HOOD - Robinhood: Turning A New Profitable Corner

2023-10-02 13:42:08 ET

Summary

- Robinhood has transformed into a solid business with a diverse range of financial services and a focus on growth opportunities.

- The company has successfully reduced operating expenses and increased net revenues, particularly in the interest segment.

- Robinhood achieved GAAP profitability in Q2 2023, demonstrating its strategic approach and sustainability as a business.

- As such, we believe HOOD is currently a Buy.

Introduction

Robinhood ( HOOD ) gained notoriety during and following the 2020 COVID-19 stock rush, as it became the go-to brokerage platform for many new retail investors and traders. Their new-gained popularity made the company go public in 2021, and the stock quickly soared to $85. Since then, the stock is down almost 90% off its all-time high and trades below $10.

Despite the crash and burn story this might look like, there is more to like about HOOD than there is to dislike right now. At this point in time, HOOD has transformed into a solid business that continues to look for growth opportunities and remain financially stable.

In this article, we will discuss some of the attractive points within their business model, how they have reduced costs and become profitable, and how they are valued against peers. Finally, we will take a look at HOOD’s chart.

An Attractive Business Model

Many new investors were driven to Robinhood initially because of their commission-free stock trading and, later on, commission-free options trading. The user-friendly mobile app, characterized by its vibrant interface, facilitated ease of use and encouraged increased trading activity. This approach aligned with the company's primary revenue source, which centered around the payment for order flow. Furthermore, the company introduced a premium subscription tier that offered features such as margin trading for a monthly fee.

However, Robinhood soon began to shift its focus. As interest rates started to rise in 2022, low-risk investments started to become more popular. As a result, there was a noticeable decrease in user engagement in stock trading. This led to a decline in revenue from this segment. In response, the company recognized the need for adaptation and transitioned toward becoming a more comprehensive financial services firm.

One of its significant endeavors is in the retirement investing sector, traditionally dominated by established brokerage firms. Robinhood introduced traditional and Roth investment retirement accounts (IRAs), which have proven highly attractive, accumulating over 325,000 IRAs with assets exceeding $1 billion.

Today, Robinhood offers a 1% match on eligible IRA deposits for at least five years. This also includes new contributions and transfers from other retirement accounts. Premium subscribers to Robinhood Gold, who pay a monthly fee of $5, receive a 3% match, a distinctive offering as it provides an IRA matching benefit without the need for employer participation.

In addition, Robinhood’s strategic evolution includes the introduction of retirement accounts and credit card services, the establishment of a 24-hour market for highly liquid stocks, expansion into the UK market, the rollout of stock screeners, the introduction of the Robinhood Wallet and Robinhood Connect features, and the offering of a high-interest savings account.

These initiatives collectively represent its commitment to diversifying its services and increasing its market share. They show the strategic shift from a commission-free stock trading platform to a multifaceted financial services provider, reflecting adaptability and ambition to meet evolving market demands.

Reduced Costs And Many Growth Opportunities

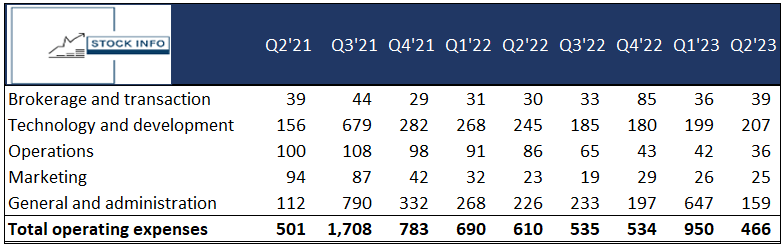

The company's continuous efforts to enhance efficiency are conspicuously reflected in its recent financial report. Notably, Robinhood's operating expenses witnessed a substantial decline of 50% between Q1’23 and Q2’23.

This reduction in operating expenses is particularly significant when viewed in the context of revenue, as operating expenses constituted 192% of revenues in Q2 2022 but dropped to 96% in Q2 2023.

Stock info and Robinhood, in millions of USD

{kind=link}

This reduction in expenses is pervasive across almost all categories. General and administrative costs notably decreased by 30% YoY, instilling confidence in investors, especially following a substantial increase in Q1 2023 driven by a $485 million share-based compensation expense. Even technology and development expenses decreased by 15% despite the company's vigorous pursuit of its product roadmap.

In addition, marketing expenses remained relatively modest, with only a 9% increase YoY. Crucially, this restrained approach to marketing expenditure did not impede the company's ability to expand its Net Cumulative Funded Accounts, a pivotal metric signifying the number of long-term users during the quarter.

