WAL - Recession Watch: A Mild Recession Is Likely Starting In July 2023

2023-05-13 07:00:00 ET

Summary

- Inflation remains stuck around 5%.

- The Fed has paused unless inflation remains stuck, then the Fed might keep hiking.

- The banking crisis is contained to relatively small banks that don't threaten another Great Financial Crisis.

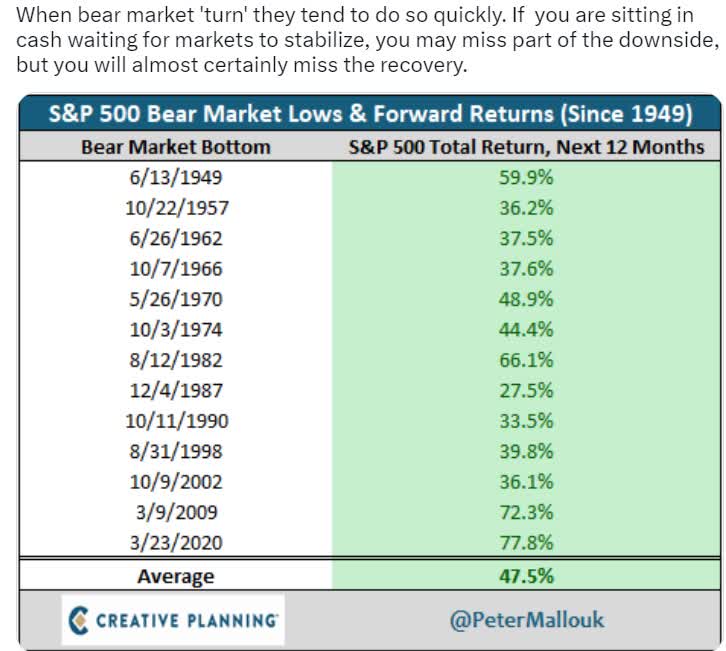

- The economic data confirms what the Fed, economists, bond market, CEOs, and Warren Buffett expect, a mild recession is likely starting in about 1 to 2 months.

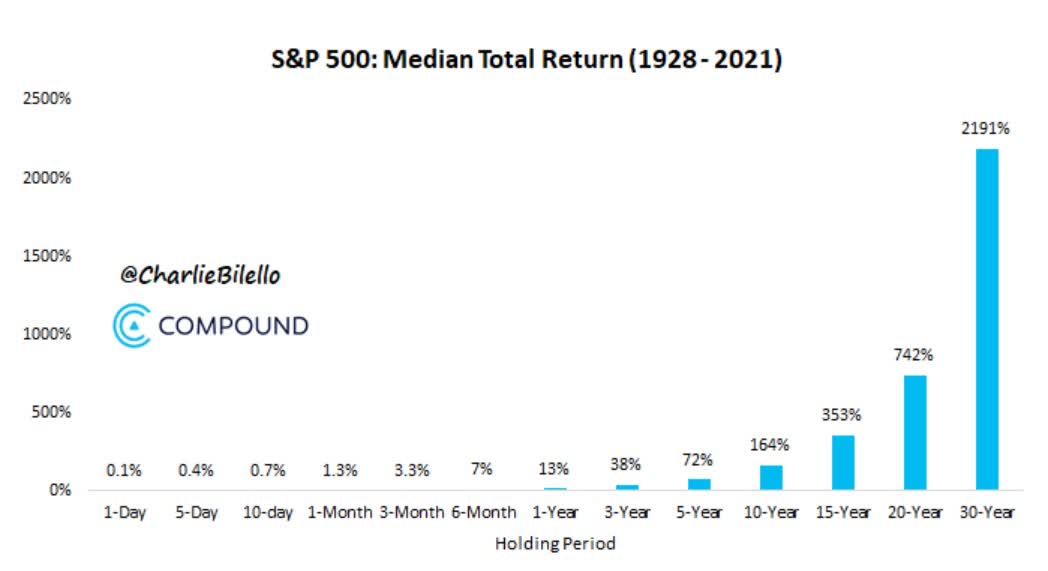

- The stock market is likely to fall 17% to 33%, possibly during the looming debt ceiling showdown (June 1st). A diversified blue-chip portfolio can not just help you enjoy 64% smaller declines in crashing markets, but preserve and grow your income throughout a recession, and profit from rebalancing bonds and hedges into blue-chips at the best valuations in years or decades.

This article was coproduced with Dividend Sensei.

The goal of these Recession watch updates isn't to help you time the market, because even perfect economic timing can't do that.

{kind=link}

And even perfect economic timing isn't enough to beat buy-and-hold blue-chip investing over the long term.

Rather our goal is to help our members get the best "big picture" view of what's going on with the economy, so they can avoid panic selling at the worst possible time.

That's so you can profit from the incredible blue-chip bargains we have today and the better ones that might or might not be coming in the next few weeks and months.

{kind=link}

That way, you can harness the incredible income and wealth-compounding power of blue-chip dividend stocks to make your financial dreams come true.

{kind=link}

We want to help you stay calm and rational through the dark times, so you can enjoy the face-ripping bull market rally that's likely starting at the end of 2023.

We're in the process of getting a new video editor. Until then, I must paste the raw video files, and time stamps won't be available.

Inflation Watch

Inflation has been the #1 concern for over a year, and despite the banking turmoil and highest volatility in bond yields since 2009, it remains a top concern today.

{kind=link}

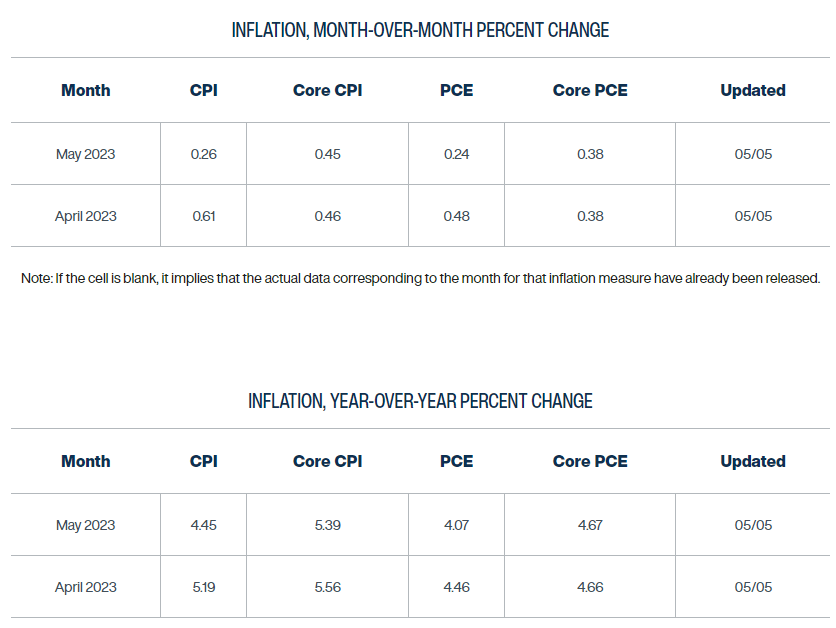

The Cleveland Fed expects core Personal Consumption Expenditures, or PCE price index, the Fed's official inflation gauge, to remain stuck at 4.7% at the end of June.

It's been 4.6% to 4.7% for the last 3 months.

CPI (Consumer Price Index) inflation is expected to print 5.2% on Wed, May 10th, up from 5% in April.

Next month it's expected to fall to 4.5%, but core CPI (ex-food and fuel) is expected to come in at 5.4%, down a bit from 5.6% in April.

Month-over-month is more important than Year-over-year and can tell you what inflation is running in real time.

The Cleveland Fed expects core PCE to remain 0.4% (4.9% annualized) through the end of June.

It expects core CPI to remain 0.45% or 5.5% annualized through June.

