CME - Riding The Market's Ups And Downs With CME Group's Exceptional Dividend

Summary

- In this article, we take a close look at CME Group's fantastic dividend, which consists of consistently rising quarterly dividends and a juicy annual special dividend.

- The company's just-released earnings confirm its earnings power, especially as margins per contract improve again.

- The valuation is attractive. I remain bullish on CME.

Introduction

CME Group ( CME ) is one of the companies I bought rather aggressively last year. The company showed tremendous financial results, yet its stock price continued to fall. To some, it was a red flag, as the company reported falling revenues per contract. It caused investors to ignore its rapidly rising daily volumes and the underlying factors that caused revenue per contract to decline. As I expected in my last article , these headwinds are now fading. Moreover, while we can expect that daily volumes will be lower in 2023, the company is an attractive bargain. After its earnings, the market seems to agree.

On top of all of this, the company paid a record special dividend earlier this year and just hiked its quarterly dividend by 10%.

In other words, in this article, I will reiterate my call to consider investing in this dividend powerhouse from the Windy City up North.

Quality Financial Dividends

Supported by a top-tier business model.

Dividend investors seeking financial exposure often end up owning banks. Banks, both regional and money center banks, often have high yields and somewhat decent dividend growth. The problem is that banks are often very mature and barely growing.

Investors looking for dividend growth in the financial sector often face low yields, as dividend growth is often found in fintech niches. For example, companies like Mastercard ( MA ) and Visa ( V ) are terrific dividend growth stocks, yet their yields are low.

The Chicago-based CME Group offers the best of two worlds. It is a mature company, yet it has plenty of growth opportunities, somewhat anti-cyclical revenue growth, a great yield, and the ability to outperform the market and its financial peers.

As I wrote in December:

Buying CME was based on buying a company with a dominant position in an important industry. This lowers competition risk, and it makes it very hard to replace CME Group.

[...] The company owns agriculture futures like CBOT corn, wheat, and soybeans, which are key global benchmark futures. The company owns COMEX gold, silver, and copper futures, which are the most traded global metal futures. Moreover, the company owns the world's most liquid and traded indices futures, including the e-mini contract (S&P 500), which you may be familiar with.

[...] close to a third of total revenues are generated in the interest rate space. While this includes swaps clearing and BrokerTec, a platform that facilitates electronically traded US and European fixed-income contracts, it makes a lot of money from products like Fed Funds futures, SOFR (the eurodollar replacement), and all US treasuries across the curve.

As of December 31, the company generated its revenue in the following segments:

- 30% (of total revenues) interest rates: this includes Fed Funds futures, SOFR, etc.

- 21% equities: for example, the famous S&P 500 contracts.

- 13% market data

- 11% energy: this includes WTI and Henry Hub futures and options.

- 8% agriculture: wheat, soybeans, corn, etc.

- 7% FX

- 6% other

- 4% metals

With that said, I own CME because of its terrific dividend. The company's commitment to its shareholders is truly fantastic.

