RBLX - Roblox: Re-Iterate Our Sell Rating

2023-10-19 18:10:03 ET

Summary

- In December last year, we concluded that the price valuation of Roblox was too high, and it is on a path of normalization post-pandemic.

- The user spending pattern revealed by its deferred revenue to bookings ratio has shown large change is happening.

- Yet the compensation and personnel expenses have only increased instead, with its payout to the in-platform game developers taking a hit.

- This path is unsustainable and there will be a reckoning for the company one way or another.

Investment Thesis

Review

In December last year, we initiated our coverage of Roblox (RBLX) explaining our view that the price valuation at the time was too high. The price at the time was $27.6, since then it has gone up to $46 and now fallen back down to $30. The analysis was based on the relations of its revenue, deferred revenue, and bookings, which revealed that the average life of the paying users has an impact on its future revenue slowdown.

Analysis Update

Roblox views its platform as an economy. As we explained in our previous article, ROBUX is the currency that floats the gaming activities developed by independent developers on the platform. According to Roblox's latest corporate update , for every dollar spent on its platform, 76 cents an average of 76% of all spending in experiences supports or goes to developers, among which 29 cents are paid directly to the developers.

rblx (rblx)

The efforts Roblox made to expand its revenue stream this year is to scale into the advertisement business through an immersive experience and its brand power among teens and young adults as the main audience. But as explained in its 10Q of last quarter ,

"Substantially all of our bookings are generated from sales of virtual currency, which can be converted to virtual items on the Roblox Platform. ... Bookings also include an insignificant amount from advertising and licensing arrangements."

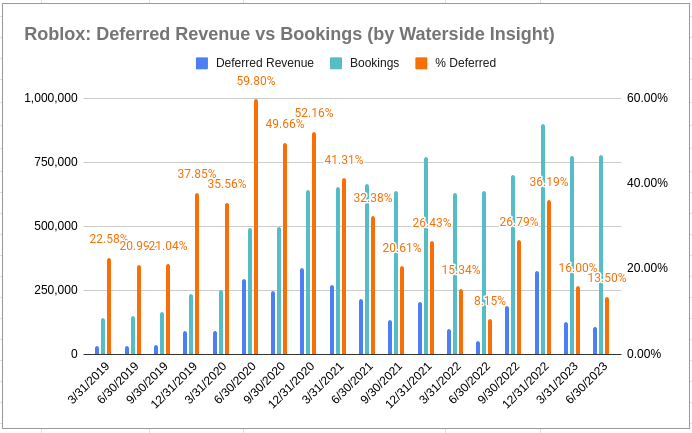

Since its revenue is from the bookings, and the bookings are "substantially from the sales of virtual currency", which was sold to the customers to buy the experience and virtual goods on the platform, which was created by the developers, then it is safe to say the revenue was mostly earned by the games the developers developed. Only when the bookings were spent then they are realized as revenue for that quarter. In the Q2 presentation , Roblox indicated the average lifetime of a paying user was still 28 months. The deferred revenue had a strong spike in Q4 last year, rising slightly above the previous high in Q4 2020. But this was the result of almost 50% higher bookings yet only 36.19% deferred in Q4 last year compared to 52.16% in Q4 2020. It means users tended to defer less of their purchased ROBUX and chose to spend them more upfront. But with the same length of lifetime, it could mean there is less interest to spend in the following 20-something months after the initial spike. The percentage of bookings that were deferred was the lowest in Q2 last year at 8.15%, but in the past two quarters, it was in the mid to low teens, which was also on the low side compared with during the pandemic boom time. As we explained in our previous article about the relationship between bookings and deferred revenue, the tailwind of higher deferred revenue helped the revenue in the next 27 months after the user's initial purchase. When anticipating the company's future revenue from here, if this trend continues, it will matter more how many bookings it attracts during that quarter than the pull from previously deferred revenue. Indeed, it seems the company has recognized this urgency and has started to look for a broadening user base. It first announced that more than 55% of its users are above 13 years old in May, and then in June announced a specific experience targeting users of 17 and older. In its own words, Roblox wanted to " grow up ". Such an age group has higher spending power but also has more active daily activities and engagements outside of playing games. It remains to be seen how Roblox can retain their attention in a lasting manner.