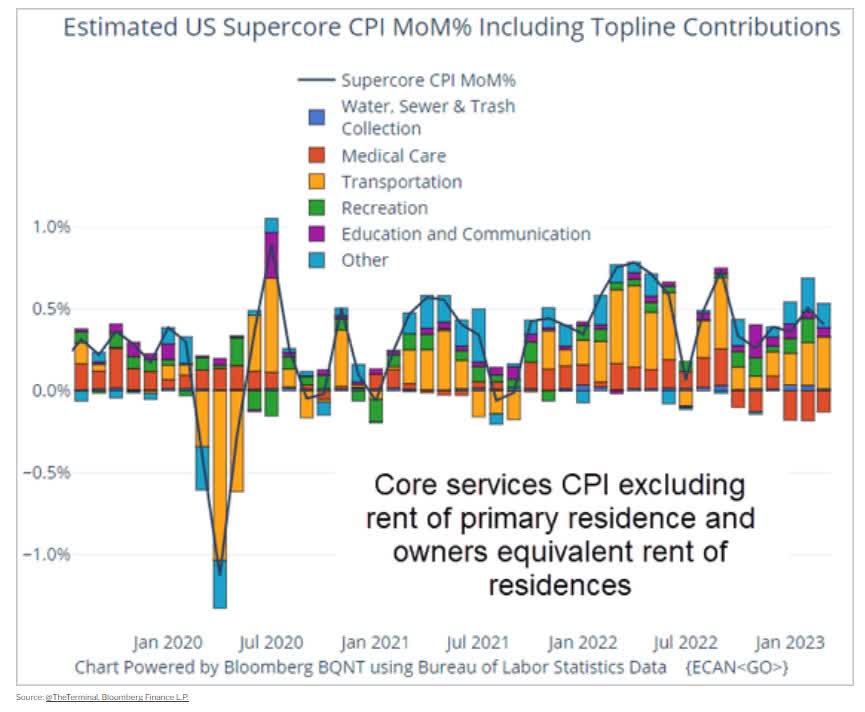

Super Core (services ex housing) inflation remains stuck at 5.5%.

{kind=link}

Annualized super core inflation has remained around 5.5% since January 2021.

Why is inflation proving so stubborn?

{kind=link}

The U.S. jobs market is proving unsinkable so far, courtesy of a 1 million job shortage created by the Pandemic.

- all services jobs

- 70% of service inflation is wage driven.

The latest jobs report showed 253K jobs created, compared to 180K expected.

Wage growth was expected to be 4.2% YOY and came in 4.4%.

Non-supervisory wages (80% of workers) rose 4.8% YOY.

Month-over-month wage growth accelerated to 0.5%, or 6.3% annualized.

That's consistent with 4.8% long-term inflation, according to the Fed and Moody's.

And guess what inflation appears stuck at? Around 5%.

The only weakness in the jobs report was a 149,000 downward revision to the previous two months' reports.

- February from +326,000 to +248,000

- March from +236,000 to +165,000

- April 253,000 (first estimate).

That's a three-month rolling average of 222,000 wage growth compared to 163,000 pre-pandemic when we were at 3.5% unemployment.

65% of the economy is consumer spending, and wages drive 70% of consumer spending.

As long as people keep their jobs and their wages are rising, they will keep spending.

The highest wage growth is in the lowest-earning industries, such as leisure and hospitality, where wage growth is running around 15% on an annualized basis.

- the lowest-income Americans are seeing the strongest wage growth

- and low-income households spend almost all of their income.

This is why the U.S. economy remains so resilient in the face of incredible headwinds.

Fed Watch

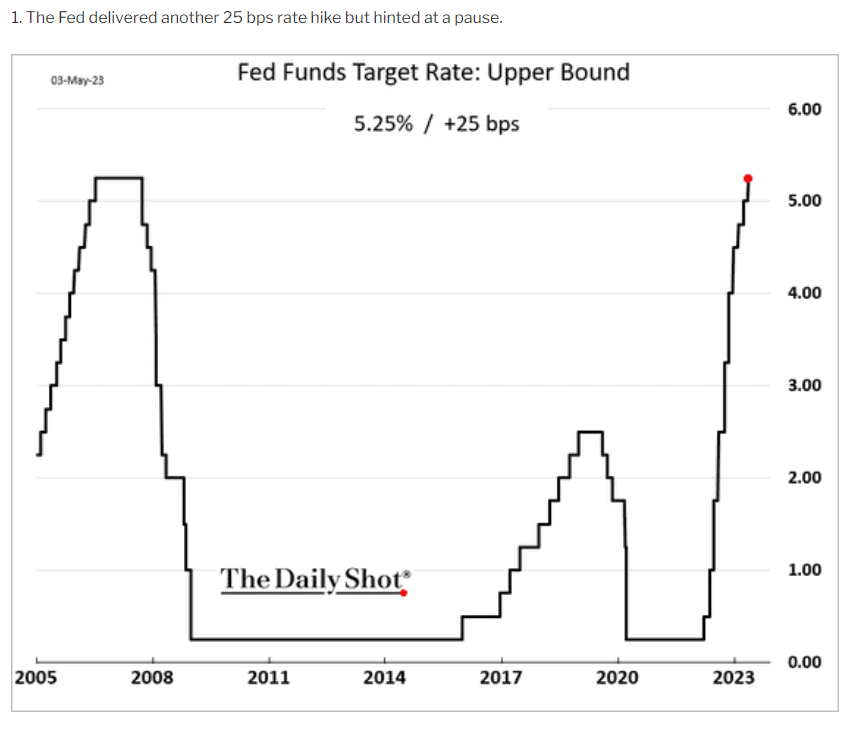

The Fed hiked to 5% last week, exactly as expected.

{kind=link}

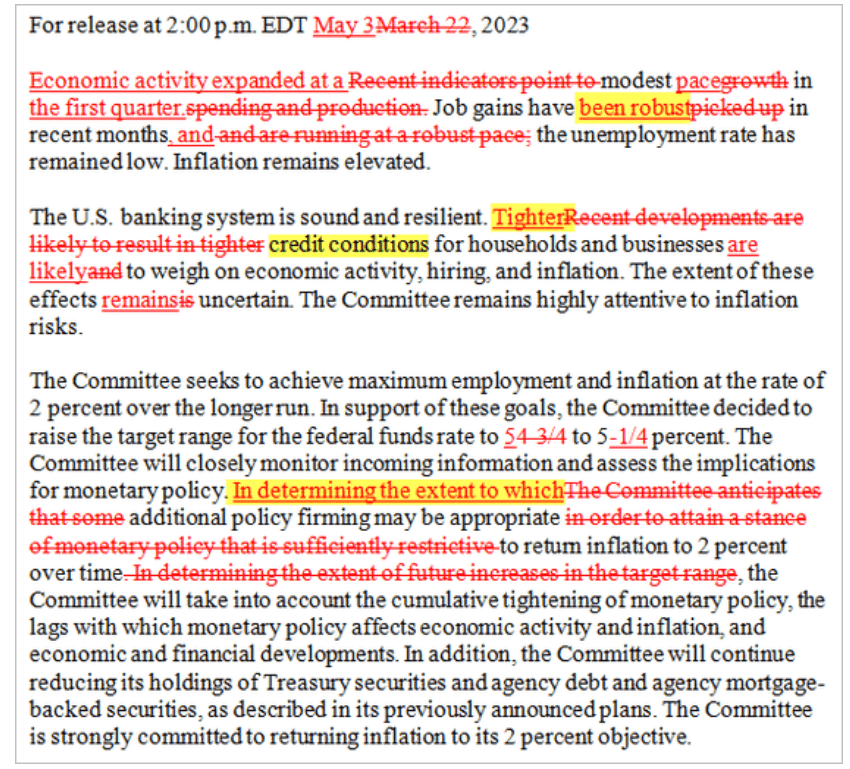

And the Fed also changed its statement language to signal a conditional pause.

{kind=link}

If and only if core inflation is falling steadily is the Fed actually done.

