REIT - Real Assets: Poised To Excel In 2024

2023-12-28 06:30:00 ET

Summary

- The markets have been so fixated on forecasting a recession and ensuing rate cuts that they have ignored an abundance of data pointing to the early stages of a manufacturing-led expansion.

- It appears the market may have been mispriced amid the Federal Reserve (Fed) emphasizing price stability, a resilient U.S. economy, and rates staying higher for longer.

- Regardless of inflation’s path in 2023, we anticipate a mean reversion of returns between real assets and nominal equities, whereby the former outperforms and the latter gives up its gains.

Originally published on November 21, 2023

By May Tong, CFA, Portfolio Manager, Asset Allocation; Jessica Bush, CFA, Portfolio Manager; Ben Rotenberg, CFA, CAIA, Portfolio Manager

Real assets vs. nominal assets: Assessed through a three-dimensional lens

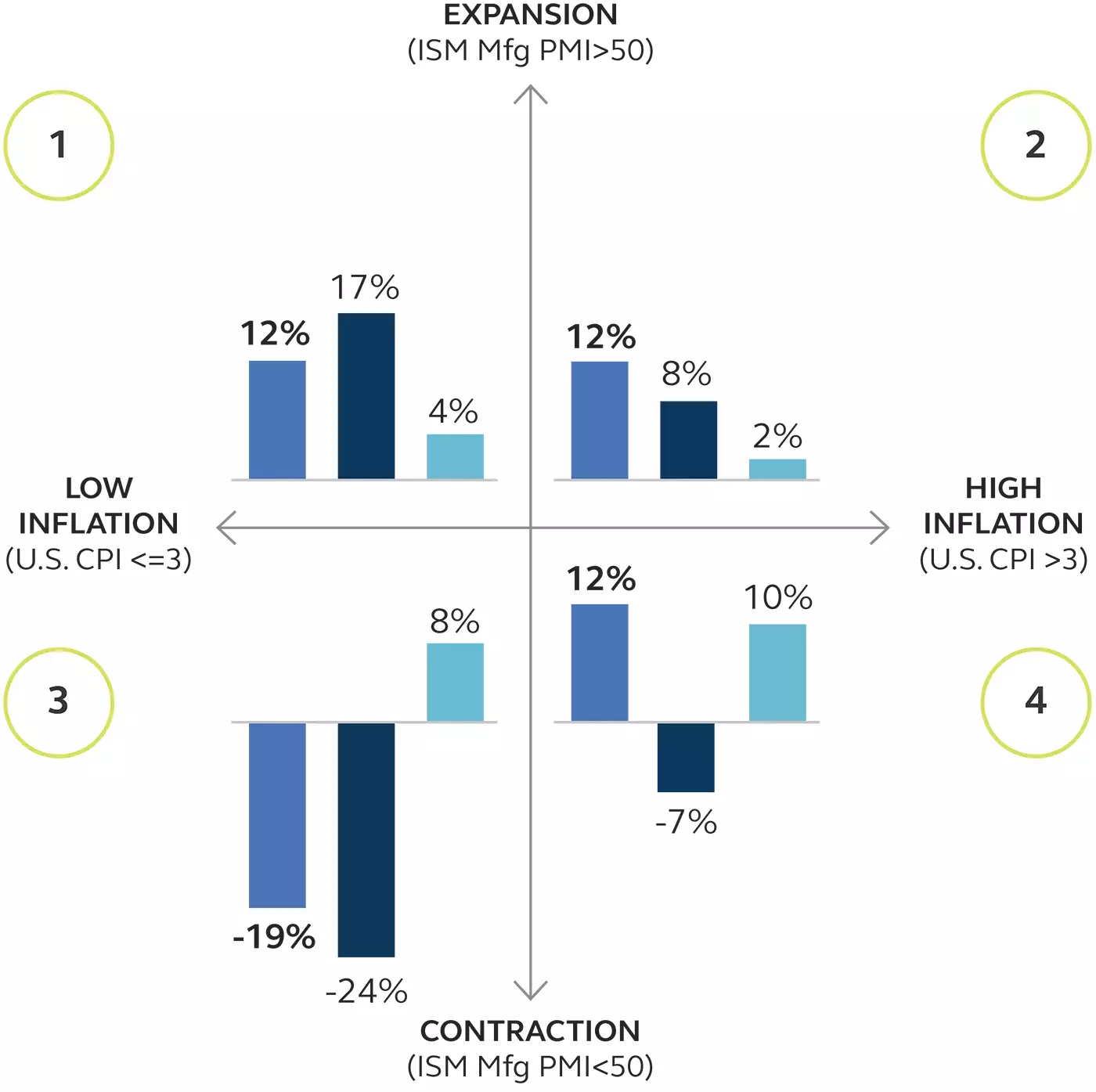

Economic growth, inflation, and interest rates are key factors in assessing the performance of real vs. nominal assets. Isolating merely one of the three variables fails to acknowledge their interplay in influencing investment returns between asset classes. As a guide for forward-looking returns, we defined eight regimes (numbered on exhibit 1) across the three variables (growth, inflation, and rates) and assessed their historical returns.

Variables

- Economic growth is measured by the ISM Manufacturing Index, also known as the Purchasing Managers’ Index (PMI).

- Expansion = PMI > 50

- Contraction = PMI <= 50

- Inflation is measured by the core U.S. Consumer Price Index (CPI).

- High inflation = CPI > 3%

- Low inflation = CPI < =3%

- Rates are measured by the Federal Funds Rate (FFR).

- Rising rates = FFR >= previous month

- Falling rates = FFR <= previous month

Exhibit 1: Three-dimensional regime analysis In 6 out of 8 regimes, real assets outperform stocks, bonds, or both.

Rising rates: Fed rate higher or equal to last month