Roblox: Deferred Revenue vs Bookings (Calculated and charted by Waterside Insight with data from company)

{kind=link}

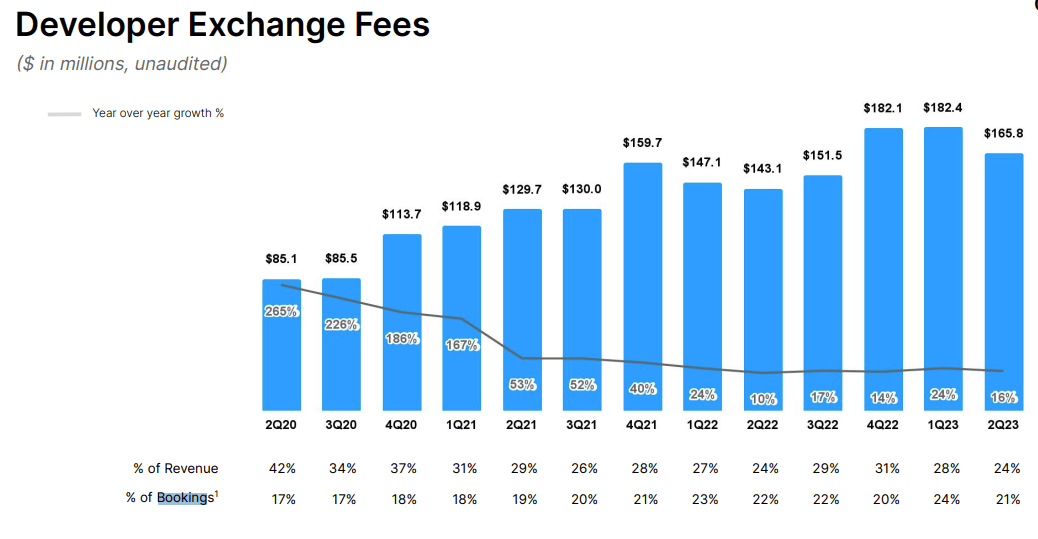

Last time we had to compile its developer exchange fees on our own, but since then, Roblox's quarterly presentation has included this figure. Since Q3 2022 when we last updated, these fees have increased to as high as $182 million and landed at $165.8 million last quarter. Although there is still 16% YoY growth, it grew 9.1% less QoQ. As a percentage of revenue, this payout to the developers on its platform was the lowest at 24%. It means it pays about 24 cents on every dollar it receives by the end of Q2. As we alluded to earlier, the entire monetary realization of Roblox's economy depends on the developers to build games and attract users. A lower payout could help to boost its top line temporarily but risk alienating its developers in the longer term.

Roblox: Developer Exchange Fees (Company 2023 Q2 Presentation)

{kind=link}

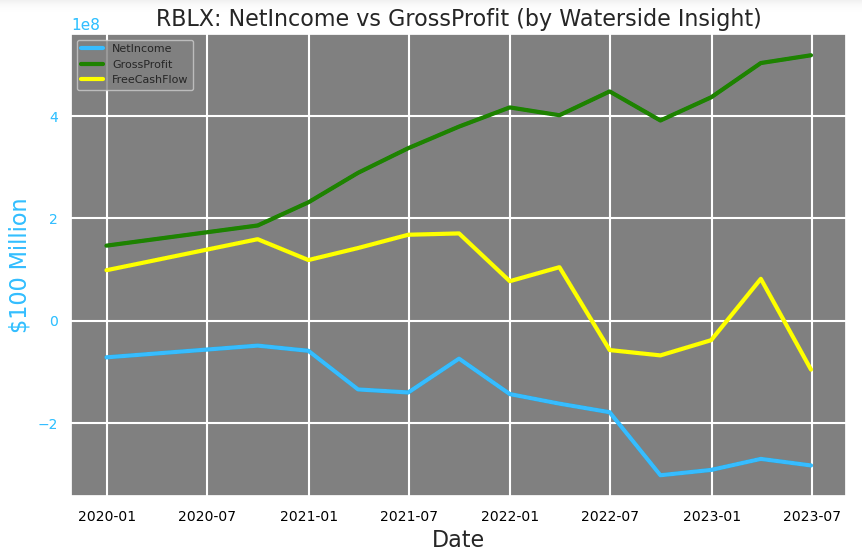

Looking at its financials, such strong bookings don't seem to have boosted its bottom line and cash flow. There is a divergence of gross profits versus its net income and free cash flow

Roblox: Net Income vs Gross Profits (Calculated and charted by Waterside Insight with data from company)