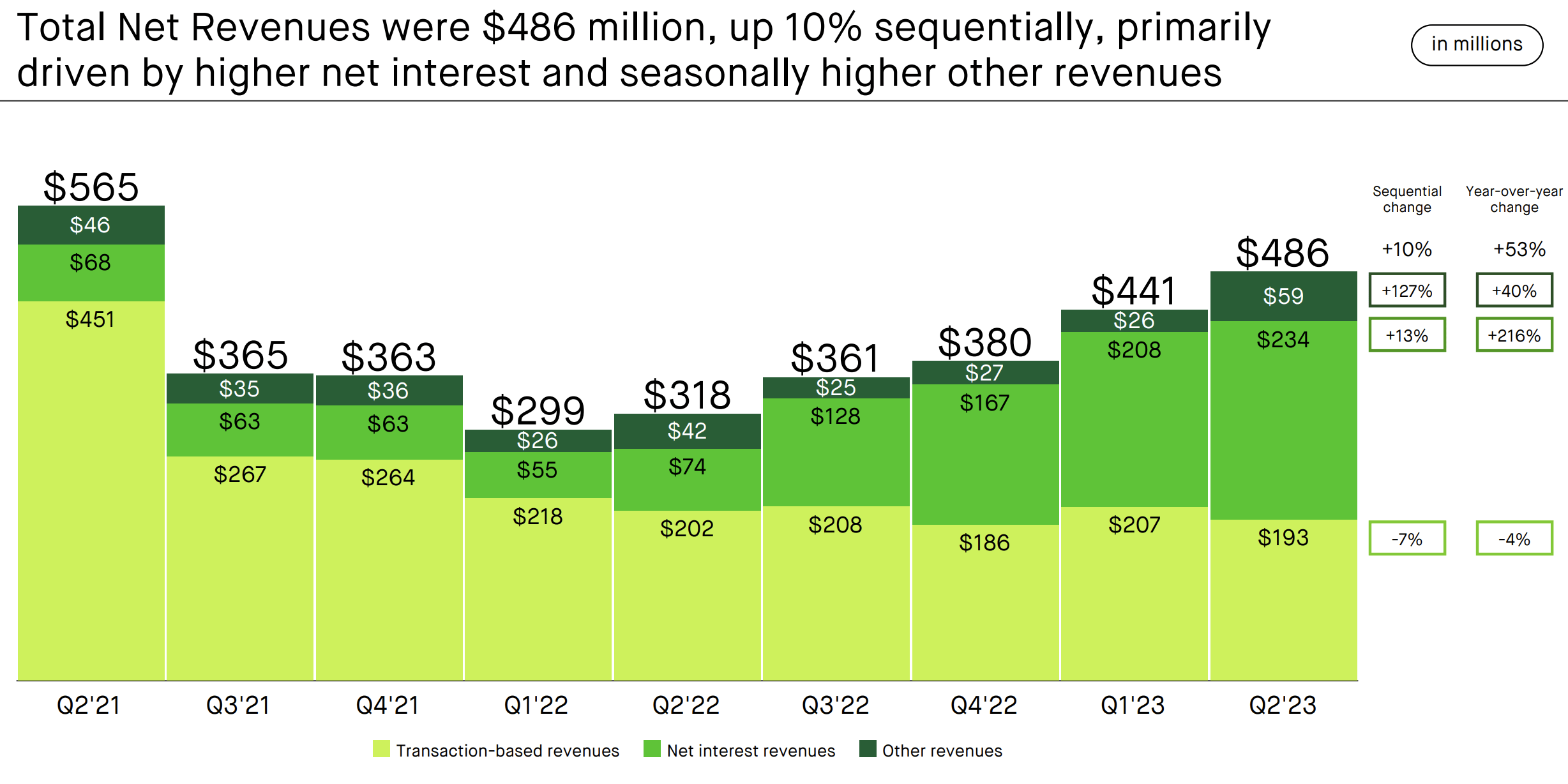

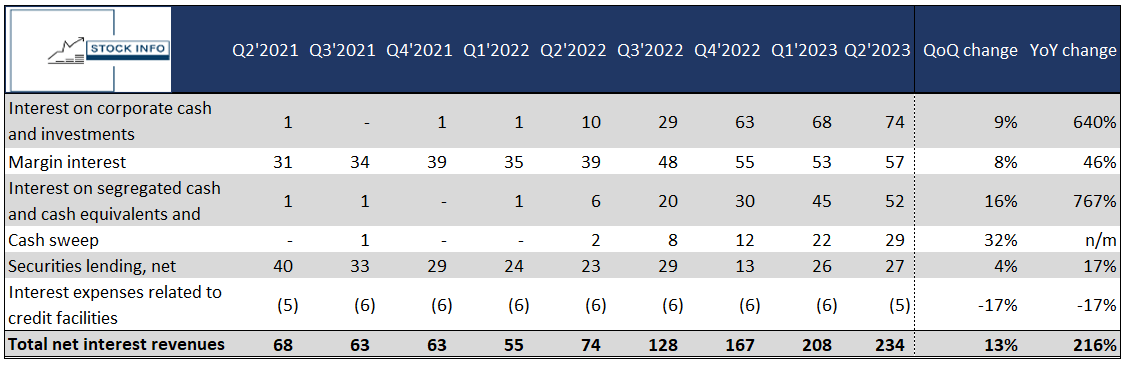

In addition to its cost-cutting endeavors, HOOD has steadily increased its net revenues, especially in the revenues from the interests segment. This may not surprise, given the interest rate regime the US and EU are currently in. This trend