REIT - REITs Lead Resurgence

2023-11-05 09:00:00 ET

Summary

- U.S. equity and bond markets posted their best week of the year after employment data showed early evidence of the long-elusive cooldown in labor markets.

- After dipping into "correction territory" last Friday, the S&P 500 posted five straight days of gains to finish the week higher by 5.8% - its best week since late 2022.

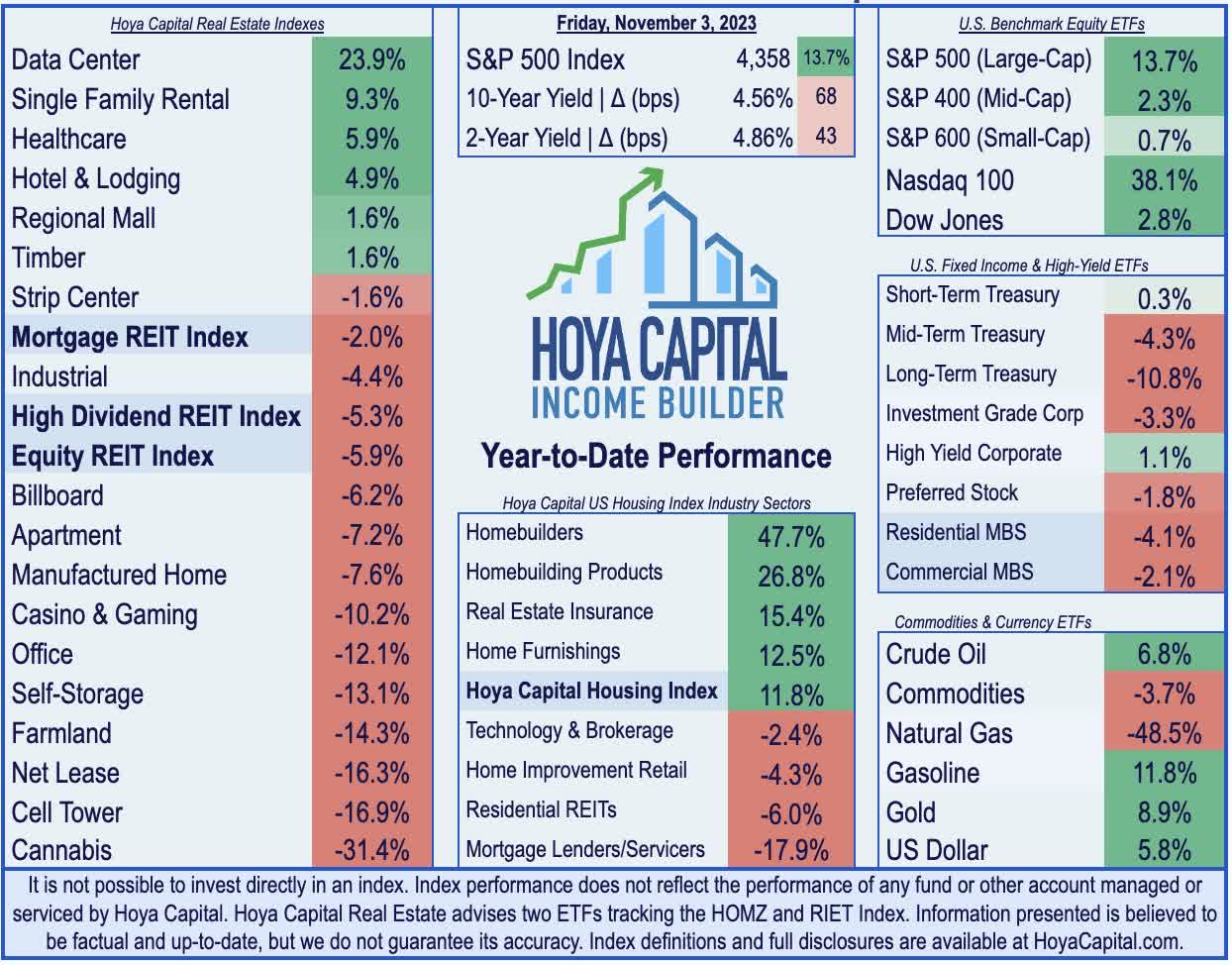

- Real estate equities - the "punching bag" of the Fed's tightening cycle - posted their best week since April 2020, lifted by the interest rate retreat and surprisingly strong earnings results.

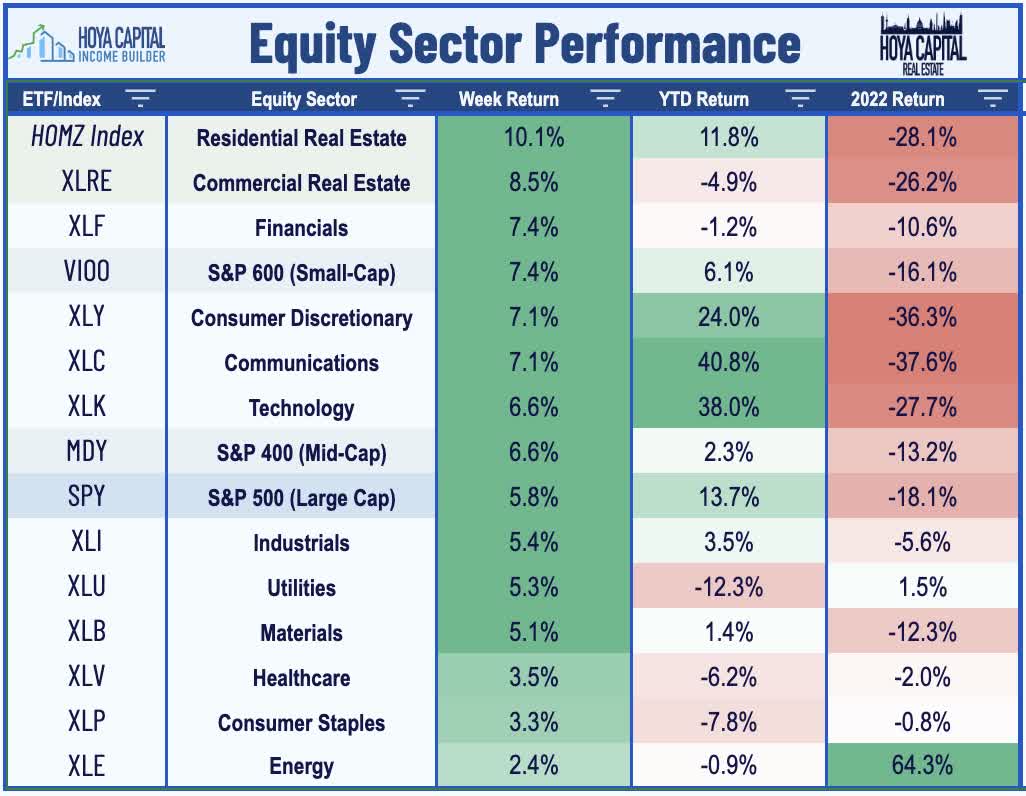

- Highlighted by double-digit gains from more than 100 U.S. REITs, the Equity REIT Index rallied 8.9% this week, with all 18 property sectors in positive territory, while the Mortgage REIT Index surged more than 13%.

