UDR - RFI: This High-Yielding CEF Is Beating The Index

Summary

- Real estate can be a good way to protect wealth in the face of inflation.

- Cohen & Steers Total Return Realty Fund invests in a portfolio of securities issued by real estate companies to generate both capital gains and income for their investors.

- The RFI portfolio has beaten corresponding index funds year-to-date, which is a good sign of management's competence.

- The distribution is sustainable, but the fund cannot keep taking unrealized losses as that will make it harder and harder to generate enough capital gains.

- The RFI fund looks quite expensive right now.

It is no real secret that many people have seen their purchasing power decline significantly over the past year. This is largely due to the incredibly high level of inflation that we have experienced, which continues to permeate our economy even to this day. In addition to needing income, many people are concerned with wealth preservation, as the rising prices of everything have caused cash savings in the bank or other places to lose their value in terms of what they can purchase.

There are some places where money can be invested that should hold its value over time, though. One of these areas is real estate. Real estate also has the advantage of being able to be rented out to other people, thereby generating an income. Unfortunately, the yields on many real estate companies are still quite low, so this income may be smaller than what an investor really wants or needs. One of the best solutions for this problem is to invest in a closed-end fund ("CEF") specializing in real estate investing. These funds have the advantage of providing investors with a diversified professionally-managed portfolio and can in many cases deliver a higher yield than any of the assets themselves actually produce.

In this article, we will discuss the Cohen & Steers Total Return Realty Fund ( RFI ), which is one of the most popular funds in this category. The fund boasts an impressive 7.38% yield at the current price, which is significantly above the yield available from real estate index funds. I have discussed this fund before, but over a year has passed since that time so a great many things have changed. This article will focus specifically on those changes as well as provide an updated analysis of the fund’s financial situation. Therefore, let us investigate and see if this fund could be a worthy addition to your portfolio today.

About The Fund

According to the fund’s webpage , the Cohen & Steers Total Return Realty Fund has the stated objective of providing its investors with a high level of total return. This is not particularly surprising, since most investors are interested in real estate for its total return characteristics. After all, a building is usually purchased with the hope of ultimately making a capital gain. In addition, the property will be rented out to a tenant in order to generate income. These are the two components of total return.

However, unlike some publicly-traded entities, the fund aims to generate its returns by investing in real-estate securities instead of owning the buildings directly. It primarily purchases shares of real estate investment trusts, which are the entities that actually own the buildings. Curiously though, the fund does not state whether it will only invest in the common equity issued by these entities or if it can also purchase fixed-income securities such as preferred stock and bonds. As it makes no mention of the specifics here, the fund can presumably invest in both types of security. Indeed, currently, it is invested in both common equity and fixed-income real estate securities, although it is much more heavily weighted toward common equity:

CEF Connect

This blend of both asset types is something that could be beneficial from a total return standpoint. For example, common stock typically has a higher potential total return since it benefits from the growth of the underlying company as well as providing a dividend to the shareholders. However, the dividend on common stock tends to be lower than the dividend on the preferred stock issued by the same company. This is why the fund’s investment in preferred stock is helpful since it will boost the fund’s income and ultimately the distribution that can be paid by the investors. However, the preferred stock almost always has a fixed dividend so it will not benefit as the issuing company grows and prospers. In addition, the preferred stock tends to be less volatile in the market so the presence of these securities should help reduce the overall volatility of the fund.

Unfortunately, real estate investment trusts have not performed especially well this year. The biggest reason for this is that the Federal Reserve has been aggressively hiking interest rates since March. As we can see here, the federal funds rate was 0.08% back in February compared to 3.78% today:

{kind=link}

The reason that this has been devastating for real estate is that this has pushed up the cost of mortgages. As very few people can afford to purchase real estate with cash, the higher cost of the mortgage means that the value of the real estate needs to decline so that the mortgage payment on a given property will remain relatively static. In addition to this, the declining stock market resulted in those investors that had large margin loans being forced to sell everything to raise the cash needed to pay off their own loans. This would include real estate investment trusts, even though the actual cash flows and dividends paid out by most of these companies are unaffected by the interest rate increases since mortgage rates tend to be fixed.

