REIT - REITs: Darkest Before The Dawn

2023-10-31 10:00:00 ET

Summary

- At the halfway point of earnings season, REIT earnings results have been stronger than expected - and certainly stronger than the recent dismal share price performance of REITs would indicate.

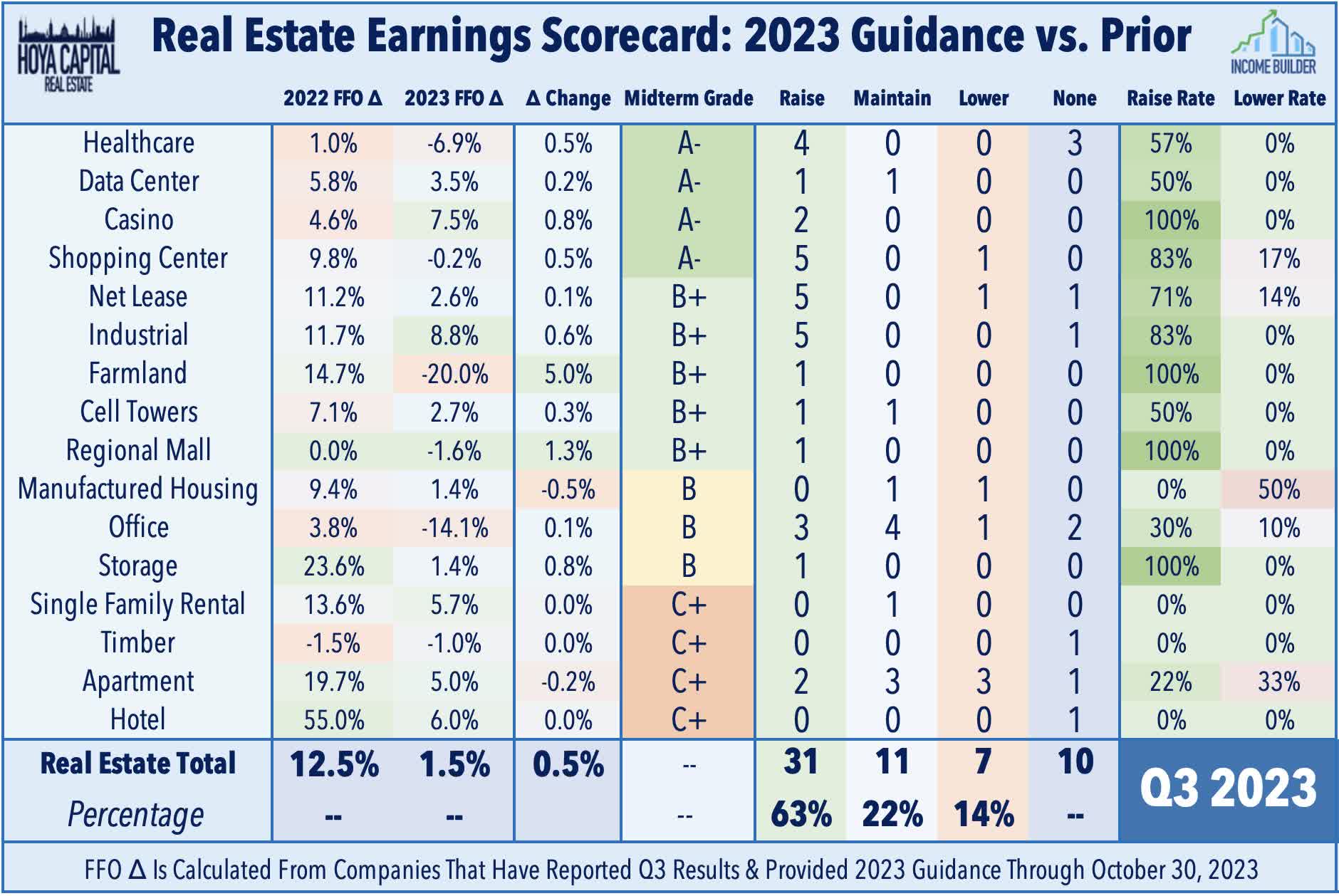

- Of the 40 equity REITs that have provided updated full-year FFO guidance, 58% have increased their forecast, while 18% have lowered their outlook. We've also seen a half-dozen REITs raised dividends.

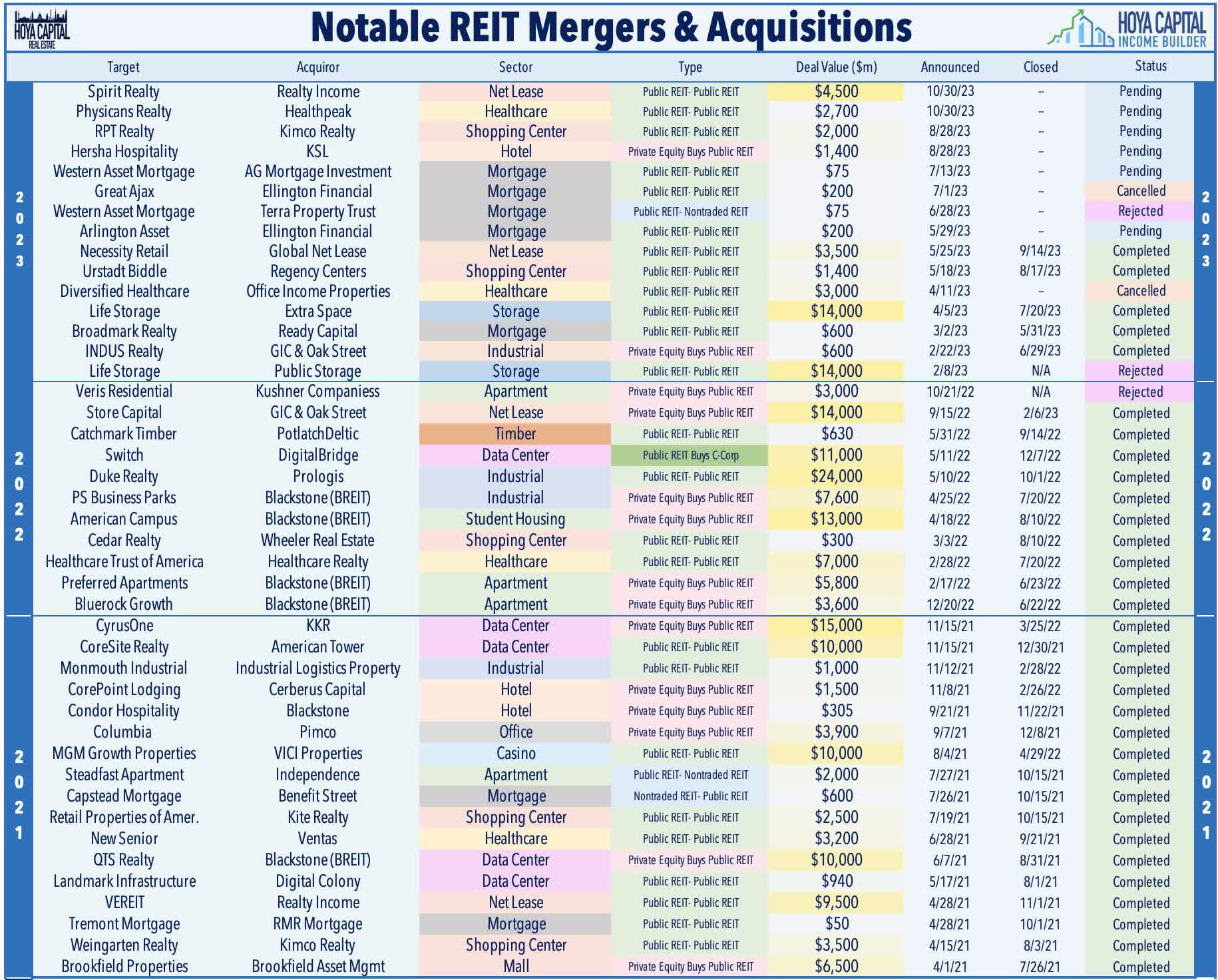

- REIT-to-REIT M&A has been a major theme, with another pair of mergers this week. Given the scarcity of debt capital, equity REITs are the "only game in town" for sellers.

- Consistent with the "higher for longer" macroeconomic story of 2023, resilient pricing power has been a common thread across most property sectors - notably in data center, retail, and residential REITs - but so has stubbornly persistent expense pressures.

- Supply growth is becoming a headwind for multifamily and industrial REITs as the pandemic-era boom in new development reaches completion, but developers have pulled back significantly this year. Soaring interest expense is the primary culprit behind the handful of downward guidance revisions.

Real Estate Earnings Halftime Report

{kind=link}

We're at the halfway point of another consequential real estate earnings season, with roughly 75 equity and mortgage REITs representing 50% of the total market capitalization now having reported results. Darkest before the dawn? Thus far, REIT earnings results have been stronger than expected - and certainly stronger than the recent dismal share price performance of REITs would indicate. Of the 49 equity REITs that have provided updated full-year Funds From Operations ("FFO") guidance, 31 REITs have increased their forecast, 11 have maintained, and 7 have lowered their outlook. Among the 30 REITs that adjusted their FFO forecast, 82% were upward revisions, while just 18% were downward guidance revisions. By comparison, FactSet reports that 59% of S&P 500 components have raised the full-year EPS outlook, while 41% have reduced their guidance. The guidance "raise rate" was stronger at the property level than at the corporate level, with only five REITs (10%) lowering their full-year Net Operating Income ("NOI") outlook.

