the first half of 2025.

When I last wrote about Pyxis Oncology ( PYXS ) in March 2023, the company looked to be about 9-12 months away from producing some data with its antibody-based cancer therapeutics. I rated the company a buy at that time, as its pipeline members had some chance of success, it had plenty of cash runway and was trading very cheaply at about half of cash. Since then, PYXS has completed an acquisition of a smaller biotech called Apexigen ( APGN ) and provided an update on the timing of a readout from one of its trials.

The Apexigen Acquisition

On May 24, PYXS announced it would acquire Apexigen in an all-stock deal. APGN is another antibody developer in the oncology space and its antibody discovery technology complements PYXS's antibody-drug conjugate ((ADC)) technology. APGN also brought with it a drug called sotigalimab, an antibody that acts as an agonist of CD40, giving it the potential to stimulate the immune system to fight cancer. Existing data (discussed below) do suggest that sotigalimab may indeed be active.

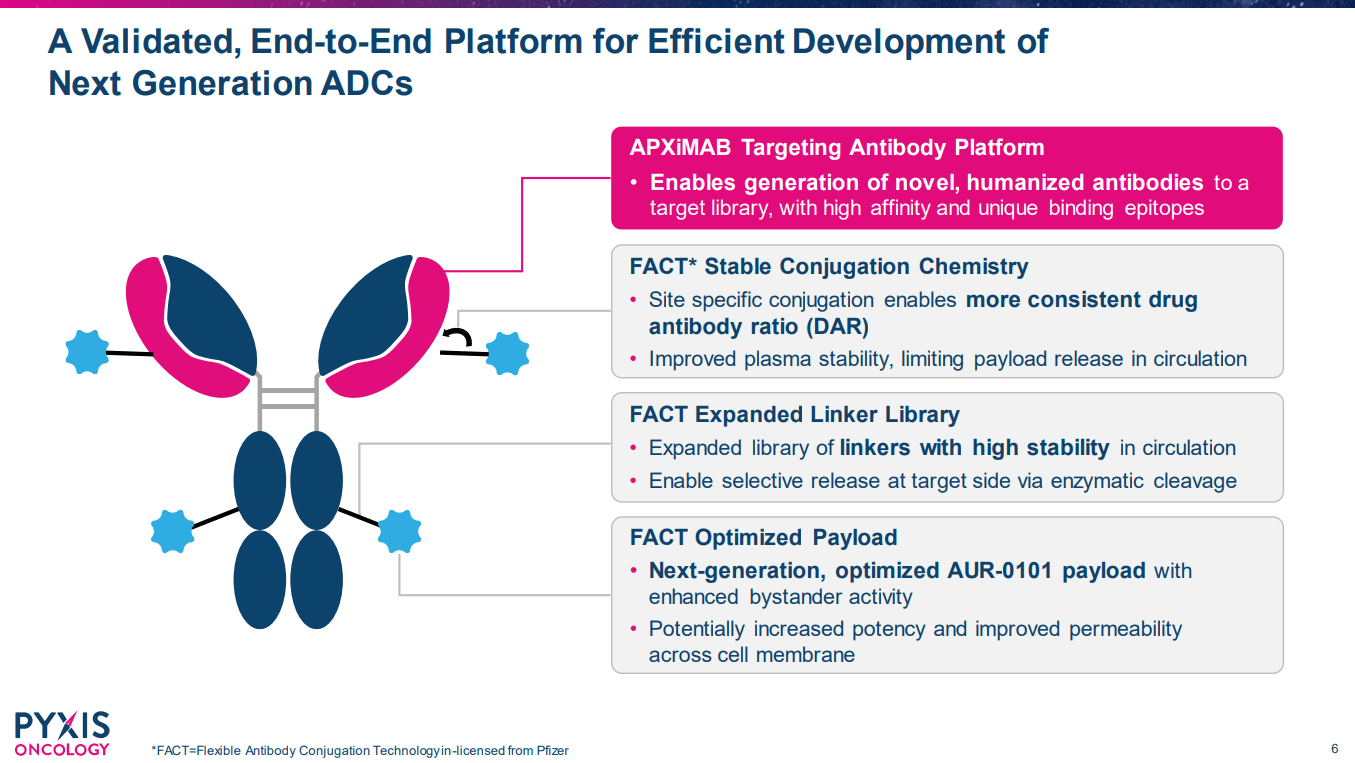

Figure 1: APGN's APXiMAB technology allows the discovery of new antibodies. (PYXS Corporate Presentation, August 2023)

