RMD - ResMed - Trading Opportunity Now

2023-09-12 15:27:28 ET

Summary

- ResMed is the global leader in the sleep apnea market.

- Sales growth accelerated during COVID and again recently as a result of a product recall from its major competitor.

- Despite a strong last quarter the market has marked the stock down due to concerns about the long term loss of market to GLP-1 medications.

- ResMed may significantly beat expectations in the next couple of quarters providing the opportunity for short term trading gains.

Company Description

ResMed ( RMD ) develops, manufactures, and distributes cloud-connected medical devices to treat breathing disorders with a particular emphasis on sleep disordered breathing (SDB) and chronic obstructive pulmonary disease (COPD). These products include airflow generators, masks and ventilation products. It also develops computer software applications for managing and supporting the out of hospital care market.

The company operates globally with distribution to over 140 countries through both wholly owned and independent companies. The company's manufacturing operations are not overly capital intensive and are increasingly being concentrated in Singapore with some production at its original base in Australia. The company also operates assembly plants in Malaysia, USA, China, and France.

Originally an Australian company, it is now based in the US city of San Diego. The company's primary listing is on the NYSE. At the time of writing this report the company's market capitalization was 23,412M.

ResMed is organized into 2 divisions - the Sleep and Respiratory Care segment (which has two components - devices and masks / ancillaries) and the Software as a Service (SaaS) segment.

According to the company's 2023 annual report the relative sales and profitability of the divisions were:

Author's compilation using data from ResMed's 10-K filing.

Business Overview

Technology has been at the heart of the company's value proposition. ResMed currently owns or licenses 9,700 patents or pending patents. It is noted, however, that over 619 US and 1,472 foreign patents will expire over the course of the next 5 years.

The company currently expenses M per year in research and development. This represents about 7% of sales and this ratio has been reasonably steady since FY2015.

The company is focused on the global sleep and related respiratory care markets which it believes are under-penetrated. Based on an independent study completed in 2013 it is estimated that 26% of all adults aged 30 - 70 years old in the US have some form of obstructive sleep apnea ((OSA)). This represents a market of 46 million people, and it is thought that only 20% have been diagnosed and treated. Clearly, this number can then be extrapolated to other countries.

Historically, surgery was the first-line treatment for OSA. These days this is not the case and although surgery remains an option there are alternative treatments including both dental and nasal appliances, etc. The most reliable treatment for OSA is currently a CPAP device. Depending upon the severity and individual preferences, a nasal interface, or a full-face mask is used with the CPAP device.

It is noted that CPAP is not a cure and must be used nightly until the symptoms disappear. Historically, the CPAP devices have not been very comfortable to use - this has resulted in extensive non-compliance by patients with their recommended treatment regimes. ResMed's focus has been on improving patient comfort (better interfaces) and feedback (both to the patent and the physician) via technological enhancements (software-controlled air-flow changes, etc.).

The other current prime market focus for ResMed are those patients with Chronic Obstructive Pulmonary Disease (COPD). This market encompasses a group of lung diseases defined by persistent airflow limitation, prolongation of exhalation and loss of elasticity in the lungs (examples are emphysema and chronic bronchitis). For these patients, home non-invasive ventilation has been shown to be a benefit and appears to extend the periods between patient readmission to hospital.

ResMed's product offering includes:

- Devices such as air-flow generators, ventilators and oxygen concentrators.

- Patient interfaces - masks, dental devices, etc. (which are disposables).

- Cloud-based software which controls the CPAP device and records patient data.

ResMed's route to market is via its direct sales force and through a dealer network. Its products are marketed directly to hospitals and medical professionals. Sales to the public are typically through a 3rd party home healthcare dealer network.

Governments have a significant role to play in this market:

- ResMed's devices must be compliant with the requisite regulations.

- Governments (and medical insurance companies) in most markets financially contribute to the purchase of these devices and products.

Since 2015 ResMed has been supplementing its organic growth with acquisitions (particularly for the SaaS division). Until 2015 they had only made a few relatively small acquisitions with an average annual investment of $14 M. This all changed in 2015 when the company decided to enter the software as a service (SaaS) business.

The company has made 3 major acquisitions to support this strategy:

- Brightree was purchased for $1,041 M in February 2016.

- MatrixCare was purchased for $750 M in November 2018.

