WBA - Realty Income Corporation: My Dollar Store Darling

2023-05-05 14:29:14 ET

Summary

- Realty Income Corporation tenants are uniquely set up to bear the brunt of any prolonged recession, possibly increasing their revenue.

- Realty Income stock looks cheap on a modified Graham Number basis, and the monthly dividend yield is now higher than the risk-free rate.

- Realty Income Corporation is also one of the highest yielding dividend aristocrats. There are only three REITs on the list, along with Federal Realty Investment Trust and Essex Property Trust.

Recession proof tenants

When looking for real estate investment trusts ("REITS") and income stocks in an environment where the cost of capital is rising by the month, the quality and resiliency of a business in the face of a poor economy are paramount. Realty Income Corporation ( O ) stands above the rest, and for good reason. Having written about O back in October 2022, the thesis seems to be strengthening and the price has been flat. I am buying this stock again as it has traded flat since last year, all the while the AFFO (adjusted funds from operations) and dividend yield have been on the up and up.

The tenants are my favorite part about Realty Income. It has a beautiful stable of Dollar, grocery, and convenience stores. This is right where I want to be if we hit a recession.

Recent earnings trends

Recent earnings trends from the May 4th call saw Realty Income miss on the top line by $883 million. It met expectations on the bottom line EPS at $.34 a share and delivered AFFO per share of $0.98. Here are some highlights from the most recent earnings call with quotes from CEO Sumit Roy and CFO Christie Kelly:

- Agreed to acquire up to 415 high-quality convenience stores from EG Group for $1.5 billion. Over 80% of this total portfolio annualized contractual rent is expected to be generated from properties under the Cumberland Farms brand

- This quarter, the company took advantage of favorable pricing internationally to acquire properties worth approximately $390 million at an initial cash lease yield of 7.6%

- For the first quarter, occupancy was 99%, matching last quarter for the highest rate at the end of a reporting period in over 20 years.

- Additionally, there was a 101.7% recapture rate across 176 renewed or new leases executed during the quarter.

- Despite continued market volatility, the company raised approximately $3.9 billion of capital this year excluding $1.5 billion of unsettled forward equity. In April, it closed a $1 billion bond offering, which was comprised of $400 million of 4.7% senior unsecured notes due in 2028 and $600 million of 4.9% senior unsecured notes due in 2033, resulting in a weighted average tenure of eight years and semi-annual yield to maturity of 5.05%. The issuance allowed Realty Income to satisfy near-term debt issuance needs while reducing exposure to variable rate revolver and commercial paper borrowings and to almost zero after a transaction closed on April 14.

- In March, it increased the dividend for the 120th time since public listing in 1994, to an annual rate of $3.06 per share, representing 3.2% growth from the prior year period.

The call highlighted some headwinds due to rates creating a $.02 a share headwind with their commercial borrowing up 300 basis points. Even with that in mind, they were able to close new debt with a semi-annual yield to maturity at 5.05%. That is an amazing rate during this era of rising interest rates. Try getting that on a mortgage as a first-time home buyer, investor or on a construction loan as a developer. Won't happen.

This speaks to the high-quality credit rating of Realty Income Corporation and its access to cheap capital. That was the most positive part of the call, especially the 8-year maturity date locking in at 5.05%. With new cash lease yield acquisitions above 7% and new building cap rates in that same territory, there are still about 200 basis points in spread or more to be had.