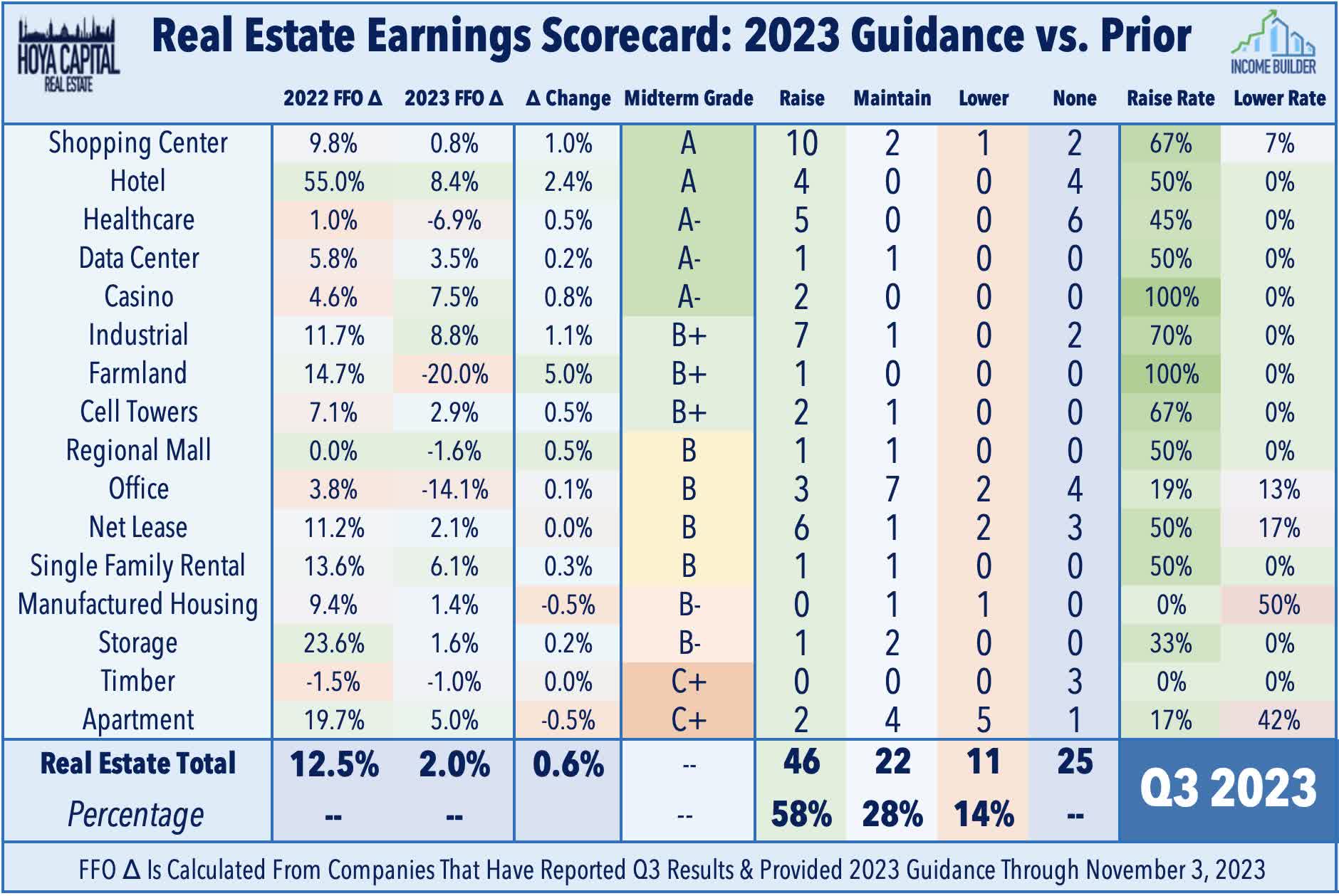

- A half-dozen REITs hiked their dividends this week, lifting the full-year total to over 70. Among the 57 REITs that adjusted their FFO forecast this earnings season, 81% were upward revisions, while just 19% were downward guidance revisions.

Real Estate Weekly Outlook

U.S. equity and bond markets posted their best week of the year after employment data showed evidence of the long-elusive cooldown in labor markets, while commentary from Federal Reserve Chair Powell opened the door for a pivot toward less restrictive monetary policy by early next year. While other forward-looking indicators have provided ample evidence of moderating inflationary pressures for over a year, labor markets are finally showing the lagged effects of historically swift monetary tightening, underscored by a rise in the unemployment rate to two-year highs - labor market conditions that are generally softer than the two-year period immediately before the pandemic, during which inflation averaged under 2%.

{kind=link}

After dipping into "correction territory" last Friday, the S&P 500 posted five straight days of gains to finish the week higher by 5.8% - its best week since late 2022. The other major benchmarks posted stronger gains, as the Mid-Cap 400 advanced 6.6% while the Small-Cap 600 rallied 7.4%. Real estate equities - which have been the "punching bag" of the Fed's tightening cycle - posted their best week since April 2020, lifted by the interest rate retreat and a surprisingly strong slate of earnings reports. Highlighted by double-digit gains from more than 100 U.S. REITs, the Equity REIT Index rallied 8.9% this week, with all 18 property sectors in positive territory, while the Mortgage REIT Index surged more than 13%. Homebuilders soared over 15% this week as mortgage rates pulled-back from generational highs.

{kind=link}

Central banks were in the spotlight, and while there was little doubt that the Federal Reserve would hold interest rates at the current 5.50% upper bound, traders interpreted Fed Chair Powell's remarks as slightly less "hawkish" than expected. Powell commented that financial conditions have “tightened significantly in recent months" and conceded that the full effects of tightening had yet to be felt. Combined with the soft employment data, bonds caught a strong bid across the curve, sending the 10-Year Treasury Yield plunging to 4.56% - down 29 basis points on the week - while the 2-Year Treasury Yield dipped 16 basis points to 4.86%. Helping the inflation and interest rate outlook, WTI Crude Oil prices declined another 4% this week to around $80/barrel - now roughly 15% below the highs in late September. The US Dollar Index dipped by over a full percentage point - posting its worst week of the year - while the CBOE Volatility Index - a measure of equity market volatility - posted its most significant weekly decline since 2020.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