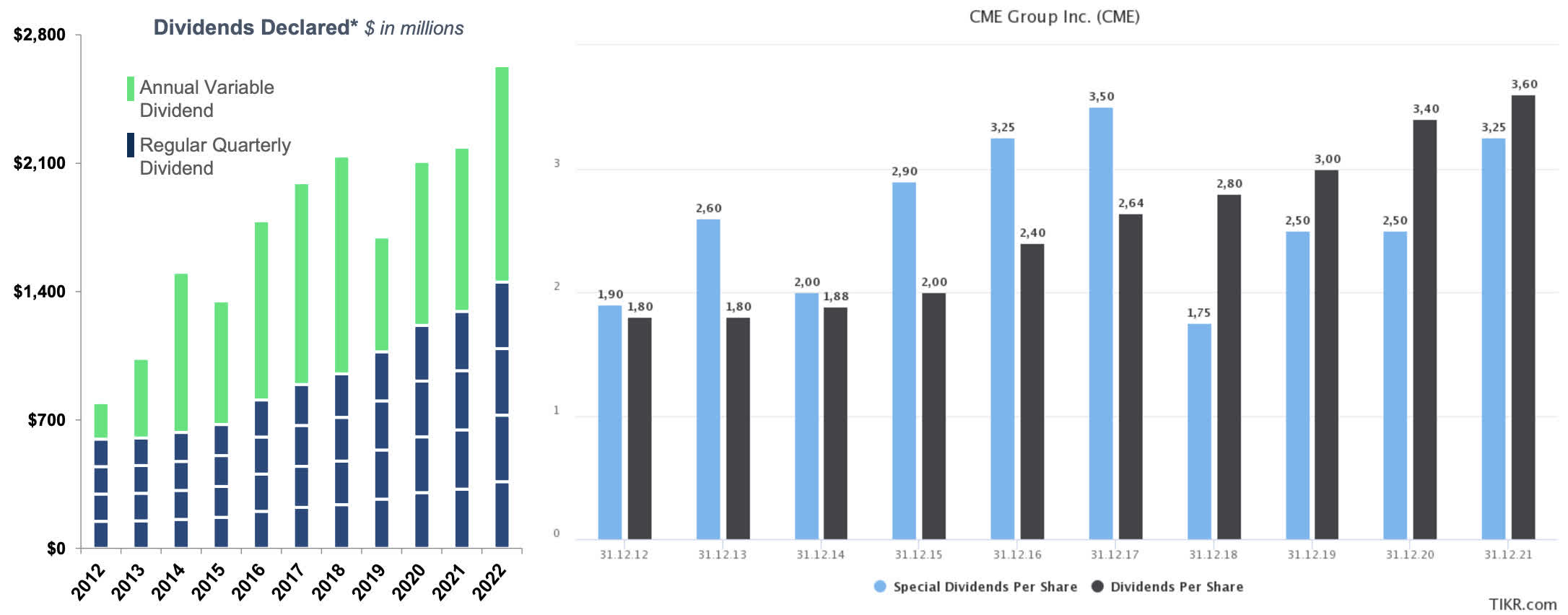

Officially, the company has a payout ratio of roughly 50%. That number isn't high, which is good news. However, we can ignore it. Why? Because CME has an annual special dividend. This special dividend is announced at the end of the year and paid at the start of the following year.

The graphs below show that the special dividend is sometimes higher than the regular dividend.

{kind=link}

The regular dividend is consistently rising. Over the past ten years, the average annual regular dividend growth rate was 8.4%.

On February 2, 2023, management announced a 10.0% hike to $1.10 per share per quarter. This implies a 2.4% dividend yield. Incorporating the pre-2022 special dividend of $3.60 (as I expect that 2022 won't be repeated this year), we get a total dividend yield of 4.3%.

On December 8, 2022, CME announced a $4.50 per share special dividend. This brought the full-year dividend yield to 4.6%.

