RRGB - Red Robin: Waiting To See Some Traction On This Turnaround Story

2023-03-30 12:29:18 ET

Summary

- RRGB Stock has seen a good run-up over the last three months.

- Investors are betting on the new management and their turnaround initiatives.

- Revenue should benefit from price increases and there should be a further upside if management’s initiatives gain traction.

- There are near-term headwinds from inflationary costs and macroeconomic environment is challenging.

- I would prefer waiting for management initiatives to gain traction before becoming more positive on the stock.

Investment Thesis

Red Robin Gourmet Burgers, Inc. (RRGB) is currently in the initial phase of its turnaround plan, which the new management is implementing to improve financial performance after poor operational execution and the impact of the pandemic over the last few years. Looking forward, revenue should benefit from price increases. There is a further upside as well if the new management's turnaround plan gains traction. On the margin front, inflationary costs remain a headwind in the near term, and costs associated with operational restructuring and hiring new staff may also pressure margins.

Compared to its peers, RRGB is currently trading at a significant discount on an EV/Sales basis. However, I would like to wait and closely monitor the new management's execution with respect to the turnaround initiatives before turning more positive on the stock. For now, I have a neutral rating on the stock.

Revenue Analysis and Outlook

Since 2017, RRGB has experienced a decline in sales due to poor guest experience resulting from low food quality, insufficient and improper staffing, and long waiting times. The situation was further exacerbated by COVID-related restaurant closures during the pandemic. When restaurants reopened in 2021, RRGB was able to recover some revenue and deliver growth due to easy comps from the pandemic and an increase in guest counts as travel restrictions eased. However, staffing issues persisted and weighed on customer satisfaction, leading to lower guest counts in 2022.

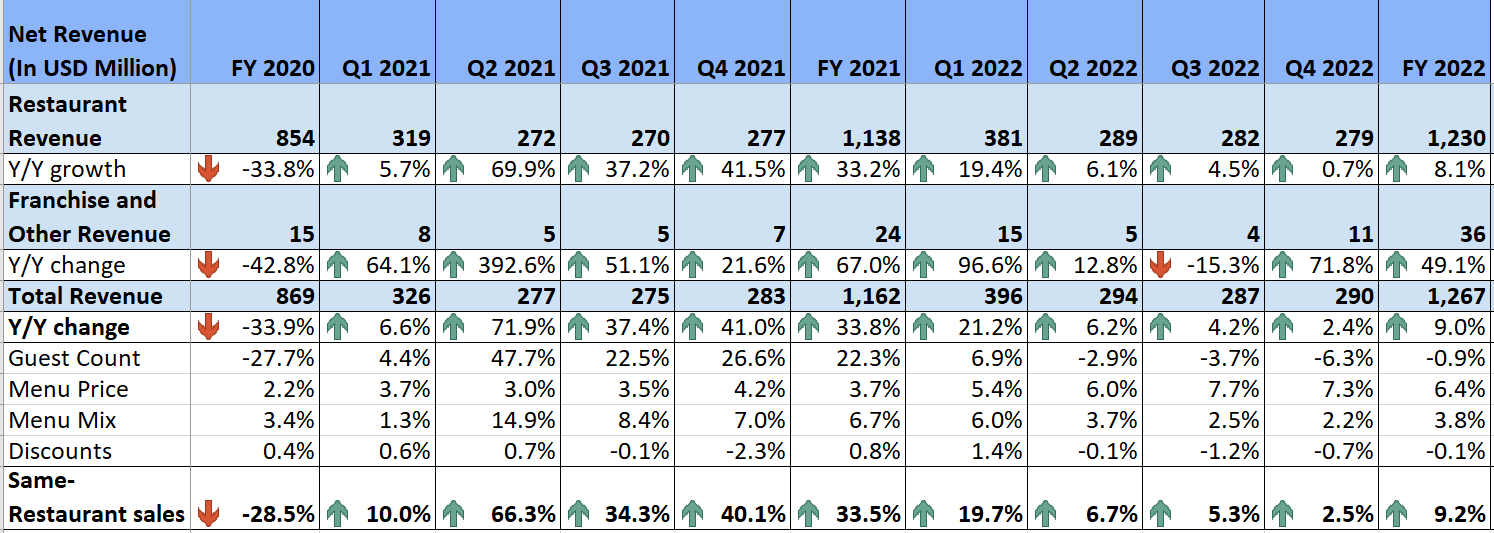

In Q4 2022, the company continued to see a decline in guest counts. However, it was able to post sales growth thanks to price increases and a favorable menu mix. This resulted in a 2.4% year-over-year increase in net sales to $290 million, reflecting comparable restaurant sales growth of 2.5%. The comparable restaurant sales saw a 7.3 percentage point benefit from price increases and a 2.2 percentage point improvement from a favorable menu mix, partially offset by a 6.3 percentage point reduction in guest counts and a 0.7 percentage point unfavorable effect from discounts.