will likely continue as rates could remain higher for longer .

{kind=link}

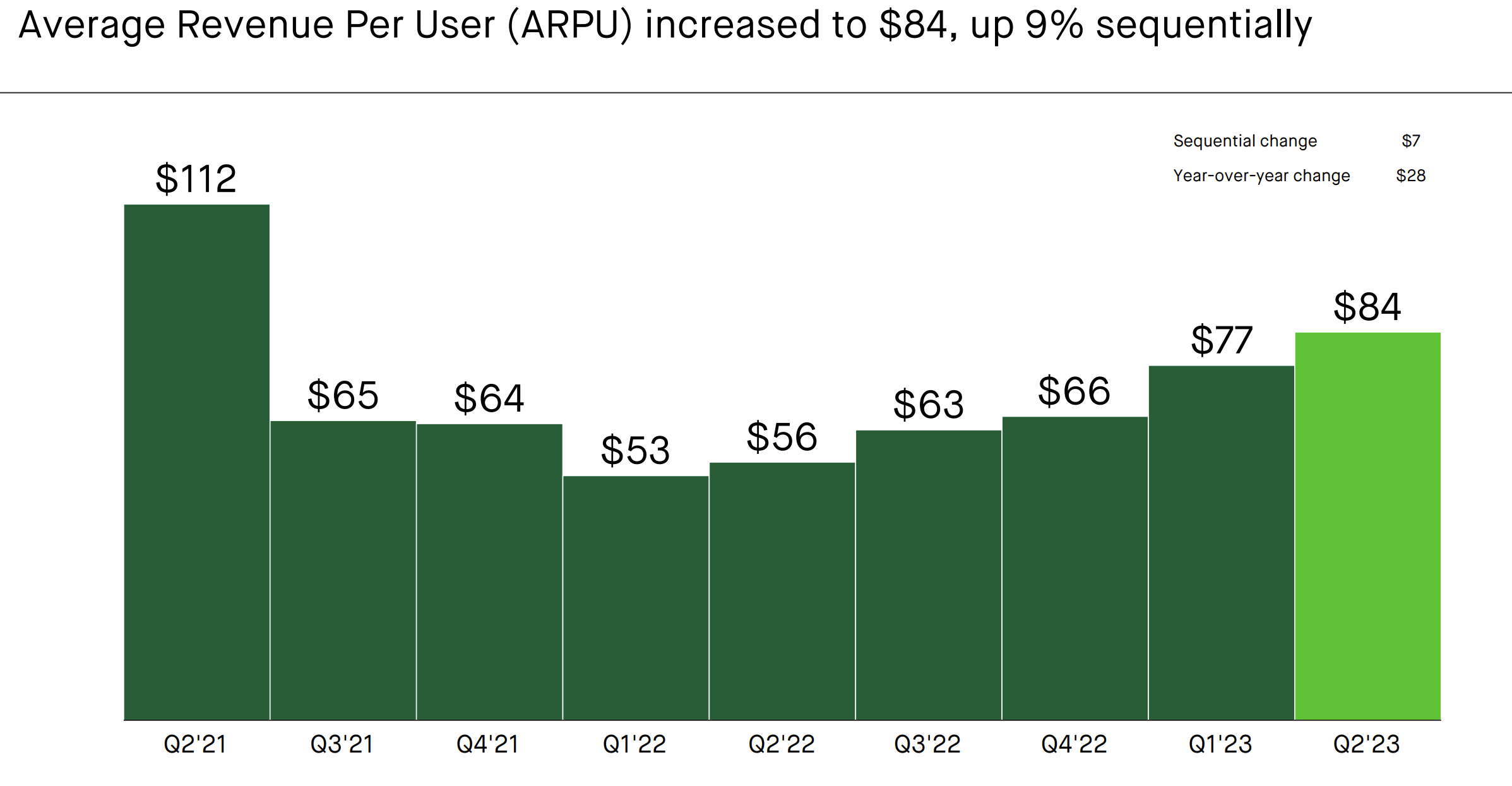

Another noteworthy metric is the average revenue per user (ARPU). Robinhood has made substantial strides in aligning ARPU with levels observed during the pandemic when ARPU oscillated in the $100-110 range.

