RMD - ResMed Has Become A Steal (Rating Upgrade)

2023-08-10 15:54:36 ET

Summary

- ResMed faces short-term challenges: poor margins due to demand prioritization and potential impact from weight loss drug competition.

- Despite these hurdles, RMD demonstrates strong revenue growth across segments, successful product integration, AI implementation, and market share gains.

- Valuation analysis indicates potential for significant upside, supporting a Strong Buy rating, with a target price of $290, as RMD remains well-positioned for long-term growth.

Introduction

I'm rather satisfied with the way things have been going recently. I was able to buy a lot of stocks at great prices, and the rotation from growth stocks back to value stocks is taking shape. However, my ResMed ( RMD ) call didn't work out the way I expected, as RMD shares have fallen by 17% since my July 4 article .

Having said this, I'm now changing my rating from Buy to Strong Buy , as the company has fallen because of two major reasons:

- The company reported poor margins.

- Weight loss drugs have been approved, which could lower the company's future growth.

{kind=link}

While both of these factors are headwinds, I see no reason to be worried.

The company's poorer margins are the result of the company's decision to prioritize demand fulfillment over short-term profits, which is poised to turn into a longer-term tailwind.

Meanwhile, weight loss drugs, called GLP-1s, are expensive. Although they are shown to be effective, I do not believe that they have the power to derail the ResMed bull case.

The biggest risk to ResMed is competition, which the company is dealing with quite effectively, as it is gaining market share in some areas.

In this article, we'll discuss all of this, including what has become a very attractive valuation.

So, let's get to it!