{kind=link}

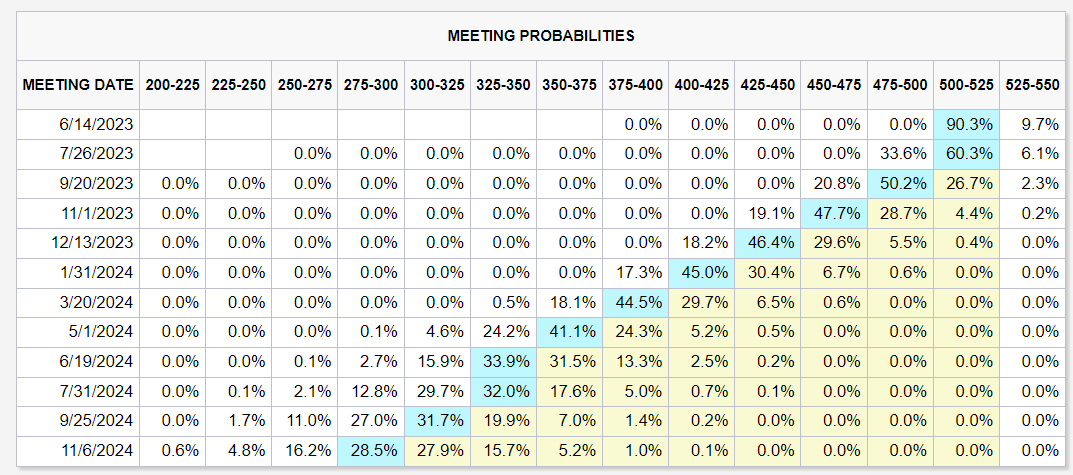

The bond market is convinced a recession is imminent, and the Fed will cut three times this year.

The Fed says it has no plans to cut this year, which the bond market thinks is a 0.4% probability.

The current data says the bond market is wrong and the Fed might hike once or twice more.

In fact, Citigroup's base-case is that the Fed will hike 25 in June, and 25 in July to 5.5% to 5.75%.

Neel Kashkari, President of the Minneapolis Fed, thinks 5.5% is an appropriate terminal rate.

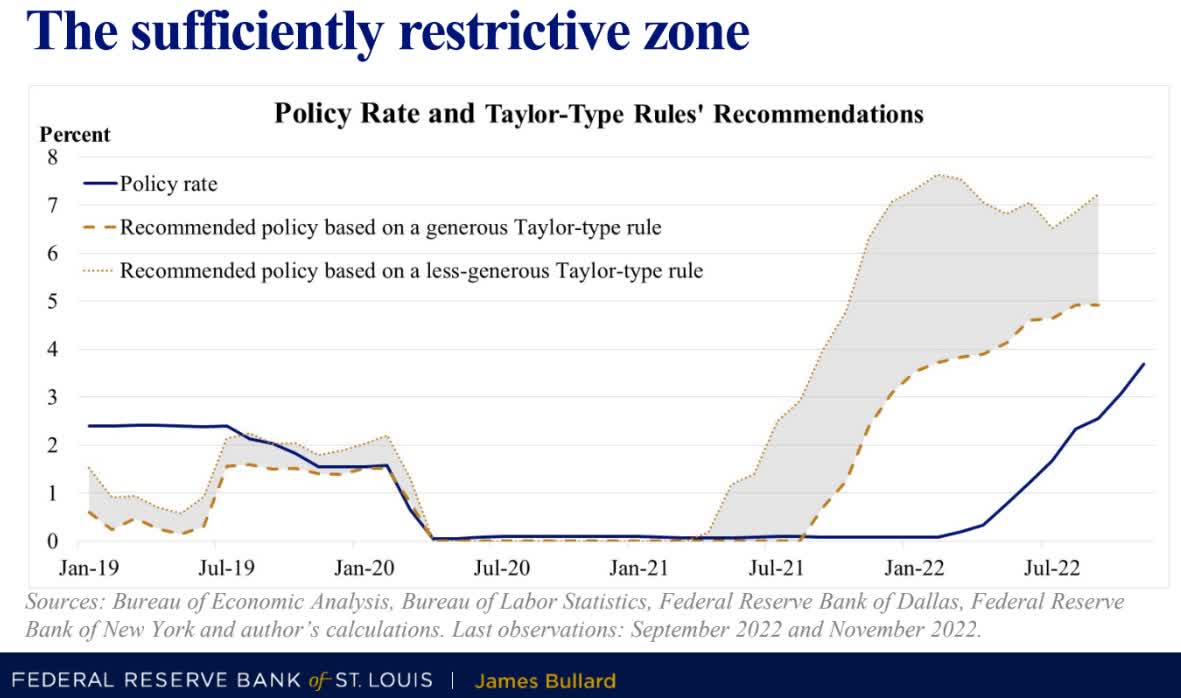

St. Louis Fed President Bullard thinks if inflation remains stuck at these levels, the Fed might have to go to 6% to 7%.

Federal Reserve Bank of St. Louis

{kind=link}

And the actual economic data says the Fed isn't restrictive, just maybe close to neutral.

{kind=link}

What about the banking crisis? And QT (reverse money printing)? Doesn't that effectively increase the Fed funds rate?

- Goldman and JPMorgan estimate the regional banking crisis adds 0.5% to the Fed funds rate

- The Atlanta Fed estimates QT adds 0.75%

- San Francisco Fed estimates QT adds 2%.

So effectively, the Fed funds rate is actually 6.25% to 7.25% right now, which means the Fed is right to pause...but not cut.

This is what the Fed is trying to prevent.

{kind=link}

If the Fed pivots too early, as it did three times in the 1970s and twice in the early 1980s, it risks a double-top inflation scenario that could result in 11% to 12% inflation, double-digit Fed funds rate, and a severe recession that results in over 8 million job losses.

- and a 50% stock market crash

- and a lost decade for stocks.

Financial Crisis Watch

JPMorgan Chase & Co. (JPM) acquired last week First Republic Bank (FRCB) in a sweetheart deal in which:

- JPM paid the FDIC $10.8 billion for FRC

- The government gave JPM a $50 billion line of credit

- and covered 80% of loan losses for the next five years

- JPM estimates it will make about $2.6 billion on the deal.

The FDIC saves about $13 billion on the deal, and FRC customers are protected from any deposit losses.

- FRC bond investors take a steep haircut

- FRC stock investors get wiped out.

PacWest Bancorp ( PACW ) then triggered more market mayhem when, about 30 minutes after Jerome Powell said the banking system was safe, it plunged 55%.

- news that it's looking to sell itself.

Is PACW the next SVB Financial Group (SIVBQ) or FRC? Yes and no.

Unlike SVB, which was 93% uninsured deposits, and FRC (67%), which mostly banked tech startups and rich people, PACW's deposits are fine.

- average FRC checking account balance: $2 million

- average SVB checking account balance: $4.5 million.

PACW's deposits are 77% insured.

And its liquidity is enough to cover 188% of its deposits.

- PACW is incapable of dying the way SVB or FRC did

- via bankrun on deposits.

So, why is PACW looking to sell itself?

PACW was founded in 1999 in Beverly Hills and is mostly focused on Los Angeles businesses.

In 22 years, it generated $3 billion in cumulative profits.

And then, in Q1, it lost $1.2 billion, an annualized rate of $5 billion.

PACW's issues aren't bad loans (not yet at least) or a run on the bank by rich clients worried about losing their deposits.

It's due to the Fed hiking rates by 5% in just over a year and putting the bank's business model underwater.

At the current rate of losses, PACW will fail within six months.

Western Alliance Bancorporation ( WAL ) also triggered some drama last week. It fell as much as 62% in a day when the Financial Times reported it, too, was trying to sell itself.

- management came out and said this was 100% false.

WAL is actually still profitable, and about 78% of deposits are insured.

Unlike PACW, it's profitable. But Moody's downgraded them two notches from BBB to BB+.

In order to reduce its now elevated reliance on higher-cost market funds, Western Alliance is in the midst of a material balance sheet repositioning that includes the disposition of significant loans and other assets. Favorably, management already completed $1.7 billion of sales in Q1 2023, which included $0.9 billion of loan sales, with the sale of securities and mortgage servicing rights accounting for the remainder. In addition, $6.0 billion of held-for-investment loans, about 12% of the year-end 2022 balance, were reclassified to held-for-sale in Q1 2023.

In announcing its earnings on 18 April, management indicated that $3.0 billion of the held-for-sale loans are already contracted for sale and expected to close in Q2 2023, with a disposition of the remaining $3.0 billion earlier in the sales process. If successful, the additional loan sales will reduce Western Alliance's use of market funding and strengthen its capital metrics." - Moody's.

Moody's is worried that asset sales at a loss could significantly weaken WAL's capital buffers.