The prevailing trend is encouraging, with Q2 2023 marking the sixth consecutive quarter of positive ARPU growth. ARPU reached $84 during this period, the highest in the past two years. This progress underscores the company's ongoing efforts to optimize its financial performance and its ability to generate more revenue from each user.

{kind=link}

Remarkably, even as Robinhood cut 23% of its workforce , the company's pace of product development remained virtually unaffected. Over the past year, the platform successfully introduced many tools and services we mentioned earlier.

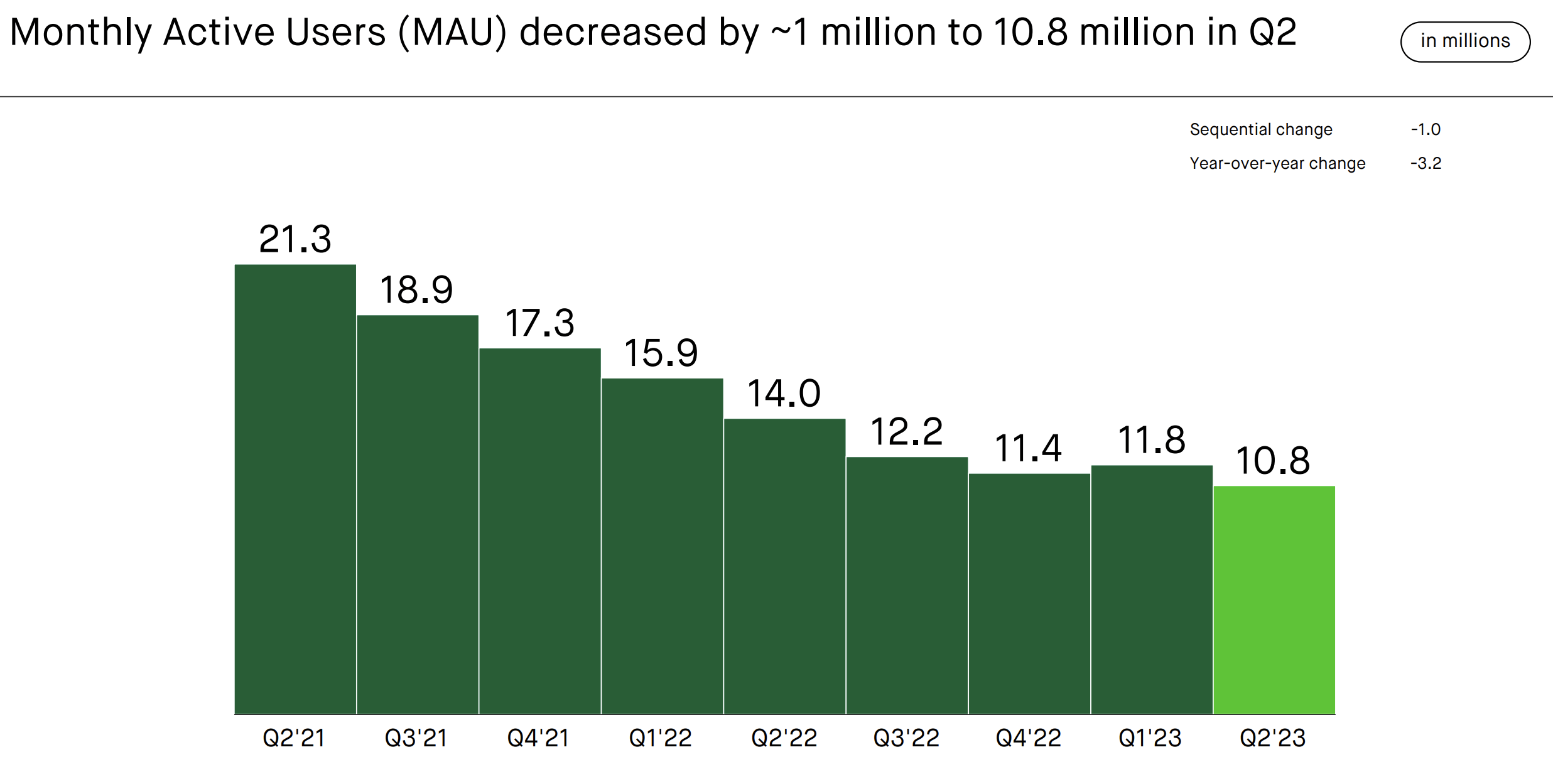

It is also important to mention that its monthly active users have declined since its IPO. This is a risk, as users will drive revenue for HOOD.

