GRFS - Rigel Pharmaceuticals Provides An Opportunity For Investors Or An Acquirer

Summary

- RIGL hoped to expand the label of its drug Tavalisse (fostamatinib), but the failure of the drug in phase 3 appeared to scupper its chances.

- RIGL sought guidance to see if a reanalysis of the failed phase 3 study might be well received, but it doesn't appear it was.

- Those two hits have created an opportunity for potential investors, or an acquirer, as RIGL still offers an existing revenue stream with growth prospects, and future readouts from clinical trials.

- If an upcoming readout in the 280-patient COVID trial is negative, an even better buying opportunity may arise.

Back in June, 2022, Rigel Pharmaceuticals ( RIGL ) announced the failure of its phase 3 trial of fostamatinib in warm autoimmune hemolytic anemia (wAIHA). The failure provided a buying opportunity as RIGL soon found a bottom and rallied. Another disappointing but expectable update on the wAIHA program has provided another potential buying opportunity, which is the focus of this article, and RIGL might get even cheaper again.

The wAIHA indication hits the stock twice

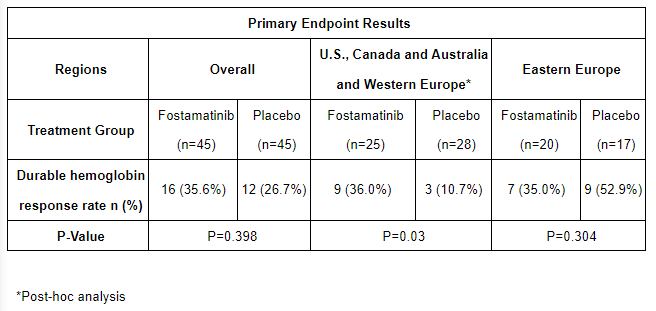

RIGL's June 8 press release , announcing the negative findings from the wAIHA trial, contained a post-hoc analysis suggesting the drug might be effective. Fostamatinib's benefit over placebo in wAIHA had fallen short of achieving statistical significance overall, but exclusion of the data from Eastern European sites yielded a significant result.

Table 1: Analysis of the primary endpoint in RIGL's wAIHA study of fostamatinib.

{kind=link}

RIGL apparently considered the possibility of submitting a supplemental New Drug Application (sNDA) for fostamatinib for the treatment of wAIHA with the reanalysed data, and sought guidance from the FDA. An October 10 press release however revealed that based on FDA feedback, that RIGL now didn't expect to file an sNDA at this time. It seems the FDA wasn't too convinced by the reanalysis. While the FDA's apparent attitude isn't surprising, the stock nonetheless took another hit.

Figure 1: Year-to-date trading of RIGL. The negative result in the wAIHA study caused the stock to drop below $1 in June, although a rally back above $1 occurred, the October 10 press release caused the stock to drop below $1 again.

There is still plenty to like

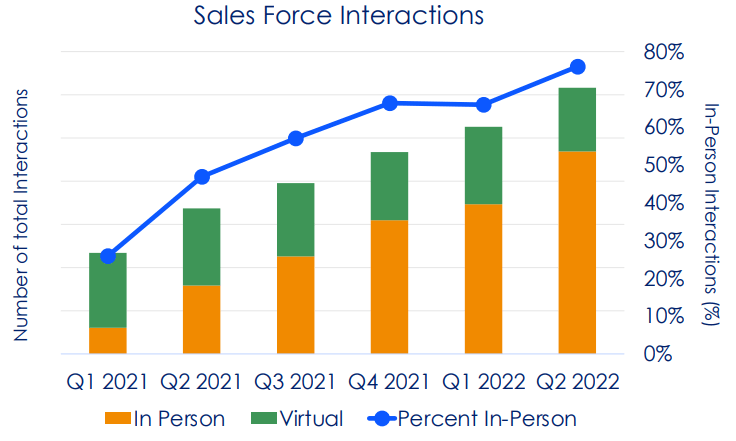

RIGL is making savings

While I've written off the wAIHA indication, RIGL would probably have to perform another trial which could take years, RIGL isn't without opportunities to boost its stock. The October 10 press release came with the news that RIGL was reducing its workforce by 16%, mostly in development and administration, which I view as a smart move. After all, the workforce cut results in just a $1.5M upfront charge due to severance but then yields $7M-$8M in reduced operating expenses beginning in 2023.