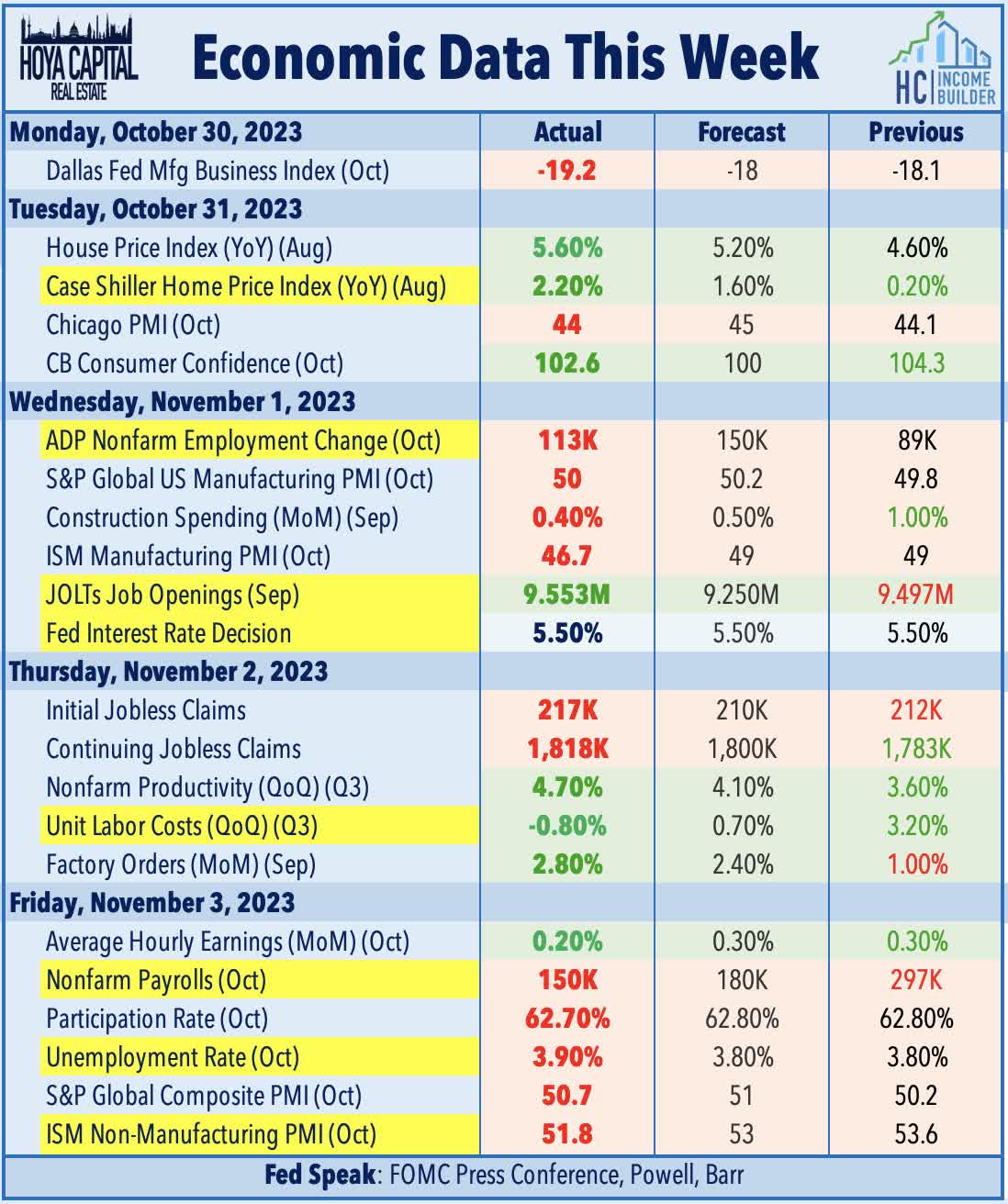

The long-awaited cooldown in labor markets - which most Fed officials have pinned their "pivot" upon - may finally be upon us, according to the latest BLS nonfarm payrolls report this week. The U.S. economy added just 150k jobs in October - below consensus estimates of 180k - while net revisions subtracted 101k jobs to the prior two months, the ninth downward revision in the past ten reports. Trends seen in the Household Survey - which is used to calculate the unemployment rate and participation rate - were also notably softer than the Establishment Survey, which drives the job growth metrics. The U3 unemployment rate rose to 3.9% - the highest level since January 2022 and above the 3.8% average in the pre-pandemic period from 2018 through 2019. The soft report followed a similarly weak slate of reports earlier in the week, including a "miss" on ADP Payrolls, Initial Jobless Claims, and Continuing Jobless Claims. JOLTS data - which is a month lagged - showed stronger-than-expected job openings during the prior month.

{kind=link}

Average hourly earnings ("AHE") - a key inflation indicator - provided additional encouraging evidence of normalizing labor market conditions following pandemic-era shortages. AHE rose 0.2% in October, which was lower than expected, and continued the trend of moderation observed in the annual increase for both the 'All Employees' and 'Nonsupervisory Employees' indexes, which each declined to their softest since June 2021. Since the start of 2023, AHE for all employees has averaged 3.9% on an annualized basis - slightly above the 3.3% increase in 2019 in a year that CPI inflation averaged just 1.8% - suggesting that concerns over wage-driven inflation - and the feared "wage-price spiral" - are likely unwarranted at this point. Earlier in the week, the BLS' productivity report showed that unit labor costs - a separate measure of hourly compensation - unexpectedly declined in the third quarter. On a year-over-year basis, the report showed a 3.9% increase in hourly compensation, offset by a 4.7% rise in productivity.