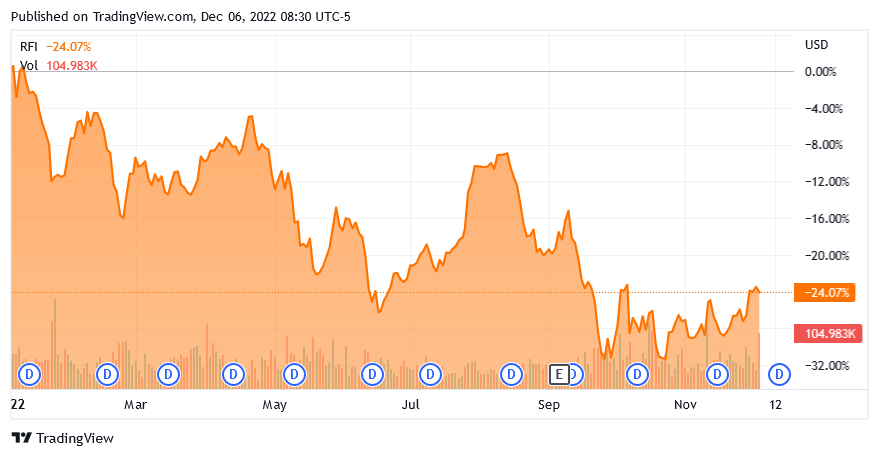

The fact that many real estate investment trusts have fallen in value also means that the value of the fund has fallen. In fact, the Cohen & Steers Total Return Realty Fund is down 24.07% year-to-date:

{kind=link}

This is actually a better performance than the iShares U.S. Real Estate ETF ( IYR ) has delivered over the same period. This is an index fund that tracks an index of American real estate investment trusts so it is probably the best index fund to compare the Cohen & Steers fund to. The index fund is down 24.35% year-to-date, so the closed-end fund has actually outperformed. This may be partly due to the fixed-income securities held by the fund, although these assets have also declined as interest rates have risen. It is quite nice to see though that the fund is outperforming its index, as it is somewhat rare to see closed-end funds accomplish that.

Real estate investment trusts are very popular investments among those investors that are seeking income. As such, they are fairly well covered by numerous authors here at Seeking Alpha and many readers will likely be at least somewhat familiar with the largest positions in the fund. Here they are:

CEF Connect

There have been a few changes since we last looked at the fund. Chief among these is that Equinix ( EQIX ), Healthpeak Properties ( PEAK ), and UDR ( UDR ) were replaced by Welltower ( WELL ), Invitation Homes ( INVH ), and Realty Income ( O ). There were also a few changes to the fund’s weightings over the past year but this could be explained by one asset outperforming another in the market. The fact is though that the limited number of changes might still lead one to believe that the fund has a fairly low annual turnover. This is in fact the case as the Cohen & Steers Total Return Realty Fund has a 36.00% annual turnover, which is fairly low for an equity fund. This is rather nice to see because trading stocks or other assets costs money, which is then billed to the fund’s investors. This creates a drag on the fund’s performance and makes the job of the fund's management that much more difficult because they have to generate sufficient extra returns to cover these added expenses as well as deliver a return that satisfies the investors. This is one reason why closed-end funds rarely outperform their benchmark indices.