{kind=link}

Falling rates: Fed rates lower or equal to last month

Source: As of December 31, 2022. Data since 1971. Source: Principal Global Investors. ISM Mfg PMI: Institute for Supply Management Manufacturing Purchasing Managers’ Index; an index of the prevailing direction of economic trends in manufacturing sectors consisting of a diffusion index that summarizes with a number from 0 to 100, whether market conditions, as viewed by purchasing managers, are expanding (>50), staying the same (=50), or contracting (<50). CPI: Consumer price index. Average real assets: An equal-weighted version of the S&P Global Infrastructure Index NTR (11/30/2001-12/31/2022), FTSE EPRA/NAREIT Developed Index NTR (12/31/1971-12/31/2022), Bloomberg U.S. Treasury TIPS Index (3/31/1997-12/31/2022), 15% Bloomberg Commodity Index (01/31/1971–12/31/2022), and S&P Global Natural Resources Index NTR (11/30/2002–12/31/2022). S&P 500 Index: market capitalization weighted index of 500 widely held stocks often used as a proxy for the stock market (stocks). Bloomberg U.S. Aggregate Bond Index: an unmanaged index of domestic, taxable, fixed-income securities (bonds).

Where are we now?

In 2022, markets appeared rational, having priced in the appropriate regime ( rising rates, contraction, high inflation - regime four ), with real assets outperforming nominal assets over the year. For much of 2023, however, markets have been pricing in a late stagflation regime ( falling rates, contraction, high inflation - regime eight ). In this regime, nominal assets have outpaced real assets on expectations that the Fed would cut rates, thereby leading to an outperformance of growth stocks, particularly among a narrow band of large-cap technology stocks. Amid the Fed consistently emphasizing price stability, a resilient U.S. economy, and rates staying higher for longer, has the market mispriced the likely market outlook? It is looking likely.

Where are we headed?