{kind=link}

Equity REIT Week In Review

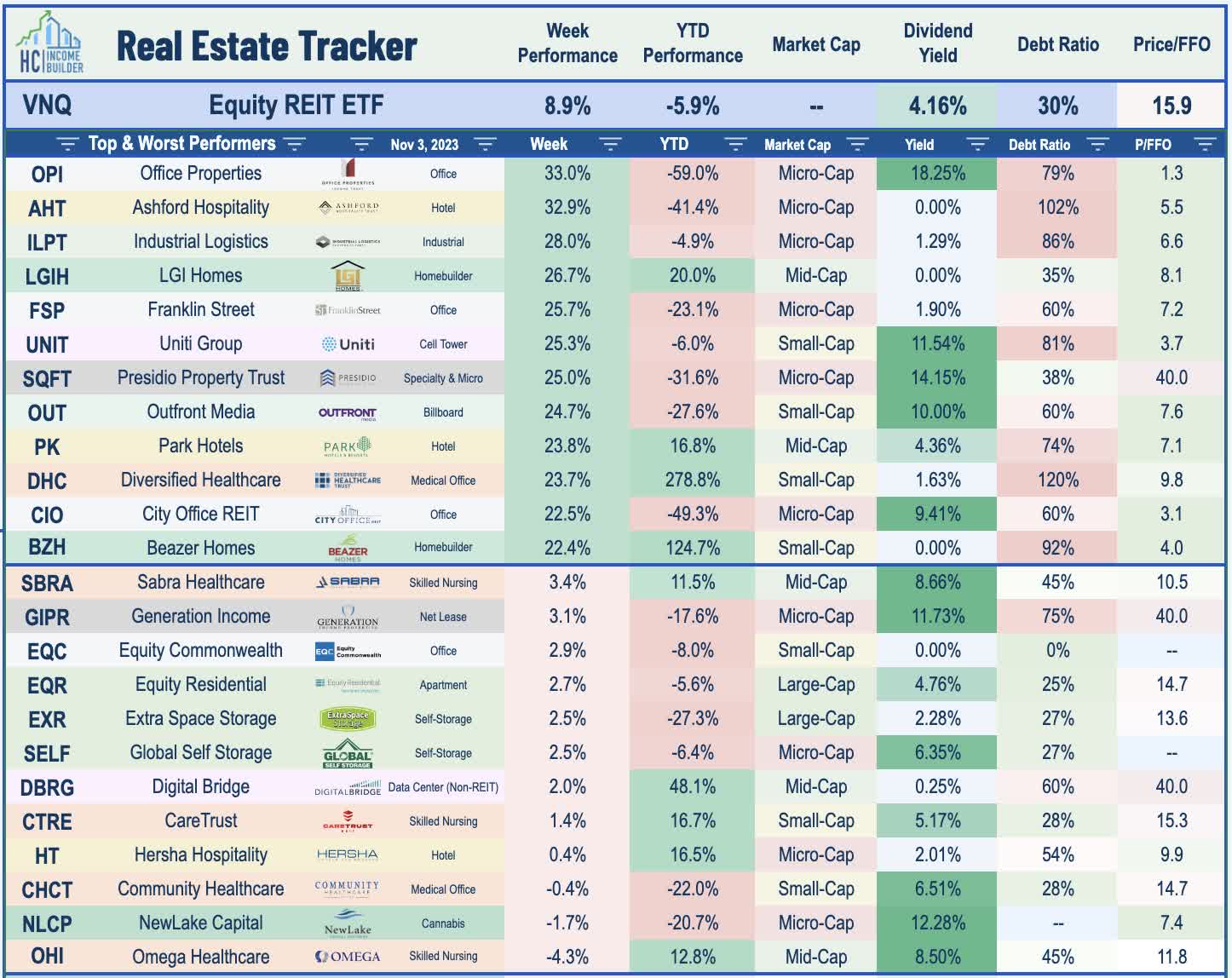

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Early in the week, we published REITs: Darkest Before The Dawn , which discussed how REITs were continuing to trade at near their lowest valuations since the Great Financial Crisis despite a solid start to earnings season. Fueled by the retreat in interest rates and a surprisingly strong slate of earnings results, REITs delivered a frenetic rally over the subsequent days with over 20 REITs soaring by more than 20% this week, and over 100 REITs gaining at least 10%. As we'll discuss next week in our Earnings Recap, results across the real estate sector have been notably stronger than expected. Of the 79 equity REITs that have provided updated full-year Funds From Operations ("FFO") guidance, 46 REITs have increased their forecast, 22 have maintained, and 11 have lowered their outlook. Among the 57 REITs that adjusted their FFO forecast, 81% were upward revisions, while just 19% were downward guidance revisions. By comparison, FactSet reports that 54% of S&P 500 components have raised the full-year EPS outlook, while 46% have reduced their guidance. Below, we discuss some highlights of the past week.

{kind=link}

As anticipated, REIT M&A has remained a major theme this earnings season, with another pair of mergers announced this week as equity REITs have become the "only game in town" for potential sellers given the scarcity of debt capital. Realty Income ( O ) - the largest net lease REIT - announced that it will acquire Spirit Realty ( SRC ) - the fifth largest net lease REIT - in a $9.3B all-stock deal at a 15% premium to SRC's last closing price. Realty Income finished the week higher by about 4%, while Spirit surged 20%. Realty Income noted that the deal is expected to add more than 2.5% to annualized adjusted FFO per share and - perhaps most important - be leverage-neutral, with no new external capital anticipated to be required to finance the acquisition. Elsewhere, medical office building REITs Healthpeak Properties ( PEAK ) and Physicians Realty ( DOC ) agreed to merge in an all-stock merger of equals. PEAK ended the week higher by about 5%, while DOC gained 7%. The combined REIT will be comprised of 52M square feet of properties, including 40M square feet of outpatient medical office building ("MOB") properties with a concentration in Sunbelt markets. The transaction is projected to be accretive to adjusted FFO for both PEAK and DOC, resulting from cost-cutting synergies of at least $40M in 2024 and up to $60M by the end of 2025. The combined company is expected to pay an annualized dividend of $1.20 per share, consistent with PEAK's current dividend level.

{kind=link}

Hotel : Among the strongest-performing sectors this week, hotel REITs were propelled by a very strong slate of earnings reports. Park Hotels ( PK ) surged 24% after raising its full-year guidance and declaring a special dividend. Citing strength in its urban portfolio and the exit from the troubled San Francisco market, PK now expects full-year FFO growth of 28.2% - up from its prior outlook for 22.7% growth. Summit Hotel ( INN ) surged nearly 20% after reporting similarly strong results and lifting its full-year outlook. Host Hotels ( HST ) rallied 11% after lifting its full-year FFO growth outlook to 7.5% - a 390 basis point increase from last quarter - and reiterated its outlook for full-year Revenue Per Available Room ("RevPAR") growth of 8.0%, which would be 5.6% above 2019 levels. RLJ Lodging ( RLJ ) gained 13% after reporting strong results and noting that its RevPAR exceeded 2019 levels for the first time in September. DiamondRock ( DRH ) gained 15% after reporting decent third-quarter results, noting that its comparable RevPAR was 8% above 2019-levels. DRH noted that leisure demand remains robust and that it is "not seeing consumer weakening," but noted that business travel remains well below pre-pandemic levels, citing softer demand from large corporations. Xenia Hotels ( XHR ) gained 10% after reporting decent results and updating its guidance to show a modest increase in its full-year FFO outlook but a slight decrease in its RevPAR target, citing a "moderating" leisure demand and ongoing renovation activity. Recent TSA Checkpoint data shows that throughput climbed to 104.9% of 2019 levels in October.