ResMed Remains In A Fantastic Spot

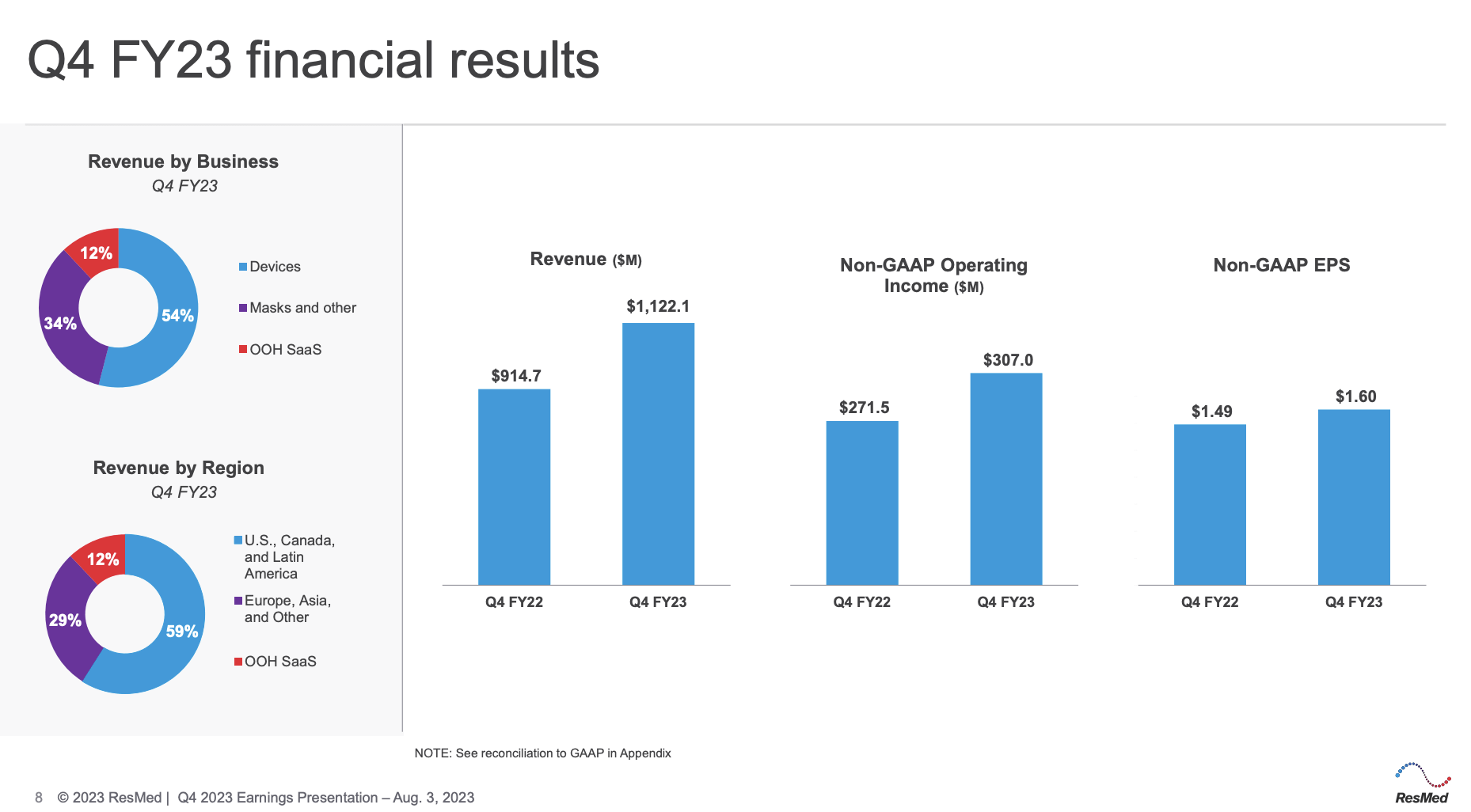

Revenue growth in 4Q23 was 22.4% and missed estimates by $20 million, but given the size of its revenues, it can be considered in line with estimates.

Adjusted EPS came in at $1.60, which was $0.09 lower than expected.

Starting with a deeper dive into revenues, the company had a good quarter, as it saw growth across all business segments, with double-digit growth in devices, masks, and software categories.

{kind=link}

The company, which sells products for sleep apnea and respiratory care in addition to software that allows doctors to monitor their patients at home, elaborated on new developments during its earnings call.