- Medi-Fox Dan was purchased for $998 M in November 2022.

There have been many other smaller acquisitions as well which has seen ResMed invest a total of $3,167 M in acquisitions over the last 10 years.

The SaaS acquisitions are part of its digital health technology strategy. It is thought that by connecting CPAP devices to the cloud to capture data this will help both patient treatment compliance and provide insights into undiagnosed patient symptoms. This in turn could lead to an increase demand for ResMed devices.

Market Overview

ResMed has 2 operating divisions:

Sleep & Respiratory Care

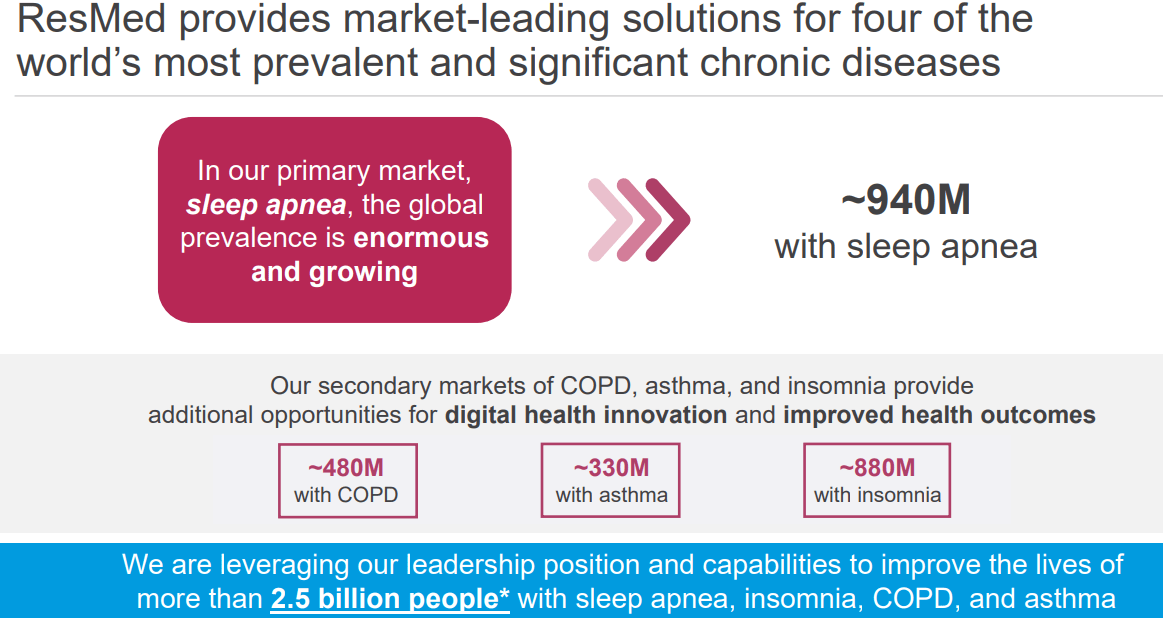

This division is primarily targeting the sleep apnea market and its secondary target markets are people who suffer from Chronic Obstructive Pulmonary Disease (COPD), asthma, and insomnia.

The following slide is ResMed's estimate of the global number of people who suffer from these conditions:

ResMed presentation, JP Morgan Healthcare Conference, Jan. 2023.