{kind=link}

Consistent with the broader "higher for longer" macroeconomic story of 2023, resilient pricing power has been a common thread across most property sectors - notably in data center, retail, and single-family residential REITs - but so have stubbornly persistent expense pressures. Residential REITs, in particular, continue to see insurance and property taxes rising by double-digits across most markets and segments. Soaring interest expense is the primary culprit behind the handful of downward guidance revisions, a theme that will be seen with greater frequency in the back half of earnings season. Supply growth is becoming a headwind for multifamily, self-storage, and industrial REITs as the pandemic-era boom in new development reaches completion, but developers have pulled back significantly this year, providing reasons for optimism heading into 2024 if current demand trends can hold up.

{kind=link}

As predicted, REIT-to-REIT M&A has been a major theme this earnings season, with another pair of mergers announced this morning. Realty Income ( O ) - the largest net lease REIT - announced that it will acquire Spirit Realty ( SRC ) - which we own in the Focused Income Portfolio - in a $9.3B all-stock deal at a 15% premium to SRC's last closing price. Elsewhere, medical office building REITs Healthpeak Properties ( PEAK ) and Physicians Realty ( DOC ) agreed to merge in an all-stock merger. Given the scarcity of debt capital, equity REITs have become the "only game in town" for sellers, and we're beginning to see more consolidation opportunities for well-capitalized public REITs - even before equity market valuations rebound from their current historic lows. We've also seen over a half-dozen REITs raise their dividend over the past two weeks - lifting the full-year total across the REIT sector to 70 - but the number of REIT dividend cuts has also ticked higher to 29, concentrated almost exclusively in the office and residential mortgage REIT segments. Below, we discuss our halftime analysis and grades for each property sector.

{kind=link}

Residential REIT Halftime Report

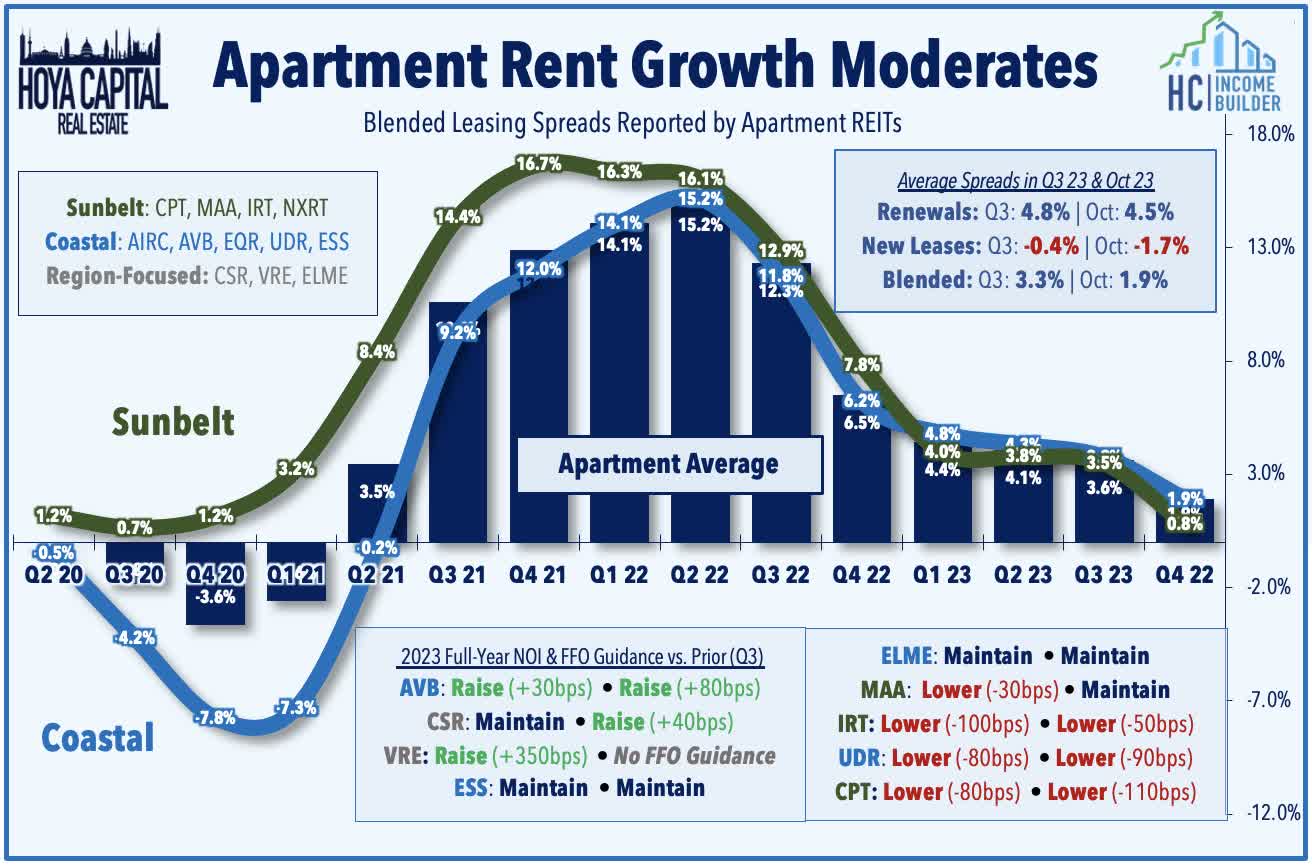

Apartment : (Halftime Grade: C+) While several property sectors haven't yet started earnings season, apartment REIT earnings season is essentially complete, with nine of the twelve largest apartment REITs reporting results. Following a surprisingly strong second quarter, we've seen softer results in Q3, with downward NOI and FFO revisions outpacing increases by 2:1 - resulting from a combination of supply headwinds and upward expense pressures. Reversing the pattern since the start of the pandemic, coastal-focused apartment REITs have generally reported stronger results this earnings season. While we've seen an uptick in concessions on new leases, renewal rent growth has remained solid at around 5% in Q3 and into October. AvalonBay ( AVB ) has been a notable upside standout, raising its outlook across the board, while noting that it's seeing less supply growth than its peers, given its focus on suburban Coastal markets. Sunbelt-focused Camden Property ( CPT ) has been a notable laggard, reporting that blended rent growth cooled to 2.5% in Q3 and dipped into negative territory in October at -0.4% - the weakest among the apartment REITs to report results thus far