Western Alliance's CRE portfolio accounted for 2.6 times Moody's tangible common equity ((TCE)) as of 31 December 2022, which Moody's views as a high concentration. The bank also has sizeable exposure to the riskier construction sector accounting for 0.8 times Moody's TCE at year-end 2022." - Moody's.

Moody's is also worried about WAL's high exposure to commercial real estate, which is the next shoe to drop in the banking crisis.

{kind=link}

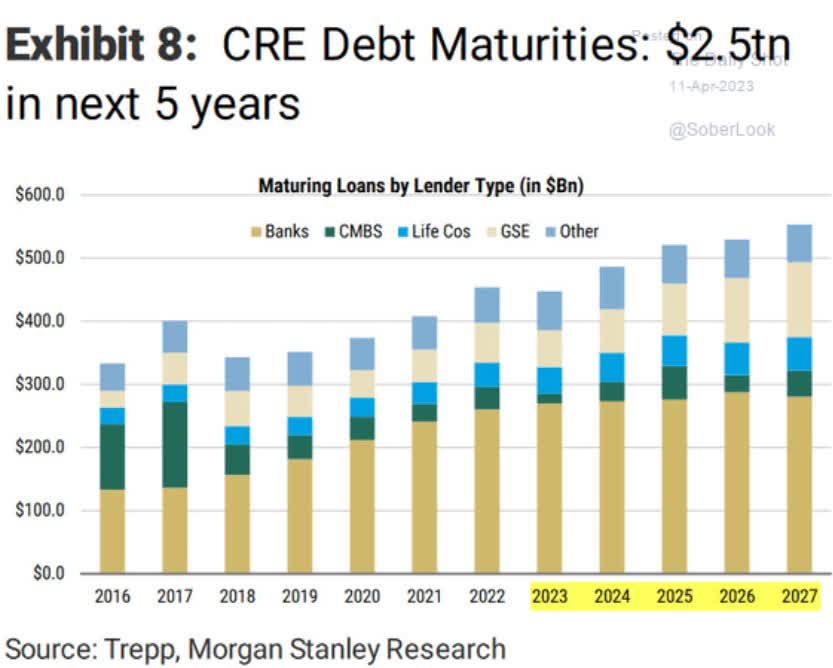

$500 billion in commercial mortgages are maturing in 2023 and the Fed says it will keep rates at 5% (at least).

Much higher borrowing costs on the refinanced debt, combined with much higher vacancy rates for office properties, is why BX, BAM, and PGIM (Prudential's asset management arm) have defaulted on some large office properties in Los Angeles.

The NYT estimates that a 10% to 20% default rate on commercial mortgages is possible in the coming recession (similar to the Great Recession).

That means $80 to $160 billion in loan losses for banks.

Regional banks are 67% of commercial real estate lending in the U.S., so around $80 billion in regional banking losses from real estate might be coming soon.

{kind=link}

In the last year, the 143 largest regional banks had $62 billion in profits, so we're potentially looking at a lot more bank failures in the coming months.

How many? A study from Stanford estimates that just over 50% of U.S. banks are insolvent if they had to sell 100% of assets right now.

- about $620 billion in unrealized bond losses

- courtesy of the Fed requiring banks to buy bonds and then jacking up rates at the fastest rate in 42 years.

The good news is that only 10% of banks (about 414) are worse off than SVB in terms of financial strength.

The bad news is that Stanford estimates 191 regional banks remain high risk and could fail.

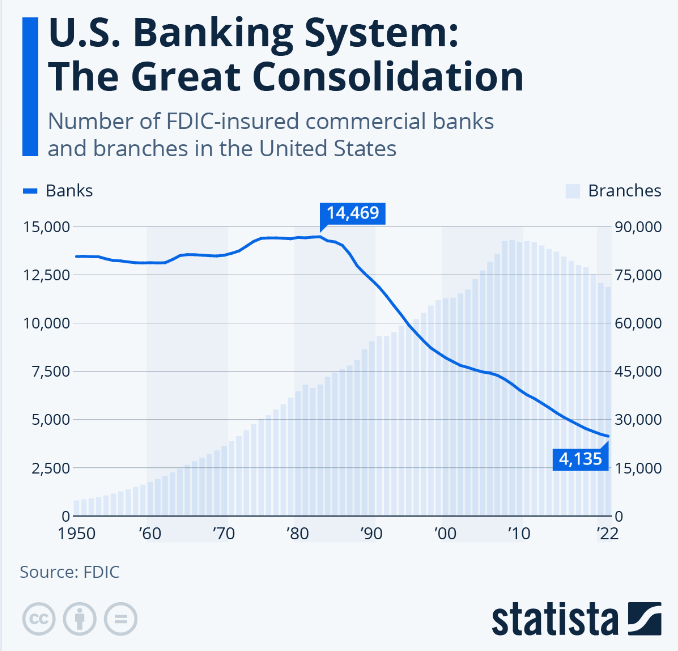

On average, four banks per year fail, and banking consolidation has been a steady trend since 1980.

- When the Fed hiked to 20% contributed to the Savings and Loan crisis

- 30% of SNLs failed over the next ten years

- no recession

- great stock market returns.

{kind=link}

In 1921, U.S. banks peaked at 31,000, and there was one bank for every 3,500 Americans.

Today there is one bank for every 80,500 Americans.

For context, Canada, famous for its banking stability courtesy of a government-enforced oligopoly, has 32 banks and 2 credit unions.

- One bank for every 1.1 million people

- the U.S. has 13.5X more banks per capita than Canada.

U.S. banks remain relatively less well-capitalized than many countries, but their capital buffers are 2X that of what they were at the start of the Great Recession.

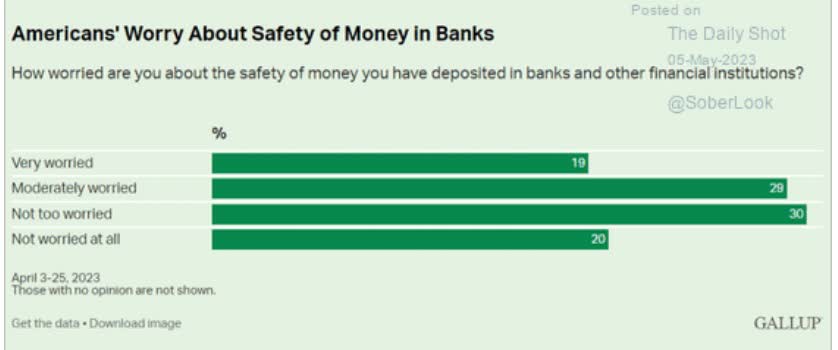

So, how worried should you be about the safety of your bank?

{kind=link}

48% of Americans are worried about their deposits, more than during the Great Recession.

This is an overreaction created by scary headlines.

The Regional Banking Crisis Is NOT A New Great Recession

First, let's consider the size of the remaining banks at high risk of failing.

{kind=link}

FRC was the 14th largest bank in the country, and no larger banks are at risk of failing.

First Citizens BancShares, Inc. (FCNCA) bought SVB because it is that strong of a bank.

Bloomberg

All the other banks are so strong and large that the U.S. government asked them to rescue FRC with $30 billion in emergency deposits.

- They have all now gotten that back.

What about PACW, which is potentially six months from being seized by the FDIC and sold to a stronger bank (most likely PNC)?

- PACW has $41 billion in assets and is the 53rd-largest bank

- WAL is the 40th largest bank with $68 billion in assets.

Stanford estimates that about $300 billion in banking assets might still fail, though there are some much larger at risk banks according to Moody's.

- Zions Bank is the 36th largest bank with $90 billion in assets

- Comerica is the 37th largest bank with $85 billion in assets

- the largest bank that MIGHT fail is KeyBank

- 20th largest with $188 billion in assets.

KEY isn't on any high-risk watchlist from rating agencies, but is the largest bank that might fail if we get a worst-case scenario (severe recession).

JPMorgan has the financial capacity to conservatively acquire another $250 billion in failed banking assets if the US government asked them to.

- JPM is only allowed to buy more banks (that have deposits) at the request of the U.S. government

- it has 16% of U.S. deposits and requires a waiver from the Office of the Comptroller of the Currency

- as do any banks with 10+% of U.S. deposits.