{kind=link}

The completion of the acquisition was announced on August 23 . APGN shareholders got 0.1725 shares of PYXS per share of APGN, meaning APGN shareholders own about 10% of the combined company. PYXS issued 4.3M shares as a result of the transaction and noted it expected to have 43,872,248 shares outstanding after the transaction. Any APGN options, warrants, and restricted stock units were also converted to PYXS options, warrants or RSUs based on the exchange ratio. According to APGN's 10-Q for the quarter ending June 30, 2023, the company had $9.37M in cash and cash equivalents as of June 30, 2023.

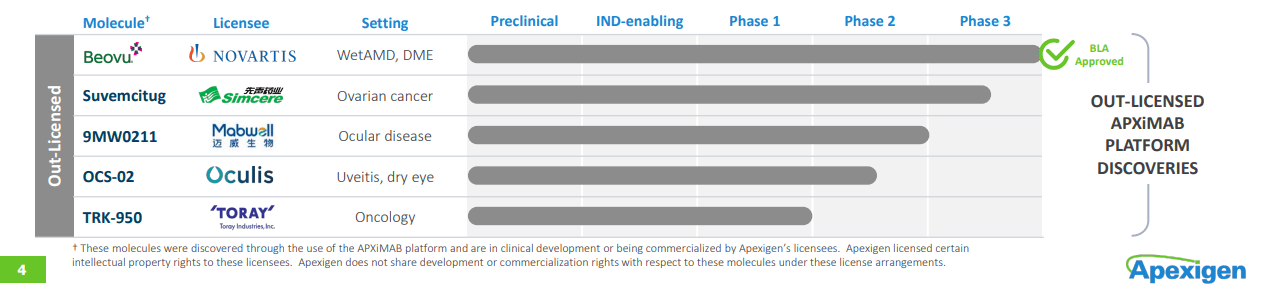

APGN also has a revenue stream from 5 antibodies it discovered using the APXiMAB platform and out-licensed.

Figure 2: APGN's out-licensed drugs. Not shown is APGN's wholly owned pipeline such as sotigalimab. (APGN Corporate Overview, January 2023)

{kind=link}

One of the out-licensed drugs was approved in 2019 called Beovu (brolucizumab) and is marketed by Novartis ( NVS ). It doesn't sound like royalties from the NVS drug, however, are worth getting too excited about.

Under this agreement, Novartis is obligated to pay us a very low single-digit royalty on net sales of the Beovu product. However, Novartis has disputed its obligation to pay us royalties on Beovu sales under this agreement. As a result, we have determined that any sales-based Beovu product royalty revenue that we may earn under this agreement is currently fully constrained. We have recorded the royalty proceeds as deferred revenue in the consolidated balance sheets. As of June 30, 2023 and December 31, 2022, deferred revenue totaled $6.7 million and $5.7 million, respectively.

Comments from APGN's 10-Q for the quarter ending June 30, 2023.

Where PYXS's Pipeline Stands Now

PYX-106 & PYX-201

At the time of my previous article, PYXS was guiding towards producing preliminary data from a phase 1 trial of PYX-201, an anti-EDB fibronectin ADC, in early 2024. With PYX-201 entering the clinic in Q1'23, that amounted to about a 12-month time frame from entering the clinic to producing preliminary data. That guidance is still in place too, there hasn't been any slippage on that timeline.