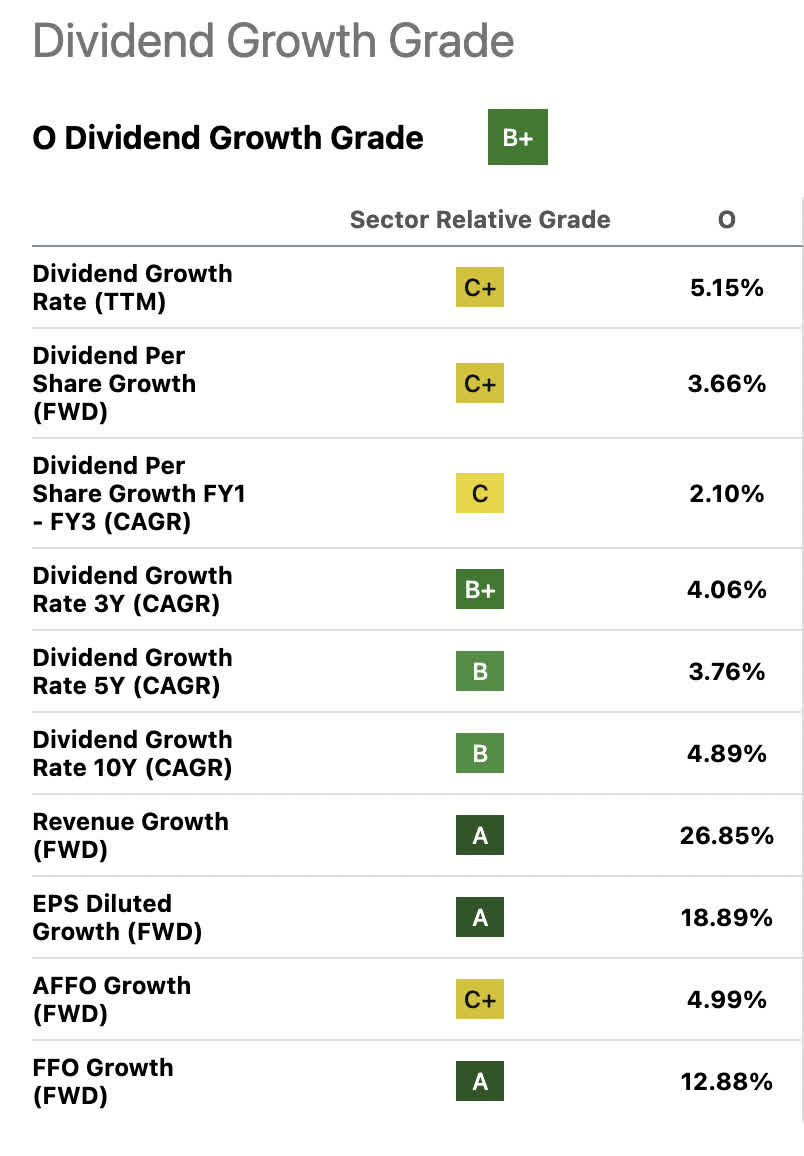

Look at that dividend yield

Hunting for stocks that both grow their yield and exceed the risk-free rate is not an easy task. High-yield FDIC-insured savings accounts and money market funds are throwing off somewhere in the neighborhood of 4.5+%. Not only is Realty Income Corporation at least matching that, their growth rate and frequency of compounding, which match the monthly compounding of an HYSA, are a great alternative that should be beating the risk-free rate in the not-too-distant future.

With the projected forward yield at a tad over 5%, we're getting Realty Income at just about the top of its trailing 10-year average. 2009 saw some amazing yields with the previous banking crisis, briefly touching 10%. All the while, the dividend per share has just kept marching upwards.

{kind=link}

AFFO growth is slated to nearly match the per share dividend growth. Not quite beating inflation at this point, but should be in the near future if the Fed starts hitting its targets.

Modified Graham Number

A value bucket I use for companies with large amounts of tangible assets is the Graham Number. Recommended by Benjamin Graham in the original version of The Intelligent Investor , it advises us not to pay more for a stock than the price at which the price-to-earnings multiple times the price-to-book multiple crosses 22.5. Getting a quick price target simply requires the square root of the book value per share X your desired earnings metric per share X 22.5. In stocks that trade on GAAP multiples, GAAP EPS is used; as the REIT industry trades on an AFFO/Share basis, this is the more appropriate multiple to use here.