{kind=link}

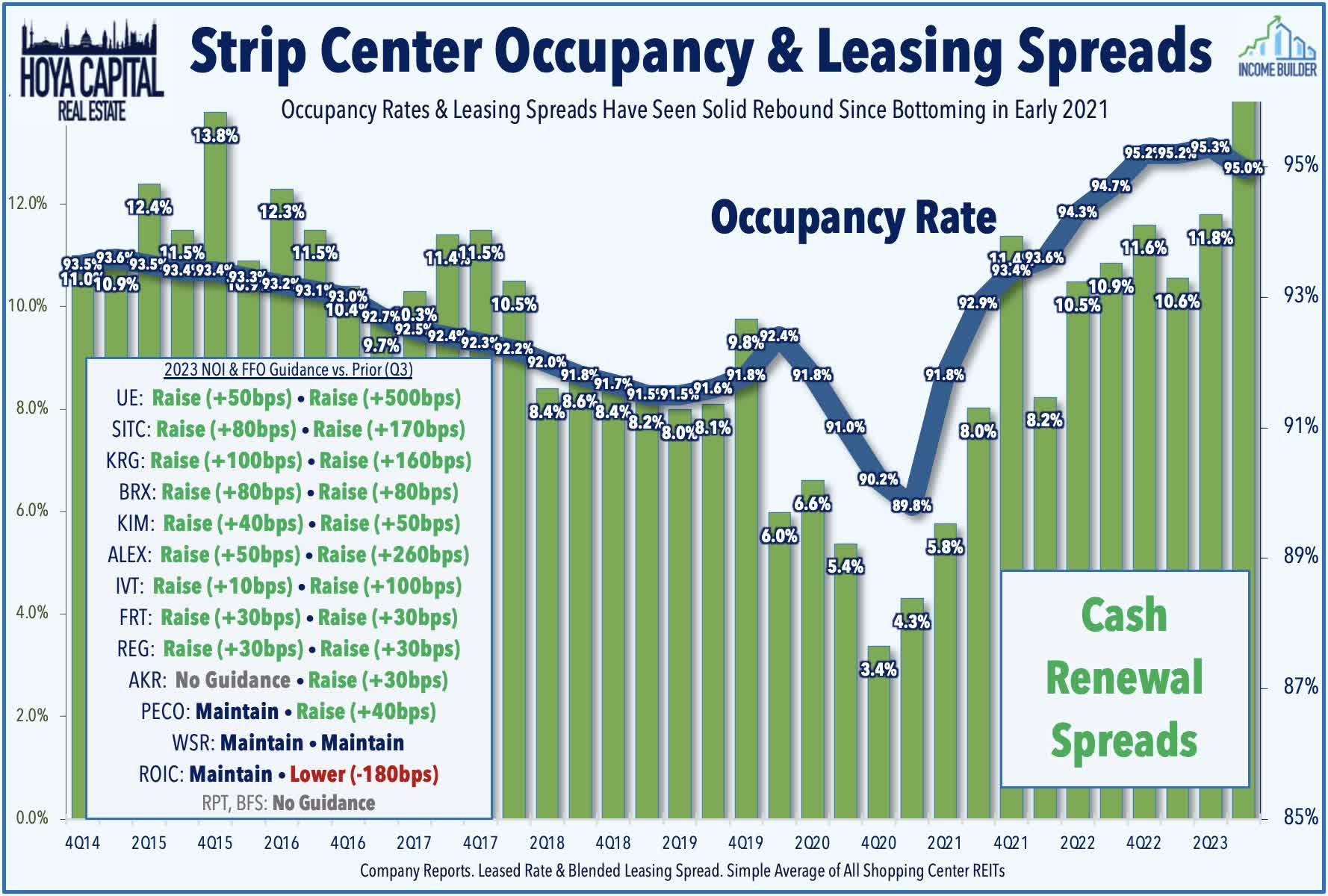

Strip Centers : The very strong earnings season for strip center REITs continued this week. Kite Realty ( KRG ) rallied 12% after raising its full-year outlook and hiking its dividend by 4%. Fueled by impressive blended leasing spreads of 14.2%, KRG now expects full-year FFO growth of 4.1% - up 160 basis points from last quarter. Brixmor Property ( BRX ) gained 9% after reporting similarly impressive results and hiking its dividend by 5%. Lifted by a record-setting 22.3% blended leasing spread, BRX now expects full-year FFO growth of 4.1% - up 80 basis points. Regency Centers ( REG ) advanced 9% after raising its full-year outlook and also raising its dividend by 3%, becoming the 72nd REIT to raise its dividend this year. Regency now expects full-year FFO growth of 1.0% - up 20 basis points from its prior outlook - and expects same-store NOI growth of 3.5% - also up 20 basis points. Federal Realty ( FRT ) gained 3% after reporting strong leasing activity and also raising its full-year outlook. SITE Centers ( SITC ) surged 15% after reporting similarly strong results, raising its full-year outlook, and also announcing that it will spin-off its convenience store portfolio into a separate publicly-traded REIT to be named Curbline Properties (CURB). Elsewhere, Urban Edge ( UE ) surged 17% after significantly raising its full-year outlook. Like its aforementioned peers, leasing spreads were impressive with a 12.5% blended increase, and UE now expects full-year FFO growth of 2.1% - up 500 basis points from its prior outlook.

{kind=link}

Mall : Retail REIT earnings results were also fairly impressive in the long-troubled regional mall space. Simon Property ( SPG ) - the largest mall owner in the nation- rallied 13% after raising its full-year outlook to levels that are now above the 2019 baseline. Lifted by a recovery in occupancy rates to over 95%, SPG now expects full-year FFO growth of 0.3% at its revised midpoint, which would be 1.3% above its full-year 2019 FFO. While SPG no longer provides leasing spread metrics, SPG reported that its base minimum rents increased 2.9% year-over-year and commented that "tenant demand is strong, occupancy is increasing, and base minimum rent levels are at record levels." Macerich ( MAC ) finished higher by 16% this week after reporting in-line results and maintaining its full-year FFO outlook, which calls for an 8.2% decline. Rent spreads and occupancy trends continued to trend in a positive-direction, with blended leasing spreads of 10.6% in Q3 - its second-straight quarter of double-digit increases. Portfolio occupancy rose to 93.4% - still below the pre-pandemic average of around 94.5% - but up 80 basis points from last quarter and 170 basis points from last year.

{kind=link}

Billboard : Outfront Media ( OUT ) soared 25% this week - extending its rally to over 40% from its lows last month - after reporting stronger-than-expected results with strength in its traditional billboard segment offsetting continued struggles in its transit advertising business. OUT noted that billboard revenues grew 2.6% year-over-year - driven largely by digital billboard conversions - while transit revenues declined nearly 9%. OUT noted weak advertising demand from national television and technology companies but reported that its local business segment performed "extremely well" with revenue growth of 6%. Lamar Advertising ( LAMR ) surged more than 18% this week after reporting solid results and raising its full-year outlook. LAMR expects to "reach or slightly exceed the upper end" of its guidance, implying that its FFO will be roughly flat this year, up from its prior outlook calling for a roughly 2% decline. LAMR reported similar industry trends, with local and regional revenues posting 2.3% growth while national revenues decreasing 3.4%. LAMR reiterated that political spending will be a drag in Q4 compared to the record-spending levels in 2022, but that it has seen "strengthening" trends early in the fourth quarter, led by a rebound in the national segment.