{kind=link}

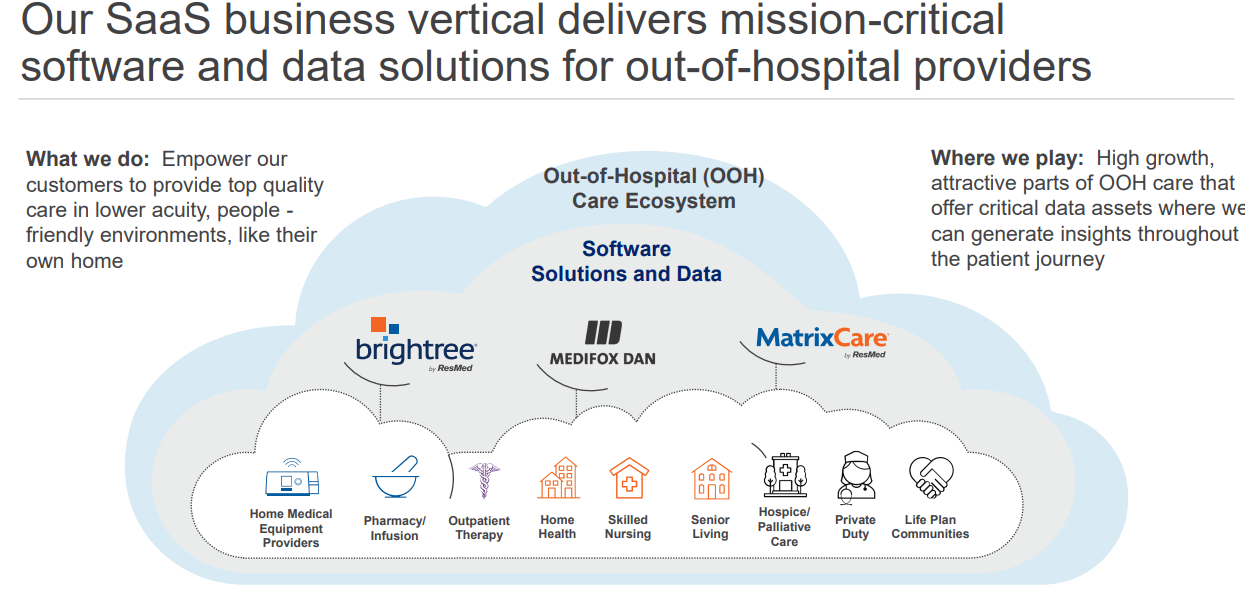

Software as a Service (SaaS)

The target market for ResMed's SaaS offering is the out-of-hospital care providers. This market is summarized by the following slide:

ResMed presentation, JP Morgan Healthcare Conference, Jan. 2023.

{kind=link}

ResMed estimates that this market is currently worth around $2 Billion, and it claims to be the market leader in this space (it is a highly fragmented market).

Competitors

The sleep apnea devices market is highly consolidated. ResMed's largest listed competitors are Koninklijke Philips (PHG) and Fisher & Paykel Healthcare (FSPKF). There are also several smaller privately owned competitors in this market.

Market research firm, Global Market Insights , estimated that in 2022 the global sleep apnea market was about $7,500 M in size. They also believe that the market will grow by 6.5% per year for at least the next 5 years.

There has been significant turmoil in the market since June 2021 because of a major product recall from Philips. Two years later, the ramifications of this incident are still playing out in the courts (there are said to be consumer class action cases pending). There has also been increased interest from regulators and major disruptions to the industry's supply chains.

ResMed has been a major beneficiary of this incident. Before the incident, ResMed and Philips held similar market shares (estimated to be around 40%). Much of ResMed's above average revenue growth for the last 2 years has been due to market share gains (particularly in the US market). This can be seen in the following chart:

Author's compilation using data from ResMed's 10-Q filings.

Although ResMed's sales have shown a long-term increase, the rate of change has been very lumpy. There was steady growth through the COVID pandemic (ResMed's respirators were in high demand for COVID patients) and then as the effects of the pandemic started to recede during 2021, revenue growth also started to decline until the Philips' recall was announced at the end of Q2 2021.

The Philips' recall has triggered two distinct bursts of extraordinary growth and at the end of the most recent quarter ResMed's TTM revenue growth was still rising.

It is rumored that Philips will re-enter the device market over the next few months which could have a negative impact on ResMed's near-term growth trajectory.

Sector Disruption

The biggest long-term risk to ResMed's business is the commercial development of a cost-effective drug which significantly reduces the target population for sleep apnea devices.

Both Eli Lilly and Novo Nordisk (there are several other suppliers as well) have developed a class of drugs called GLP-1 medications. These drugs were created to treat Type-2 diabetes but have since been found to suppress appetites and induce weight loss. There is a link between obesity and sleep apnea.

GLP-1 drugs are treatments but not cures for these conditions.

GLP-1 drugs have been available for diabetes treatment for several years but earlier this year (2023) they were promoted for weight-loss treatment when several celebrities disclosed that they were using the drugs. As a result of this promotion the drugs are in short supply.

During the recent 2023 Q4 earnings conference call , ResMed was questioned on the potential impact of these drugs on their business. ResMed believes that there are 3 drawbacks to the uptake of GLP-1 drugs:

- Cost - current treatment costs are $800 to $1,200 per month which is significantly more expensive than CPAP treatments (up to 35 times).