Based on book value and AFFO/share

| Book Value |

| $43.46 |

| Graham Number |

| AFFO/Share |

| $3.93 |

| $62 |

Based on NAV adjusted for depreciation and AFFO/share

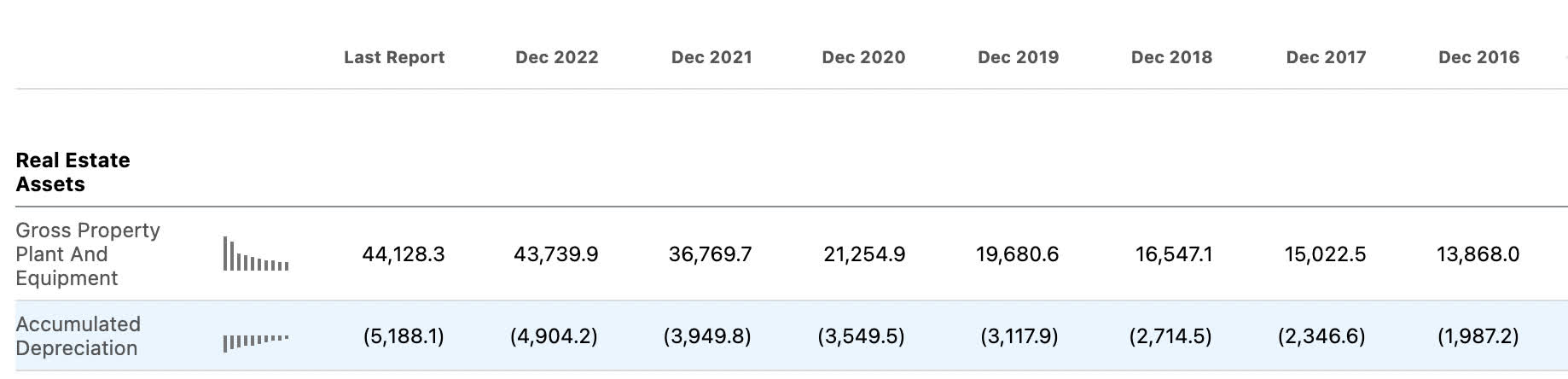

Using NAV with depreciation added back in versus book value, which records value at cost minus accumulated depreciation, is valid and would result in a higher number which can add back at least $5.188 billion on this basis. Some may also appraise the market value of properties that have appreciated more than their accumulated depreciation differential to cost based on cash flow and cap rates. However, as CRE values are interest rate sensitive, the most I would consider in this environment is cost plus accumulated depreciation, being ultra-conservative when shooting for a high figure.

{kind=link}

At $5.188 Billion in accumulated depreciation and 637 million shares outstanding, this would add another $8.14 a share to the book value equation. That would alter the price target upwards to $67.67 a share with a modified book value of $51.80 a share.