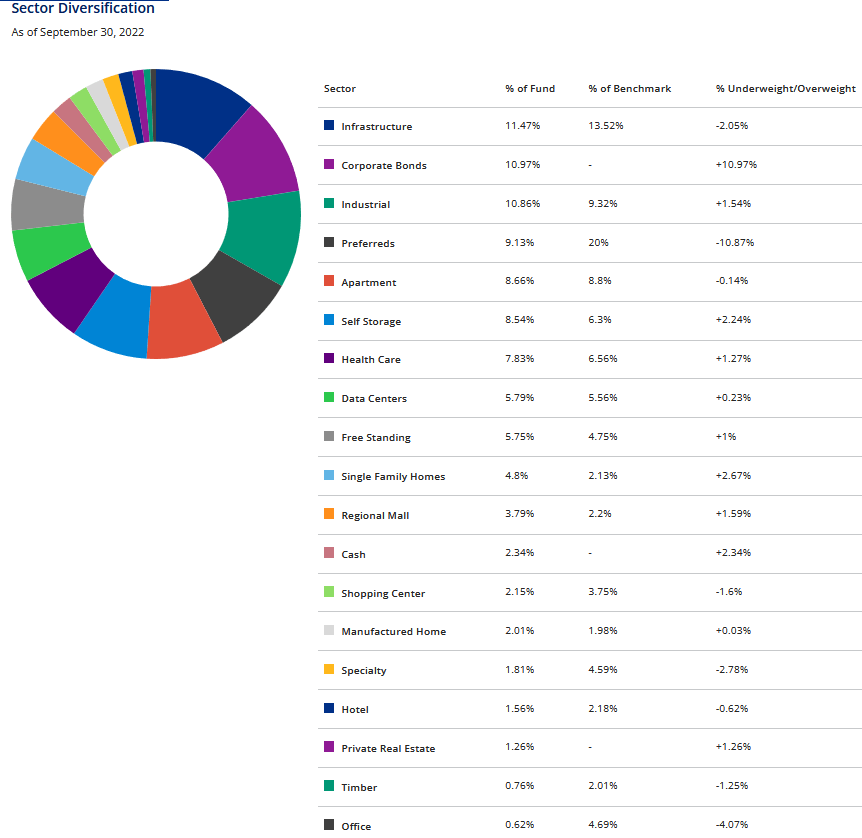

Anyone that is fairly familiar with real estate investment trusts will quickly see that the companies above operate in various sectors of the actual real estate universe. For example, American Tower ( AMT ) and Crown Castle ( CCI ) own cellular towers that they lease out to service providers. Simon Property Group ( SPG ), on the other hand, owns some of the premier shopping malls around the United States. Overall, the fund is fairly well diversified across the different types of real estate:

{kind=link}

This is something that is fairly nice to see because different types of real estate have different fundamentals. For example, regional malls and shopping centers are much more exposed to consumer spending patterns than healthcare trusts. After all, should consumer spending decline, which is typical in recessions, then the revenue of the tenants renting space in these shopping centers will decline and pressure their ability to make rent. This is something that could be very important today as the high inflation in necessities has reduced the ability of consumers to engage in discretionary spending. In October, about 40% of small businesses failed to pay their rent . A healthcare real estate investment trust is much less exposed to something like this because consumers will seek out their tenants’ services whenever they need them regardless of their own financial condition. At the same time, retail real estate tends to outperform healthcare real estate during strong economies with rapidly growing spending. Thus, the fact that the fund is exposed to all different types of real estate is nice as it provides it with exposure to all these different fundamentals.

Real Estate As Inflation Protection

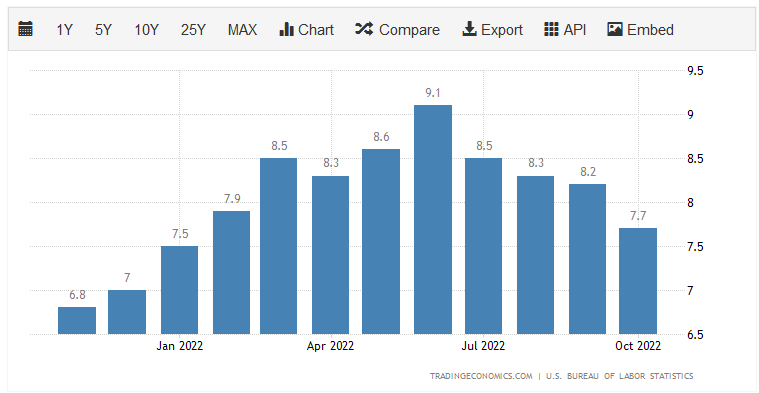

As I mentioned in the introduction, real estate can act as protection against inflation. This is something that is important today considering that inflation is running at 40-year highs:

{kind=link}

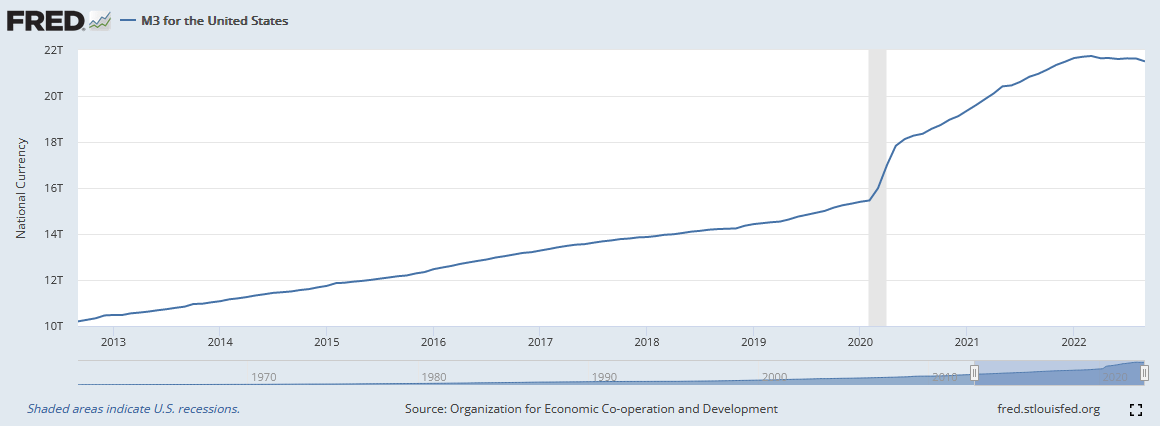

The reason why real estate can act as a hedge against inflation is due to the cause of inflation. Many analysts and even economists consider inflation to be a natural phenomenon but this is not exactly correct. It is caused by the money supply growing more rapidly than the production of goods and services. This is because such a scenario results in more units of currency attempting to purchase a given unit of economic production, which drives the price up. This has been the case in the United States for a long time now, although it became especially prevalent in 2020:

{kind=link}

This chart shows the M3 money supply over the past ten years, which is the most comprehensive measure of the supply of money in the United States. As we can see, the money supply went from $10.2008 trillion in September 2012 to $21.5034 trillion in September 2022 (the most recent date for which data is available). We can see that the rate of growth accelerated substantially in 2020, which was a direct result of the enormous amount of money printing in response to the pandemic, although the interest rate increases this year have had a tempering effect on monetary growth. This represents a 110.8% increase over the ten-year period, which was substantially higher than the production of goods and services growth. We can see that here:

{kind=link}

This chart shows the gross domestic product of the United States over the same period. This is the best measure we have of the value of goods and services produced by an economy during a given time period. As we can see here, the gross domestic product went from $16.31954 trillion in the third quarter of 2012 to $25.69896 trillion today. That is only a 57.47% increase over the period. Thus, we can see that the money supply grew almost twice as quickly as the production of goods and services in the economy over the past decade. This is the biggest cause of the inflation that we are seeing today.

Real estate has the same characteristics as other things that see price increases during inflationary periods. For example, it is in limited supply as we cannot simply print more land. It requires actual human or mechanical effort to improve. After all, a magical fairy did not just snap their fingers and cause your house to appear. These characteristics mean that real estate should hold its value over time. With that said, there will undoubtedly be some who point out that we have seen real estate prices decline as interest rates rise. That is mostly due to the rising value of the dollar in such a situation but the basic fundamental remains that real estate should hold its value over the long term and protect your wealth against inflation.

Distribution Analysis

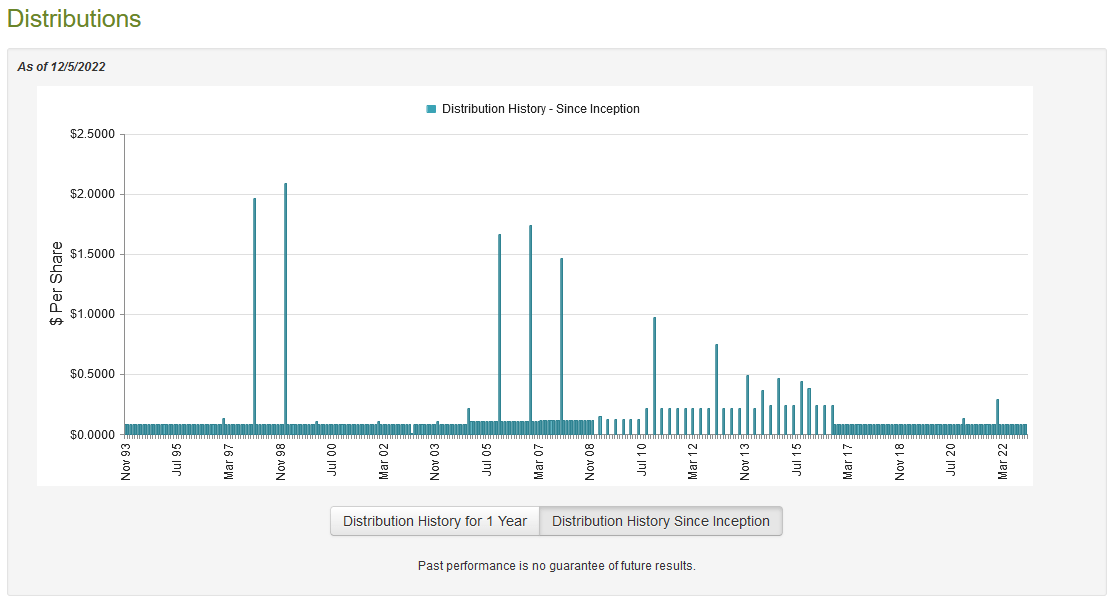

As mentioned throughout this article, real estate investment trusts tend to be a fairly popular investment among those seeking income. This is because not only does real estate have intrinsic value but it can also be rented out to tenants. A real estate investment trust is required by law to pay out a substantial portion of its profits to investors so that tends to result in high yields. The Cohen & Steers Total Return Realty Fund passes the dividends that it receives from these companies through to its investors so we might expect that it would also have a fairly high yield. This is certainly the case as the fund pays out a monthly distribution of $0.08 per share ($0.96 per share annually), which gives the fund a 7.38% yield at the current price. The fund has generally been consistent about this payout in recent years, although its long-term history is spottier:

{kind=link}

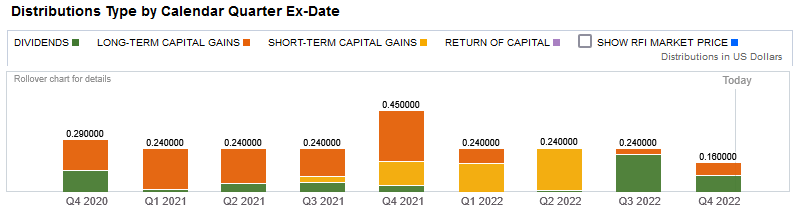

We can see that the fund has been paying out its current monthly distribution since October 2016, which is a pretty nice situation for those investors that are looking for a safe and secure source of income to support their lifestyles. Another thing that may be comforting to these same conservative investors is that the fund’s distributions are entirely classified as capital gains distributions or dividend income, which no return of capital component:

{kind=link}

The reason why this may be comforting is that a return of capital distribution may be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, the fund’s capital gains also may not be sustainable long-term since it is not always possible to generate large capital gains during weak markets, such as the one that we are in today. As such, we do want to investigate the fund’s finances to determine just how sustainable these distributions are likely to be.

Fortunately, we do have a fairly recent report that we can consult for this purpose. The fund’s most recent financial report corresponds to the six-month period ending June 30, 2022. As such, it should give us a great deal of insight into the fund’s performance during the first half of the year, which was a somewhat punishing time for many real estate companies as that is when the Federal Reserve started its interest rate-hiking campaign. During the six-month period, the Cohen & Steers Total Return Realty Fund reported a total dividend income of $3,980,528 and an interest income of $685,054 from the assets in its portfolio. This gives the fund a total income of $4,665,582 during the period. The fund paid its expenses out of this amount, leaving it with $2,921,279 available for investors. This was nowhere close to enough to cover the $12,635,361 that the fund actually paid out in distributions during the period.

As we see in the chart above though, the fund historically obtains a substantial amount of the money that it pays out from capital gains. As we might expect though, the fund was not particularly successful at this during the period. The fund realized net gains of $10,800,091 during the period but this was more than offset by $84,050,194 in net unrealized losses. Overall, the fund’s assets declined by $82,277,701 after accounting for all inflows and outflows. This is certainly concerning at first glance, although the fund did have enough realized gains and net investment income to cover the distributions. We will want to keep an eye on this though since the more that the fund’s assets decline, the harder it will be to generate sufficient capital gains to maintain the distribution.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Cohen & Steers Total Return Realty Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. This is not the case with the Cohen & Steers Total Return Realty Fund today. As of December 5, 2022 (the most recent date for which data is available as of the time of writing), the fund had a net asset value of $12.22 per share but the shares actually trade for $12.95 per share. This gives the fund’s shares a 5.97% premium to net asset value at the current price. This is a bit higher than the 5.06% premium that the shares have had on average over the past month and it is quite a bit more than the fund’s assets are actually worth. As such, it may not make sense to buy today and most investors would be best off waiting for a better entry price.

Conclusion

In conclusion, real estate can be a very good asset to include in a portfolio during times of inflation. This is because real estate both acts as a store of value as well as generates income if it is rented to tenants. There will likely be some short-term pressure on real estate stock prices but the long-term trends are hard to ignore. The Cohen & Steers Total Return Realty Fund appears to be a good way to invest in the sector and generate a high yield at the same time. The fund is very well diversified across the real estate universe and has managed to beat the index year-to-date, which is a feat that few funds can boast. The fact that the fund has also been able to maintain its distribution over extended periods is also a bonus. The biggest disadvantage here is that the Cohen & Steers Total Return Realty Fund is fairly expensive today, although some people might be willing to pay that extra expense for the performance that the fund has historically delivered.

For further details see:

RFI: This High-Yielding CEF Is Beating The Index