{kind=link}

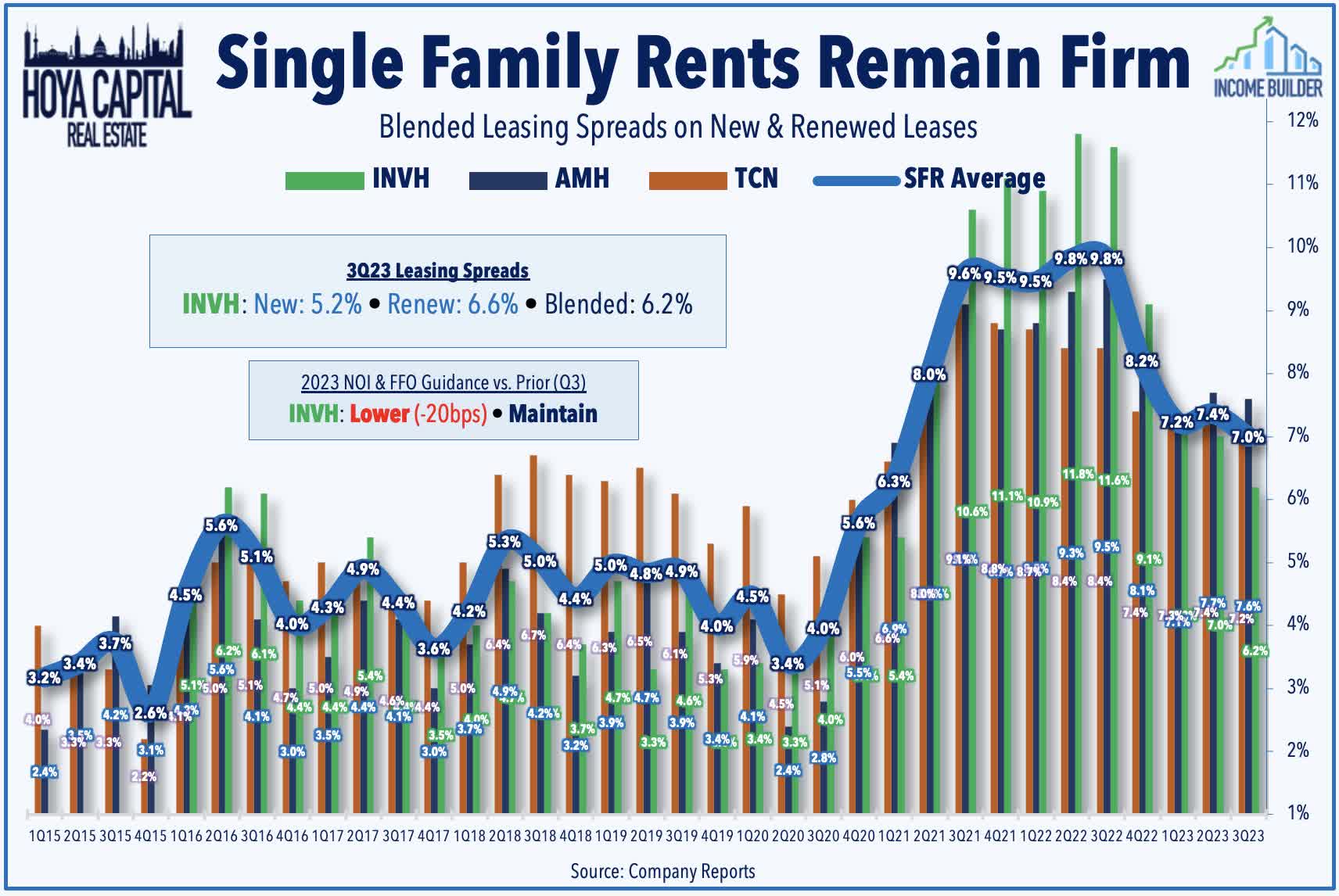

Single-Family Rental : (Halftime Grade: C+) Rent growth trends have been quite a bit stronger on the single-family side - which is not facing the same supply headwinds as their multifamily peers - but expense pressures remain a headwind. Invitation Homes ( INVH ) - the largest single-family housing owner in the U.S. - reported mixed results and trimmed its full-year NOI outlook on higher property taxes and insurance expenses. INVH maintained its full-year AFFO outlook - which calls for 5.0% growth this year - but trimmed its same-store NOI guidance to 4.8% - down 20 basis points from its prior outlook. INVH now expects same-store expenses to rise 10.5% this year, and reported that property tax expense was higher by 13% year-over-year, while insurance expense was 15% higher. Leasing trends remained solid, however, with INVH recording blended leasing spreads of 6.2% comprised of 6.6% increases on renewals and 5.2% increases on new leases. While new homeowners can now expect to pay in excess of 8% on a new mortgage, INVH noted that it raised $800M in Q3 at an average interest rate below 5.5%. This cost of capital advantage facilitated a robust quarter of acquisitions, with INVH buying 2,291 homes for $854 million. We'll hear results from American Homes ( AMH ) later this week and Tricon ( TCN ) next week.

{kind=link}

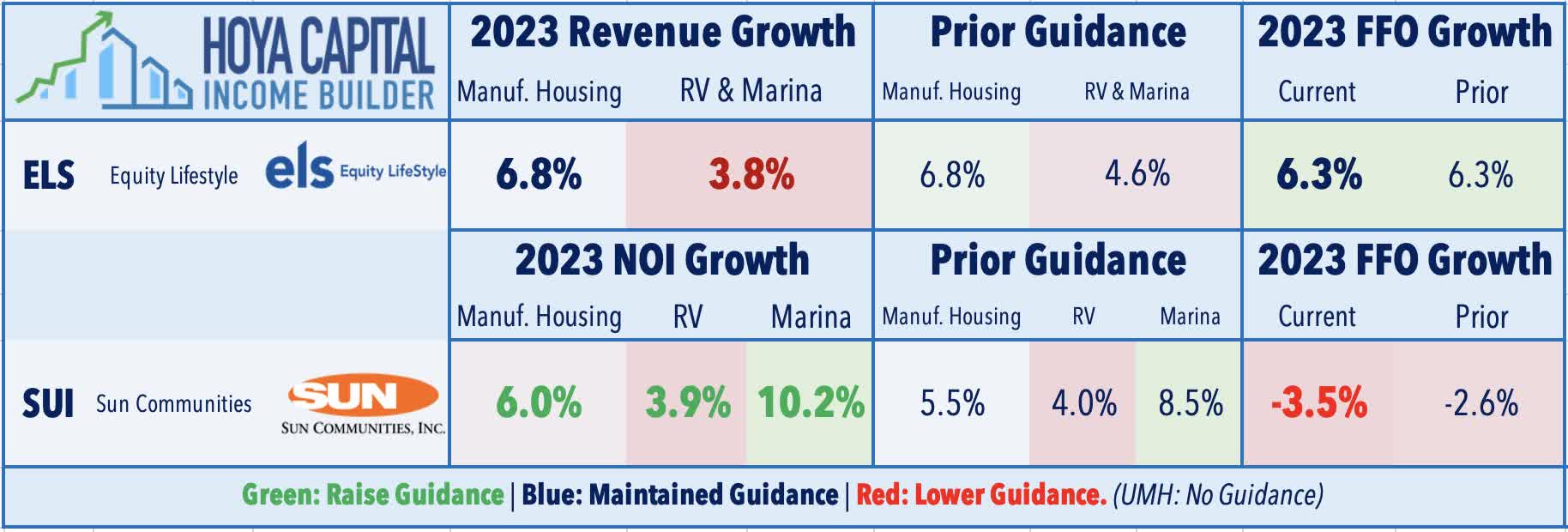

Manufactured Housing : (Halftime Grade: B) MH REITs - which had uncharacteristically lagged from mid-2022 through mid-2023 - have been among the top performers this earnings season. Sun Communities ( SUI ) reported solid results, as strong property-level fundamentals in the U.S. offset ongoing weakness in its international segments. SUI boosted its full-year NOI growth outlook for each of its three U.S. business segments, projecting growth of 6.0% in its core MH portfolio, 3.9% in its RV segment, and 10.2% in its marina segment. Sun also established preliminary guidance for 2024, noting that it expects MH rent growth of 5.4%, RV rent growth of 6.5%, and marina rent growth of 5.6%. Sun's ill-timed international expansion into the UK last year continues to weigh on its overall results, however, as continued weak home sales performance in its Park Holiday portfolio and a separate default on a $361M loan to a different UK manufacturing housing operator prompted a downward revision to its FFO forecast. Equity LifeStyle ( ELS ) maintained the midpoint of its full-year growth FFO outlook at 6.3% and maintained its full-year outlook for MH same-store revenue growth at 6.8%. Excluding the struggling transient RV component, full-year revenues in the RV & Marina segment are expected to increase 8.6% for the year. ELS also noted that it will begin sending renewal offers to its MH residents this month for the 2024 period, with average rent increases of 5.4%. ELS has set annual rates on 95% of its annual RV sites, with average rent increases of 7.0%.