RRGB’s Historical Sales (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, RRGB has the potential to increase its sales with the help of price increases, an emphasis on improving staffing issues, and the new management's turnaround plan .

To offset inflationary costs, the company has been increasing prices. The carryover price increases from the second half of 2022 should support comparable restaurant sales growth in the first half of 2023. Additionally, management plans to implement further price increases, which should also support revenue growth in the current year.

Regarding the turnaround plan, RRGB's staffing structure in the last five years was problematic because it reduced restaurant managers to only two full-time salaried managers, with the rest being hourly wage associate managers, even at the busiest locations. Bussers were also removed, increasing the workload of table servers. The new management is addressing this issue by hiring 4-5 full-time salaried managers, depending on traffic at a certain location, a kitchen manager, and associate managers. This should help restaurant managers execute daily operations more effectively, improve guest satisfaction, and drive sales. Furthermore, RRGB is bringing back bussers, hosts, and bartenders, reducing the burden on table servers by providing additional staff to offer fast service and reducing customer wait times. This improvement in guest experience is a priority of the turnaround plan, which I believe should help the company drive sales growth in the near to medium term if properly executed.

Additionally, RRGB is focusing on repairing and remodeling its existing restaurants to enhance the guest experience. It is transitioning from the existing conveyor belt cooking system to a more traditional flat-top cooking method, which should enable RRGB to deliver a product that is 20% larger with even greater quality and value for guests. In January, the company installed the flat-top system in 10 restaurants and is receiving positive feedback from guests and team members. RRGB targets completion of the flat-top cooking systems in remaining restaurants by mid-FY23. It is also launching new appetizers and menu items at different price points to further enhance customer experience and improve the guest count.

The company is also taking other initiatives that are expected to bear fruit in the long term. For example, the company is planning to involve frontline operators (restaurant managers) in key decision-making, and the management team at each restaurant will be compensated every month based on the profits of their restaurant. This should lead to a sense of ownership and drive more accountability.

I believe the new management turnaround plan is a step in the right direction to improve the quality of restaurant service and overall guest satisfaction.

For FY23, the company has guided for ~$1.3 billion in sales, which is almost in line with last year’s $1.27 bn in sales. So, management is not building a significant upside in its growth from turnaround plans. This leaves some room for an upside surprise in case management is able to stabilize and increase guest counts in the near term. However, execution is the key here, and one needs to closely watch it to see if the management’s turnaround plan is gaining traction.

Margin Analysis and Outlook

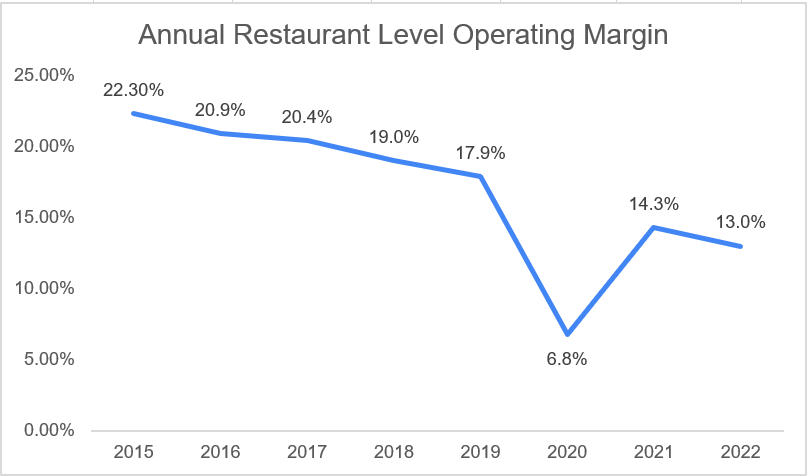

Since 2017, RRGB's margins have been negatively impacted by poor execution of cost-cutting initiatives, improper staffing leading to low productivity, underinvestment in the business, and operating deleverage. Margins have also been impacted by inflationary labor wage and commodity costs in recent years. These headwinds resulted in a 740 basis point decline in restaurant-level operating margin from 20.4% in FY2017 to 13% in FY2022.