{kind=link}

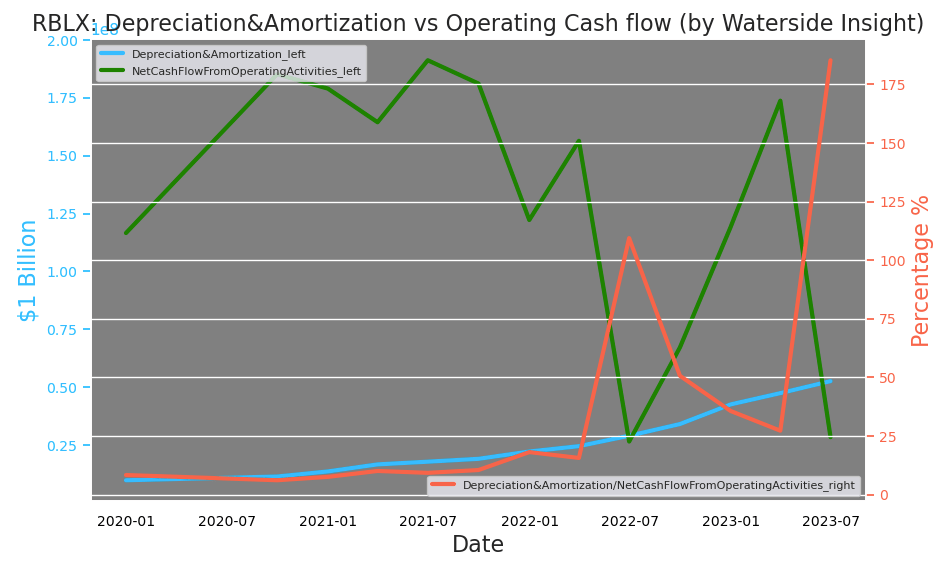

Such a low free cash flow is on the basis of higher depreciation and amortization (D&A) provided for the operating cash flow.

Roblox: Depreciation & Amortization vs Operating Cash Flow (Calculated and charted by Waterside Insight with data from company)

{kind=link}

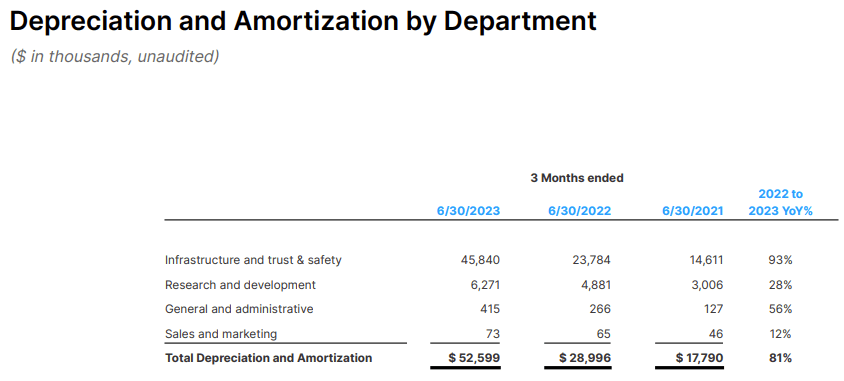

The company indicated most of the D&A came from its "Infrastructure and trust & safety" department, which has produced 93% more than a year ago.

{kind=link}

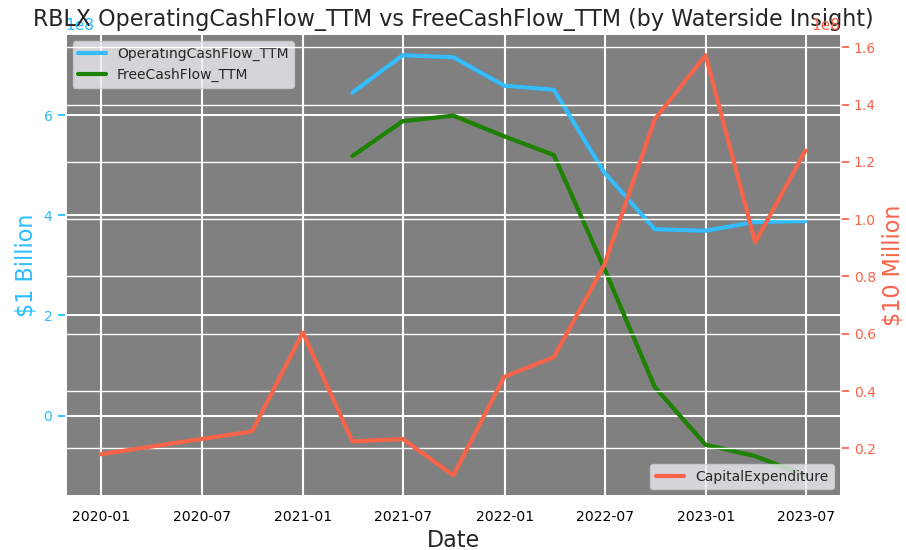

Yet its free cash flow was still pushing deeper into the negative compared to a year ago. It seems the higher CapEx, which is still almost double compared to a year ago, has exerted quite a lot of downward pressure on its FCF. Along with higher cost of revenue and higher operating expenses.