{kind=link}

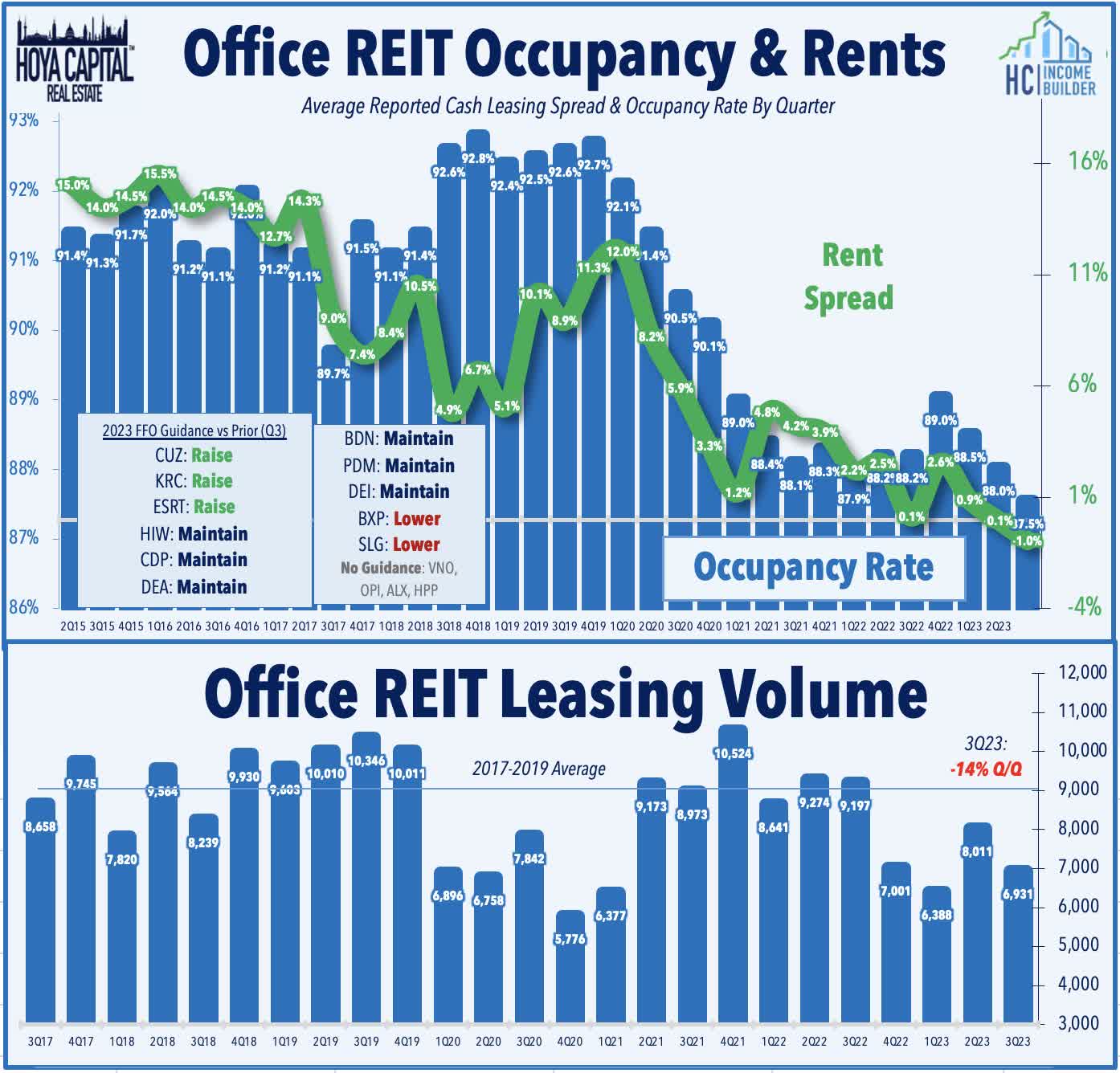

Office : Also delivering double-digit gains this week, office REITs rebounded as the back-half of earnings season proved to be surprisingly stronger than the initial slate of reports. Boston Properties ( BXP ) - the largest office REIT - rallied over 12% after reporting better-than-expected results, highlighted by a sequential acceleration in leasing volume. BXP recorded total leasing volume of 1.06M square feet - its highest in over a year - which lifted its occupancy rate higher by 50 basis points to 88.8%. BXP maintained its full-year outlook, calling for an FFO decline of 3.5%. West Coast-focused Hudson Pacific ( HPP ) - among the weakest-performing office REITs this year - rallied 20% after reporting total leasing volume of 519k SF - its strongest quarter of activity since Q2 of 2022. Douglas Emmett ( DEI ) advanced 16% after reporting in-line results and marginally increasing its full-year outlook. DEI focuses exclusively on the Los Angeles market, which has held up far better than the other major West Coast markets. DEI reported another quarter of solid leasing volume with 934k SF of total activity - slightly above its pre-pandemic average from 2017-2019 - but pricing trends have been notably weak, with cash spreads of -9.7%. Elsewhere, NYC-focused Paramount ( PGRE ) surged 13% after reporting similarly solid leasing trends, recording its strongest quarter for leasing volume in over a year at 227k SF - up from just 72k SF in Q2.

{kind=link}

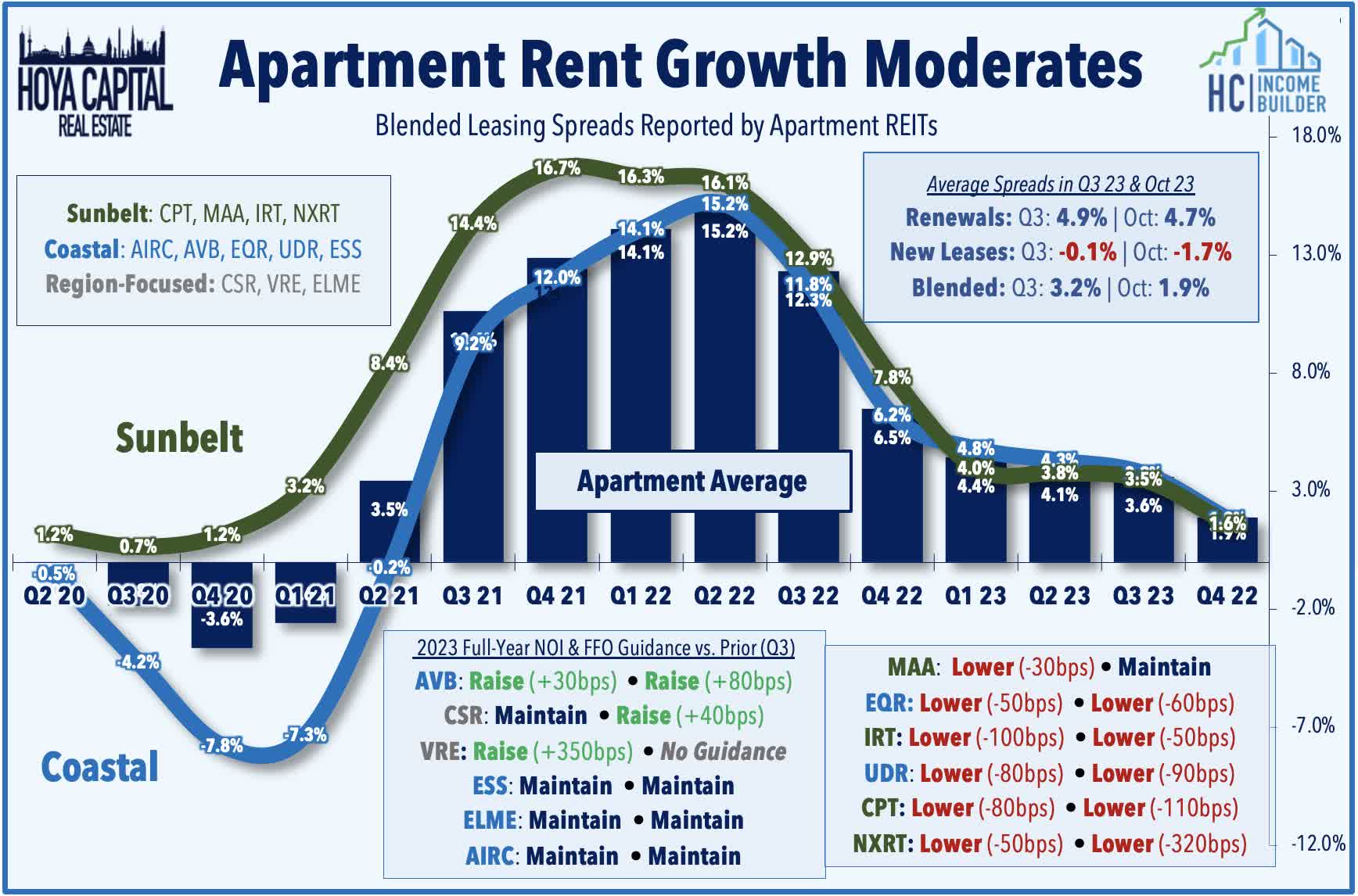

Apartment : Among the laggards this week, apartment REIT earnings results were among the few soft spots this earnings season, accounting for nearly half of the total downward guidance revisions across the REIT sector. Equity Residential ( EQR ) was the laggard this week after lowering its full-year outlook, citing weakness in its San Francisco and Seattle markets. Like its peers, EQR noted that relatively buoyant rent growth on renewals helped to keep overall rent spreads modestly positive, even as lease rates on new leases ticked negative in early Q4 amid supply headwinds in several major markets. On the upside, Sunbelt-focused Independence Realty ( IRT ) and NexPoint Residential ( NXRT ) each rallied 12% this week despite trimming their full-year earnings outlook. Apartment Income ( AIRC ) was also a notable upside standout after reporting solid results and maintaining its full-year outlook. AIRC reported the strongest third-quarter blended leasing spreads in the sector at 4.7% - comprised of 6.0% growth in renewal rents and a 3.6% increase on new leases. AIRC continues to expect sector-leading same-store NOI growth of 9.2% in 2023 and continues to expect its full-year FFO to be unchanged from 2022. AIRC also provided an initial 2024 outlook, noting that it expects same-store revenue growth of 3.5% at the midpoint of its outlook.