The portfolio

realtyincome.com/our-portfolio

{kind=link}

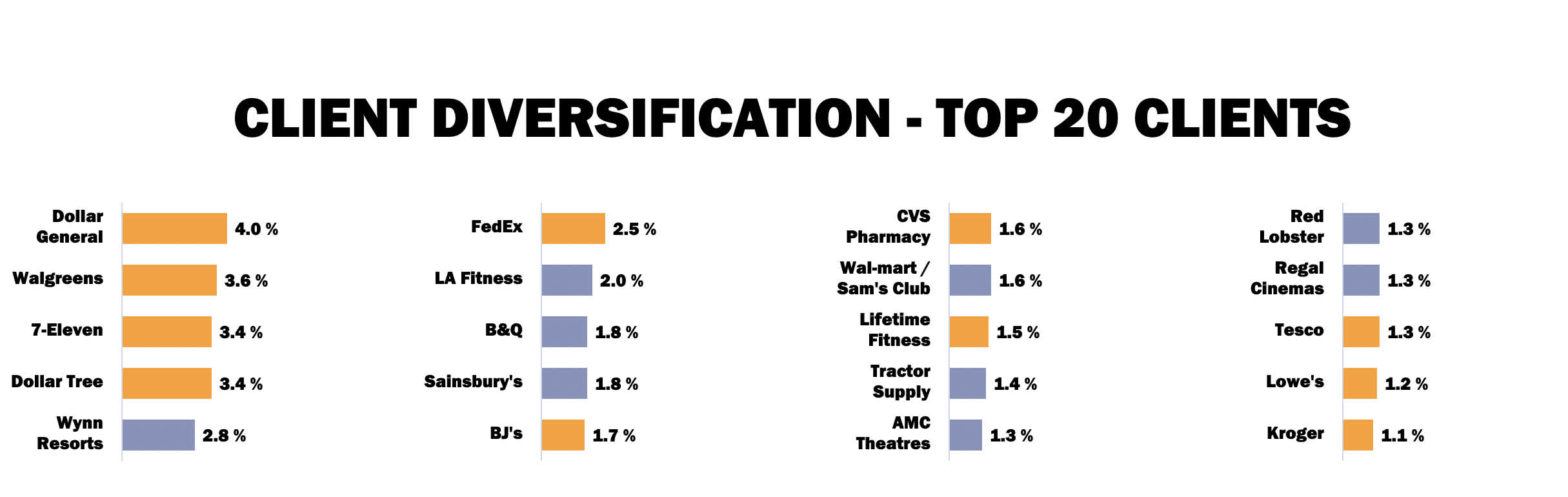

- Dollar stores Dollar Tree ( DLTR ) and Dollar General ( DG ) represent 7.4%

- Walmart ( WMT ), 7-Eleven, CVS ( CVS ), Walgreens ( WBA ), Tesco ( TSCDF ) and Kroger ( KR ) represent 16.0%

That's 23.4% of the portfolio that I would label A+ recession-proof tenants that are either anchor tenants themselves or could function without an anchor. These are tenants that I would expect would not only be resilient but even increase their revenue as times get tougher and credit starts to pinch the consumer more and more every day.