Roblox:TTM Operating Cash Flow vs Free Cash Flow (Calculated and charted by Waterside Insight with data from company)

{kind=link}

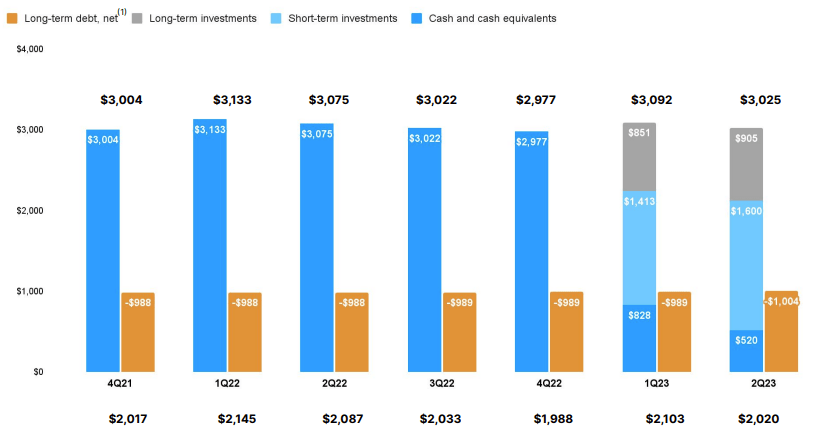

Reviewing its cash and cash equivalent, it shows that Roblox has converted a large part of it into investments, long-term and short-term since Q1 this year. Its cash and cash equivalents were $2.98 billion in Q4 2022, and now it is only $520 million, while its long-term investment is $905 million and short-term investment was $1.6 billion, totally to be about $3 billion, in the ballpark of its previous cash pile in sum.

Roblox: Cash and Cash Equivalent, Investments (Company 2023 Q2 Presentation)

{kind=link}

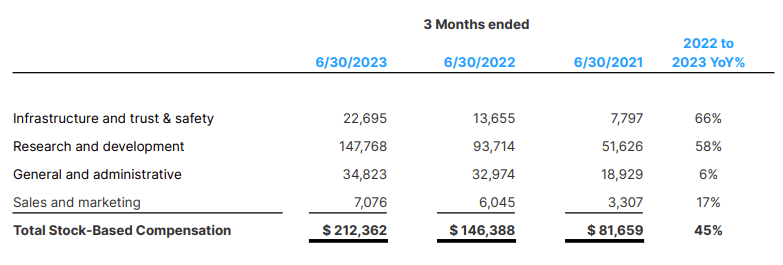

These investments are mostly in fixed-income securities, including money market funds and other debt securities. So far, the investment has gained $103,000 and lost about $15 million through June 30 this year. However, its short-term investment, reaching $1.6 billion in Q2, also contains a portion that is held in mutual-fund investments. These mutual fund investments are in a structure called ' rabbi trust ". Such a trust is to "support the non-qualified benefit obligations of employers to their employees". Simply put, to make more payments to their employees. In comparison, its employee-based compensation has been growing steadily upward in contrast to its EBITDA declining further to negative. It was losing $223.79 million in earnings in the last quarter while paying $212.36 million in compensation, another divergence we are seeing here.

The breakdown of the comps shows the majority of it was paying the research and development personnel, which we already knew from the last analysis.