{kind=link}

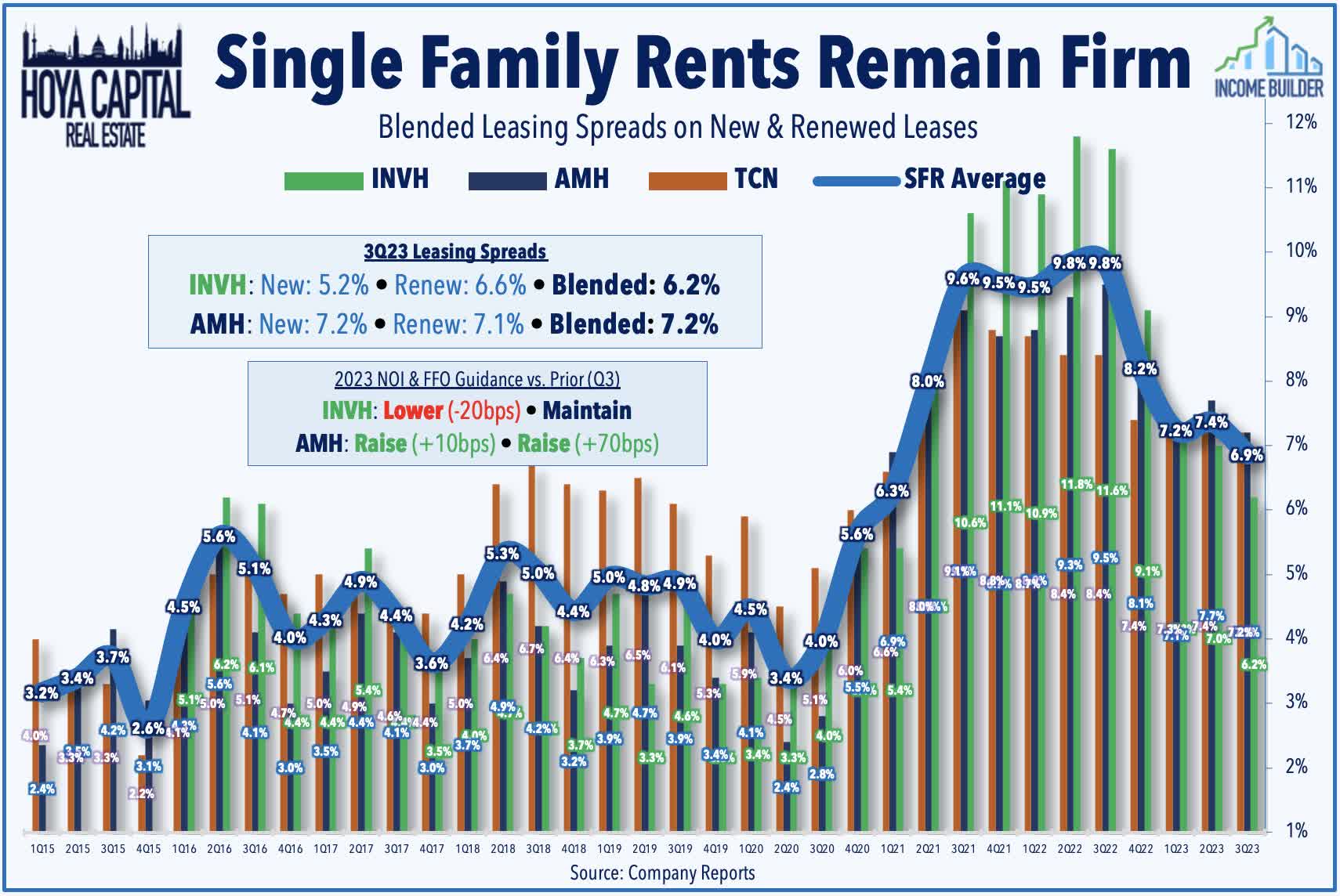

Single-Family Rental : Sunbelt-focused American Homes ( AMH ) rallied 12% this week after reporting strong results and raising its full-year outlook. Driven by impressive blended leasing spreads of over 7% - underscoring the continued lack of supply across single-family markets - AMH now expects full-year FFO growth of 7.1% - up 70 basis from last quarter - and expects same-store NOI growth of 4.9% - up 10 basis points from last quarter. Providing some initial commentary on 2024, AMH noted that it expects rent growth to be "better than historical averages" and noted that it has continued to throttle the increases on renewal leases, estimating that its "loss to lease" is still 4% below market rents. More generally, AMH commented, "The demand backdrop is fantastic. We'll be in a good position going into next year. Single-family sector and value proposition is as strong as it's ever been. So we have good expectations on continued strong rent growth."

{kind=link}

Mortgage REIT Week In Review

Posting a frenetic rebound following a skid of over 20% in the preceding six weeks, the iShares Mortgage Real Estate Capped ETF ( REM ) soared 13.4% this week - its best week since April 2020 - lifted by the retreat in interest rates and earnings results that were less ugly than feared. Beginning on the residential mREIT side, Two Harbors ( TWO ) soared over 30% after reporting that its Book Value Per Share ("BVPS") declined 6% in Q3 - less than feared - as credit-focused and services-focused mREITs continue to report stronger results than their agency-focused peers. Cherry Hill ( CHMI ) rallied 26% after reporting that its BVPS declined 3.9% in Q3 - the best among agency-focused mREITs - and noted that its distributable EPS was flat in Q3 at $0.16, which covered its $0.15 dividend. AGNC Investment ( AGNC ) rallied 19% this week - recovering from a dip of over 15% last week - after confirming its previously reported Q3 metrics showing a 19% decline BVPS, but provided upbeat commentary on economic return potential and reiterated that its current dividend level "remains well aligned with the return that we expect."

{kind=link}

Among the laggards this week on the residential side, Redwood Trust ( RWT ) gained just 3% after reporting that its BVPS declined 5% during the quarter - a bit softer than expected for the credit-focused mREIT - while noting that its distributable EPS fell to $0.09 - shy of its $0.16 dividend. Another credit-focused mREIT - Chimera ( CIM ) - gained 5% after reporting comparable EPS of $0.13 - shy of estimates - and noted that its BVPS declined 5% in Q3. CIM also trimmed its dividend for the second time this year, one of twelve residential mREITs to lower its dividend this year. New York Mortgage ( NYMT ) also gained 5% after reporting that its BVPS declined 9% in Q3 and warned that its earnings are expected to remain below its current dividend based on current market conditions. Great Ajax ( AJX ) - which plunged 35% last week after Ellington Financial called off its planned acquisition - gained 8% after reporting in-line results, noting that its BVPS declined 6.7% in Q3. AJX also slashed its dividend for the second time this year, reducing its payout by 45% to $0.11/share (10.0% dividend yield).