- Adherence - trial data shows that adherence levels are 33% whilst CPAP is 87%.

- Side Effects - there are significant major and minor side effects.

In summary ResMed does not yet appear to be overly concerned about the impact of these drugs on its business but it would appear that investors have taken a different view and ResMed's stock price has declined by 35% since the release of its FY2023 results.

ResMed's Historical Financial Performance

Revenues and Operating Margins

The following chart shows ResMed's revenues and adjusted operating margins:

Author's compilation using data from ResMed's 10-K filings.

I have made significant adjustments to ResMed's published financial statements to calculate the "Adjusted Operating Income". The adjustments include:

- R&D expenditure has been capitalized and I have applied an amortization rate to these investments (it assumes a 5-year life). This causes the operating margin to increase.

- Operating lease expenditure has been converted into interest payments and depreciation (this causes the operating margin to increase).

- One-off expenses have been removed from the operating results.

The sales chart shows a classic staircase growth pattern that has now been in place for more than 10 years. Sales have been growing at over 10% per year for the last 10 years whilst for the last 5 years the CAGR has been nearly 13%.

Post-COVID operating margins have started to decline after a long period of steady improvement. This decline has been caused by increases in manufacturing costs (as reflected in lower gross margins). ResMed has suffered from supply chain constraints which they claim are now slowly being resolved.

Typical operating margins in the medical device sector are currently 13.3% and ResMed's margins are in the sector's highest quartile.

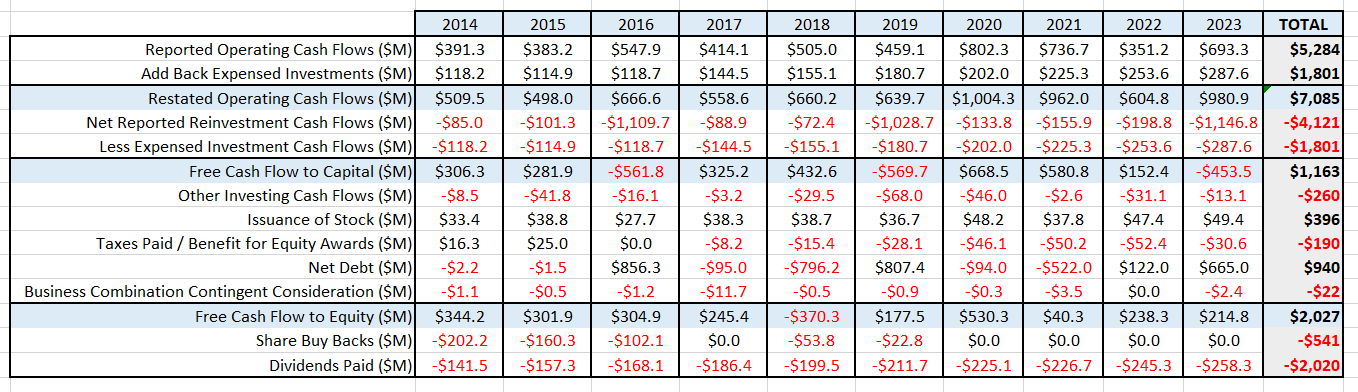

Cash Flows

The following table summarizes ResMed's cash flows over the last 10 years:

{kind=link}

It should be noted that I have made some adjustments to the reported Cash Flow Statement - I have moved the expensed R & D cash flows out of operating cash flows and properly accounted for them in the investing cash flows.

ResMed's R&D investment to sales ratio is 7% which is the median of the medical device sector.

The vast majority of ResMed's return to shareholders is via dividends (although the stock's dividend yield is relatively low at 1.1%). The company is typically paying out its entire free cash flow to equity in dividend payments. This means there are limited opportunities to significantly increase the dividend coupon unless the company's free cash flow materially rises. Whilst the company continues to make periodic large acquisitions there will also be no opportunities to buy back shares.

Capital Structure

The following chart shows the history of ResMed's capital structure:

Author's compilation using data from ResMed's 10-K filings.

The chart shows the history of ResMed's acquisition story. Each major acquisition has been funded by new debt issuance. In the years after the acquisition the company uses its excess cash flow to pay the debt down before repeating the process.