PNC was reported to be the #2 choice to buy FRC, and all of the remaining high-risk banks are ones that PNC or USB (also asked to bid) could acquire.

As could Truist Financial Corporation (TFC), the 3rd super regional rescue bank the U.S. government called on to save FRC.

In other words, the U.S. is likely to have a lot less banks in the future, but not necessarily due to spectacular collapses like SVB or FRC.

- if 1,000 banks get consolidated the U.S. will have 10X the banks per capita of Canada.

- if 2,000 banks get acquired the U.S. would have 5X the banks per capita of Canada.

The U.S. loves small, local banks, which is why we've had ten banking crises since 1792.

- 9,000 failed in the Great Depression

- none failed in Canada.

Since 1929, there has been one bank failure in Canada...due to fraud, not banking weakness.

{kind=link}

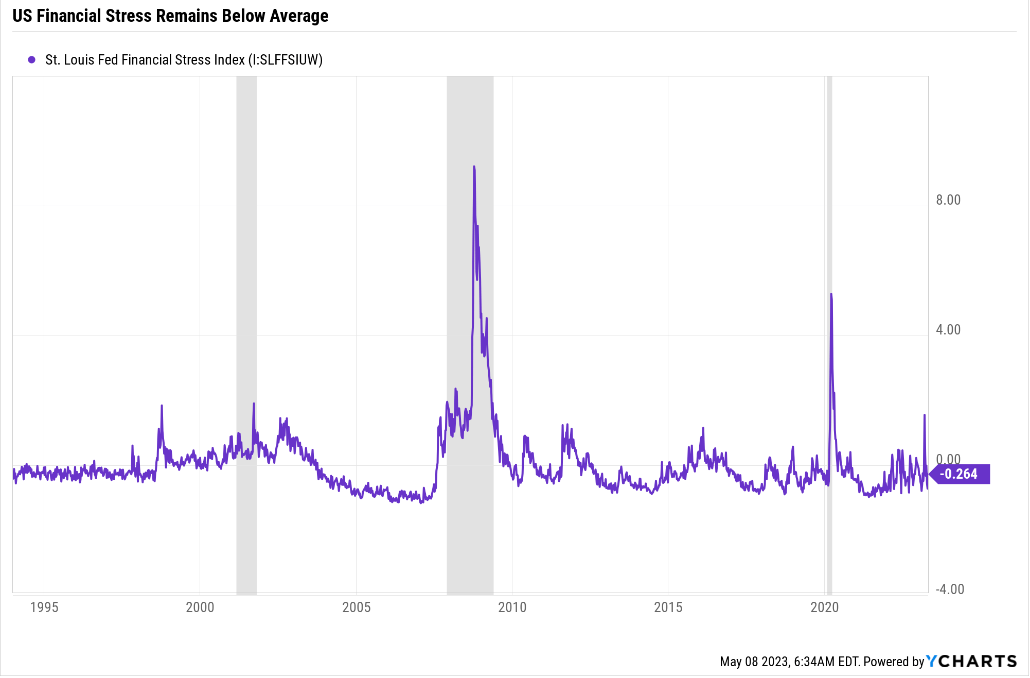

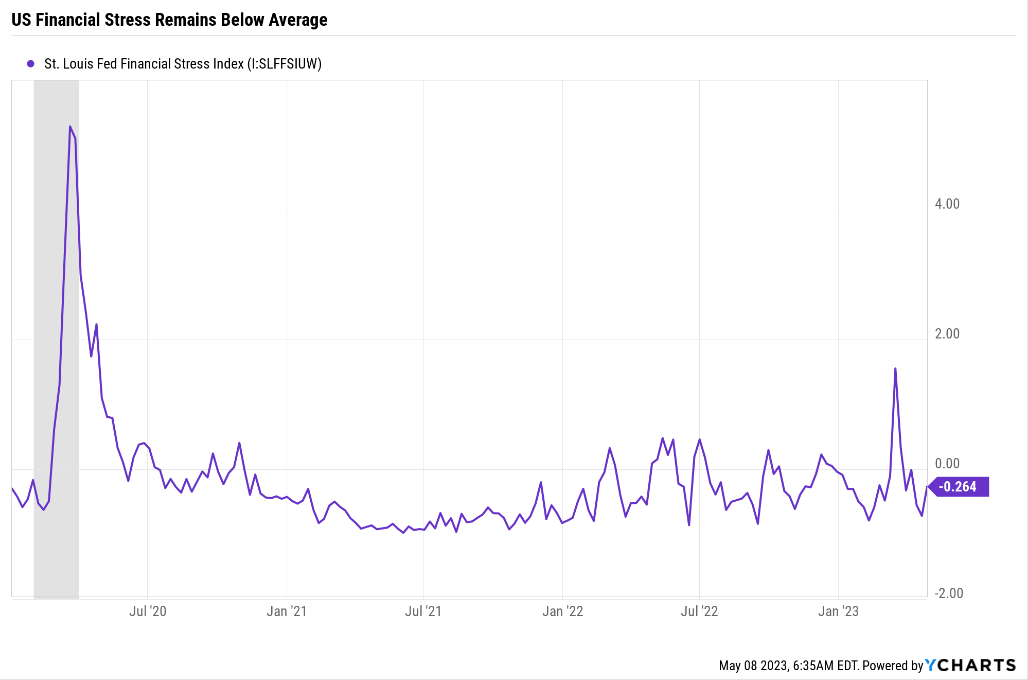

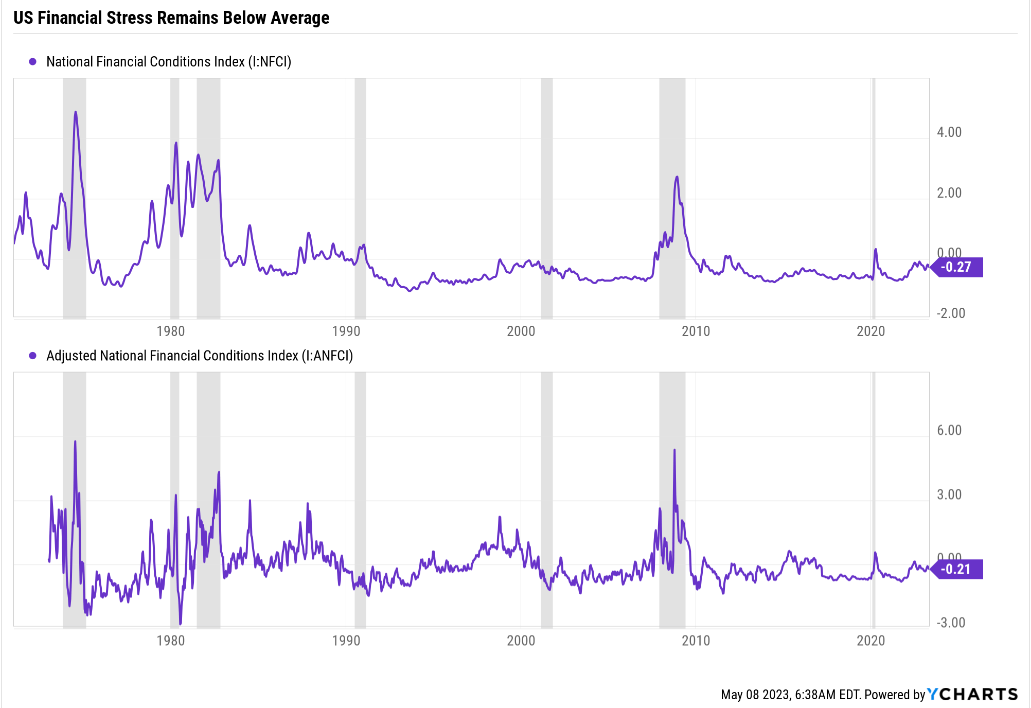

The St. Louis Financial Stress Index tracks 18 weekly financial metrics; zero is the average stress level since 1993.

{kind=link}

The failure of 3 banks plus Credit Suisse within 11 days caused a share spike in financial stress...to historically average levels for a recession.

And since then, financial stress has collapsed back to below-average levels.