{kind=link}

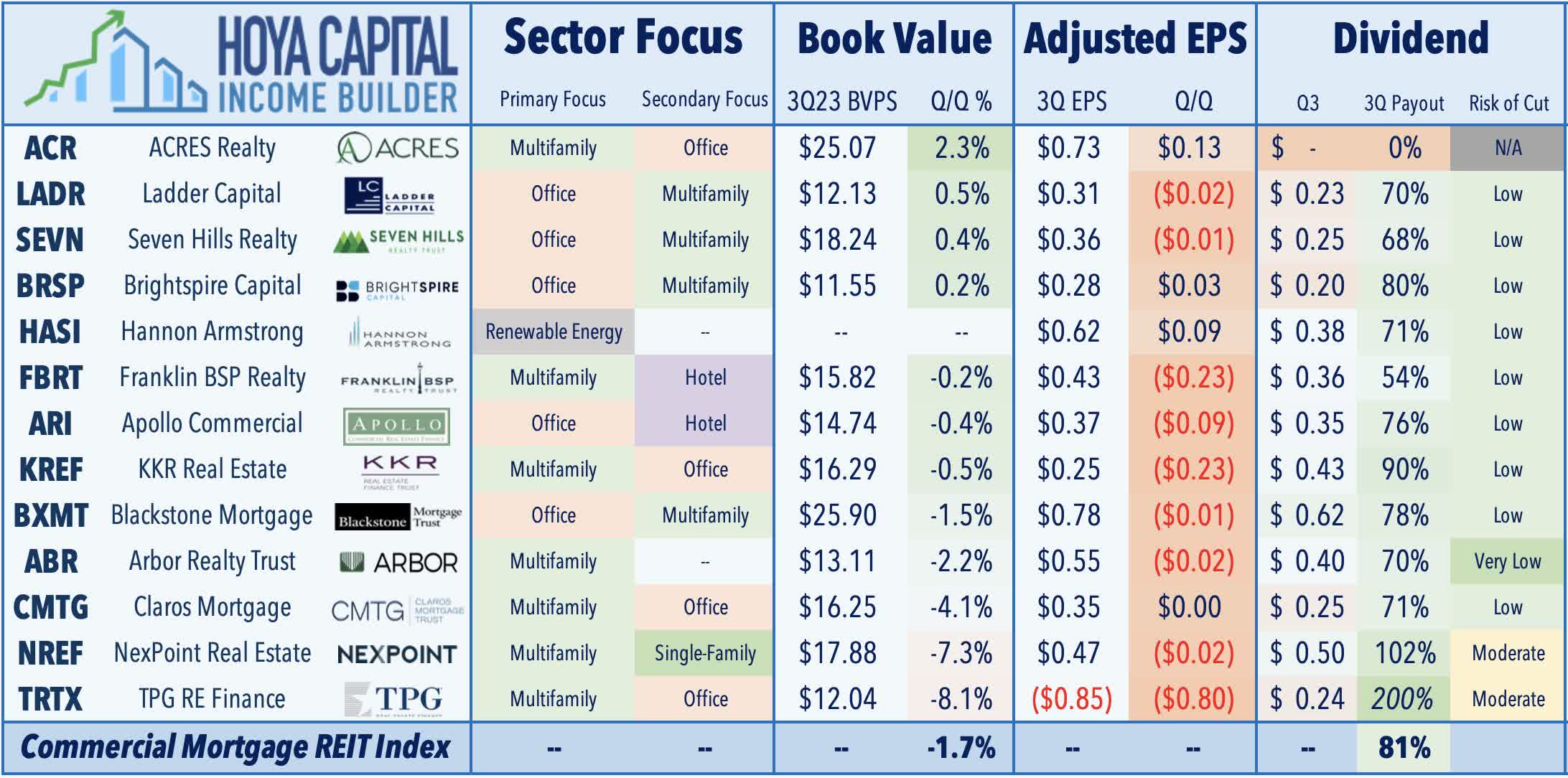

On the commercial mREIT side, Hannon Armstrong ( HASI ) - which focuses on renewable energy lending - soared nearly 30% this week after reiterating its expectation that distributable EPS is expected to grow at a compound annual rate of 10% to 13% from 2021 to 2024, while dividends are expected to grow at a compounded annual rate of 5% to 8%. NexPoint Real Estate ( NREF ) - which focuses on multifamily and single-family rental loans - rallied 13% after reporting that its comparable EPS was roughly flat in Q3 at $0.47, while also declaring a special dividend of $0.185/share in addition to its regular quarterly dividend. Office-focused lender Apollo Commercial ( ARI ) rallied 15% after reporting that its BVPS was little changed in the third-quarter, while noting that credit quality within its loan portfolio "remains stable" with no additional asset-specific CECL allowances during the quarter. BrightSpire Capital ( BRSP ) surged 18% after reporting that its BVPS increased slightly in Q3 - one of four commercial mREITs to report a sequential increase - while recording distributable EPS of $0.28 - covering its $0.20/share dividend.

{kind=link}

Elsewhere, multifamily-focused lender Franklin BSP ( FBRT ) gained 11% after reporting that its BVPS was flat in Q3, while recording distributable EPS of $0.43 - easily covering its $0.36/share dividend. ACRES Commercial Realty ( ACR ) - which also focuses on residential lending - gained 6% after reporting that its BVPS rose 2.3% during the quarter - the strongest among the commercial mREITs to report results thus far. Seven Hills ( SEVN ) gained 4% after reporting that its BVPS climbed 0.4% during the quarter, the third-highest among the commercial mREITs to report results thus far. Claros Mortgage ( CMTG ) gained 7% after reporting that its BVPS declined 4% during the quarter and downgraded three of its loans to the highest-risk level. TPG Real Estate ( TRTX ) was a laggard this week after reporting that its BVPS dipped 8% during the quarter, reflecting an increase in CECL reserves related to a risk downgrade of a San Francisco office loan and a Chicago apartment loan. TRTX also noted that 8% of its loan portfolio is non-performing, a slight improvement from last quarter following the pair of loan sales.

{kind=link}

2023 Performance Recap & 2022 Review

Through ten months of 2023, the Equity REIT Index is now lower by 5.9% on a price return basis for the year (-2.8% on a total return basis), while the Mortgage REIT Index is lower by 2.0% (+7.3% on a total return basis). This compares with the 13.7% gain on the S&P 500 and the 2.3% gain for the S&P Mid-Cap 400 . Within the real estate sector, six property sectors are still in positive territory on the year, led by Data Center, Single-Family Rental, and Healthcare REITs, while Cell Tower and Net Lease REITs have lagged on the downside. At 4.56%, the 10-Year Treasury Yield has surged by 68 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - but down from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index is lower again this year, producing total returns of -0.5% thus far. WTI Crude Oil - perhaps the most important inflation input - is higher by 6.8% this year.

{kind=link}

Economic Calendar In The Week Ahead

Following a frenetic two weeks of economic data and central bank decisions, we'll see a slower slate of data in the week ahead as corporate earnings season winds down. On Friday, we'll get the first look at Michigan Consumer Sentiment for November - a report that includes the closely-watched inflation expectations survey. Sentiment and consumer inflation expectations have closely tracked gasoline prices, which have been on a favorable trajectory since mid-September following a late-summer resurgence. Per GasBuddy , gasoline prices declined to $3.39/gallon by week-end - the lowest levels since February and lower by 12% from the recent mid-September peaks. Following the soft slate of employment data this past week, we'll also be watching Jobless Claims data on Thursday. Continuing Claims have risen for six-straight weeks, while Initial Claims have increased in five-of-six weeks.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

REITs Lead Resurgence