{kind=link}

That said, we see an overall trend for HOOD, where they can both steadily cut costs and build up their revenue streams. This is a trend we do not foresee change any time soon.

Robinhood Is Now Profitable

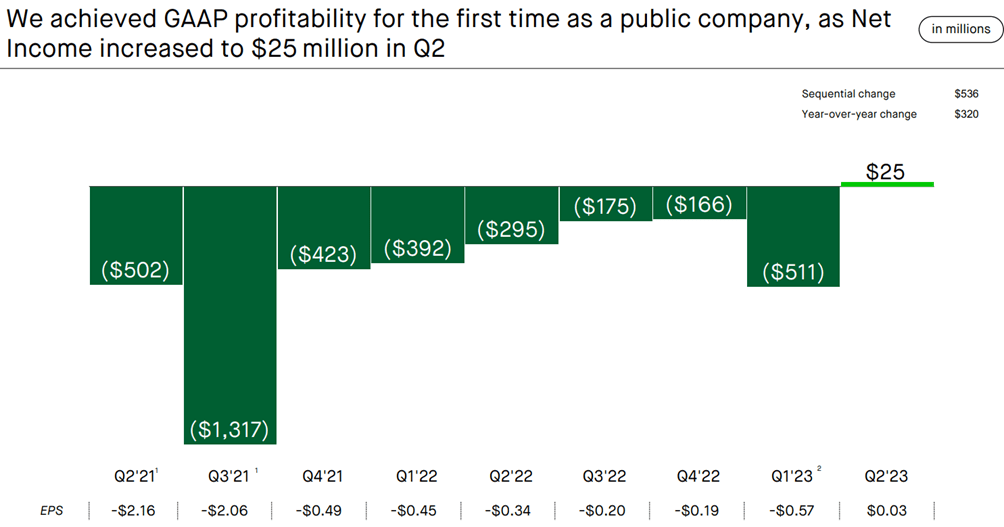

Robinhood’s recent strategic moves have already shown promising results, as evidenced in its latest quarterly report for Q2 2023. In this report, Robinhood met and exceeded expectations, achieving remarkable growth in both revenue and earnings. One standout highlight was an impressive 53% year-over-year revenue growth, a significant milestone. Equally noteworthy is that the company achieved GAAP profitability, which it hadn't accomplished since its IPO.

Given the current investment climate, this achievement is significant for investors, which places a high value on profitability and value-oriented investments. Robinhood's positive GAAP earnings per share ( EPS ) position it favorably among a broader range of investors and could potentially drive further stock growth.

This milestone demonstrates the effectiveness of Robinhood's strategic approach and reaffirms its business model's sustainability.

This achievement is even more impressive because it was realized despite ongoing investments in product enhancements, which are typically expensive endeavors. This indicates that the company has managed to maintain the quality of its services and products while achieving favorable financial results.

On the revenue side, a significant growth driver was the strong performance of net interest revenues, which we also discussed previously. Notably, the primary contributors to this growth were interest earnings on corporate cash and investments, which increased by an astonishing 640% year over year, and interest earnings on segregated cash and deposits, which saw a remarkable 767% year-over-year surge.

{kind=link}

Furthermore, Robinhood's financial strength is highlighted by its cash and short-term investments balance, exceeding $6 billion, constituting nearly 65% of its market capitalization. This represents an attractive value proposition for investors, even considering the company's $3 billion in long-term debt.