By comparison, PYX-106 was only just entering the clinic at the time of my last article, with the first subject dosing expected to occur in early Q2'23. Indeed, PYXS didn't put out a press release until May 30, noting the first patient had been dosed. Despite that, the company is guiding to preliminary data in late 2023 from PYX-106, so we are looking at only around a six to seven-month time frame from entering the clinic to producing initial data. The quick turnaround adds a catalyst to the 2023 calendar that I didn't expect.

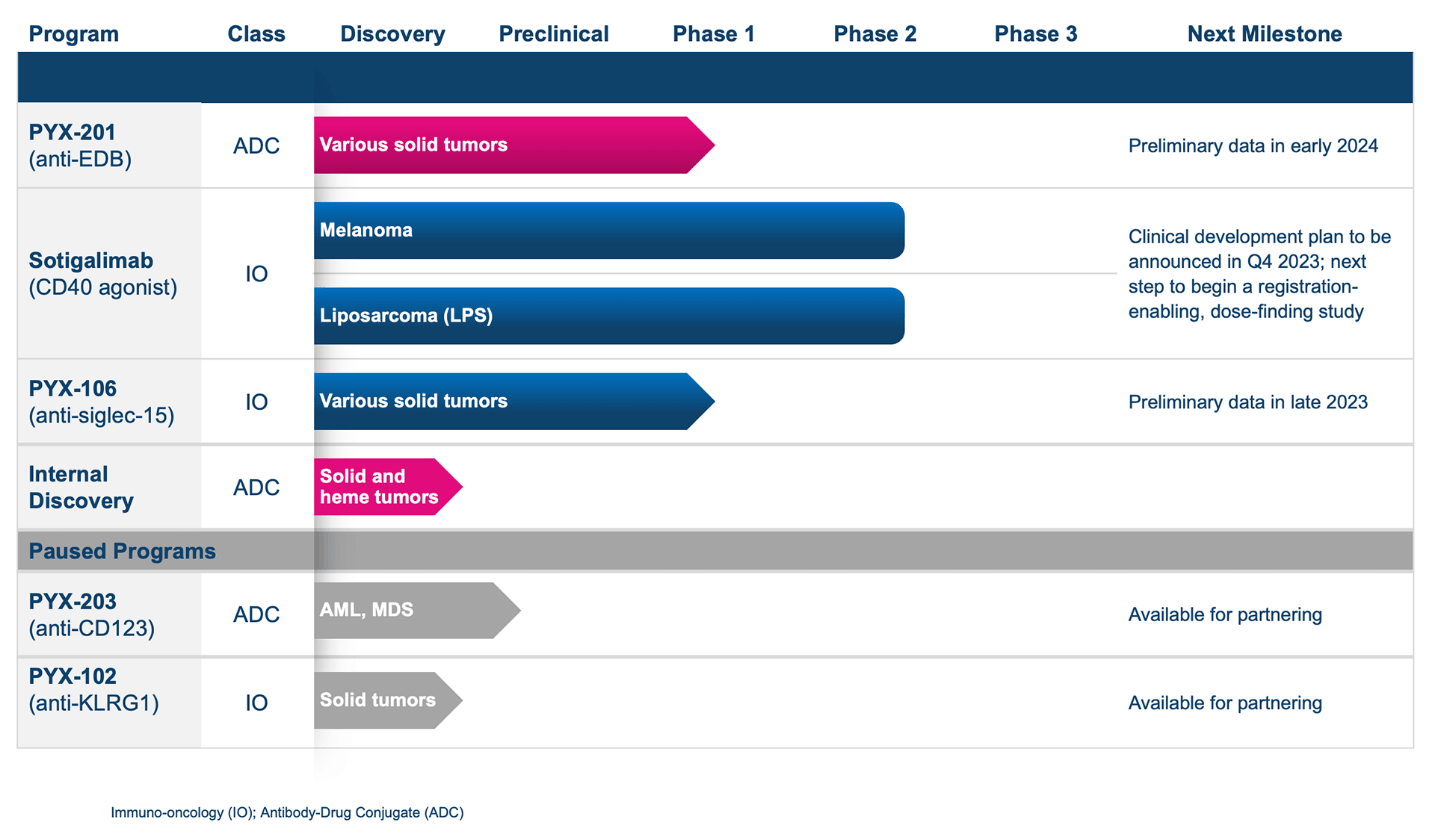

Figure 3: PYXS current pipeline. Note the addition of sotigalimab and the late 2023 timeline for PYX-106 preliminary data. (PYXS website)