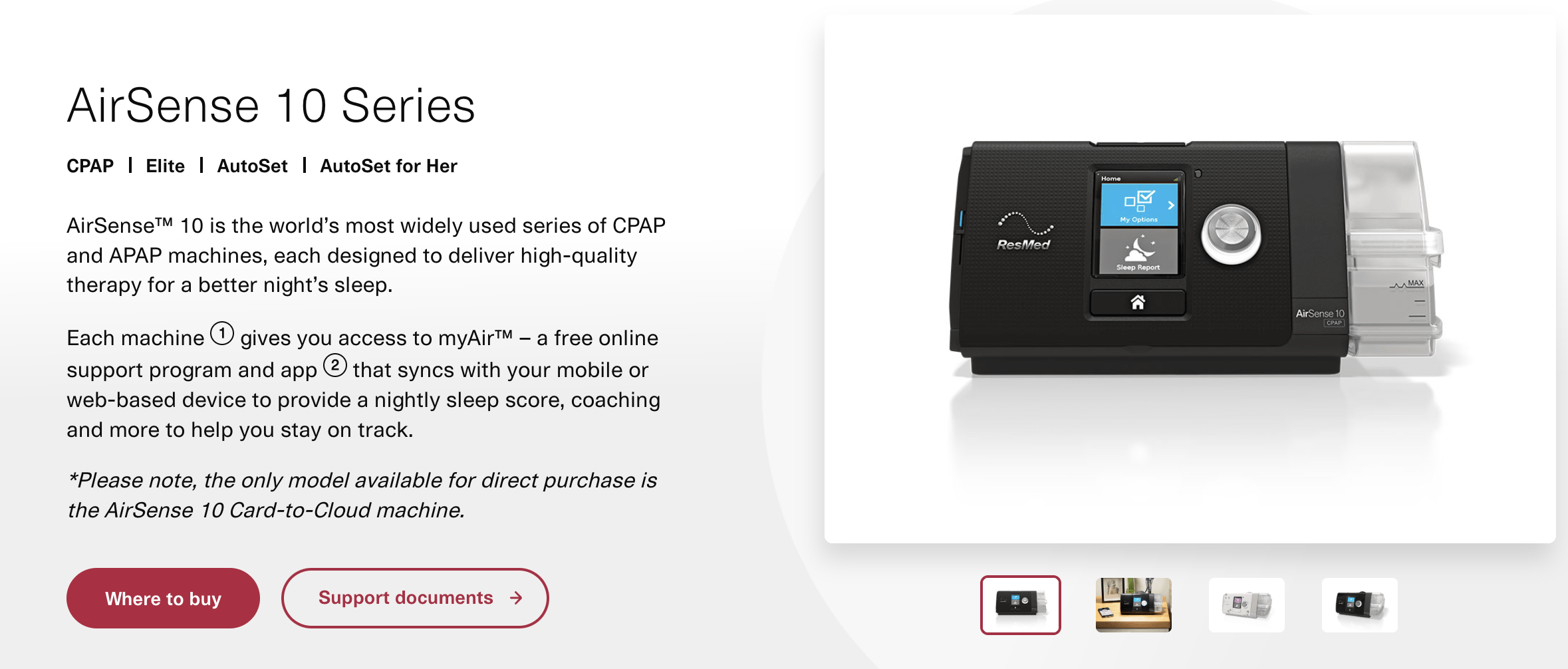

CEO Mick Farrell emphasized the successful availability of the cloud-connected AirSense 10 flow generator platforms globally, along with the ongoing launch of the AirSense 11 platform, which is set to receive regulatory approvals in various geographic regions throughout the fiscal year 2024.

Furthermore, despite ongoing challenges in the post-COVID supply chain, the company is optimistic about steady improvements in component and product supply in upcoming quarters, aided by the combination of AirSense 10 and AirSense 11 platforms.

{kind=link}

Not only is the company pushing out more products, but it is also seeing success in the very core of its business: providing a well-integrated service with its products.

The feedback we hear from patients and healthcare professionals remains very positive. We are seeing strong adoption of the myAir patient app by folks using AirSense 11. In fact, it is more than double the adoption rate that we saw with our AirSense 10 platform with many, many millions of patients signing up and engaging daily on their myAir app to view their own sleep data on their own phone and to review their own therapy data . This is important as engagement with a digital health platform like myAir is directly linked to higher adherence to therapy in patients. - RMD 4Q23 Earnings Call

Based on that context, the company also highlighted the recent acquisition of Somnoware, which is a leader in sleep and respiratory care diagnostics software, as a move to enhance patient pathways and streamline diagnosis and management processes for sleep labs and physicians.

The company is also implementing AI into products for both physicians and patients.

Essentially, this will allow the company to emphasize its core strengths, which is reducing the workload for healthcare providers to improve patient care.

Early testing of these AI driven data products is very positive in both of these customer groups , and we will refine to the optimal digital design and then we will launch and then we will scale these products around the world . These AI driven data products provide personalized suggestions to increase therapy adherence and to ultimately improve patient outcomes as well as patient, physician, and provider experience. - RMD 4Q23 Earnings Call

While I'm fully aware that a lot of companies talk about AI a lot to make their business seem more advanced, I really think RMD is onto something here and in a great place to maintain high growth.

{kind=link}

Having said that, the company's SaaS (Software as a Service) results were impressive, with 34% year-on-year growth in the fourth fiscal quarter.

According to RMD, growth was supported by a full quarter's contribution from the rapidly expanding MEDIFOX DAN business and solid organic growth of 8% across the Brightree and MatrixCare SaaS portfolio.

The sustained high-single-digit organic growth was attributed to the strength in the Home Medical Equipment and infusion segment, along with increased stability in the facility segment as patient flows rebounded post-COVID.

One major secular factor supporting the company is staffing shortages, which is great for products that lower the workload for healthcare providers.

Unfortunately, the company ran into margin issues in the fourth quarter.

- Gross margins declined by 200 basis points to 55.8%, attributed to factors such as component cost increases, warranty and manufacturing costs, and shifts in product mix due to sleep device sales.