ResMed is still conservatively geared, and its current debt ratio is 5% versus the sector's median ratio of 33%. I have no concerns about ResMed's capital structure.

Return on Invested Capital

The following chart shows the history of ResMed's return on invested capital [ROIC]:

Author's compilation using data from ResMed's 10-K filings.

Note that my calculated ROIC for ResMed will be lower than the published figure because I capitalize the research & development expenditure which consequently increases the denominator in the calculation.

The chart shows the negative impact that the SaaS acquisitions initially had on the ROIC, but ResMed is now slowly moving the ROIC back to its historical levels.

The current ROIC of 22% compares very favorably to the sector's median 0f 9%. This is a clear demonstration of the strength of ResMed's competitive position.

My Investment Thesis for ResMed

There are 2 extreme scenarios for ResMed depending upon how successful GLP-1 drug companies are in resolving the issues which may prevent the widespread usage of these drugs for weight loss.

For reasons of convenience, I have concluded that the financial impact of GLP-1's success or failure will be shown in ResMed's operating margins. I have assumed that there will be limited impact on sales volumes (of course this is arguable) because there will still be demand for the relatively lower-cost ResMed products.

I have chosen to use the consensus revenue forecasts for the next 2 years (noting that ResMed does not provide any revenue guidance). These forecasts appear to include the impact of the re-introduction of the Philips' product to the market. The projections are for FY2024 revenue growth of 9.6% and 7.6% for FY2025.

Growth Story

ResMed's recent historical revenue growth has benefited from both COVID-19 and the product withdrawal of Philips. The market is expected to grow at 7.5% CAGR for the next 10 years. The growth runway is quite long because of the current relatively low treatment rates for the effects of sleep apnea.

ResMed has the benefit of additional revenue coming from its SaaS division. Due to the fragmentation of this market and ResMed's acquisition activities this will enable it to generate higher than market growth.

ResMed should be able to maintain a growth rate of 9% per year for the period FY2026 until FY2032.

Margin Story

ResMed's current adjusted operating margin of 29.5% is 1% lower than its COVID peak margin due to the negative supply chain impacts.

In my optimistic scenario I expect that ResMed can resolve its supply chain issues and maintain its margins at the medical device sector's 90th percentile.

In my pessimistic scenario, competition (both from the GLP-1 drugs and other device suppliers) force operating margins down to 22% (the sector's 75th percentile). Note that the sector's median operating margin is 14%.

Growth Efficiency / Reinvestment

ResMed currently reinvests at the median rate for the device sector. I see little opportunity for ResMed to reduce its level of reinvestment. Its device market leadership is dependent upon maintaining a technology gap over its competitors. Similarly, its SaaS growth is coming from acquisitions, and I expect that this will also continue.

Risk Story

Clearly, there are substantial risks around ResMed's future trajectory. From a valuation perspective there are two ways that I could handle this uncertainty.

Project out my optimistic scenario and apply a heavy discount rate to account for the high level of uncertainty. Project out both scenarios at a market average discount, assess a probability for each scenario and calculate a weighted average valuation.

I have chosen to follow the last option which will allow readers to assign their own scenario probability.

I estimate that the median cost of capital in the US is currently 8.7% and this is the terminal discount rate that I have used in both scenarios.

Competitive Advantages

ResMed's current competitive position is very strong as indicated by its relatively high ROIC. There will be inevitable decline in the ROIC into maturity, but I would expect that it should be higher than the cost of capital.

