RBLX - Roblox: 'Magnificent' Potential

2023-11-20 08:27:32 ET

Summary

- Roblox delivered strong Q3 results, with $713 million in sales and a 38% YoY growth, driven by growth in all regions.

- The company is focused on cost control and operating leverage to drive profitability, with a reduction in infrastructure costs and plans for future cost efficiency.

- Roblox has significant growth potential in internationalization, AI, advertising, and platform expansion, with financial objectives aiming for a 20% annual growth rate in bookings and increased EBITDA margin.

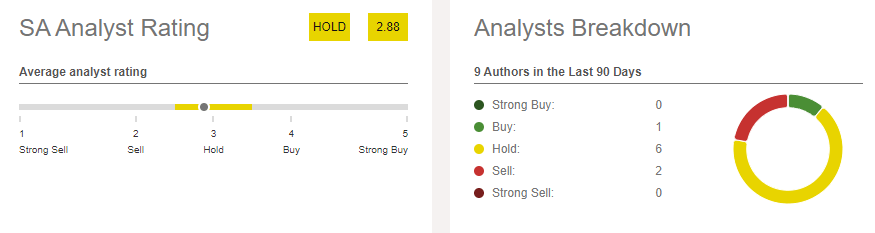

Roblox (RBLX) does not see much love on Seeking Alpha. Over the past 90 days, Seeking Alpha analysts assigned six Hold recommendations, and two sell, compared to only one Buy recommendation. And this lone bull standing, the one with the Buy recommendation, that is me.

{kind=link}

I am completely unconvinced by all the bearishness contrasting to my bullishness. In fact, following an exceptionally strong Q3 reporting , with DAUs reaching new all-time highs, I am more than ever convinced that Roblox could grow into a centi-billion consumer platform (like the "Magnificent Seven"), building on two-sided consumer/ vendor network effects.

For reference, Roblox stock is up about 36% YTD, outpacing the S&P 500 (SP500) by a factor of almost 2x.

Strong Q3 Topline Supports Bull Thesis

Roblox delivered surprisingly strong Q3 results, beating analyst consensus on top line: During the period spanning June through the end of September, the gaming platform generated $713 million in sales, indicative of a 38% YoY growth compared to the same period one year earlier, and beating analysts' projections by close to $25 million according to estimates collected by Refinitiv. Roblox's strong growth was carried by all regions, with Europe (39%), APAC (52%) and RoW (49%) outpacing growth in NAM (34%).

Roblox Q3 2023

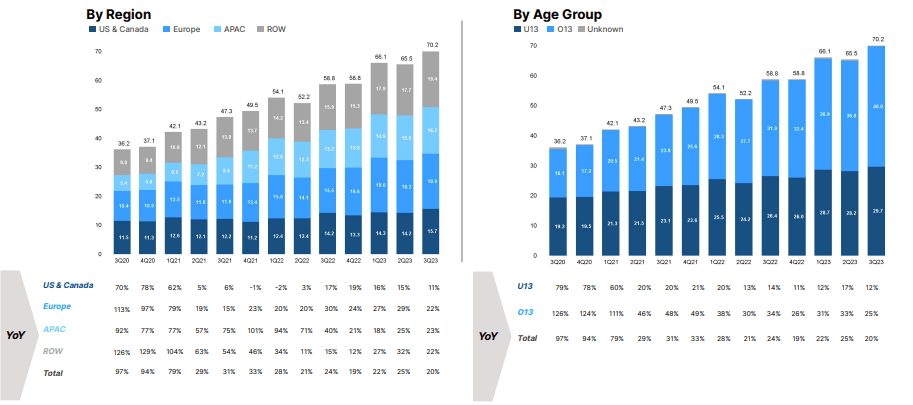

On revenue, investors should note that Roblox's growth is not (yet) a monetization story. In fact, the growth is supported by a DAU expansion in line with the company's mission to connect 1 billion people. As highlighted in the chart below, Roblox DAUs in the September quarter jumped to a record 70.2 million. In that context, performance in Roblox growth vectors, internationalization and aging-up, stands out:

Firstly, I point out that Roblox's DAU expansion was led by the over 13 years age group, with users aged 13-16 growing 22% YoY, 17-24 growing 27% YoY, and users 25+ growing 25% YoY. Secondly, on internationalization, there was a strong 66% YoY increase in Japanese DAUs. Bookings for the same region surged 174% YoY, respectively. This suggests that the Japanese market is displaying a similar viral pattern observed in other affluent international markets. In Germany, Roblox saw a 27% rise in DAUs, a 30% increase in hours, and a 75% boost in bookings YoY. Similarly, in India, Roblox experienced a 53% growth in DAUs, a 49% increase in hours, and a 76% surge in bookings YoY.