{kind=link}

Figure 2: RIGL's Tavalisse sales force interactions by quarter.

Fostamatinib royalties and milestones remain in play

RIGL's partners around the world continue to launch or move closer to launch of Tavalisse in the ITP indication, which should only see RIGL's revenues grow as it is eligible for royalties and milestones under these agreements. RIGL's Japanese partner, Kissei Pharmaceutical ( KSPHF ), paid a $5M milestone to RIGL in Q2'22 as the result of submitting NDA to Japan's Pharmaceuticals and Medical Devices Agency in April. A December 2021 press release from Kissei noted that the company had achieved positive results in a Japanese phase 3 study of fostamatinib in ITP. Given those positive results, it seems likely that Kissei's NDA will be approved, which could result in more milestones, but certainly the confirmation of a new royalty stream for RIGL.

Rigel's European partner, Grifols ( GRFS ) continues to launch the drug in additional countries, with launches in Denmark, Sweden and Finland planned. RIGL also inked a deal with Knight Therapeutics ( KHTRF ) for marketing rights in Latin America. KHTRF's September investor presentation (page 10) notes that fostamatinib is at the "Pre-Submission" stage of development but milestones and royalties owed to RIGL under the deal represent another source of revenue growth for RIGL in the future.

Upcoming readouts in COVID-19

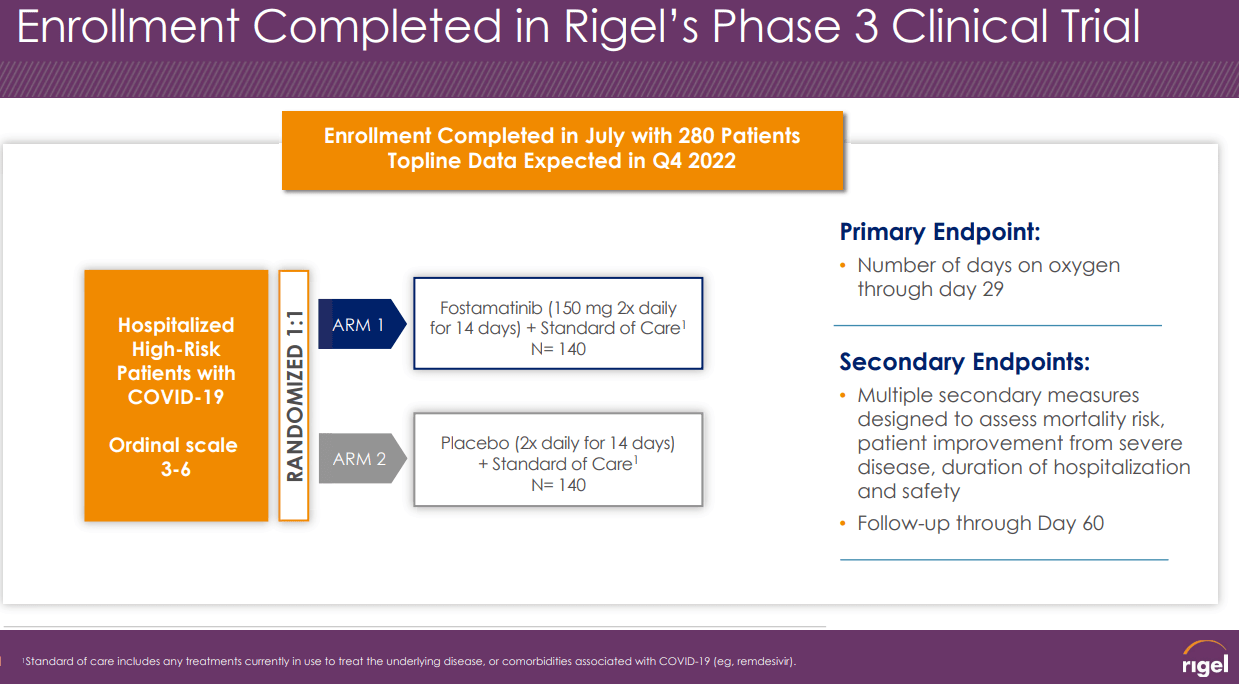

Following some delays, RIGL is finally set to report data from a 280-patient phase 3 trial of fostamatinib in high-risk patients hospitalized with COVID-19. An initial target enrolment of 308-patients wasn't reached, but 280 patients is hardly a large downsizing.

{kind=link}

Figure 3: Design of RIGL's 280-patient COVID trial.

If this readout is negative, despite encouraging phase 2 data from a 59-patient study, then RIGL still has additional shots on goal in COVID.

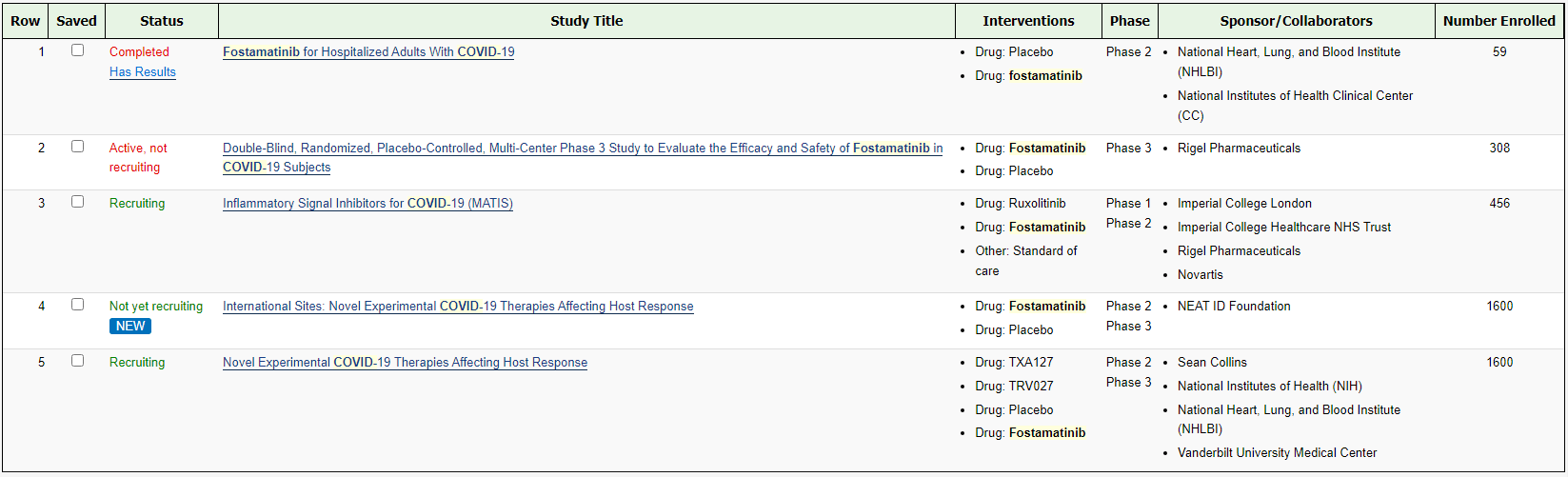

Other than RIGL's 280-patient study, there are other phase 3 studies that include RIGL's fostamatinib. These phase 3 studies include; the 456-patient MATIS study (sponsored by Imperial College London), the ACTIV-4 study which includes approximately 300 patients per arm (300 placebo, 300 fostamatinib) and a version of the ACTIV-4 study with international sites.