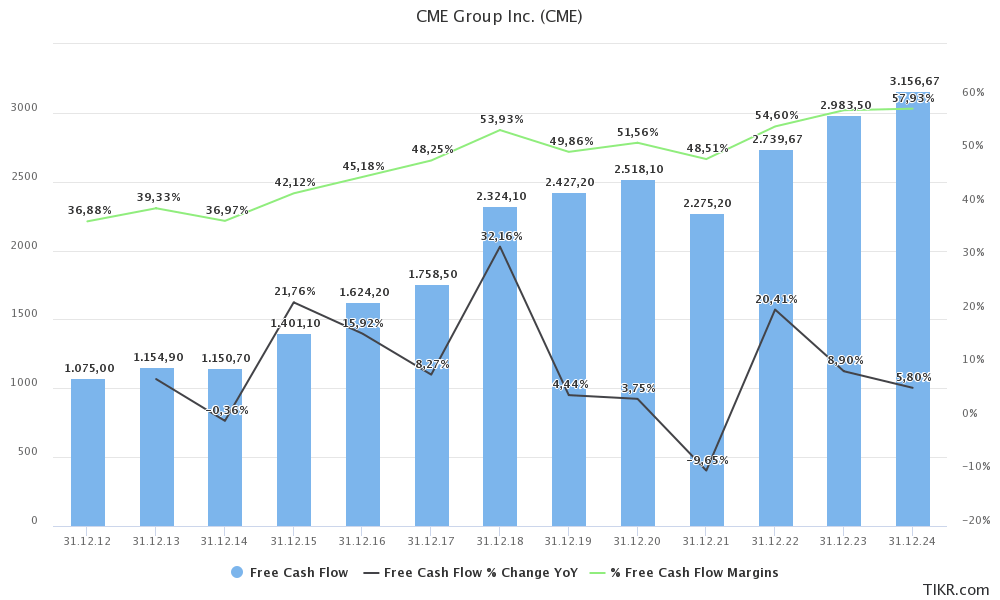

What this means is that the dividend growth number itself isn't very relevant, as weird as that may sound. What matters is free cash flow growth. After all, CME has a mature business that does not require high investments. Capital expenditures are less than 3% of total revenues, and nobody expects CapEx to rise in the years ahead. This explains why the company is able to pay a high special dividend. A steadily rising quarterly dividend is handy because it increases investors' regular cash flow. Other than that, it doesn't matter too much.

The company also has a net debt ratio of less than 0.5x, which explains why there is no need to prioritize debt reduction over shareholder distributions.

With that said, CME isn't *that* mature. It's still growing. While free cash flow tends to be somewhat volatile during and after large spikes in market volatility (it impacts total transactions), the company is consistently growing free cash flow in the mid-single-digit range. Free cash flow margins are also rising, indicating increasingly efficient operations. In 2024, the company is expected to do $3.2 billion in FCF, implying a free cash flow yield of almost 5.0%, which is terrific news for dividend investors.

{kind=link}

With that said, the just-released quarterly numbers were good news for everyone waiting for CME's stock price to take off.

The Stock Seems To Bottom

4Q22 was terrific for multiple reasons

Earlier this month, I got messages from people who were seriously worried that something was wrong with CME. The reason was the January ADV (average daily volume) number. It declined by 12%. That seems very bad. After all, CME makes money on every trade. Fewer trades mean less income.

However, there's no reason to be worried, as 2023 volumes are expected to be worse than 2022. The only way 2023 can compete with 2022 in terms of volume is if we get another bear market with volatility in all asset classes.

Whether it's the Great Financial Crisis, the 2011 debt crisis, the pandemic, or whatever we call the 2022 bear market, the company almost always saw a weaker stock price while net income soared. Once confidence in the market returns, net income growth slowed, and the stock price took off.

Now, it seems we're at such a point again. The worst volatility might be behind us, and CME is finally rising again after falling from $250 in early 2022.

FINVIZ

In this case, it helps that CME reported great earnings. Revenue came in at $1.2 billion, which is 4.3% higher compared to the prior-year quarter and roughly in line with estimates. Adjusted EPS came in at $1.92, which is $0.04 higher than expected.

The fourth quarter was a good end to the best year in CME's history. The average annual daily volume was 23.3 million contracts, an increase of 19% compared to 2021. in 4Q22, the ADV was 21.8 million contracts, an increase of 6%.

Here are some of the company's 4Q22 highlights:

- The metals ADV increased by 7%, boosted by 24% base metal and record aluminum growth.

- Total micro products ADV rose by 29%, supported by micro WTI and options contracts.

- Record quarterly ADV for combined SOFR futures and options, Equity Index options, E-mini S&P 500 options, E-mini Euro FX futures, Copper options, and Micro Copper futures.

- Record quarterly average daily notional volume (ADNV) for BrokerTec US Repo of $281 billion.

- Record Interest Rates Large Open Interest Holders (LOIH) reached on November 15, 2022, and peaked again in mid-January 2023.