realtyincome.com/our-portfolio

{kind=link}

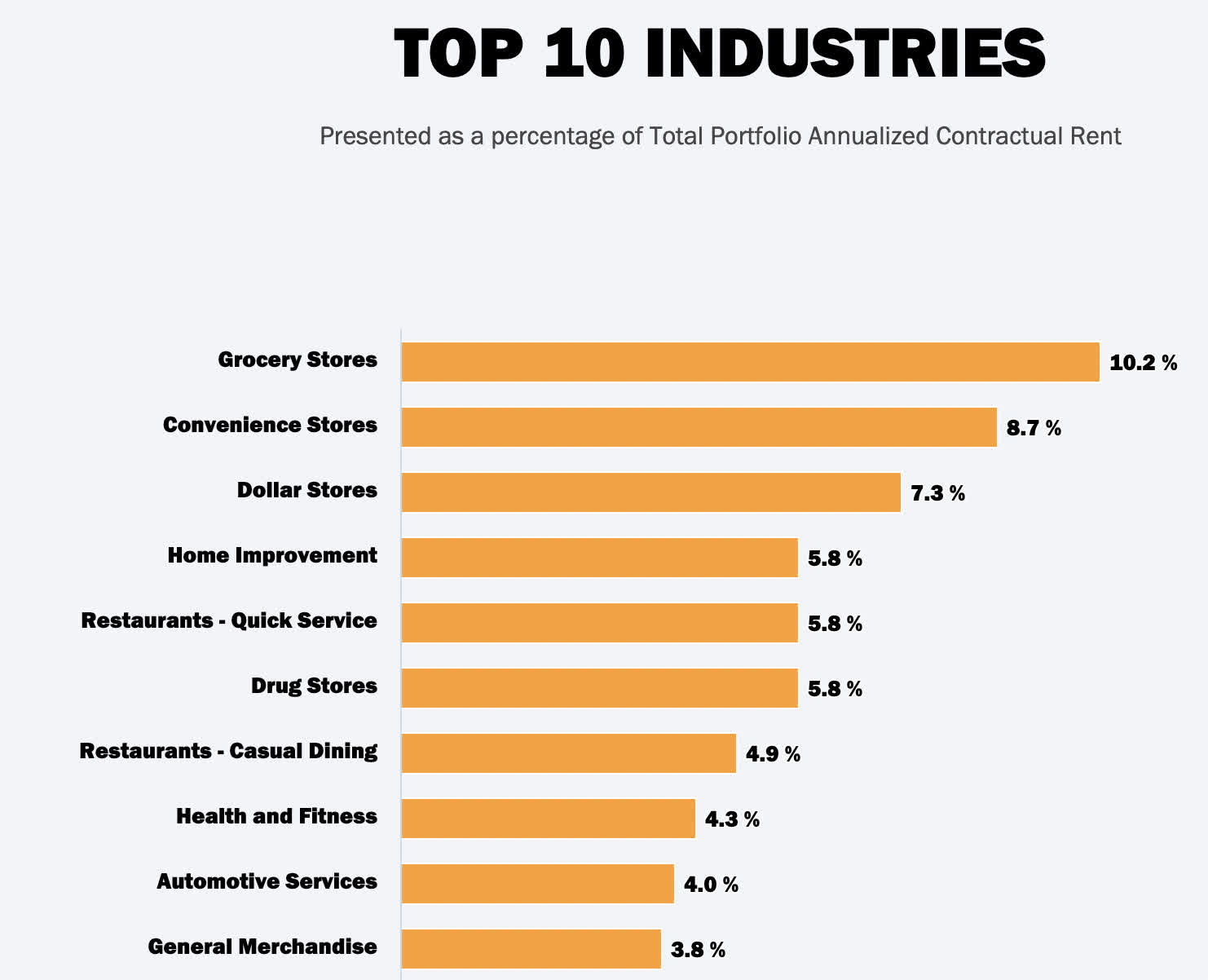

Regardless of the tenants in this top 10 industry makeup, these are exactly the sectors of commercial real estate I would be looking to in an environment where I am becoming more defensive by the day. Steering clear of office is a no-brainer at this point. I could even imagine some primo strip mall deals coming up that Realty Income Corp could help a major partner slip into. The Dollar Stores are especially ripe for expansion.

According to the most recent 10K , Realty Income Corporation boasts the following:

At December 31, 2022, our diversified portfolio consisted of:

• Owned or held interests in 12,237 properties;

• An occupancy rate of 99.0%, or 12,111 properties leased and 126 properties available for lease or sale;

• Clients doing business in 84 separate industries; • Locations in all 50 United States ("U.S."), Puerto Rico, the United Kingdom ("U.K."), Spain, and Italy;

• Approximately 236.8 million square feet of leasable space;

• A weighted average remaining lease term (excluding rights to extend a lease at the option of our client) of approximately 9.5 years; and

• An average leasable space per property of approximately 19,350 square feet, approximately 13,000 square feet per retail property and approximately 234,100 square feet per industrial property.

Of the 12,237 properties in the portfolio at December 31, 2022, 12,018, or 98.2%, are single-client properties, of which 11,894 were leased, and the remaining are multi-client properties.