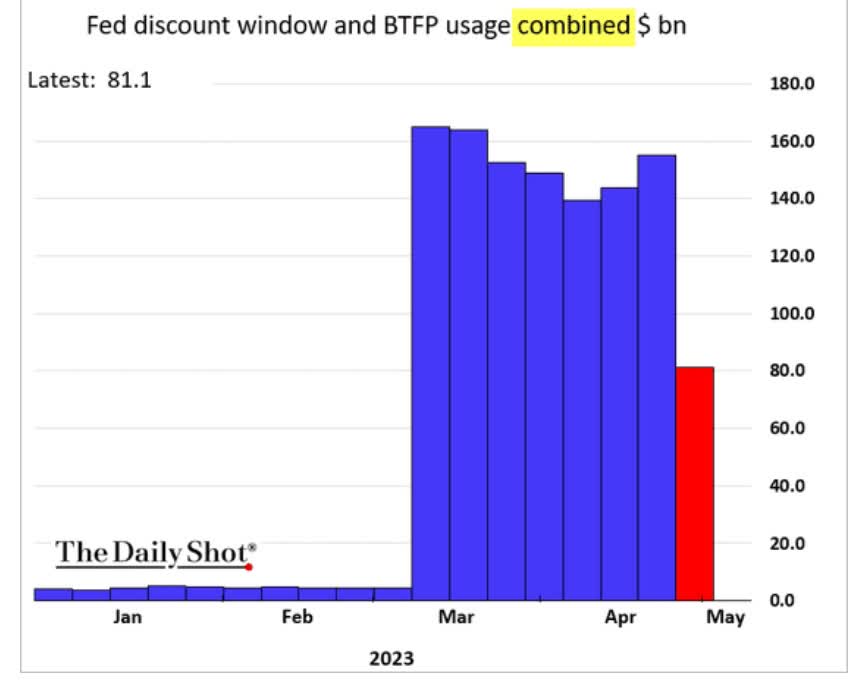

{kind=link}

Emergency borrowing by banks from the Fed has been cut in half now that JPM has acquired FRC.

{kind=link}

The Chicago Fed has been tracking financial stress since 1971 using 105 weekly metrics. Zero is average financial stress, and we're below average right now.

{kind=link}

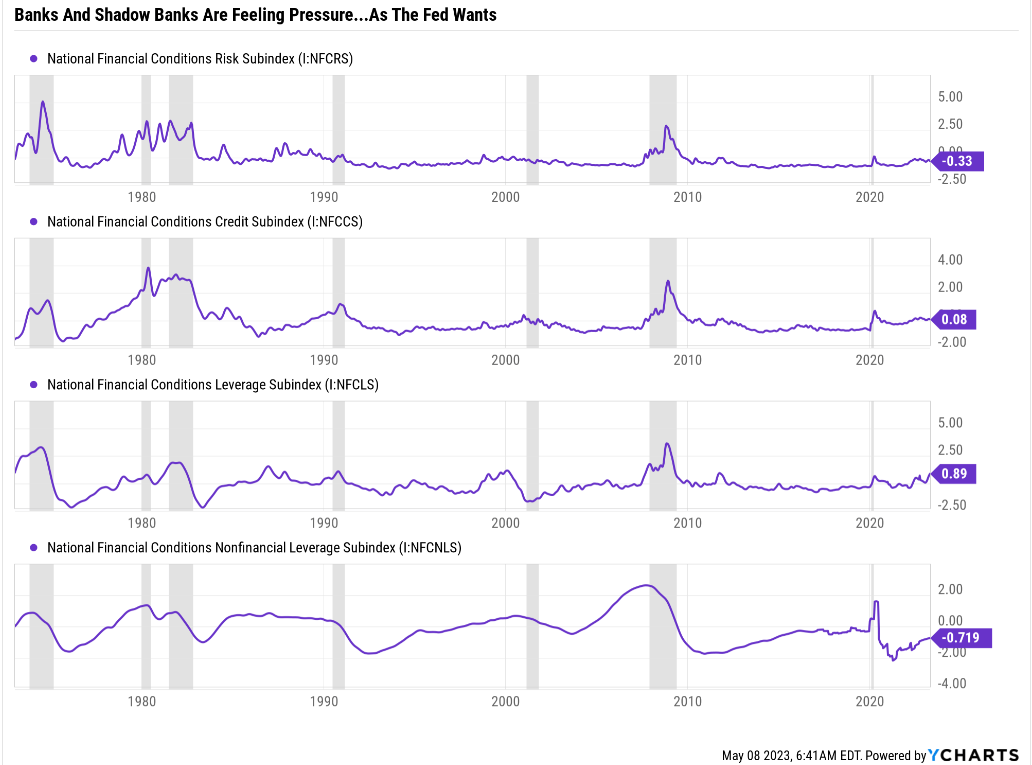

The credit and leverage subindexes indicate stress in the financial markets, including the shadow banking system.

However, they remain at levels consistent with a mild recession at worst.

Kiyosaki Is Still A Crank That's Safe To Ignore;)

{kind=link}

Economy Watch: A Mild Recession Is Likely Starting In July

{kind=link}

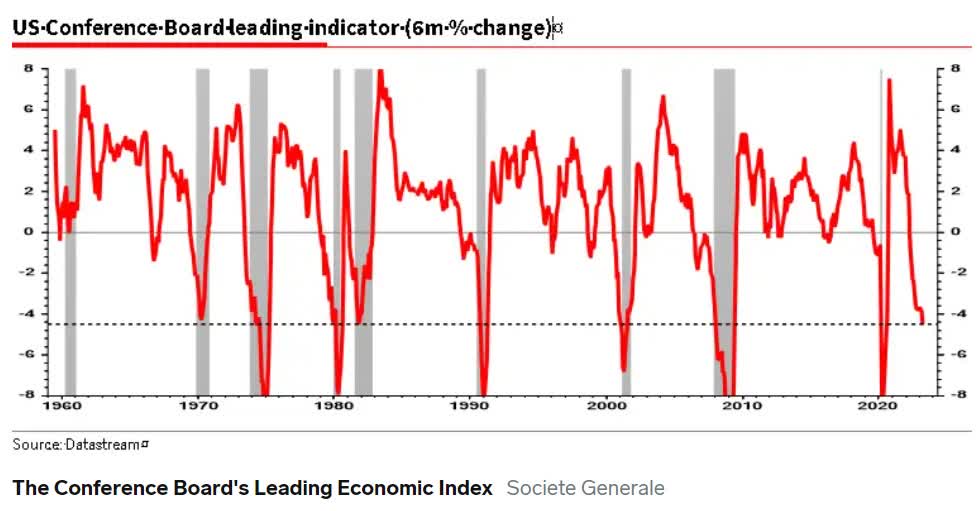

The Conference Board's leading economic index has never fallen at this rate over six months without a recession starting soon after.