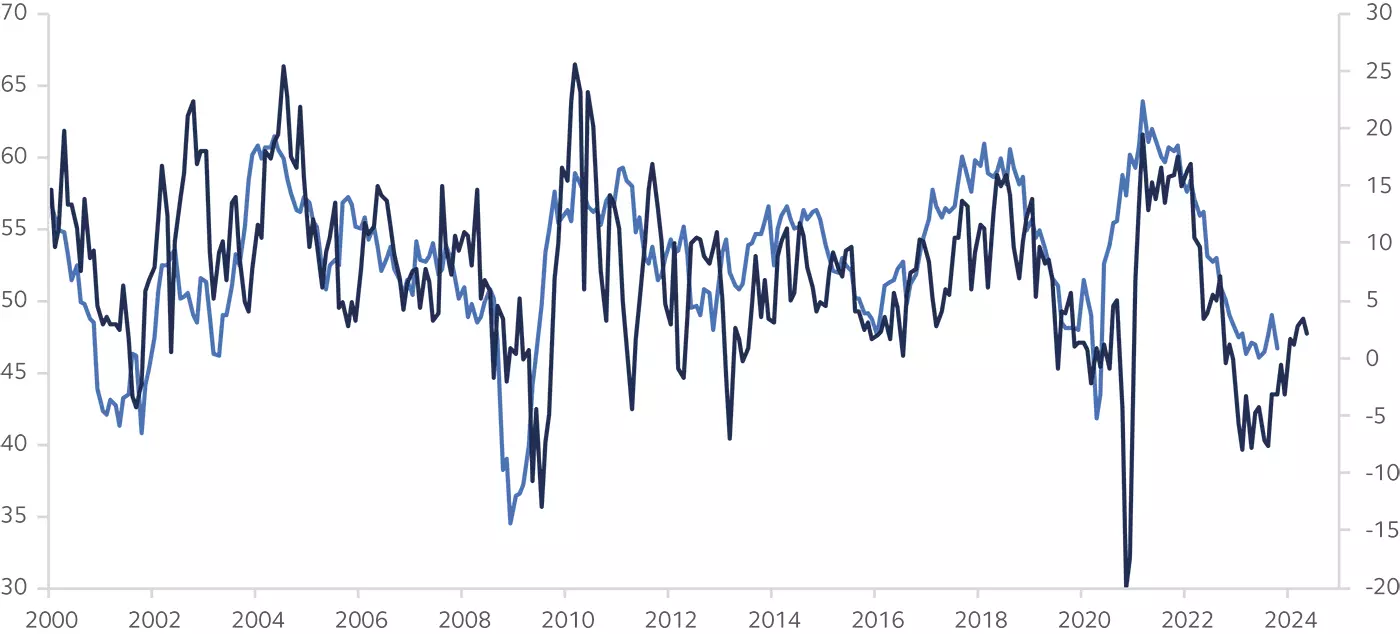

The markets have been so fixated on forecasting a recession and ensuing rate cuts that they have ignored the abundance of data pointing to the early stages of a manufacturing-led expansion. Inventory levels and manufacturing prices are two leading indicators that support this thesis (see exhibits 2 and 3).

After a buildup during COVID-19, inventory levels have been drawn down and may need replenishment. The ISM Manufacturing PMI has been hovering just below expansion territory, defined as a reading at or above 49, and could be close to a trough. This belief is supported by a notable surge in the ISM Prices Paid Index, which could lead the ISM Manufacturing PMI to above 50 in the near term.

Exhibit 2: PMI trough could be near as orders recover

{kind=link}

Source: Institute for Supply Management, Bloomberg, Principal Asset Management.

