WBA - Rite Aid Q4 2023 Earnings Preview: What To Expect?

2023-04-19 09:10:42 ET

Summary

- Bears are betting heavily against Rite Aid Corporation ahead of the earnings report.

- RAD must post stronger fiscal Q4 results to win back shareholders.

- Walgreens Boots Alliance, Inc. and CVS Health Corporation and discussed.

After Rite Aid Corporation ( RAD ) posted third-quarter results, investors sold the stock. RAD stock fell by around 13% . Since then, the stock has lost almost one-third of its value.

Investors who considered Rite Aid’s competitors only fared relatively better. CVS Health Corporation ( CVS ) dropped by 14.8% in the quarter while Walgreens Boots Alliance, Inc. ( WBA ) fell by 2.06% in the period. Walgreens fell by less on favorable low valuations. Its forward price-to-earnings ratio is currently only 7.4 times. The stock pays a dividend that yields 5.4%.

Rite Aid Q4 2023 Earnings Expectations

Concerns that shareholders face a massive dilution or get wiped out will matter more than the Q4 2023 earnings report that is expected premarket on April 20. Results will still move RAD stock one way or another. According to its earnings history , the drugstore beats expectations half the time.

seekingalpha

For FQ4 2023, analysts expect Rite Aid to lose 77 cents a share. Investors who look at the next several quarters should expect negative year-on-year growth to improve to -10.17% by FQ4 2025:

seekingalpha

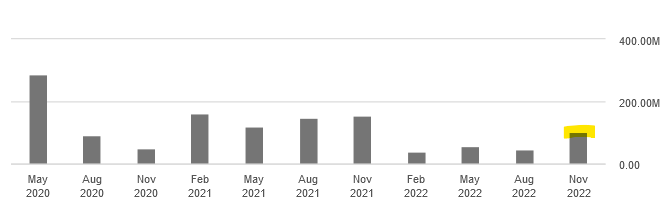

Cash on hand will matter in the earnings report. The company needs to cover the persistent losses in the next several quarters. Cash on its balance sheet improved steadily recently:

{kind=link}

According to its cash flow statement , Rite Aid had heavy non-cash restructuring charges in the May and August 2022 quarters. Inventory levels increased. It offset the negative cash flow with lower capital expenditure and the sale of property, plant, and equipment.

Debt Balance

Rite Aid said that it ended last quarter with $3.1 billion . It continued to build its CMS receivable for 2022 and seasonal inventory in its regional business. In the upcoming report, shareholders need to see the company report strong revenue and no inventory write-down. Without those two data points, investors will not have the confidence that it will report positive free cash flow for 2023.

Rite Aid needs cash flow to pay down its debt. It faced higher-than-expected retail margin pressures in the last quarter. Pharmacy margins also hurt its previously issued forecast in its last report. If those pressures continue in the reporting period, it would validate the short-seller's bearish thesis.

Bears have a short interest of 25.31% .

Covid Catalyst Absent

Between late 2020 and some of 2022, drugstores benefited from higher customer traffic. People needed Covid-related vaccines, cold medicine, and Covid testing. Rite Aid modeled only $5.2 million from the Covid vaccine. Furthermore, it factored in negligible PCR (polymerase chain reaction) and antigen tests. At the most optimistic level, investors should expect no more than $20 million in EBITDA, as Executive Vice President and Chief Financial Officer Matt Schroeder guided.

In Q3/2023 , same-store sales increased by 7.5%. Pharmacy sales increased by 9.5%. With Covid immunizations excluded, prescriptions increased by 3.6%. For Q4/23, shareholders should expect maintenance prescription growth of at least 2.1%. In addition, same-store acute prescriptions should grow again by at least 8%.

Rite Aid previously improved its overall prescription market share by 20 basis points. It had an 11% market share. The company should report a benefit from the flu immunization season.

Related Investments

Investors who took advantage of Walgreens stock trading in the low $30s would have returns of up to 17%. The company remains an attractive turnaround story after it posted a profit and revenue growth. Walgreens reported Q2 non-GAAP EPS of $1.16 on revenue growth of 7.6% Y/Y to $34.9 billion.

More importantly, Walgreens maintained its full-year EPS guidance of $4.45 to $4.65.

CVS Health is in a sustained downtrend. After failing to break out above $100 - $105 since Oct. 2022, bearishness continued. CVS stock trades at a P/E of only 8.79 times. Investors are fearful that CVS overpaid for Signify. It bought the healthcare platform for $8 billion , closing the acquisition last month.

According to SA Premium, CVS has strong profitability, while Walgreens and Rite Aid have a strong valuation grade of A- and A+, respectively.

SA Premium

The quant rating is neutral for all three drug stores. Wall Street’s "strong sell" rating for RAD stock is notable:

SA Premium

Your Takeaway

Bears continue to hold their bet against Rite Aid Corporation. They believe the business will continue struggling. It will take only surprise revenue results to squeeze bearish investors.

Long-term investors will need Rite Aid to post consistently stronger same-store sales and higher prescription volumes beyond this quarter. Without that trend, Rite Aid Corporation stock cannot form an uptrend from here.

For further details see:

Rite Aid Q4 2023 Earnings Preview: What To Expect?