{kind=link}

Operating Leverage To Drive Up Profitability

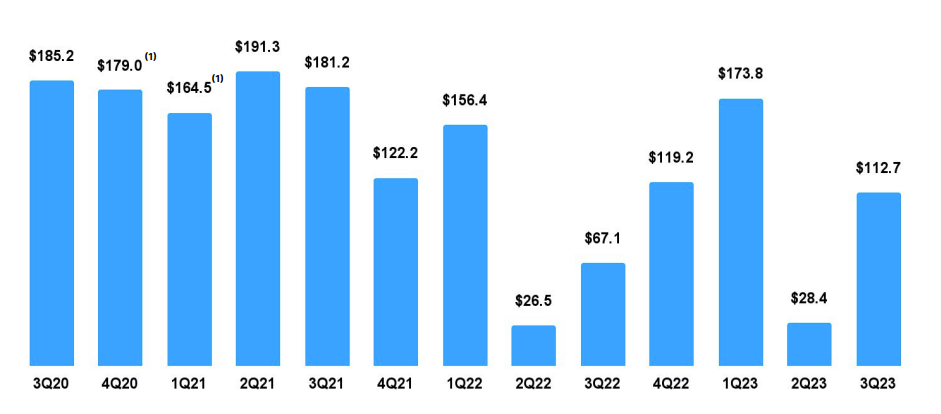

Arguably a major concern for Roblox investors relates to the company's presumably loss-making business operations. However, I point out that Roblox's income statement accounting reflects non-cash expenses, most notably share-based compensation and D&A. Focusing on the operating cash flow, Roblox is more than capable of supporting its operations without any debt/ equity financing. In fact, in Q3, Roblox posted the 13th quarter of consecutive net operating cash profitability, at $13 million.

{kind=link}

Despite the net cash profitability, Roblox is getting more serious about expanding profitability on both cost discipline and operating leverage. A first indication of this was already provided during Q3, with Roblox achieving an 18% YoY reduction in infrastructure costs per hour of engagement. The company also said that its data center capacity should be sufficient to meet Roblox's projected needs up to FY24. Moreover, during the call with analysts, management highlighted multiple avenues for future cost efficiency: headcount expenses will start growing slower than bookings already in Q1 FY 2024, and IT&S expenses per hour will keep decreasing. Looking ahead, I anticipate this emphasis on cost control also to extend to broader personnel efficiency. Surprisingly, R&D personnel expenses actually decreased this quarter compared to last quarter).

So Much Growth Ahead - Looking Forward To FY 2024

In 2024, continued penetration in internalization and aging-up will drive Roblox DAUs higher. But there is also the AI and advertising tailwind that makes me excited when thinking about Roblox.