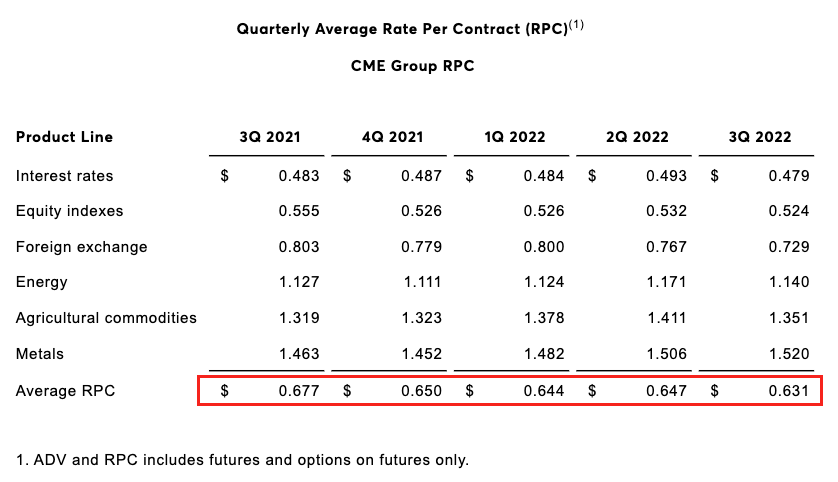

That said, there was one thing that caused some frustration among investors before the 4Q22 release. The company's RPC, or rate per contract, was weak in prior quarters.

In 3Q21, the company made $0.677 on every trade (on average). That number was $0.631 in 3Q22. While it's good news that total volume is rising, making less money per trade is somewhat of a red flag.

{kind=link}

However, this is what I wrote in my prior article:

This decline isn't perfect, but there are good reasons for it.

- The company had market-wide fee waivers in June, July, and August. These were removed at the end of August.

- The company had significant liquidity incentives in June, July, and August. These, too, are gone.

- CME still has above-average incentives for eurodollar futures and options. These will be reduced.

- RPC for SOFR options is expected to be strong, which will positively impact RPC in 4Q22.

Moreover, it is important to view lower RPCs as a way to boost volumes. For example, CME has Micro E-mini contracts (allowing traders to trade the S&P 500 and other indices with less margin). These are about 1/10 the size of the E-mini contract. However, they are about 1/4 to 1/3 of the cost. This means that CME has deliberately chosen to sacrifice RPC growth for the sake of volumes. I believe that is the right decision as these products are what drive CME's success.

With that said, I'm happy that I was right. 4Q22 RPC was $0.651, which is the highest since 3Q21.

Overall, 4Q22 futures and options RPC was 65.1 cents, up from 63.1 cents in 3Q22, primarily due to lower sequential volume leading to less incentives, a higher proportion of block trading, and product mix shifts.

Even if volumes come down in 2023, the company is in great shape to recover in the quarters ahead.

Valuation

CME is trading at 19.6x 2023E EBITDA of $3.5 billion. This is based on its $67.1 billion market cap and $1.4 billion in 2023E net debt. That seems expensive. However, it's fair, as investors mainly care for its free cash flow. Hence, the implied free cash flow yield of 5.0% makes the stock rather attractive.

I believe that CME's fair value is close to $240, with more room to grow beyond that.

Takeaway

The CME Group has once again demonstrated its ability to drive high volume growth and outperform in key segments such as FX and micros, as well as its potential for improvement in rates per contract.

Moving forward, investors can anticipate consistent growth in quarterly dividends and the possibility of significant special dividends. The company's current valuation presents a compelling opportunity for investment.

Given my confidence in CME Group's performance and dividend potential, I regret not having invested more in the company in 2022. However, I firmly believe that it remains one of the premier dividend stocks in the financial sector, and presents a solid investment opportunity at current levels.

(Dis)agree? Let me know in the comments!

For further details see:

Riding The Market's Ups And Downs With CME Group's Exceptional Dividend