{kind=link}

Figure 4: Screenshot of results from a search of trials of fostamatinib in COVID. Some trials also contain other drugs, the first result is a 59-patient study from which RIGL already reported results.

There are some differences between these studies, for example RIGL's 280-patient phase 3 study includes patients with disease severity on the ordinal scale from 4 (hospitalized, oxygen mask or nasal prongs) to 6 (hospitalized, intubation and invasive mechanical ventilation). The ACTIV-4 study includes patients with disease severity on the ordinal scale from 4 to 7 (hospitalized, invasive mechanical ventilation plus additional support such as pressors or extracorporeal membrane oxygenation). If RIGL's benefit is particularly apparent in less severe or more severe disease, these differences could come into play in terms of nudging the drug over the line of achieving a statistically significant benefit.

RIGL's other drugs

Olutasidenib

On August 1, RIGL announced it had acquired worldwide commercialization rights to the mutant isocitrate dehydrogenase ((mIDH1)) inhibitor, olutasidenib, from Forma Therapeutics (formerly FMTX). Forma Therapeutics was recently acquired by Novo Nordisk ( NVO ) in a deal worth $1.1B. Forma received an upfront payment of $2M as part of the deal and RIGL is also on the hook for $17.5M in near-term milestones. Beyond that there are potential future milestones of up to $215.5M and royalties in the low teens to mid thirties percentage-wise, owed to Forma (now NVO).

I like that olutasidenib is close to potential approval in relapsed/refractory acute myeloid leukemia, with an NDA being submitted already, a Prescription Drug User Fee Act (PDUFA) date of February 15, 2023 doesn't seem too far away. Time will tell if the deal is worth it for RIGL, but it will take a few quarters of sales to get an idea of that. Those that are impatient can track the launch of competitor Servier's Tibsovo (ivosidenib).

{kind=link}

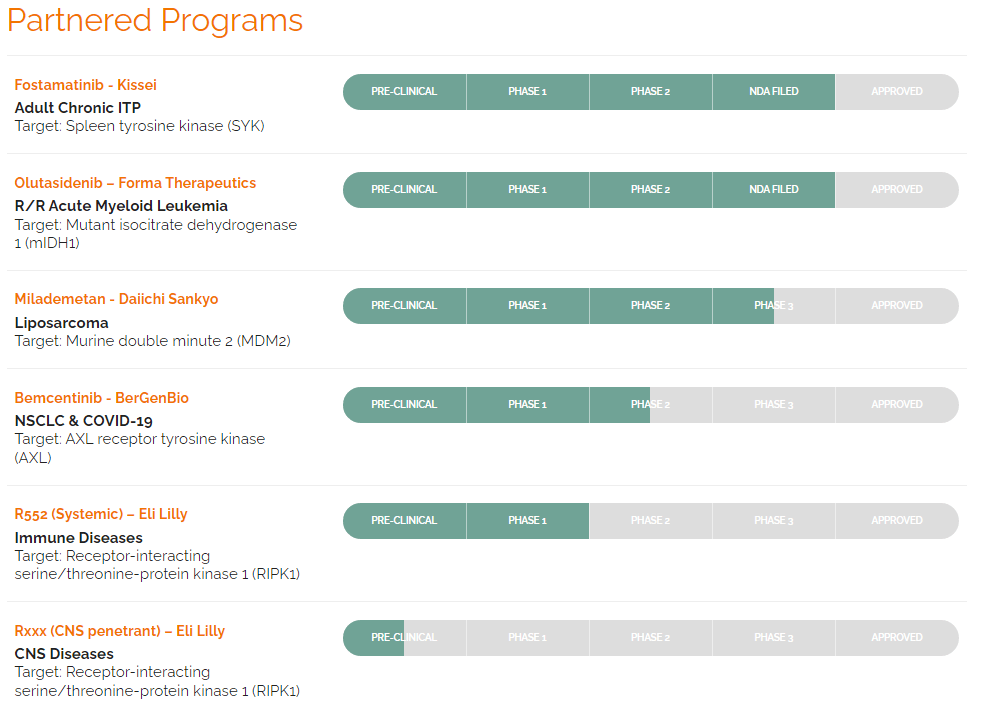

Figure 5: RIGL's partnered programs.