{kind=link}

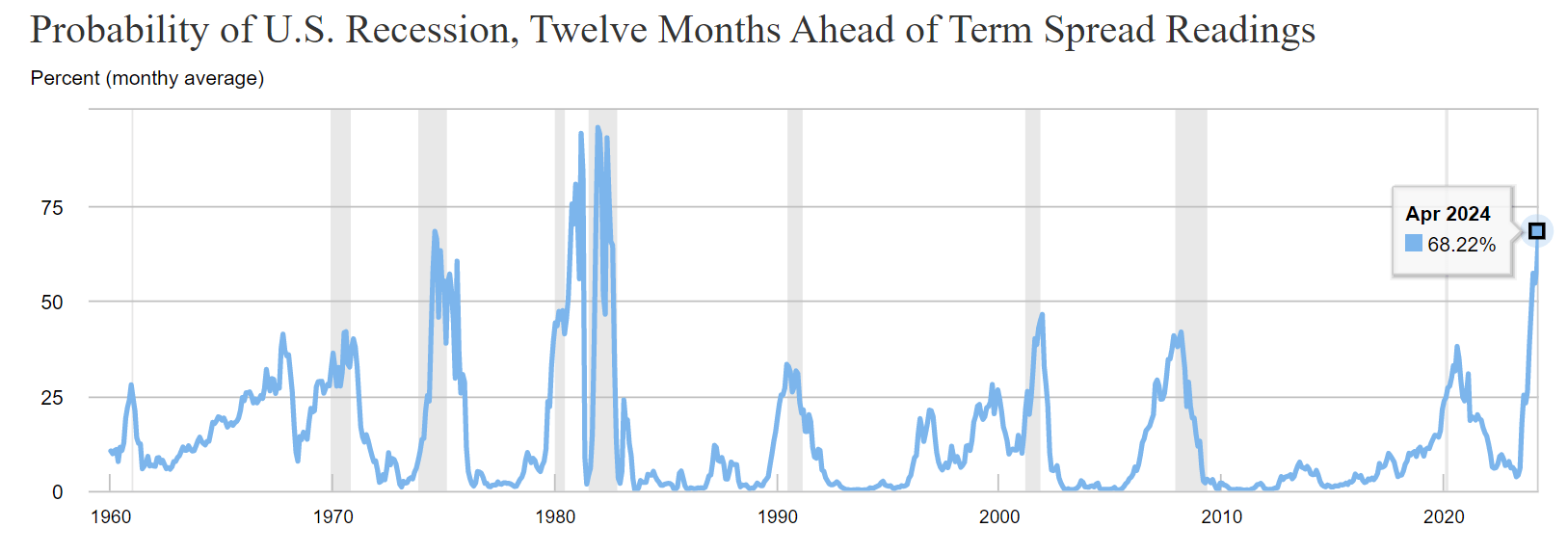

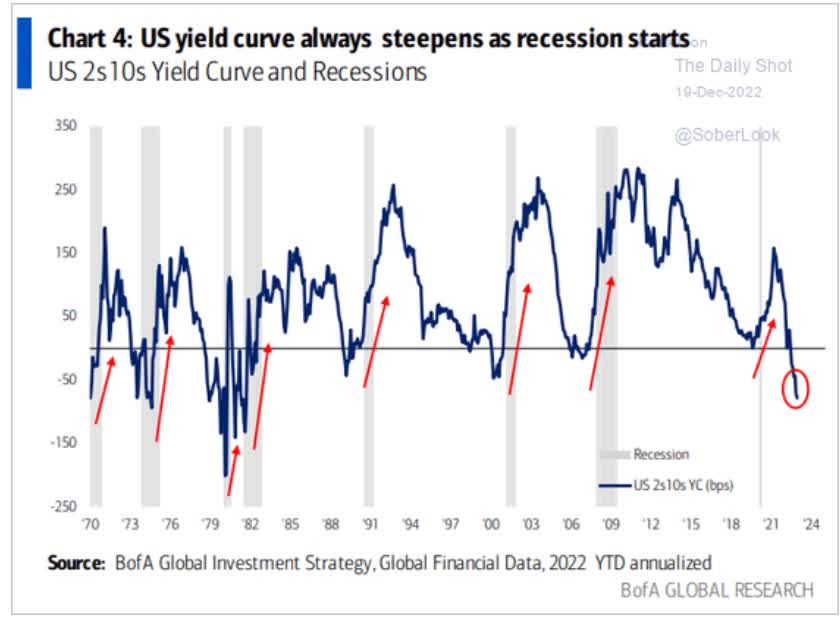

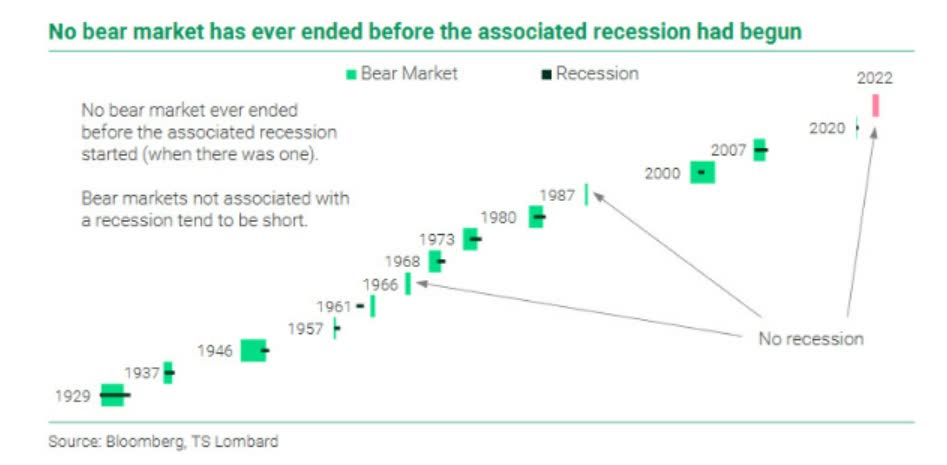

The 3m-10yr yield curve, the most accurate recession forecasting tool in history, has never been so inverted.

- Last week it hit -1.92%

- -1.79% on Monday, May 8th.

{kind=link}

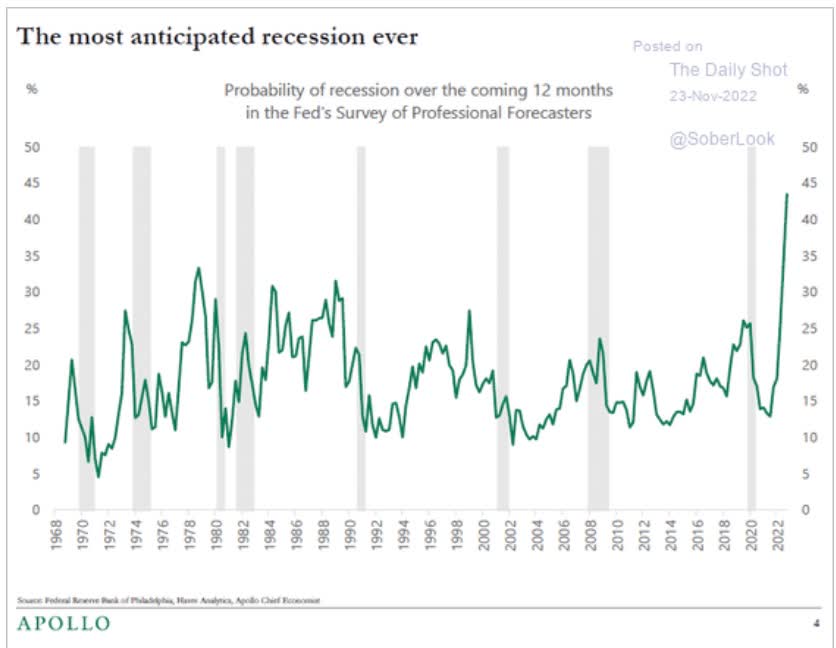

It's the most anticipated recession in history.

- 80% of Americans expect a recession

- 96% of CEOs

- the Fed

- Warren Buffett

- the bond market (100% chance by October 2024).

{kind=link}

The NY Fed estimates it's the highest recession risk in 42 years. Never in history has risk been this high without a recession starting soon afterward.

Behold The Mildest Expected Recession In History

{kind=link}

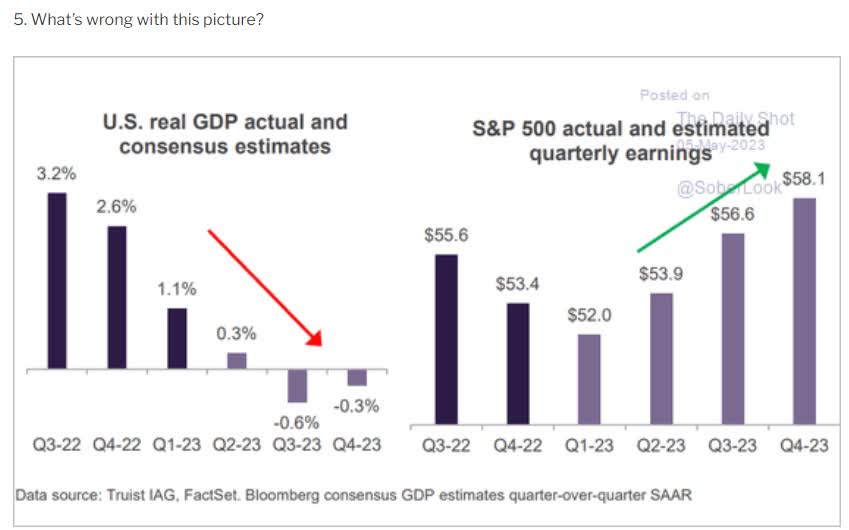

Wells Fargo agrees with the Bloomberg consensus that the recession begins in July, lasts six months, and peaks at a 0.9% GDP contraction.