RRGB’s Annual Restaurant-Level Operating Margin (Company Data, GS Analytics Research)

{kind=link}

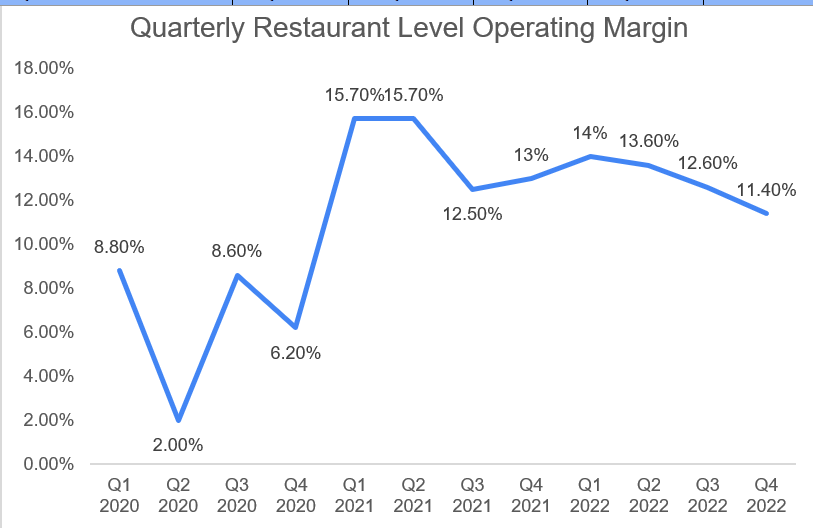

In Q4 2022, high commodity costs, which were up 13% YoY, continued to impact margins but were partially offset by price increases. This resulted in a 170 basis point YoY decline in restaurant-level operating margin to 11.4%.

RRGB’s Historical Restaurant-Level Operating Margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I believe near-term headwinds from inflationary costs are still a concern for margin recovery. Management expects mid-to-high single-digit labor and commodity inflation in FY23 with a similar level of price increases which should somewhat offset the inflationary headwind. However, the cost associated with restructuring operations, remodeling and repairing existing restaurants, and the constant hiring of new staff should also put pressure on margins in the near term resulting in a Y/Y margin decline.

In the medium to long term, management expects margins to recover with the implementation of the turnaround plan. The focus area supporting margin growth in the plan is the removal of cost and complexity. RRGB is simplifying its supply chain through changes like increasing pack sizes for purchased products and rightsizing contracts with current vendors to reflect competitive prices. It is also eliminating unnecessary third-party contracts. Moreover, the installation of a flat-top cooking system in RRGB kitchens should eliminate repair and maintenance costs associated with the conveyor belt cooking systems. Additionally, easing staffing issues and implementing a proper restaurant management structure should improve productivity. I believe these turnaround initiatives should help recover margins in the longer term, but again, execution is the key here. Further, margins are likely to get worse (due to investments) before getting better, and investors need a lot of patience to reap the benefits.

Valuation and Conclusion

RRGB has negative EPS, so we can't compare it with its peers on a P/E basis. I have used EV/EBITDA to compare it with some of its peers. However, it is not the best metric as the company’s EBITDA margins are currently depressed due to years of mismanagement. So, I have also added EV/sales ratio to compare with its peers and get a sense of undervaluation.

| Peers |

| EV/EBITDA ((FWD)) |

| EV/Sales ((FWD)) |

| The Wendy’s Company ( WEN ) |

| 14.98x |

| 3.63x |

| Restaurant Brands International Inc. ( QSR ) |

| 14.23x |

| 5.11x |

| McDonald's Corporation ( MCD ) |

| 19.21x |

| 10.23x |

| Jack in The Box Inc. ( JACK ) |

| 14.44x |

| 2.83x |

| Red Robin Gourmet Burgers, Inc. ((RRGB)) |

| 12.62x |

| 0.64x |

Relative valuation based on consensus estimates (Source: Seeking Alpha)

Clearly, RRGB is undervalued if we look at EV/EBITDA and significantly undervalued if we look at EV/sales. However, whether its valuation multiples can re-rate near its peers depends on the success of management efforts. Investors have so far cheered the initiatives of new management, and the stock has run up from mid-single digit levels around the end of last year to low teens currently. In the good old days, the stock had also seen $90-plus levels in 2015 when everything was going fine. So, there is clearly a meaningful upside if management is able to turn around the company.

However, I believe further upside won't be as easy as what we have seen over the last three months, and investors would prefer seeing some turnaround in terms of stabilization and improvement in guest counts before buying the stock. The current macroeconomic environment doesn’t make things easier either, and it should take some time before management’s initiatives start showing results. Further, as of the last quarter's end, the company’s long-term debt was around $203 mn, the long-term portion of operating lease liabilities was around $393 mn, and net cash was around $48.8 mn. The turnaround will involve investment in hiring new staff and remodeling restaurants which should increase leverage and pressure the company’s margins in the near term. So, net leverage should further increase in the near term, which adds to risk if management’s plan doesn’t exactly go as expected.

There is a potential for a good upside if turnaround plans go well, and I would certainly be watching out this stock closely. But for now, I prefer to be on the sidelines and wait for management’s initiatives to gain traction and reflect in the company’s financial results.

For further details see:

Red Robin: Waiting To See Some Traction On This Turnaround Story