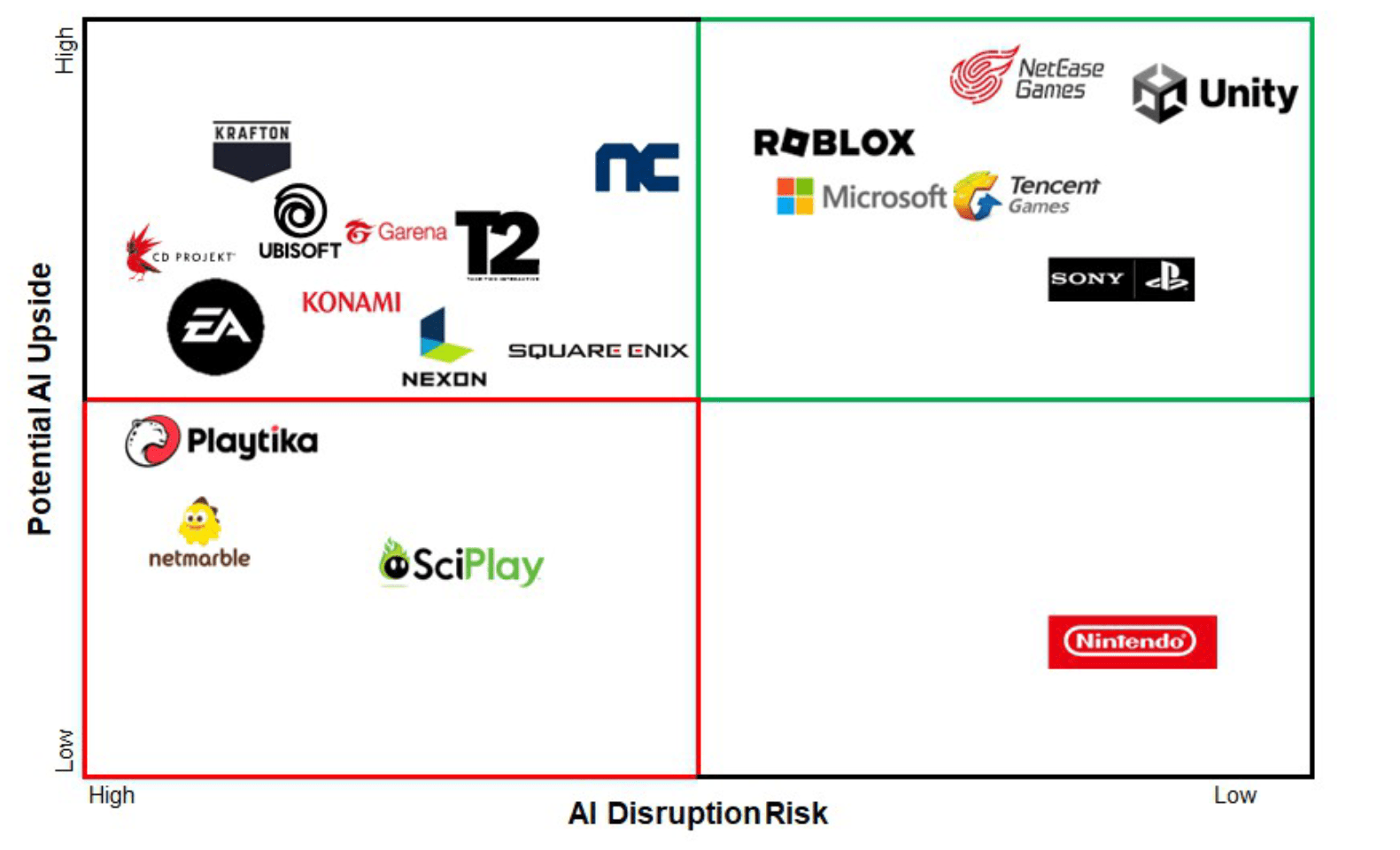

On gaming and AI, Morgan Stanley's equity research team has recently published a study on how AI will change the future of gaming (Research Note: How Will AI Change the Game Industry...and Who Could Benefit? Dated October 22). In that context, Morgan Stanley categorized Roblox AI exposure with low risk and high upside. Specifically, the report identifies several growth drivers: First, there are potential benefits of AI tools on cost savings and increased efficiency in game development, which could lead to higher earnings and advertising budgets for game publishers; Second, AI tools are poised to lower the barriers to entry in the gaming industry which could lead to a bigger gaming market on more published games; Third, AI will likely strengthen gaming engagement and payer conversion, which could drive in-game monetization.

Morgan Stanley Equity Research

{kind=link}

Relating to advertising, I see a huge potential for Roblox here, as I point out $30 million in advertising revenue for Roblox YTD, despite only sub-optimal/ emerging advertising roll-out. More broadly, investors should also consider that currently only 20% of the 70.2 million DAUs on the platform are paying users -- suggesting that a staggering 80% is not monetized. Initiatives planned for the first six months in 2024 include the launch of video ads, portals, and automated payouts; For the second half of 2024, Roblox is working on e-commerce initiatives. Roblox management sees about $1 billion of advertising revenue by 2027; and, I have no doubt that this target is achievable.

Lastly, Roblox is poised to see growth from the platform extension strategy. In Q3 Roblox launched its presence on Meta Quest, as well as the PlayStation. And in less than 3 months, Roblox has reportedly seen 2 million and 15 million installations/ downloads on Quest and PlayStation, respectively. Looking into 2024/ 2025, I personally believe that the Nintendo Switch could be next, supporting Roblox's ambition to make the gaming platform more ubiquitous.

Amazing Financial Guidance

Roblox has long refused to give forward-looking guidance to analysts. But in Q3 the company changed its stance with a bang. Not only did Roblox management say that the company feels very comfortable delivering on the analyst implied consensus for FY 2024 of bookings around $4.03 billion and adjusted EBITDA around $489.9 million, but management also guided for 2027 CAGR target on both top line and profitability. Specifically, during the most recent investor day , Roblox said to target a 20% compound annual growth rate in bookings for the period spanning 2025 to 2027. Using the '24 consensus of $4.03 billion as the benchmark, this projection implies a notable $8 billion in bookings for the year 2027! Notably, if achieved, this would suggest a 30-35% surge beyond current FY 2027 analyst expectations of around $6 billion, according to data collected by Refinitv.

On profitability, Roblox targets an anticipated annual enhancement of EBITDA margin by 100 to 300 basis points over the subsequent 3 to 5 years. As discussed above, this projected operating leverage predominantly hinges on controlling fixed costs, notably through headcount management, and a progressive decline in Infrastructure & Safety expenses relative to the increasing bookings over time.

Furthermore, the potential for substantial growth in Daily Active Users (DAUs) on the PlayStation platform emerges as a significant source of upside in the upcoming year, representing a promising avenue for expanded market traction.

Investor Takeaway

Roblox is full of growth, innovation, and opportunity: The company's ambitions to internationalize and age-up are seeing good success, while platform expansion should render the Roblox platform more accessible and ubiquitous. Additionally, 2024 will likely establish the groundwork for a highly lucrative advertising business, while the integration of generative AI will support the platform experience of both creators and users. In numbers, Roblox recently announced financial objectives aimed at a 20% or compounded annual growth rate in bookings from 2025 to 2027, alongside an annual 100 to 300 basis points increase in EBITDA margin over the next 3 to 5 years. If Roblox indeed achieves a 20% annual top-line growth and an annual 200 basis point expansion (mid-point) through 2027, the platform would generate an EBITDA of about $1.3 billion. As I project an implied exit EV/EBITDA multiple of around 30x for 2027, anchored on secular growth potential, I estimate Roblox's intrinsic worth at about $70-75/ share. Buy.

For further details see:

Roblox: 'Magnificent' Potential