SBNY - Rithm Capital: Undeservedly Priced For A Crisis

2023-05-08 10:00:00 ET

Summary

- Rithm Capital reported a solid first-quarter earnings release, highlighting its ability to thrive in "all interest rate environments."

- RITM has held its March lows robustly, as buyers have not panicked further. However, buying sentiments remain fragile, as the banking crisis has not abated.

- Rithm sees increasing opportunities in the commercial real estate space, which could be the next shoe to drop.

- With RITM priced at an attractive next twelve months dividend yield of 12.7%, investors should consider capitalizing while sentiments remain pessimistic.

Rithm Capital Corp. ( RITM ) investors have managed to hold the defense line they established in March following the collapse of Silicon Valley Bank ( SIVBQ ) and Signature Bank ( SBNY ).

We updated investors in March that the collapse could find investors rushing back as RITM has dropped back into attractive zones. However, while buyers have generally not panicked further, they have not rushed back as well, as RITM has been consolidating over the past six to seven weeks.

RITM last traded at an NTM dividend yield of 12.7%, just below the one standard deviation zone above its 10Y average of 11.6%. Therefore, RITM is attractively valued, as investors remain concerned.

Hence, it seems like the current consolidation could be an accumulation zone, even as momentum buyers are likely still on the sidelines, awaiting more clarity from the banking fallout.

The leading mREIT posted a decent FQ1'23 earnings release , delivering earnings available for distribution or EAD of $0.35, down 5.4% YoY. However, it's much better than FQ4's 17.5% decline and FQ3's 27.3% drop, suggesting its operating performance has not deteriorated.

Management assured investors that the company continues diversifying its business model with the Rithm 2.0 roadmap , moving beyond its operating companies and pivoting toward alternative asset management .

Moreover, the company maintains a strong slate of liquidity, posting a liquidity position of about $1.5B. As such, management assured investors that the company is "in a strong position to take advantage of market dislocations."

Rithm Capital reminded investors that it's "starting to see" opportunities in the commercial real estate space. However, given the recent banking crisis, the commercial real estate space could be the next shoe to drop, worsened by possible tightening in lending standards by banks.

As such, the company sees opportunities to participate as a direct lender "focused on distressed asset strategies or acquiring distressed assets." However, investors should be assured that the company is likely not focusing on the troubled office property space, maintaining its core focus on "development deals around multifamily."

With that in mind, Rithm has proved that it could sustain its diversified operating model through low and high interest rate environments. Moreover, management assured investors it's primed to "generate attractive risk-adjusted returns in all interest rate environments."

Wall Street analysts' estimates largely concur with management's optimism. Moreover, Rithm Capital is projected to report an EAD of $0.35 over the next two quarters, suggesting things aren't likely to worsen.

As such, it should proffer robust defense for the company's dividend yields, with an annualized dividend per share of $1, representing a projected payout ratio of about 70%.

Despite that, we assessed that the market remains tentative over the recent banking crisis, as investors anticipate a further fallout in the space. It could explain why buying momentum has remained tepid, even though its valuation seems attractive.