Full-year 2023 growth is expected to be +1.0%.

If economists are right (they always underestimate recession severity), it would be the mildest recession in history.

- the previous record -1% peak decline and -0.4% full-year growth in 2001

- the September 11th recession.

Here's how mild the recession might be.

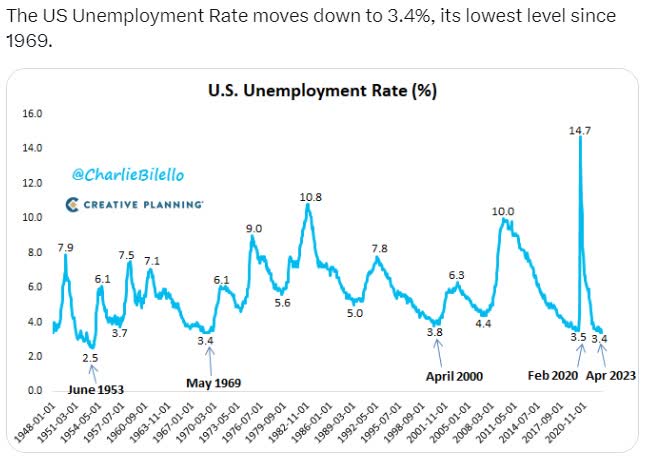

The Fed thinks unemployment will rise from 3.4% to 4.6%.

Wells Fargo thinks 5.1% peak unemployment.

Since WWII, the average unemployment is 5.75%.

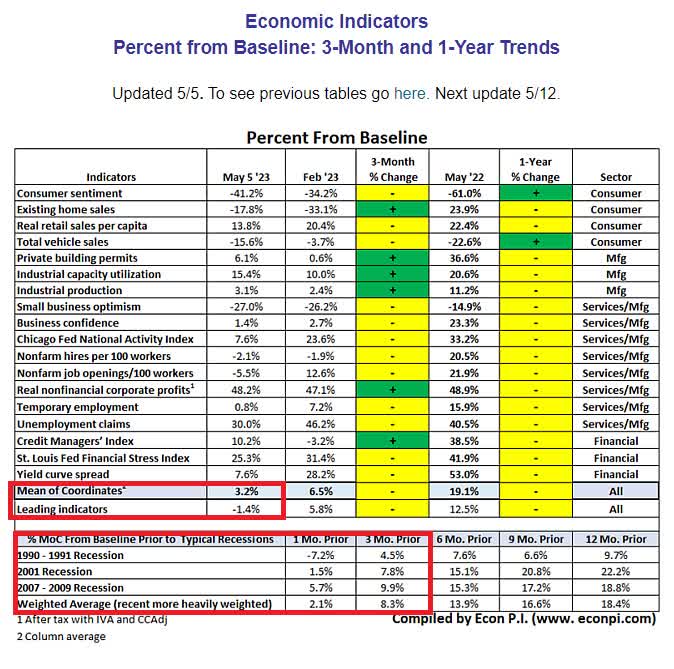

The Economic Data Confirms A Mild Recession Is Most Likely To Begin In About 6 Weeks

{kind=link}

Eighteen economic indicators say that a recession will likely start in July, confirming expectations from economists, the Fed, CEOs, Warren Buffett, and Americans in general.

How will we confirm the recession?

National Bureau of Economic Research will likely tell us after it's over.

Unemployment rises by 0.5% to 3.9% (Sahm rule).

Yield curve un-inverts.

{kind=link}

Bottom Line: A Mild Recession Is Likely Starting In July

The data confirms that:

- A mild recession is likely starting in a few weeks

- it's NOT a financial crisis

- the regional banking crisis is like the Savings and Loan crisis, NOT another Great Financial Crisis

- stocks are likely to have terrible few months.

{kind=link}

S&P Bear Market Bottom Scenarios

Best Case

| Earnings Decline |

| S&P Trough Earnings |

| Historical Trough PE Of 15 (upper end of the range) |

| Decline From Current Level |

| Peak Decline From Record Highs |

| 0% |

| 229 |

| 3439 |

| 16.9% |

| -28.6% |

| 5% |

| 218 |

| 3267 |

| 21.0% |

| -32.2% |

| 10% |

| 206 |

| 3095 |

| 25.2% |

| -35.8% |

| 13% |

| 199 |

| 2992 |

| 27.7% |

| -37.9% |

| 15% |

| 195 |

| 2923 |

| 29.3% |

| -39.3% |

| 20% |

| 183 |

| 2751 |

| 33.5% |

| -42.9% |

Base-Case

| Earnings Decline |

| S&P Trough Earnings |

| Historical Trough PE Of 14 (historical mid-range) |

| Decline From Current Level |

| Peak Decline From Record Highs |

| 0% |

| 229 |

| 3210 |

| 22.4% |

| -33.4% |

| 5% |

| 218 |

| 3049 |

| 26.3% |

| -36.7% |

| 10% |

| 206 |

| 2889 |

| 30.2% |

| -40.1% |

| 13% (average since WWII) |

| 199 |

| 2793 |

| 32.5% |

| -42.1% |

| 15% |

| 195 |

| 2728 |

| 34.0% |

| -43.4% |

| 20% |

| 183 |

| 2568 |

| 37.9% |

| -46.7% |

Worst Case

| Earnings Decline |

| S&P Trough Earnings |

| Historical Trough PE Of 15 |

| Decline From Current Level |

| Peak Decline From Record Highs |

| 0% |

| 229 |

| 2981 |

| 27.9% |

| -38.1% |

| 5% |

| 218 |

| 2832 |

| 31.5% |

| -41.2% |

| 10% |

| 206 |

| 2683 |

| 35.1% |

| -44.3% |

| 13% |

| 199 |

| 2593 |

| 37.3% |

| -46.2% |

| 15% |

| 195 |

| 2533 |

| 38.7% |

| -47.4% |

| 20% |

| 183 |

| 2384 |

| 42.4% |

| -50.5% |

| 25% (Joint Economic Committee, 3 Month Debt Default Scenario) 5% probability |

| 172 |

| 2235 |

| 46.0% |

| -53.6% |

Even in a mild recession where inflation keeps corporate profits from declining at all, stocks are likely to fall about 17%.

Treasury, Moody's, JP Morgan, Goldman

A 3-month debt default is the realistic worst-case scenario according to Moody's and the Joint Economic Committee, and that's a 5% probability.

- consistent with the bond market's estimates

- 2X the risk of nuclear war with Russia.

Why Worry About Bear Markets When You Can Have An Ultra SWAN Portfolio Like This?

| Bear Market |

| ZEUS Income Growth |

| 60/40 |

| S&P |

| Nasdaq |

| 2022 Stagflation |

| -11% |

| -21% |

| -28% |

| -35% |

| Pandemic Crash |

| -10% |

| -13% |

| -34% |

| -13% |

| 2018 |

| -13% |

| -9% |

| -21% |

| -17% |

| 2011 |

| -1% |

| -16% |

| -22% |

| -11% |

| Great Recession |

| -24% |

| -44% |

| -58% |

| -59% |

| Average |

| -12% |

| -21% |

| -33% |

| -27% |

| Median Decline |

| -11% |

| -16% |

| -28% |

| -17% |

(Source: Charlie Bilello, YCharts, Portfolio Visualizer Premium.)

Even in the worst-case scenario, a 54% market crash caused by a 3-month debt default, diversified portfolios like what DK has been teaching our subscribers to build are likely to remain safe.

- dividends remain safe and growing

- 19% peak decline for ZEUS income growth in a 54% market crash

- rebalance bonds and managed futures into blue-chips at the best valuations in years/decades/ever.

That's what we do at DK and iREIT. We're not just a stock picking service but world-class analysts who teach you how to be a better investor and build optimal sleep-well-at-night dream portfolios perfect for your needs.

Source: Imgflip

For further details see:

Recession Watch: A Mild Recession Is Likely Starting In July 2023