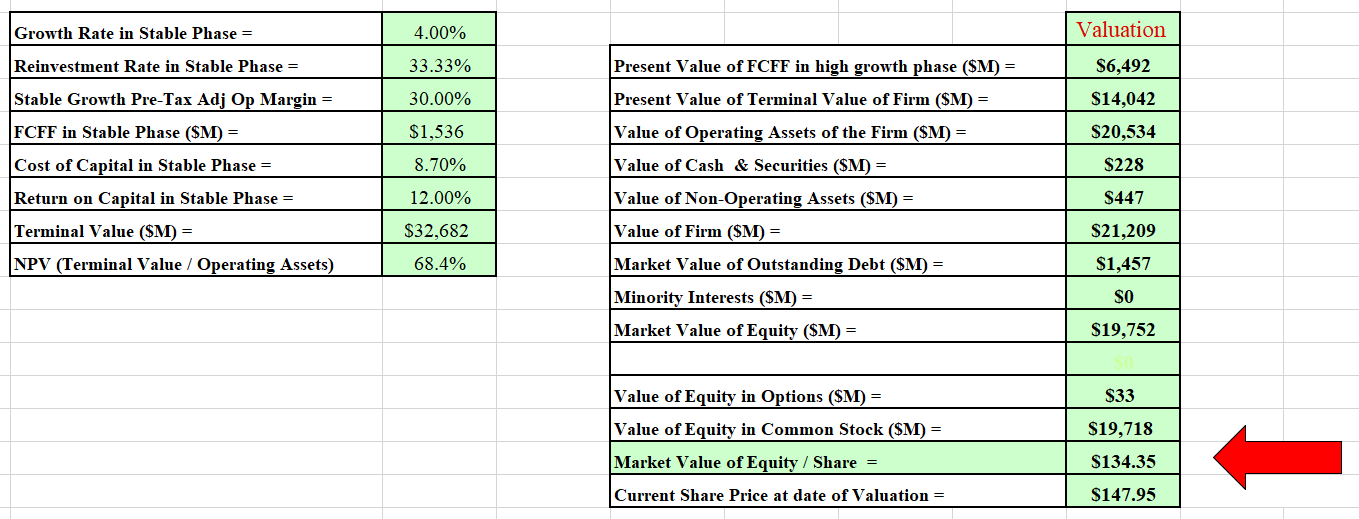

Valuation Assumptions

The following table summarizes the key inputs into the valuation:

Author's valuation model inputs.

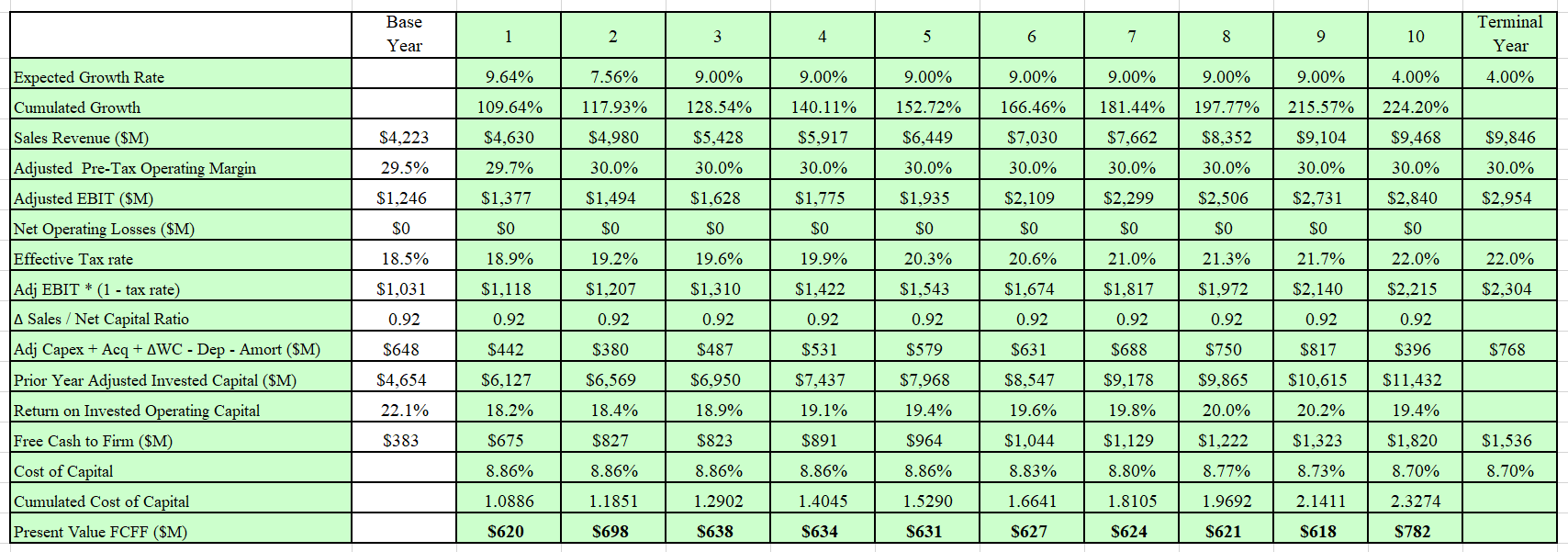

Discounted Cash Flow Valuation Output

I will only show the Optimistic model's output in full as I suspect that it is the closest to ResMed's current market price and I will state the value of the Pessimistic model for comparison.