{kind=link}

Office & Healthcare REIT Halftime Report

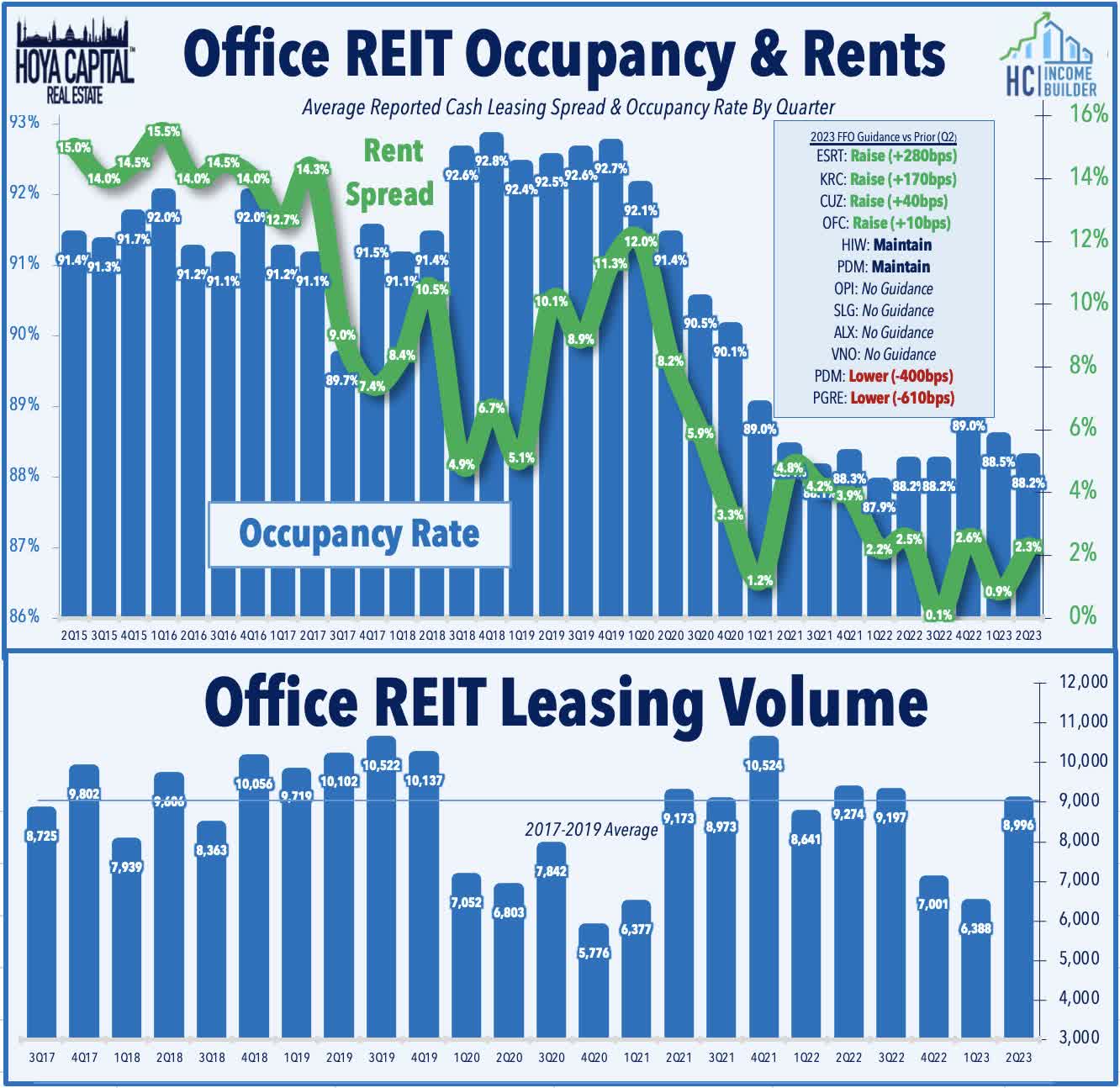

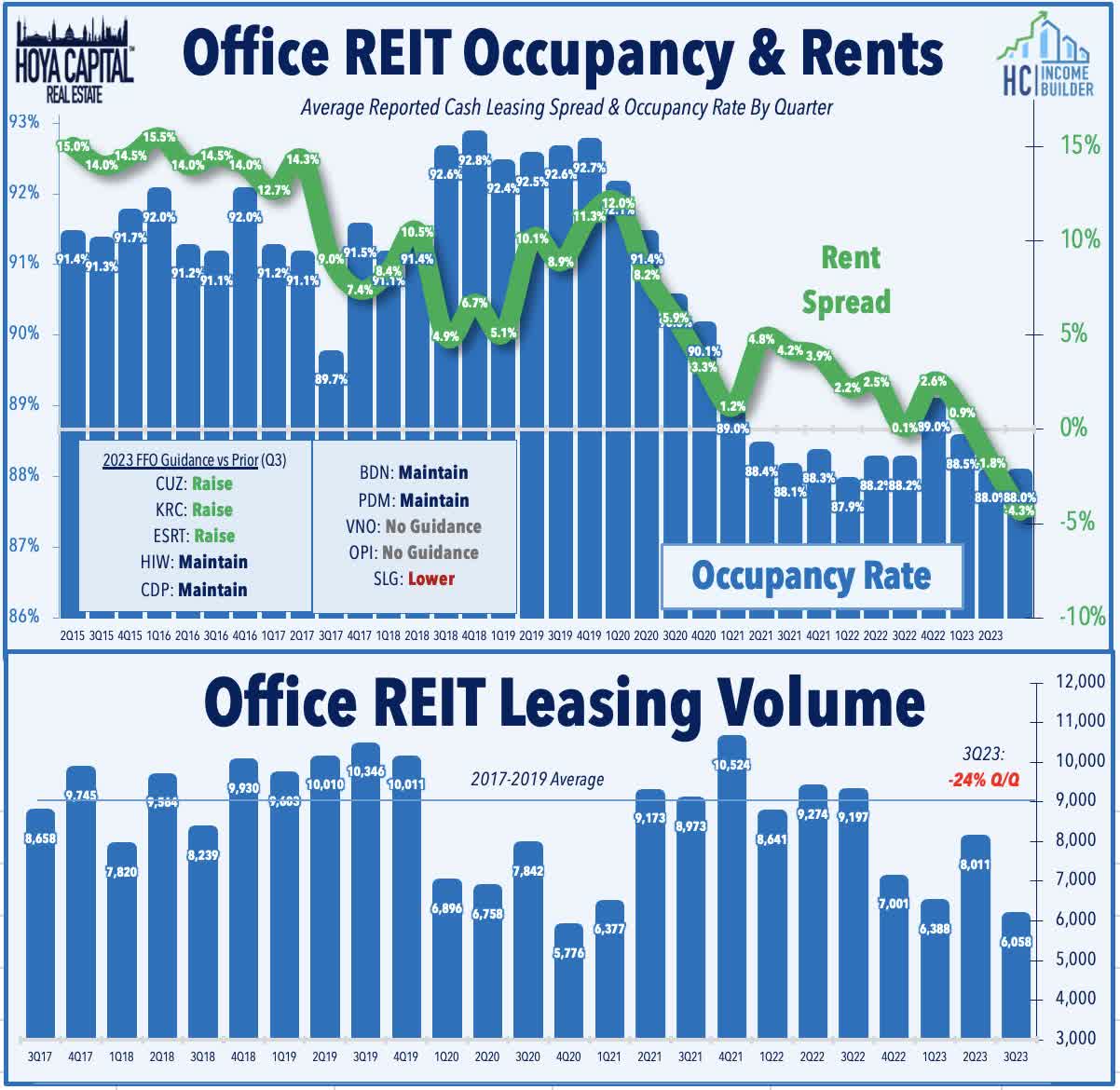

Office : (Halftime Grade: B) We've seen third-quarter results from ten of the 19 office REITs. Unsurprisingly, results thus far from office REITs showed continued demand headwinds, but Sunbelt markets continue to exhibit notable - and underappreciated - outperformance over clearly troubled coastal markets. Among the seven office REITs to report results this far, leasing activity has averaged 24% below last quarter, while occupancy rates - already at historic lows - have been roughly flat. Sunbelt-focused Cousins ( CUZ ) has been an upside standout after reporting decent results and raising its full-year outlook. Bucking the trends, CUZ reported an acceleration in leasing activity in Q3, recording 548k square feet of activity and achieving rent growth of 9.8% on renewed lease. Cousins is one of three office REITs to raise its full-year FFO outlook this quarter, joining Empire State Realty ( ESRT ) and Kilroy ( KRC ). On the downside, Philadelphia-focused Brandywine ( BDN ) has been a laggard after reporting soft leasing volume at 351k SF, down from 411k in the prior quarter. NYC-focused SL Green ( SLG ) also reported unimpressive results, lowering its full-year FFO guidance to reflect a -23% decline from last year - down from its prior outlook calling for an -18% FFO decline.