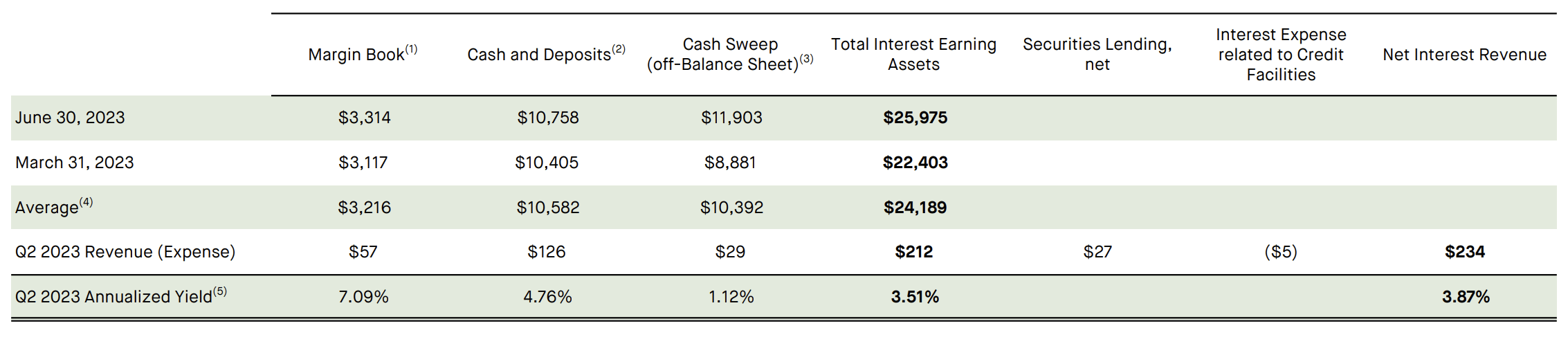

Robinhood's recent initiatives, particularly those aimed at strengthening relationships with existing customers, are starting to yield positive results. For instance, Robinhood's offering of an attractive 4.90% interest rate resulted in a substantial cash sweep balance of $11 billion, a notable increase from $8 billion at the end of Q1.

{kind=link}

Robinhood remains on track to launch its brokerage services in the UK by the end of 2023, with reports indicating the commencement of crucial role hirings in Q2. Additionally, the company introduced 24x5 hour market access for select stocks and ETFs, available to all customers as of July 2023, further enhancing its customer offerings.

Robinhood's fundamental strength is evident in the growing cash sweep balance, reaching $ 13.3 billion in August , up from $12.7 billion in July and $11 billion at the end of Q2. This demonstrates that customers perceive Robinhood as a relatively secure destination to invest their funds while earning an attractive 4.9% interest rate. The company's plans for a significant buyback of nearly 55 million shares previously held by Emergent Fidelity Technologies, equivalent to 6% of its float, are further facilitated by its substantial cash reserves of $8.5 billion.

Notably, expectations are rising as Robinhood's projected earnings per share ((EPS)) for Q3 2023, to be reported in early November, have shifted from an initial estimate of -9 cents per share at the beginning of the year to breaking even. This shift reflects growing confidence in the company's ability to generate revenue and establish consistent operational profitability in the near future. These developments underscore Robinhood's path toward financial stability and market leadership.

You may ask yourself whether their second quarter is just a “one-off,” and by Q3 or Q4, they will be back losing money. First, we would like to emphasize the trends we have seen in the graphics above, which clearly show a trend of cost-cutting and higher revenue per user on the platform.

We can see the trend more prevalently in the graph below, where their EPS has been trending towards a positive number since Q4’21 (with Q1’23 being an outlier due to a $485M charge related to 2021 Founders Award Cancellation).