- Sequentially, unfavorable foreign currency movements and strong growth in sleep devices in the US contributed to a 30 basis points decline in gross margin.

- Operating expenses increased by 25% (26% in constant currency terms) for SG&A expenses and 21% (23% in constant currency terms) for R&D expenses.

What's important to mention here is that the company decided to focus on short-term demand fulfillment instead of prioritizing margins.

The company decided to sell more last-gen products (AirSense 10) to take care of demand, instead of pushing for its AirSense 11. This is bad for margins, but it does benefit short-term demand for its products and patients who are in need of these products.

So it's better for the patient. It is slightly low margin for us, but we get that patient on therapy, and there is the better together with ResMed that it's more likely, hopefully, that they get a ResMed mask and that they use that mask for the rest of their life. And so I think there's an overlap there, if you like of altruism and the profit motive to do the right thing on a gross profit, cash flow driven environment. - RMD 4Q23 Earnings Call

And on top of this, the company commented on the competition.

For example, the company discusses the return of Philips, noting that Philips' reentry into the market has been gradual and challenging due to reputation issues and slow progress.

The company also emphasized that its smaller, quieter, more comfortable, and more connected solutions are gaining and maintaining market share against competitors, which is key in this competitive industry.

Furthermore, the company sees no real threat from so-called weight loss pills. The company noted high costs, adherence, and side effects. Especially costs are a big issue, as GLP-1s can cost up to $1,200 per month, which is why some healthcare providers (especially in Europe) are unlikely to cover these costs.

{kind=link}

The Wall Street Journal seems to agree, as it highlighted that if just 10% of Medicare beneficiaries were to sign up, it would cost the program $27 billion a year.

Insurance coverage is still spotty, and how the U.S. healthcare system will deal with the immense cost remains a major question. Medicare still doesn’t cover drugs for obesity, and there is good reason to be cautious: A recent article in the New England Journal of Medicine warned that if just 10% of obese Medicare beneficiaries were to take Wegovy, it would cost the program $27 billion a year.

As happy as I am that we're seeing new developments that could help obese people, I do not believe that these pills pose a real threat to ResMed or any of its relevant peers.

Going forward, the company does not give specific guidance, but it remains confident, thanks to its stellar position in the market, which is confirmed by analysts.

Looking at the overview below, we see that while revenue growth is expected to slow (while remaining high), EBITDA growth is expected to remain strong in low-double-digit territory until at least 2025 - and likely beyond.

Leo Nelissen (Based on analyst estimates)

{kind=link}

So, what about the valuation?

Valuation

ResMed has a very healthy balance sheet. Analysts expect the company to lower net debt to just $320 million by the end of the fiscal year 2024. That number could turn into $690 million in net cash in the year after that.

So, for the enterprise value calculation, I'm going with zero net debt.

The company is now trading at 16.0x FY2025E EBITDA, which is well below its long-term EBITDA multiple.

Using a conservative 21x EBITDA multiple, which is low for a company growing its EBITDA by >10% per year, we get a fair value at least 30% above the current price.

That's my base case, which is why I'm now switching to a Strong Buy rating. The most recent stock price crash obviously contributes to that.

On a longer-term term basis, I expect RMD to rise to $290, which was the target I gave in my July article.

Furthermore, unless the company's competitors suddenly show the ability to stop RMD's market share gains, I expect RMD to remain a great long-term compounder.

Takeaway

Recent market shifts and ResMed's strategic decisions have presented both challenges and opportunities.

While my initial ResMed call didn't pan out as expected, the company's transition from Buy to Strong Buy is rooted in its resilience and potential for growth.

Despite facing margin pressures and the emergence of weight loss drugs, I remain confident.

ResMed's focus on demand fulfillment over short-term profits reflects a commitment to patient care and positions it for long-term success. The incorporation of AI and its SaaS results underscore its adaptability and innovation.

While competition exists, ResMed's reputation and superior solutions maintain its competitive edge.

With a favorable valuation and a projected target price of $290, ResMed appears poised for substantial growth as a promising long-term investment.

For further details see:

ResMed Has Become A Steal (Rating Upgrade)