{kind=link}

While we'll have to wait a little longer for something potentially market-moving from PYX-201 than PYX-106, there has been an update or two in the PYX-201 phase 1 trial. The May 30 press release noting the dosing of PYX-106 also came with news that the PYX-201 trial had progressed to the second dose. With earnings for Q2'23 , PYXS provided a further update on the phase 1 study of PYX-201, noting that the third dose cohort was now initiated. I wouldn't be surprised to see five or six-dose cohorts, but at least there haven't been any toxicity issues in the first two cohorts, even if these were only lower doses.

Sotigalimab

PYXS is waiting until Q4'23 to announce further plans for sotigalimab. It also plans to report some additional pharmacokinetic/pharmacodynamic data in Q4'23 from work with the drug. I don't think that data will be a high impact for the share price, as it doesn't sound like additional anti-tumor activity data. Further, I don't really expect a big impact on the share price of PYXS announcing exactly what it plans to do moving forward with sotigalimab.

Still, I do look forward to future work with sotigalimab given the results seen previously. Notably, previous data in melanoma show that the addition of sotigalimab to the anti-PD-1 antibody, nivolumab, in patients with progressive disease on an anti-PD-1 antibody, resulted in 5 partial responses from 33 patients. A further 10 patients achieved stable disease, with a duration of response up to 14+ months. That's certainly the type of result I think would be worth following up on. Perhaps PYXS will announce a similar trial in PD-1 refractory patients when it announces its development plan for sotigalimab in Q4'23.

Financial Overview

PYXS had cash, cash equivalents, restricted cash, and short-term investments of $144.1M at the end of Q2'23. Even considering the now inflated share count of 43,872,248 shares, PYXS is trading with a market cap of $98.3M ($2.24) per share. R&D expenses were $11.4M in Q2'23, and G&A expenses were $6.7M in the same quarter. Net loss was $15.9M in Q2'23 with net cash used in operating activities of $37.9M in the first six months of 2023. At the current rate then, PYXS could afford to go on for 18 more months until it ran out of cash. Indeed, PYXS believes current cash will last into H1'25. Even if expenses kick up, such as with further work on sotigalimab, PYXS isn't short on cash right now.

Summary and Risks

PYXS's price action following my previous article shows the potential the stock has to run. The stock went from $3.15 on the day the article was published, to a closing high of $6 in the following days. With two readouts in the period of late 2023 (PYX-106 data) to early 2024 (PYX-201), the stock has the potential to run as traders take a position. Put that with the current cash balance, and the fact the company is trading below cash, and I've rated PYXS a buy again.

There is one more catalyst this quarter to keep an eye on. While NextCure ( NXTC ) previously ceased its own clinical development of an anti-Siglec-15 antibody called NC318, the company continued to support a trial run by Yale. PYXS notes it anticipates a presentation of data from that trial in September at the International Association for the Study of Lung Cancer (IASLC) 2023 World Conference on Lung Cancer. A positive result with NC318 would reflect well on the potential of PYXS's own PYX-106, but if there is a negative result, it could read through to PYXS also, so that is one risk to consider. Of course, PYXS can claim PYX-106 offers potential advantages such as less frequent dosing and potentially higher affinity than NC318, but the market may not be convinced.

Further risks include underwhelming or outright negative data from the PYX-106 phase 1 trial, or the PYX-201 phase 1 trial. Lastly, prior to announcing data from those phase 1 trials, an issue due to toxicity could occur and this can result in clinical holds in some cases. I have no inkling currently that a toxicity issue is in play, nor do I suspect one, but it is always technically a possibility.

For further details see:

Pyxis Oncology: Catalysts Ahead, Cash In Hand And An Acquisition Completed