{kind=link}

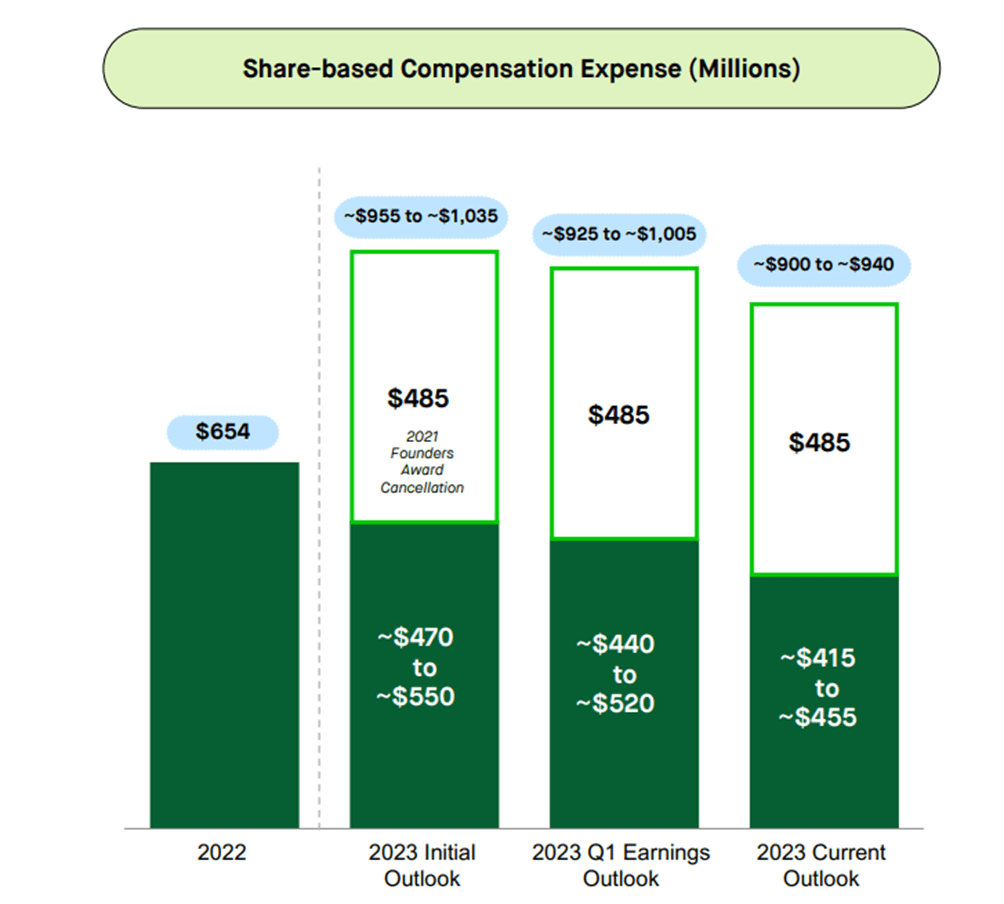

In addition, HOOD is committed to lower its stock-based compensation expenses going forward, as seen below.

{kind=link}

Therefore, we believe HOOD’s continuous strides in cost-cutting and revenue-generating strategical implementations are finally starting to pay off.

If they continue to trend this way, which we see them do, Q3’23 could become even better than the previous quarter.

Comparative analysis

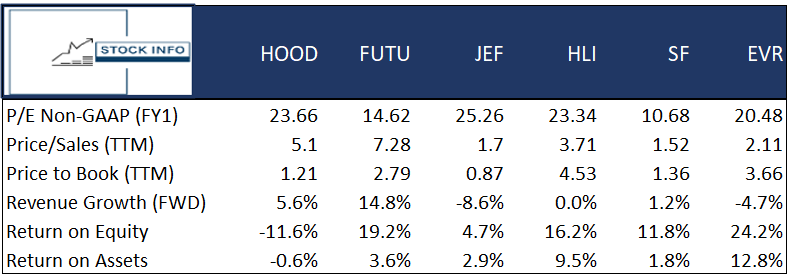

To gauge whether Robinhood is currently at an attractive valuation, looking at how it compares to other competitors is always favorable. The figure below compares the P/FCF between HOOD and several of its competitors. At first glance, we can see that HOOD trades around 7.5 times its FCF and only SF trades at a lower price.

In addition, HLI and JEF trades at significantly higher P/FCF, which could signal that HOOD is trading at quite a significant premium. In our view, it would seem that HOOD is currently undervalued compared to its peers, based on this parameter.

Ycharts

The picture gets a little murkier if we examine various other metrics, both in terms of growth, profitability, and valuation. HOOD's P/E ratio for the next fiscal year FY1 is 23.66, positioning amongst the middle of its peers. While exceeding SF and EVR, it falls short of FUTU, suggesting the market’s relative confidence in HOOD's future earnings potential remains close to its peers.

Regarding P/S ((TTM)), HOOD's ratio is 5.1, which is on the higher end of the rest of the included peers. HOOD's P/B ((TTM)) ratio stands at 1.21, placing it similarly to SF and higher than JEF. Trading at a P/B of 1.21 is still relatively low, suggesting that HOOD still has room to raise in price. HOOD's projected revenue growth for the forward period is 5.6%, trailing FUTU's 14.8%, but a projected growth of 5.6% remains well above the rest.

Unfortunately, HOOD reports negative ROE and ROA. However, Q2 has shown us that HOOD has become profitable. Therefore, we believe it is quite possible that these metrics can improve shortly as well. Looking at these metrics and the P/FCF, we see that HOOD may be undervalued compared to its peers.