{kind=link}

{kind=link}

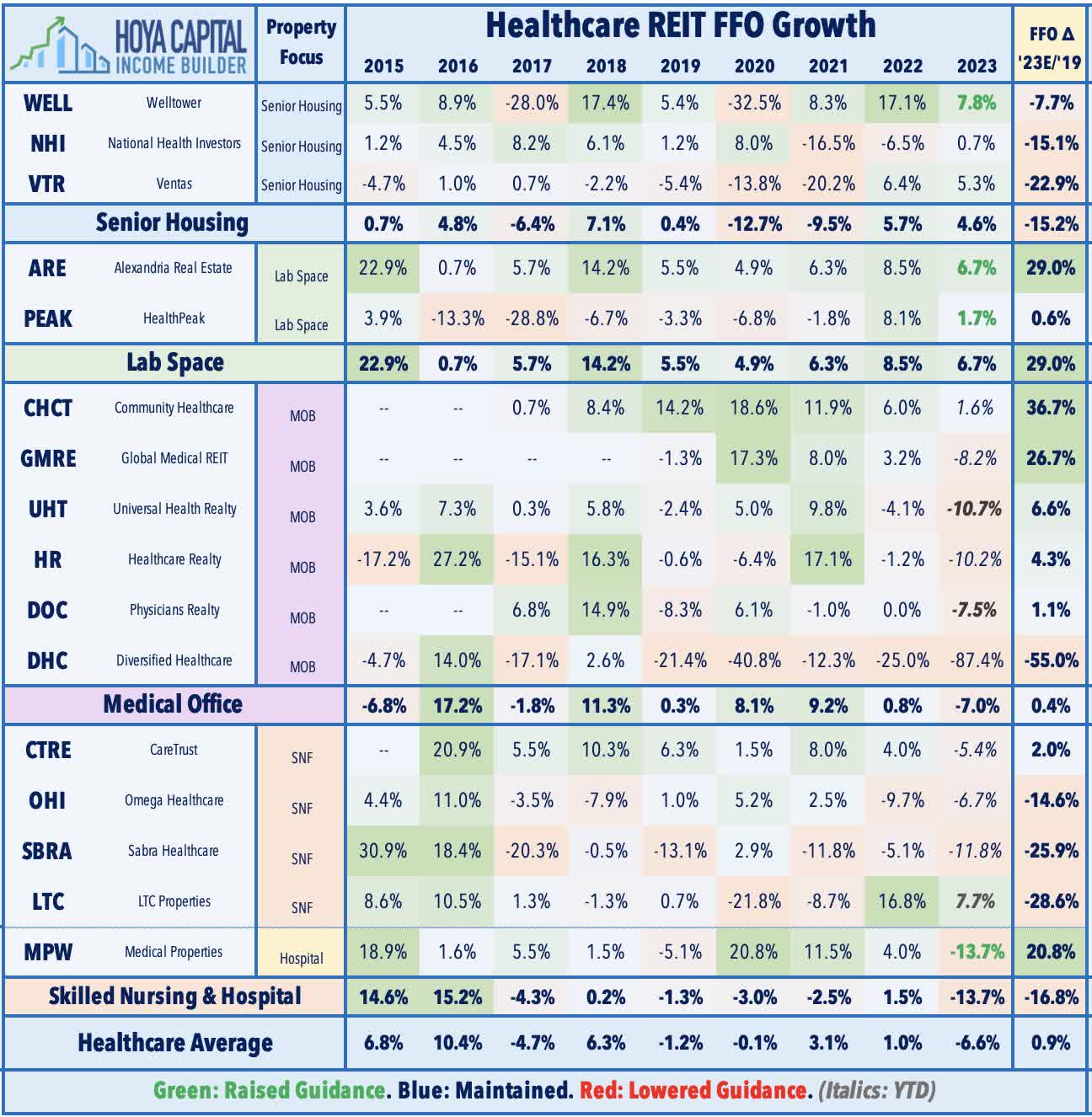

Healthcare : (Halftime Grade: A-) We've heard results from eight healthcare REITs. Results have been surprisingly strong this earnings season, with all four REITs that provide full-year guidance raising raised their outlook. Embattled hospital owners Medical Properties Trust ( MPW ) - which has plunged over 65% since the start of 2022 amid rent collection issues from a handful of struggling hospital operators - has been a leader this earnings season after reporting decent results and raising its full-year outlook. MPW now expects its full-year FFO to decline 13.7% - a 110 basis point improvement from its prior outlook. Importantly, MPW noted that it resumed collecting cash rent payments in September and October from Prospect Medical, which had been struggling to pay rent. HealthPeak ( PEAK ) - which this week announced its plan to merge with Physician's Realty ( DOC ) - also reported strong results and raised its full-year FFO and NOI outlook, driven primarily by outperformance in its relatively small senior housing segment. Lab space owner Alexandria Real Estate ( ARE ) reported solid results as well and raised the midpoint of its full-year FFO outlook. Leasing activity remained sluggish in Q3, as expected, with total volume of 867k square feet - its lowest since Q1 of 2020 - but rent spreads rebounded with cash renewal increases of 19.7%.

{kind=link}

Industrial & Technology REIT Halftime Report

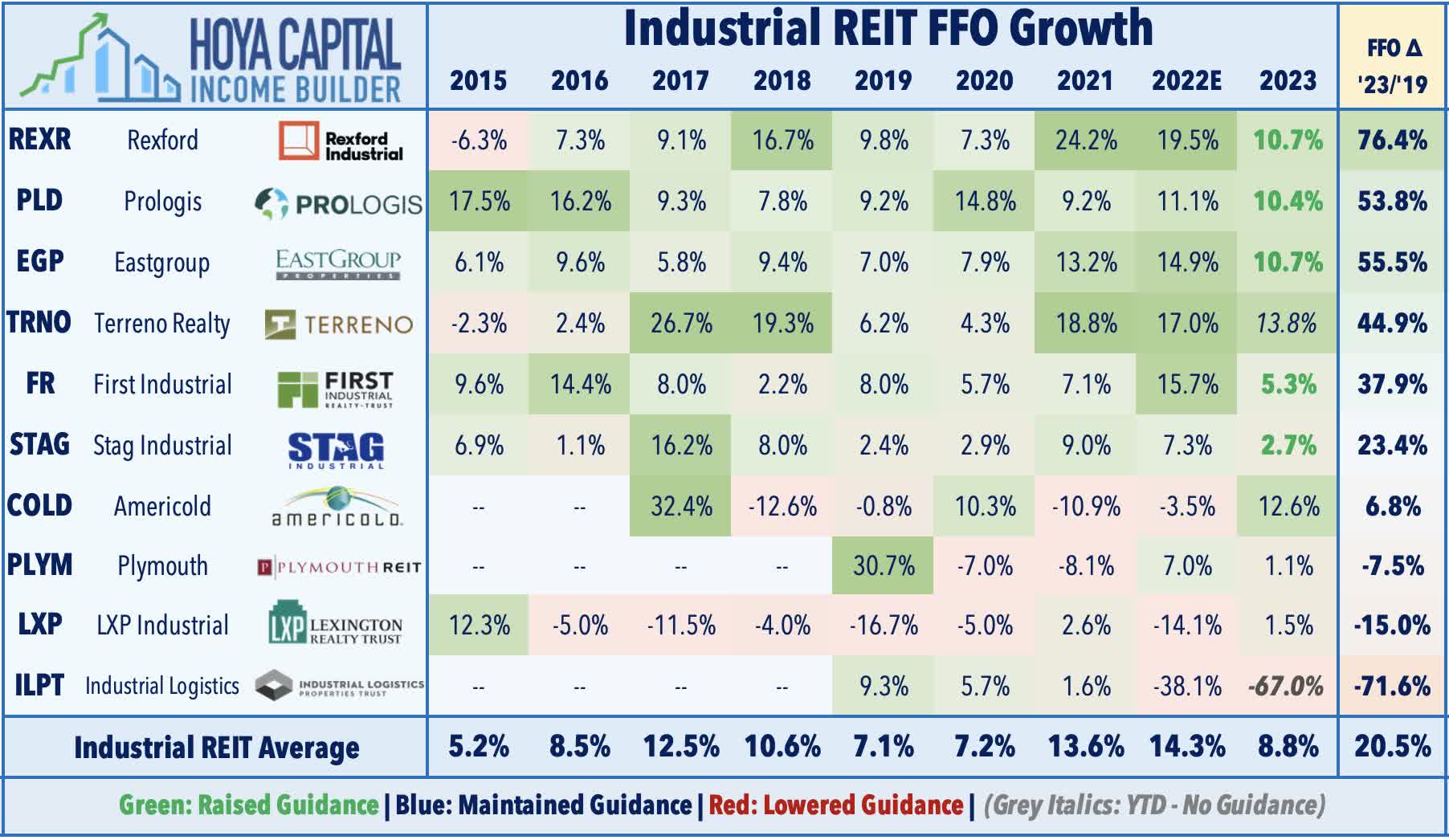

Industrial : (Halftime Grade: B+) We've seen results from the six largest industrial REITs, all six of which have increased their full-year FFO outlook. Prologis ( PLD ) - the industry bellwether - reported "beat and raise" results but reiterated its expectation that elevated supply growth will negatively impact market fundamentals in the coming quarters and noted pockets of weakness in its Southern California markets. A common thread across the sector this earnings season, this cautious commentary was really nowhere to be seen in the third-quarter metrics or the updated full-year outlook, which continued to reflect extremely strong supply/demand conditions for logistics space, especially in the United States. Fueled by a record-setting cash re-leasing spread of 63.1% in the US, Prologis now sees FFO growth of 10.4% this year - up 20 basis points from its prior forecast - and expects NOI growth of 9.9% - up 10 basis points. Rexford ( REXR ) - which focuses exclusively on the Southern California region - has been a laggard after reporting mixed results, raising its full-year FFO outlook but recording a sequential deceleration in leasing activity. Outside of Southern California and a handful of coastal metros, however, demand continues to outstrip supply. Sunbelt-focused EastGroup ( EGP ) has been an upside standout, reporting strong results and raising its outlook. Bucking the trend of moderating leasing spreads seen across other industrial REITs, EGP reported an acceleration in cash leasing spreads to 39.1% in Q3, up from 38.3% in the prior quarter. Stag Industrial ( STAG ) reported similarly solid results and raised its full-year outlook.