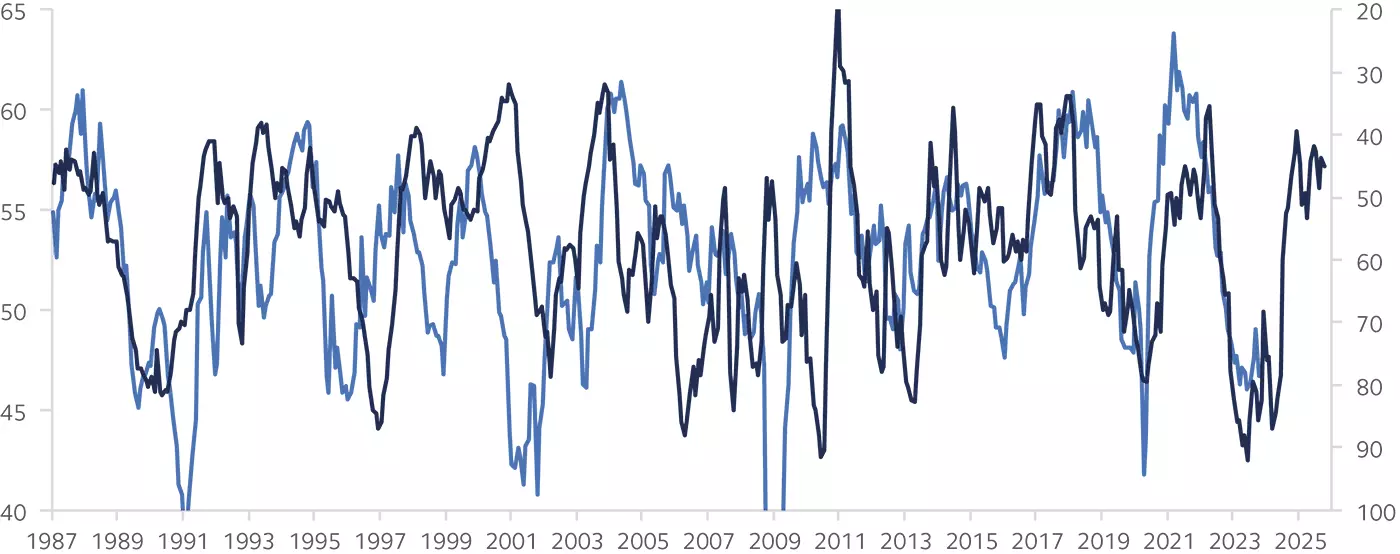

Exhibit 3: Recovery in manufacturing prices typically leads to higher output activity

{kind=link}

Note: Value of Private Construction Put in Place for Manufacturing. Monthly SAAR. Nominal spending deflated by PPI for Intermediate Demand for Materials and Components for Construction.

Source: U.S. Census Bureau, Bureau of Labor Statistics, Bloomberg, Principal Asset Management.

This manufacturing activity suggests we are in the early stages of a potentially enduring manufacturing renaissance in the U.S. that will be driven by ongoing deglobalization trends (onshoring, near-shoring) and economic incentives such as the CHIPS and Science Act and the Infrastructure Investment and Jobs Act. These incentives have catalyzed investments into U.S. manufacturing, with robust spending growing at a year-over-year pace not seen in the last two decades. Since CHIPS was signed, companies have announced more than $166B in plans for new U.S. manufacturing facilities for semiconductors and electronics. 1 Along with the deglobalization tailwinds supporting manufacturing and decarbonization initiatives - such as those supported by the Inflation Reduction Act - have provided incentives for U.S. manufacturers to invest and build new clean energy facilities to produce solar panels, wind turbines, battery storage technologies, and other green energy projects. Exhibit 4 highlights the significant boost in manufacturing construction spending that the policies have triggered.

Exhibit 4: Real total manufacturing construction spending

{kind=link}

Source: Institute for Supply Management, Bloomberg, Principal Asset Management.

Investment takeaway

As the manufacturing renaissance takes hold, we believe we may be entering the early stages of a higher growth and elevated rates backdrop. Whether inflation reverts to the Fed’s target of 2% or remains structurally higher, we anticipate a mean reversion of returns between real assets and nominal equities, whereby the former outperforms, and the latter gives up its gains.

_____________

1 Fact Sheet: One Year after the CHIPS and Science Act, Biden-?Harris Administration Marks Historic Progress in Bringing Semiconductor Supply Chains Home, Supporting Innovation, and Protecting National Security, 2023

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Real Assets: Poised To Excel In 2024