{kind=link}

Technical Analysis

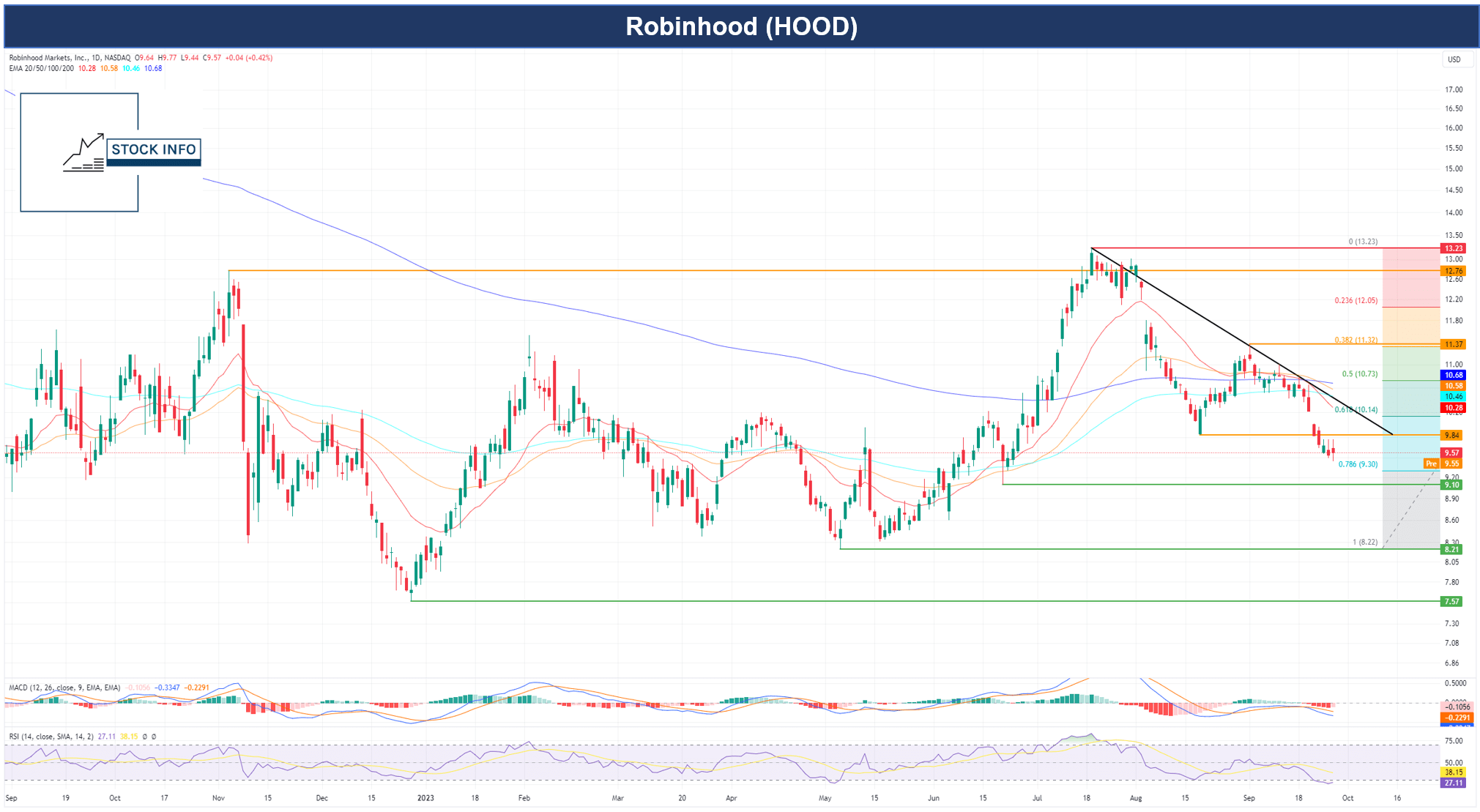

Moving on to the technical analysis of HOOD’s 1-year chart, we see an opportunity for an exciting entry point.

{kind=link}

Specifically, HOOD is currently between the 0.618 and 0.786 Fibonacci levels, at $9.30 and $10.14, respectively. In addition, there is also a level that acted as strong support back in June at $9.10. The range between $9.30 and $9.10 could be a good entry point for investors, whether they’re averaging down on an existing holding or a whole new position.

Investors should be wary of $9.84, a level of support broken through around mid-September. If the stock revisits this level, it could be a case of break-and-base price action, meaning HOOD could keep its downward trajectory.

Another point of interest is the trendline shown in black, which HOOD has respected quite a few times in the last couple of months. The trendline is heading into the Fibonacci zone mentioned earlier, which can be challenging for the stock to break.

In addition, the stock trades below all included EMAs, which is bearish overall. However, if we look back briefly to September 2022 and ahead, it's clear that HOOD has never truly respected these. Nevertheless, it can still be challenging for the stock to break.

Here is the kicker, though; if we look at the RSI, it is currently below 30, thus showing that HOOD is very oversold. In addition, the MACD is starting to show upward momentum. These two combined could give HOOD the kick it needs to surpass the trendline and EMAs. Thus, we believe opening a position in the $9.10-$9.50 area could be a good entry point.

Conclusion

Robinhood's transformation from a platform known for commission-free stock trading to a versatile financial services provider shows how adaptable it is in a changing market. Their ability to cut costs while boosting revenue, especially in the interest area, highlights their resilience and potential for ongoing success. With promising valuation metrics, a compelling technical analysis, and a clear commitment to staying financially stable, Robinhood looks like an appealing investment opportunity ready for further growth.

For investors, keeping an eye on Robinhood's short-term price action could be very profitable. We are currently watching the $9.10-$9.30 level. Higher prices may still be viable entry, too, however. It is still important to watch how the stock will react in case of a revisit to $9.84.

Regardless, we believe Robinhood has enough growth potential and limited downside risk and, therefore, rate it a buy.

For further details see:

Robinhood: Turning A New Profitable Corner