{kind=link}

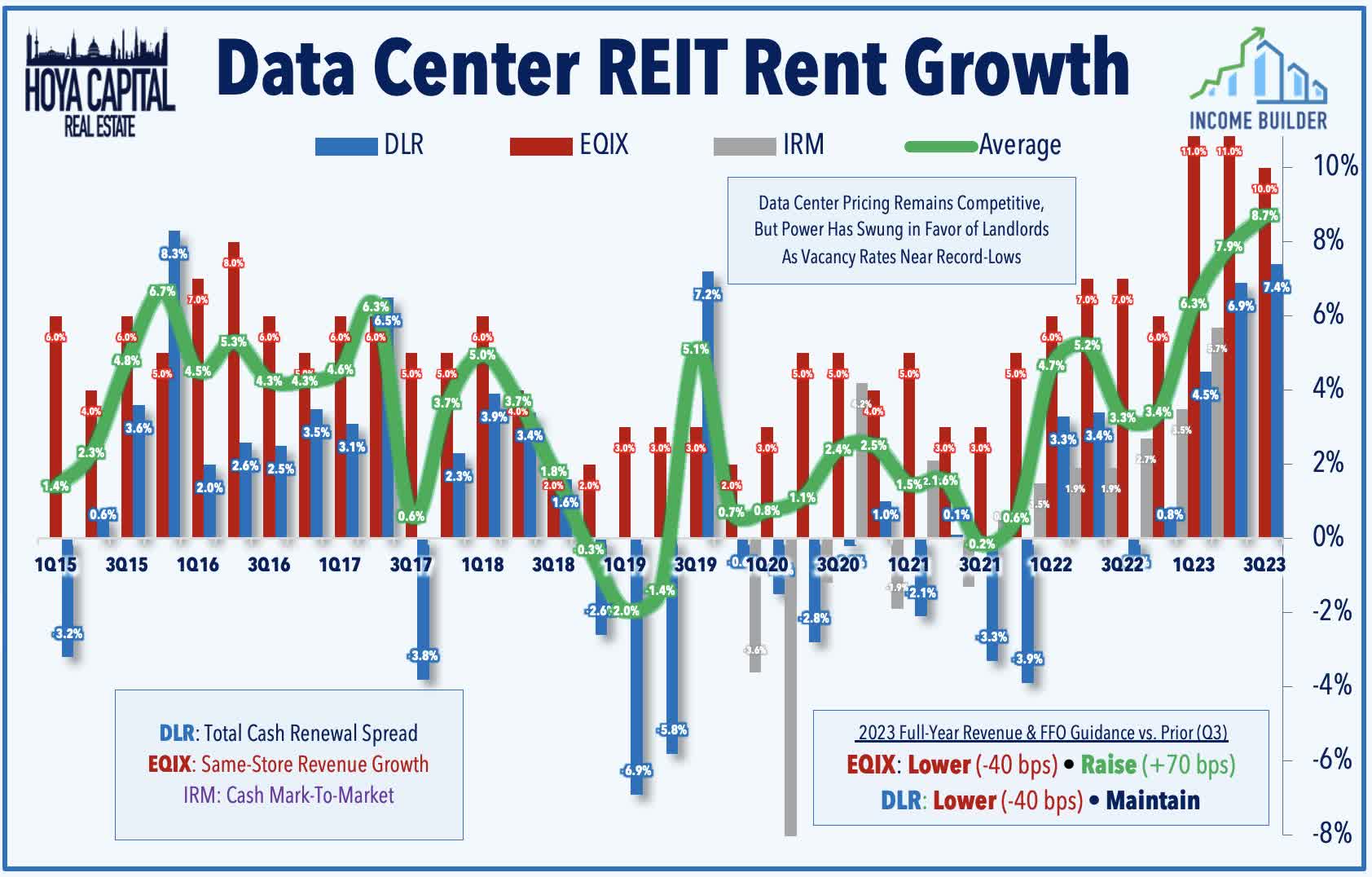

Data Center : (Halftime Grade: A-) Both data center REITs have reported results. Digital Realty ( DLR ) has been an upside standout after reporting strong results, with robust underlying pricing and AI-fueled demand trends partially offset by currency headwinds. DLR reported total bookings of $152M - its strongest quarter of leasing activity in a year - and achieved renewal rent growth of 7.4% - its best quarter for pricing since 2015. DLR now expects 5.0% rent growth on renewals - up from 4.0% last quarter - and expects same-capital cash NOI growth of 6.5% - up from 4.5% last quarter. DLR has been an active seller this year, raising $2.5B through non-core asset sales and joint venture monetizations in an effort to bolster its balance sheet and reduce its variable rate debt exposure, which remains relatively elevated at 14% of total debt. Underscoring this rate headwind, DLR maintained its guidance that its FFO will decline 1.5% this year despite a 17.2% jump in revenues. Equinix ( EQIX ) reported similarly solid results and raised its dividend by 25% to $4.26/share (2.5% dividend yield). EQIX now expects its full-year FFO to increase by 8.4% - up 70 basis points - while its revenue outlook was trimmed on FX adjustments. EQIX commented, "Demand remains strong. New logo growth is accelerating. Our pricing dynamics are very positive given the tight supply environment across many of our metros."

{kind=link}

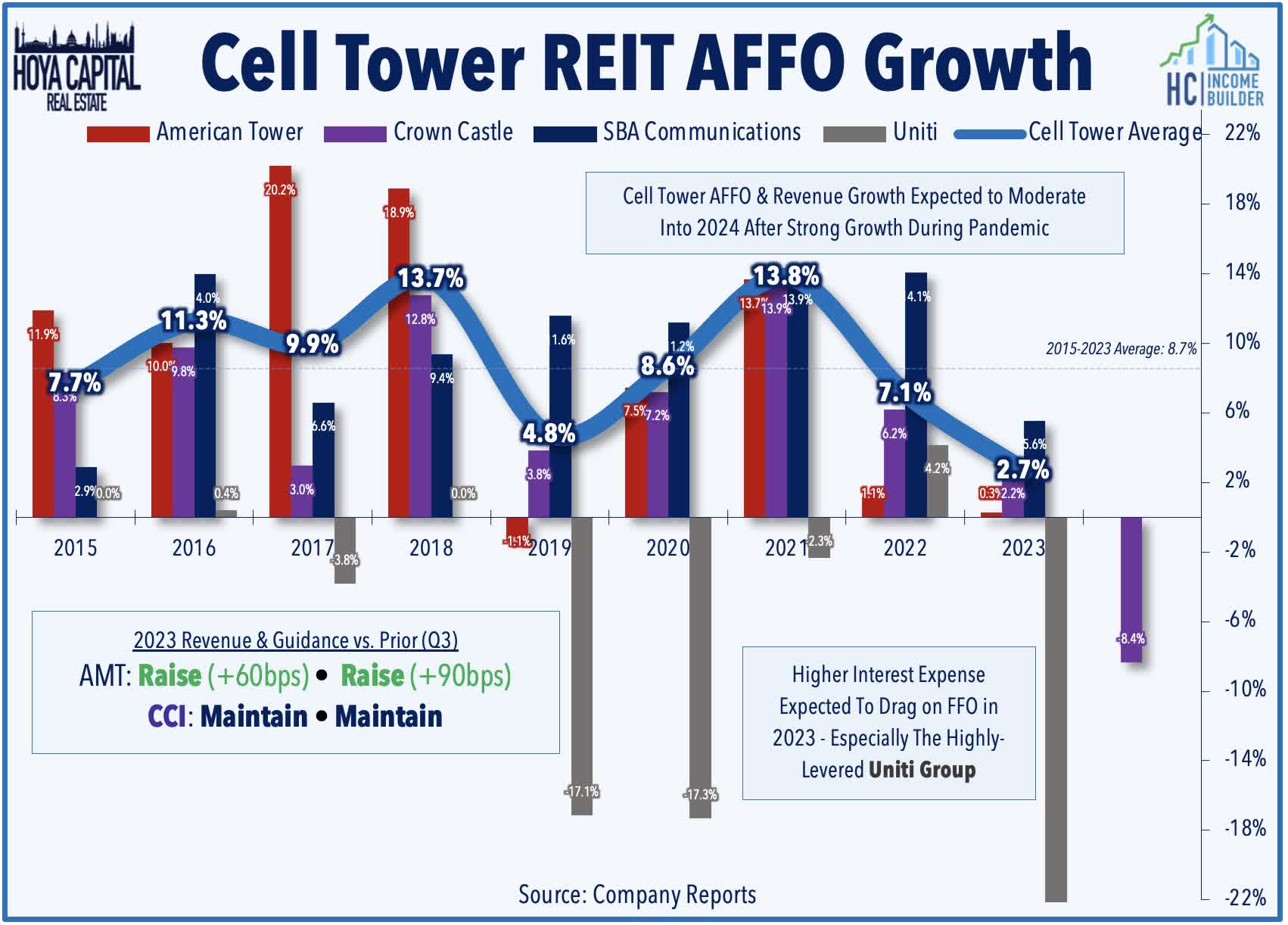

Cell Tower : (Halftime Grade: B+) Two of the three cell tower REITs have reported results. American Tower ( AMT ) has been the upside standout after reporting strong results and raising its full-year outlook while pushing back on concerns over a broader industry slowdown and noting the outperformance of its newly acquired data center business. Driven by domestic same-store ("organic billings") revenue growth of 6.3% - an acceleration from the 6.2% reported last quarter - AMT increased its full-year FFO growth target to 0.3% at the midpoint - up 90 basis points from its prior outlook. While AMT did not provide a full 2024 outlook, it noted that it expects continued same-tower revenue growth of "at least 5% in the U.S. and Canada segment between 2023 and 2027." Crown Castle ( CCI ) reported mixed results, maintaining its full-year 2023 outlook, but provided a downbeat initial 2024 outlook driven by higher interest expense. CCI continues to expect FFO growth of 2% this year, but forecasts an 8% decline in FFO in 2024, commenting that it expects the "low-point of AFFO to occur during the first half of 2024, with growth expected in the second half of the year and beyond." Despite having an investment-grade balance sheet with 86% of its debt at fixed interest rates, the updated outlook notes that interest expense is still expected to soar 22% in 2023 from a year earlier - amounting to a $0.35/share negative impact - and is expected to rise by another 12% in 2024 - an additional $0.12/share drag. Property-level metrics remain steady, with CCI forecasting organic growth (excluding Sprint cancellations) of 4.8% next year - up from 4.1% in 2023 - comprised of 4.5% growth from towers, 13% from small-cells, and 3% from fiber.