Higher risk programs

Outside of fostamatinib which is approved in ITP, has phase 2 data in COVID-19 and olutasidenib, which is already under review, RIGL's other programs are higher risk. I've mentioned them here for those looking at the company, but I'm not banking on anything coming for these programs, despite their promise, simply because we don't have much clinical evidence yet.

RIGL has a commitment to Eli Lilly ( LLY ) for 20% of development costs of R552 (a RIPK1 inhibitor) in the US, Europe and Japan up to a cap, but as of yet we haven't seen if RIPK1 inhibitors actually work. Still commitments to LLY and milestones due to Forma/NVO are another reason I like RIGL's workforce cuts and the savings they bring. Indeed as of June 30, 2022, RIGL notes outstanding financing liability of $53M to LLY as part of the RIPK agreement.

Then there is milademetan, while the drug is in a phase 3 study for liposarcoma, and I'd be excited to see results, as of yet we don't know if the drug actually works.

The same issue exists with bemcentinib, it's been on RIGL's pipeline slides for a while, but BerGenBio ( BRRGF ) hasn't provided a key display of bemcentinib's efficacy yet.

Conclusions and financial information

As of July 29, 2022, there were 172,836,336 shares of RIGL's stock outstanding , corresponding to a market cap of $122.7M at $0.71 per share. RIGL had cash, cash equivalents and short-term investments of $89.2M as of June 30, 2022. In July, RIGL accessed another $10M from MidCap Financial Trust through its loan facility, bringing the principal owing to $40M. Total revenues were $29.8M in Q2'22 with $18.6M coming from net product sales of Tavalisse and $11.3M from contract revenues from RIGL's collaborations ($7.5M from KSPHF, $2M from KHTRF, $1.4M from GRFS, $0.3M from LLY). Net cash used in operating activities was $38.5M in the first six moths of 2022. Net loss was $13.5M in Q2'22. RIGL expects its cash to last for at least the next twelve months. Rigel expects to report Q3'22 earnings after the close on Thursday, November 3.

While RIGL's fostamatinib has disappointed in wAIHA and this has brought the stock down, the current valuation doesn't seem to build in much growth for fostamatinib. RIGL trades currently with a price-to-sales ratio ((ttm)) of 1.44, and yet I expect sales of fostamatinib to grow, both for RIGL and its partners. Further the company has multiple shots on goal in COVID-19, with a drug that looked promising in the 59-patient phase 2 study. Outside of fostamatinib, the recent olutasidenib deal has a good chance of bringing in future revenues for RIGL, and while RIGL's other programs aren't a sure thing, additional shots on goal with milademetan and the LLY RIPK program can't be completely dismissed, they are just an unknown.

A long in RIGL has several risks, a few of which are discussed here. Firstly, the upcoming readout from the 280-patient COVID-19 study could be negative. While I argue this could be another opportunity to buy in ahead of other catalysts (other COVID readouts, milestones from partners, olutasidenib approval) the stock would very likely trade down if news from the COVID-19 study isn't good. Secondly, upcoming earnings could disappoint, increased Tavalisse sales might not materialize, for example, causing the stock to fall. Lastly, the olutasidenib NDA could be rejected, causing delays, triggering a fall in the stock.

For further details see:

Rigel Pharmaceuticals Provides An Opportunity For Investors Or An Acquirer