The valuation is performed in and the output from my DCF model is shown below:

{kind=link}

{kind=link}

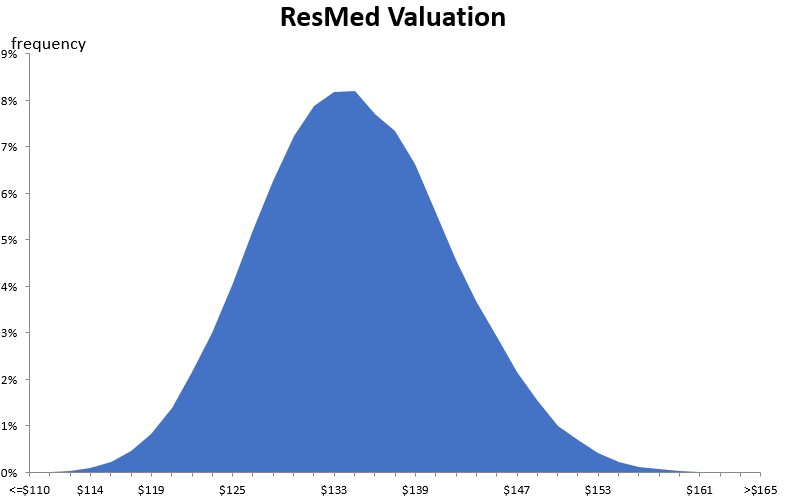

I also developed a Monte Carlo simulation for the valuation based on the range of inputs for the valuation. The output of the simulation was developed after 100,000 iterations.

{kind=link}

My model suggests that for my Optimistic scenario the intrinsic value for ResMed is between $110 and $165 with a typical value around $134 per share.

For Australian investors there is a conversion of 1:10 from stock to the ADR security followed by the currency adjustment (64 cents is the current exchange rate). This equates to a range in price of between and with an expected value of per share.

I think that based on my scenario, ResMed is currently fairly priced.

The following table shows ResMed's intrinsic value for both scenarios:

Author's valuation model output.

How do I Use the Scenarios

Now that I have created the two extreme scenarios, readers can decide for themselves what is the likelihood for each scenario and use the following table to develop their own intrinsic value for ResMed:

{kind=link}

My assessment of the probability of the GLP-1 drugs being successful is influenced by the opinions expressed by ResMed's management. I have always found the company's leadership to be honest and trustworthy.

As a result, I have assessed the current probability to be 10% to 20% that GLP-1 drugs will significantly impact the long-term health of ResMed's business.

Of course, I reserve the right to change my opinion as more data comes to light.

Final Recommendation

I have been valuing ResMed for many years. The key company inputs into the valuation - sales growth, margins and reinvestment have been relatively stable for a long time. The input which changes regularly is the cost of capital which is significantly influenced by the macro-economic environment.

Generally, I have found ResMed to be over-priced.

There are undoubtedly risks on the horizon relating to the impact of the GLP-1 drugs on the sleep apnea device market. I don't believe that these are immediate risks, but that it will take a couple of years to become more obvious.

ResMed's recent sales trajectory has been higher than the company's historical run rate. This has been influenced by the introduction of a device model upgrade (AirSense 11) and the market withdrawal by a major competitor.

As ResMed does not provide any revenue guidance I suspect that analysts may be under-forecasting revenues for the next couple of quarters. This may lead to a situation where the company easily beats expectations which may cause a significant short-term bounce in the stock price.

I think that the stock may currently be oversold and for this reason, I have recently started accumulating a modest holding in the stock for a near-term trading opportunity.

At this stage I am not recommending a long-term investment in the stock but purely a near-term trading position.

Is ResMed today a buy, hold or sell?

I think that ResMed is a BUY. Traders should carefully assess their exposure to the stock and the uncertainties that I have highlighted in the report and make decisions appropriately based on their portfolio construction and risk profile.

For further details see:

ResMed - Trading Opportunity Now