{kind=link}

Retail REIT Halftime Report

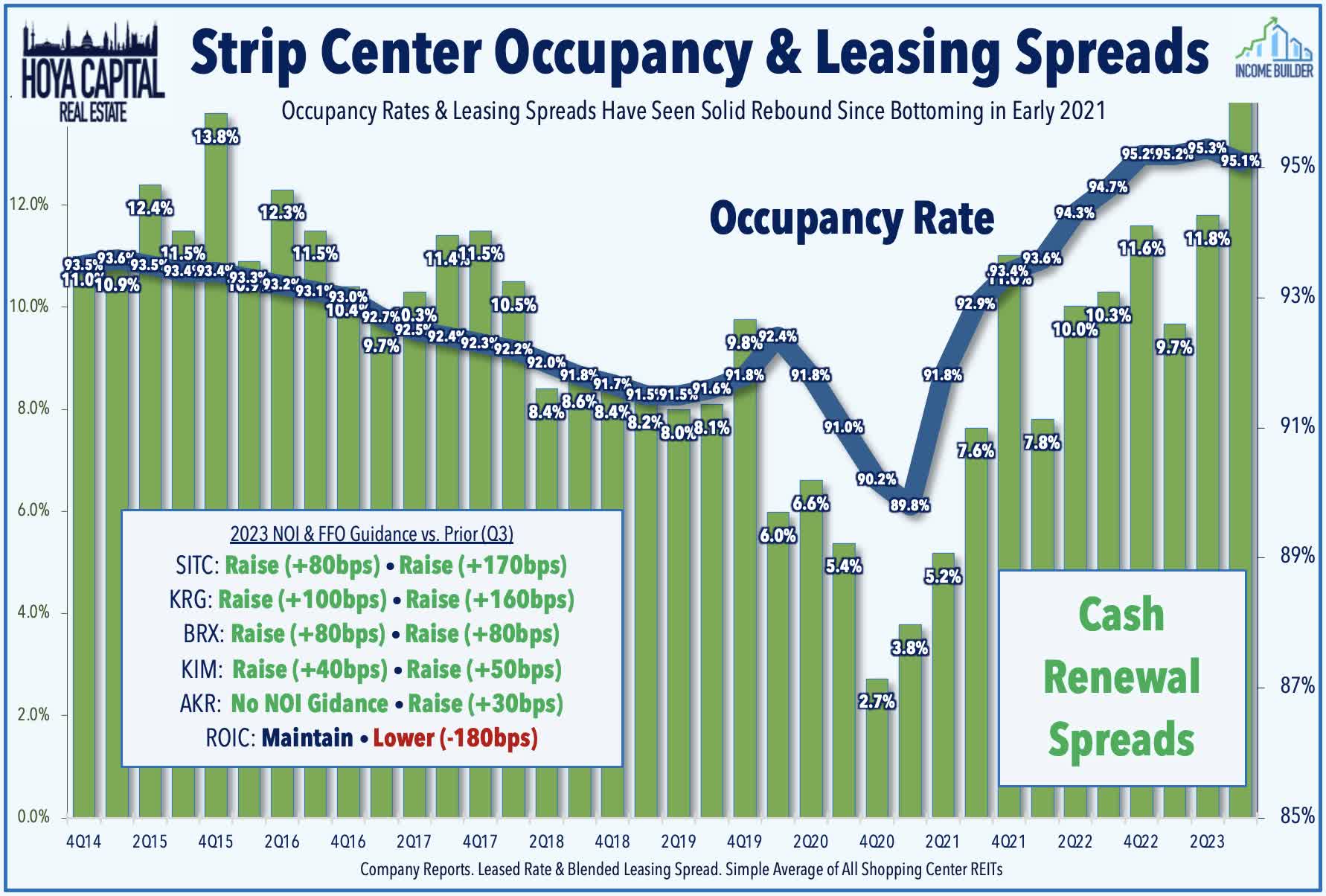

Strip Centers : (Halftime Grade: A-) S ix of 16 strip center REITs have reported results thus far, with five of these six REITs raising their full-year FFO outlook. Kimco ( KIM ) - the largest strip center REIT - has been an upside standout, boosting its full-year outlook and dividend. KIM now expects its full-year FFO to decline 0.9% at the midpoint of its range - a 40 basis point improvement from last quarter - and expects NOI growth of 2.0%, up from 1.5% last quarter. Demand remains robust for well-located strip center space, as KIM noted that it leased 2.1M square of space in Q3, achieving blended rent of 13.4%, the highest level of combined leasing spreads in six years. Pro-rata portfolio occupancy ended the quarter at 95.5%, increasing 20 basis points year-over-year. Additionally, Kimco became the 70th REIT to raise its dividend this year, hiking its payout by 4.3% to $0.24/share (5.9% dividend yield). Retail Opportunity ( ROIC ) has been a laggard, however, after reporting mixed results and lowering its full-year FFO outlook on higher interest expense. ROIC now expects its full-year FFO to decline 3.6% - a 180 basis point downward revision. Property-level fundamentals remained strong, as ROIC maintained its same-store NOI growth at 3.5%, achieving impressive rent spreads of 36.0% on new and renewed leases in Q3, resulting in a 7.2% overall increase in base rents. ROIC commented, "demand continues to be consistently strong with a broad range of new tenants actively seeking space."

{kind=link}

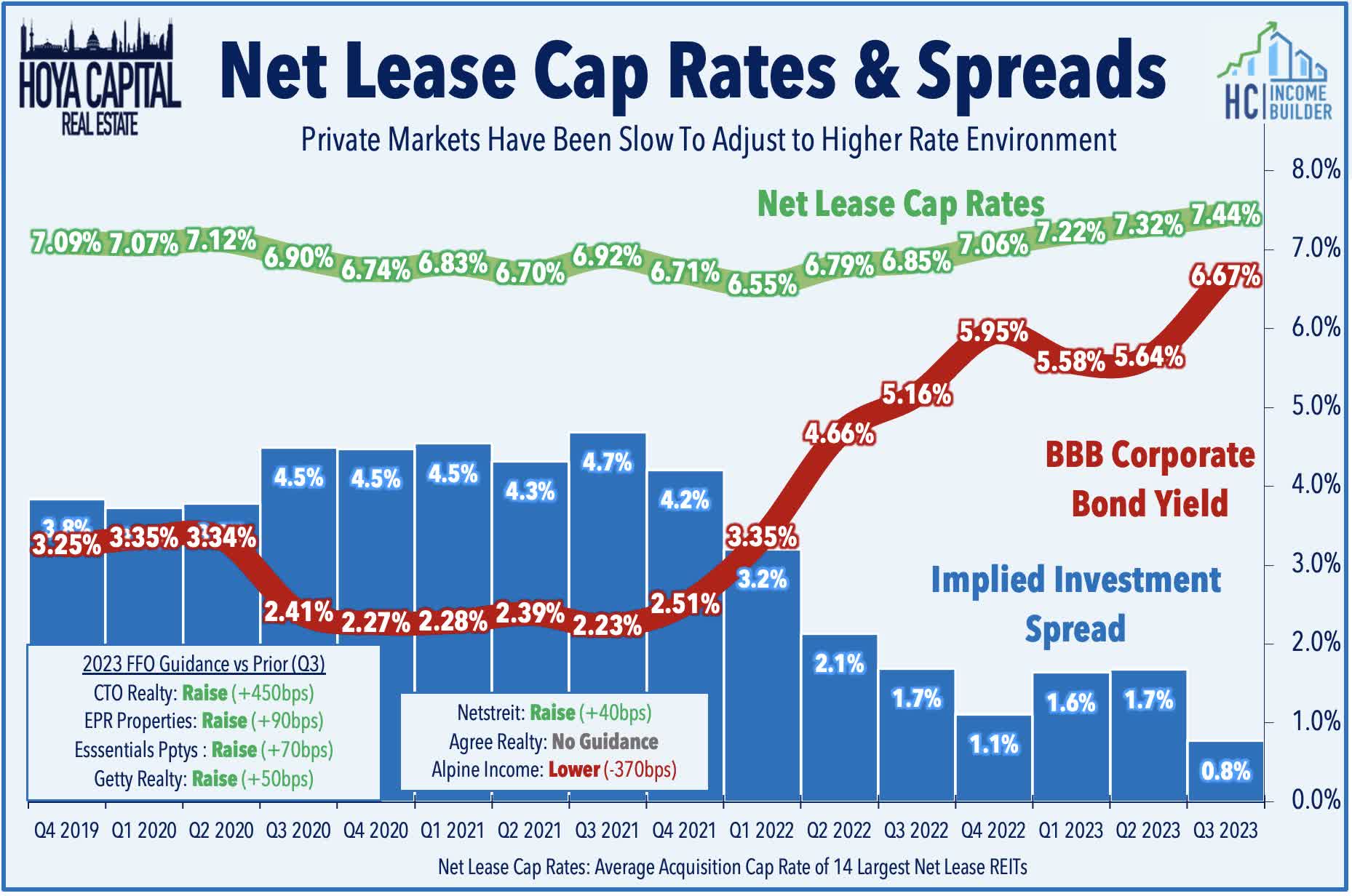

Net Lease : (Halftime Grade: B+) We've seen results from seven of the 16 net lease REITs, four of which have raised their full-year FFO outlook. Results have shown that these REITs are among the few active buyers left across the real estate industry amid the surge in financing costs, but also that private market pricing has been slow to reflect the surge in rates. Among the seven net lease REITs that have reported results thus far, acquisition cap rates have trended higher by only 20 basis points from last quarter, pressuring the implied net investment spread to below 1%. Agree Realty ( ADC ) has remained among the most active buyers across the REIT space, continuing to plow ahead with acquisitions, buying another $398.3M in properties at an average cap rate of 6.9%. Five of the six net lease REITs that provide FFO guidance raised their outlook. Essential Properties ( EPRT ) boosted its full-year FFO growth guidance to 7.5% - up 70 basis points - and provided initial 2024 guidance calling for FFO growth of another 5.4%. EPR Properties ( EPR ) raised its full-year FFO growth guidance to 9.6% - up 90 basis points - driven by "significant deferral collections" and the improved outlook for movie theater operator Regal. Netstreit ( NTST ) raised its full-year FFO growth outlook of 5.2% - up 40 basis points. Getty Realty ( GTY ) boosted its full-year FFO growth target to 4.9% - up 50 basis points - while also boosting its dividend by 4.7%. Alpine Income ( PINE ) is the lone net lease REIT to lower its FFO outlook, pressured by rising interest expense and the bankruptcy of one tenant.