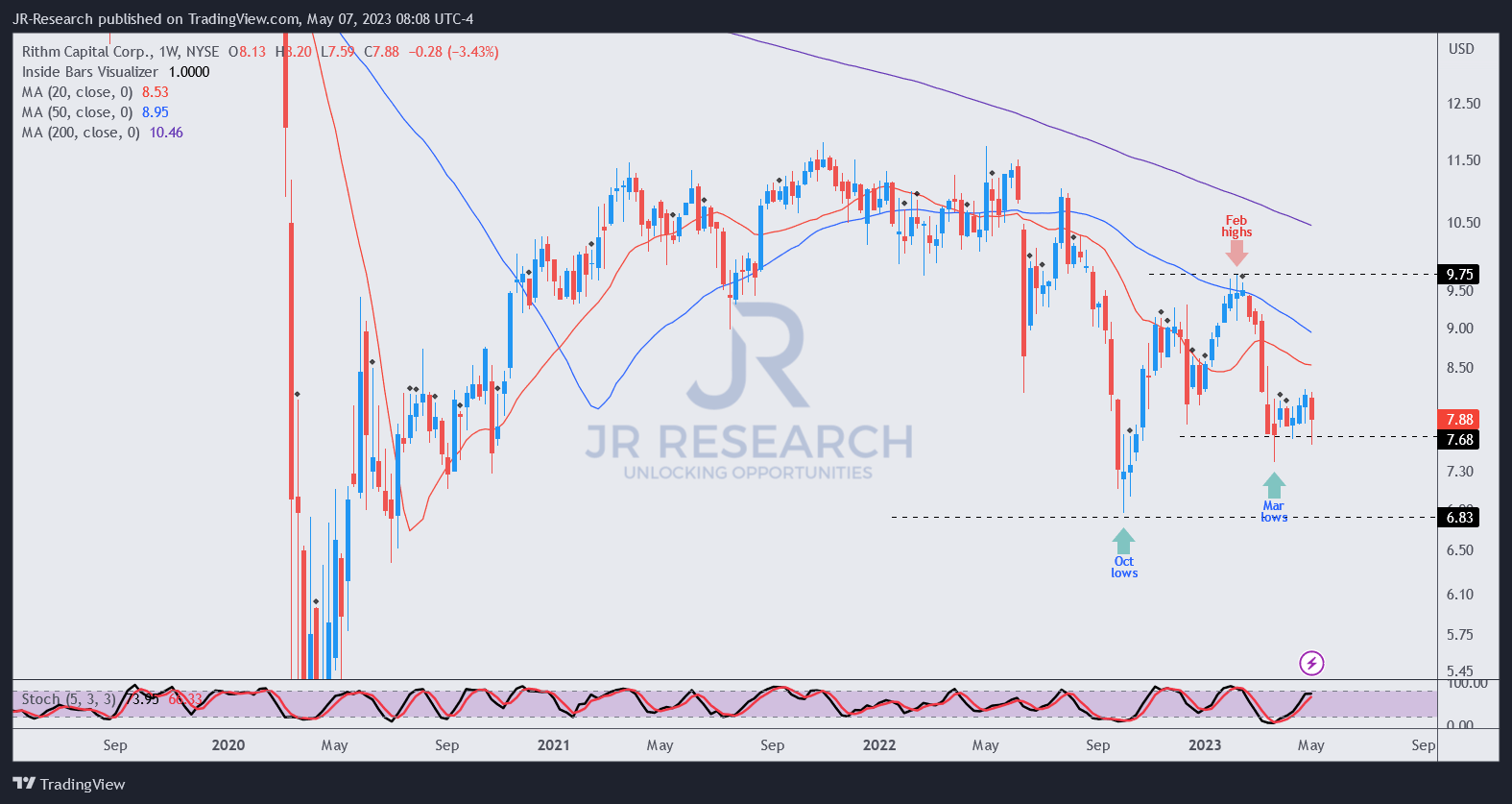

RITM price chart (weekly) (TradingView)

{kind=link}

As seen above, RITM buyers continue to hold the defense line established since its March lows.

With Rithm not expected to post worse EAD over the next two quarters, selling pressure should abate from here.

Despite that, investors must remain patient, as buying sentiments are expected to remain fragile and volatile as the banking crisis could worsen, leading some investors to panic.

However, we view the consolidation zone as constructive. Hence, investors should consider capitalizing on it before momentum buyers return, anticipating that the worst of the crisis could be over in due course.

Rating: Buy (Reiterated).

Important note: Investors are reminded to do their own due diligence and not rely on the information provided as financial advice. The rating is also not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have additional commentary to improve our thesis? Spotted a critical gap in our thesis? Saw something important that we didn’t? Agree or disagree? Comment below and let us know why, and help everyone in the community to learn better!

For further details see:

Rithm Capital: Undeservedly Priced For A Crisis