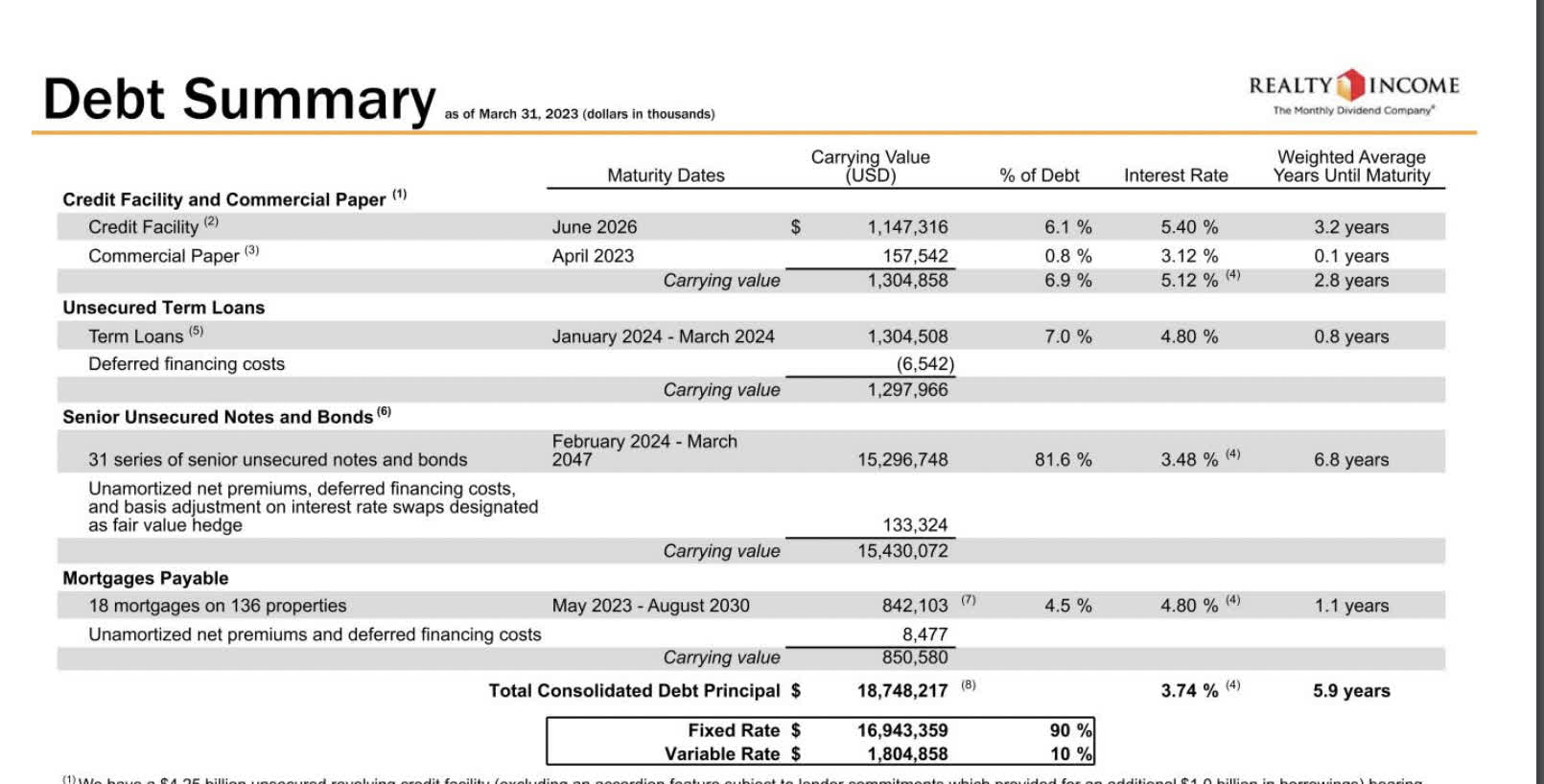

Debt maturities

{kind=link}

At 90% fixed rate debt and a 5.9-year average weighted maturity, this is a nice runway to get beyond this stretch. With the majority of debt, 81.6% of it in multiple series of unsecured notes and bonds maturing between February 2024 and March 2047, and an average length of 6.8 years, the debt schedule for Realty Income Corporation is not all that foreboding.

Risks

Growth. REITS can get growth through rent increases and growth through acquisitions. Although the maturity schedule of their trailing debt looks pretty good, they will certainly need some forward debt to grow the business in addition to increasing the float. If the WACC skews harder towards issuing equity versus debt when evaluating the cost of capital versus the returns, we could see larger-than-average dilutions all across the REIT industry. Here's hoping Realty Income Corporation will be more resilient in this aspect, but nothing is guaranteed.

Catalysts

Rate cuts. If the FED cuts rates next year or even by the end of this year, this should have a stronger-than-average effect on the profitability of REITS versus other sectors. Tech, which is considered long duration, will be the other beneficiary. Cutting rates before 2025 seems to be the consensus, and the consensus says that it would need to be done dramatically, with many 10-year CRE maturities coming due by then.

Summary

With a dividend yield now at the top of its 10-year average and a price that is only about 1.5 X the asset value, depending on how you want to slice it, the Realty Income Corporation price seems attractive. I am accumulating here under the assumption that the yield will exceed the risk-free rate within 24 months and keep surpassing it thereafter based on my cost of acquisition. This dividend aristocrat is down nearly 10% YTD and I have started adding monthly. Buy Realty Income Corporation stock with a target of $62 on the low end and $67 on the high end.

For further details see:

Realty Income Corporation: My Dollar Store Darling