{kind=link}

Mortgage REITs Halftime Report

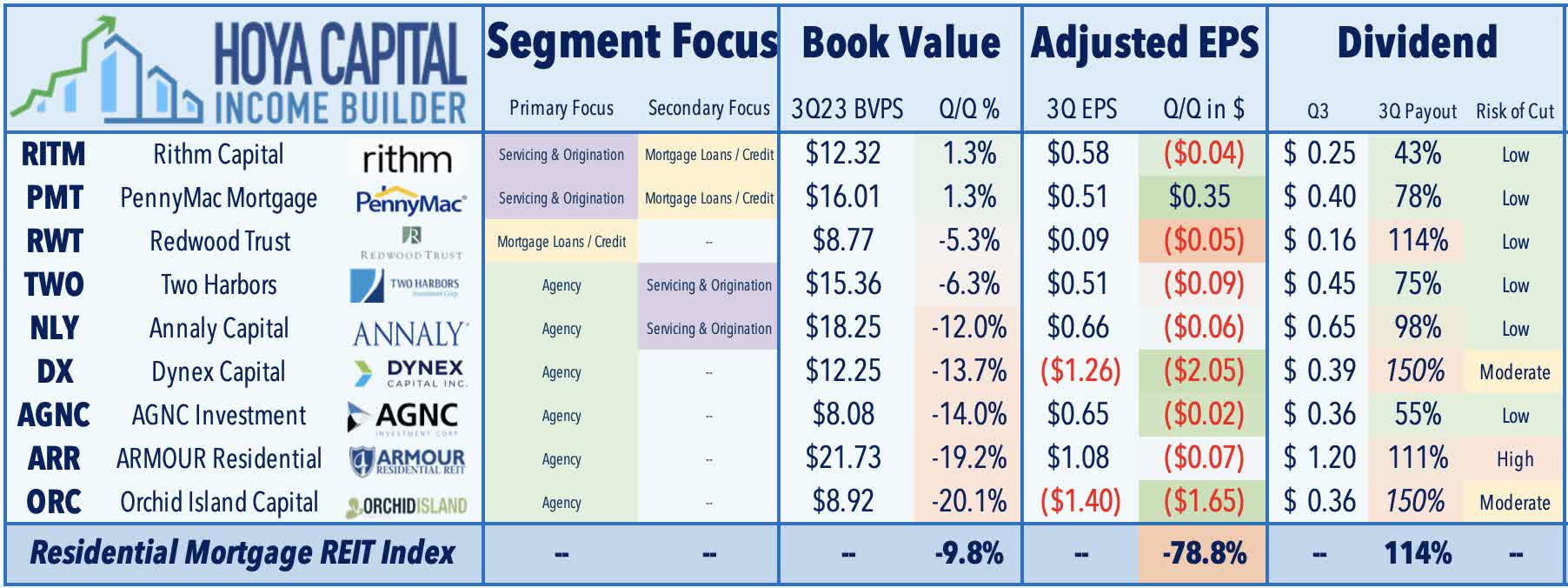

Residential mREITs : (Halftime Grade: C-) We've seen results from 9 of the 21 residential mREITs. Results have been ugly - with some exceptions - as the resurgence in benchmark interest rates and the widening of MBS spreads resulted in a significant deterioration in book values for agency-focused mREITs. AGNC Investment ( AGNC ) - the largest pure-play agency mREIT - has been a notable laggard after reported that its BVPS dipped 14% in Q3 and estimated that its current BVPS as of last week had dipped another 14-15%. The five agency mREITs reported an average decline in Book Value Per Share ("BVPS") of 15% in Q3. Not all residential mREITs have been negatively impacted by the surge in interest rates. PennyMac ( PMT ) - which focuses on the inversely-rate-sensitive Mortgage Servicing Rights ("MSR") business - surged after reporting very strong results, noting that its BVPS increased by 1.2% in Q3. Fellow services-focused mREIT, Rithm Capital ( RITM ) has also been a notable upside standout after it reported that its BVPS increased 1%.

{kind=link}

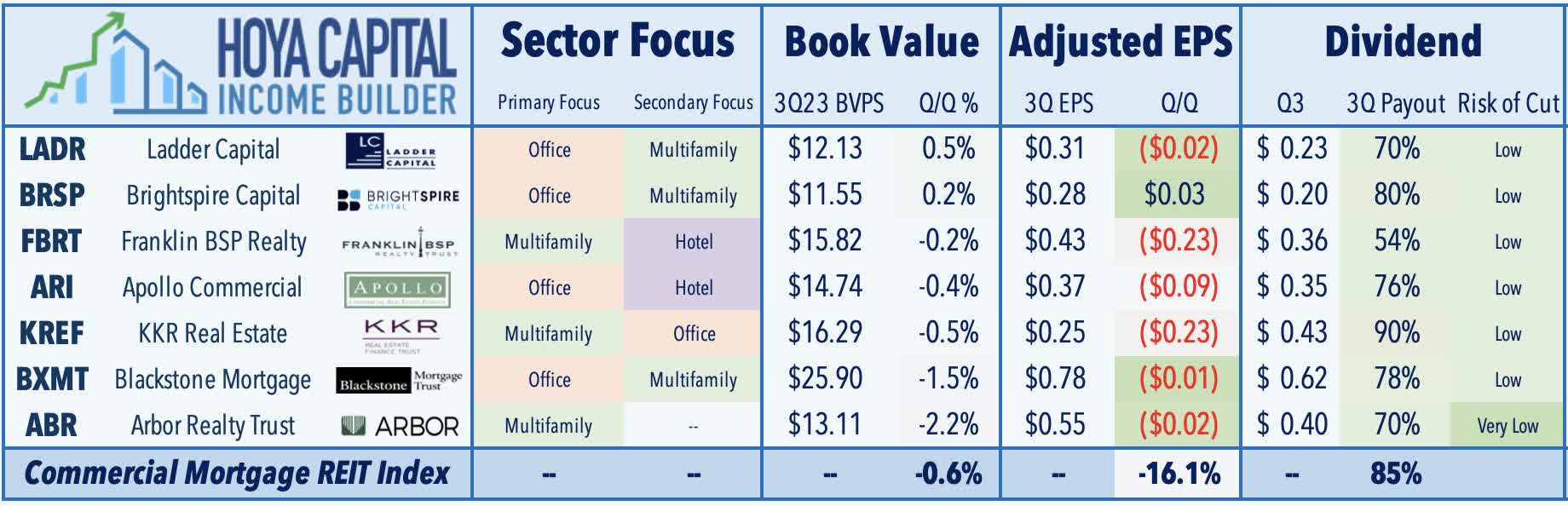

Commercial mREITs : (Halftime Grade: B+) On the commercial mREIT side, we've seen results from 7 of the 17 commercial mREITs, where the movement in BVPS remains far more muted on a quarter-to-quarter basis with a sequential average change of -0.6%. Two REITs have reported a sequential increase in BVPS: Ladder Capital ( LADR ) and Brightspire Capital ( BRSP ) - each of which focus on office and residential lending. KKR Real Estate ( KREF ) - which focuses on residential and office lending - has also been an outperformer after recording comparable EPS of $0.25 - topping the $0.11 consensus. On the downside, multifamily-focused lender Arbor Realty ( ABR ) dipped after it reported an uptick in delinquency rates, noting that it now has twelve non-performing loans with a carrying value of $137.9M, up from seven loans with a carrying value of $122.4M last quarter. Blackstone Mortgage ( BXMT ) - the largest commercial mREIT - has also lagged after reporting an uptick in delinquency rate on its office loans - which comprise a third of its portfolio - and noted that it has increased its CECL reserve on its office assets by more than 10X in the past year, implying an average decline of over 50%.

{kind=link}

Previewing The Second-Half of Earnings

At the halfway point of earnings season, REIT earnings results have been stronger than expected - and certainly stronger than the recent dismal share price performance of REITs would indicate. Of the 49 equity REITs that have provided updated full-year Funds From Operations ("FFO") guidance, 31 REITs have increased their forecast, 11 have maintained, and 7 have lowered their outlook. Among the 30 REITs that adjusted their FFO forecast, 82% were upward revisions, while just 18% were downward guidance revisions. Consistent with the broader "higher for longer" macroeconomic story of 2023, resilient pricing power has been a common thread across most property sectors - notably in data center, retail, and single-family residential REITs - but so have stubbornly persistent expense pressures. Residential REITs, in particular, continue to see insurance and property taxes rising by double-digits across most markets and segments. Soaring interest expense is the primary culprit behind the handful of downward guidance revisions, a theme that will be seen with greater frequency in the back half of earnings season, given the composition of generally smaller and more highly-levered names. We'll continue to provide real-time coverage and follow-up analysis articles for Hoya Capital Income Builder members throughout earnings season.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

REITs: Darkest Before The Dawn