Roblox: Stock-Based Compensation (Company 2023 Q2 Presentation)

{kind=link}

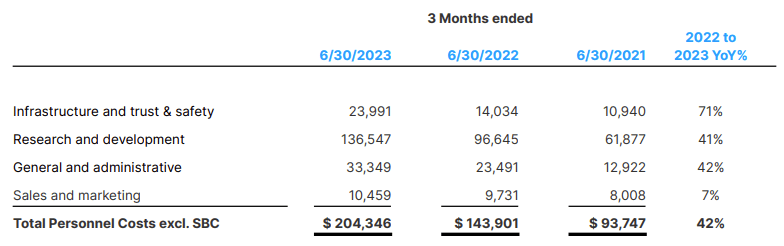

Its personnel costs excluding stock-based compensation are as follows:

Roblox: Personnel Costs excl. SBC (Company 2023 Q2 Presentation)

{kind=link}

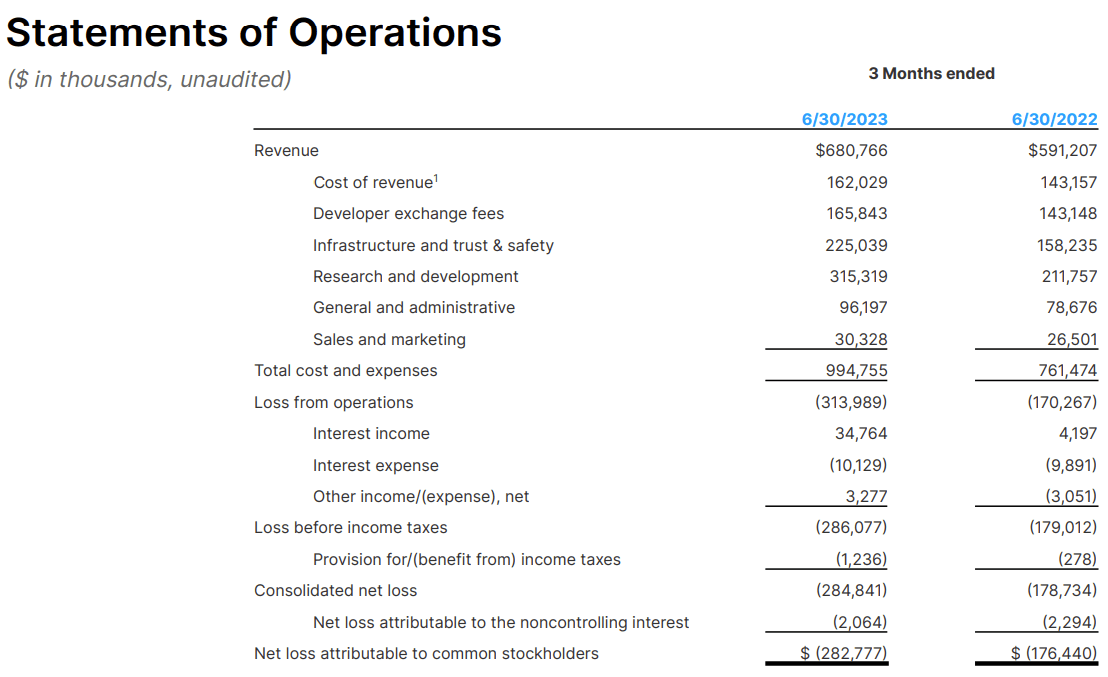

So adding these two items, the payout to its research and development department is $284.315 million. However, the Statements of Operations for Q2 stated the expenses were actually $315.319 million.

Roblox: Q2 Statements of Operations (Company 2023 Q2 Presentation)

{kind=link}

Perhaps it was added with the payout from the "rabbi trust" account. But now it seems there are three layers of compensation to its personnel, and the majority of the beneficiary is in R&D. And this total amount accounts for 46.32%, up from 25.82% a year ago. It is now paying its own in-house researchers and developers about 46 cents on every dollar it realized as revenue. Compared with its lower payout ratio to the in-platform developers, perhaps we can see who the company is betting on to improve the company's profitability. Its researchers recently developed new generative AI tools called "ControlNet" and "StarCoder" for game developers to use. They marked substantial advancements for the platform in AI during the recent boom ignited by ChatGPT. However, in order to attract 17-24-year-old age group users, the games are most likely being developed by this age group instead of the younger under-13 group. The earnings expectation for them will be relatively higher, we speculate. And as we alluded to earlier more revenue is being realized upfront, so this gives the context that the payout ratio to the developers in Q2 was even lower than the 24 cents on a dollar indicated. It seems the company is stretching it thin in order to compensate for the operation loss. We don't think this can last and the payout for its in-house R&D will have to come down.

Financial Overview & Valuation

Roblox: Financial Overview (Calculated and charted by Waterside Insight with data from company)

{kind=link}

We previously concluded that Roblox was coming out of the pandemic boom and looking to normalize its growth trajectory. And what we see after 10 months, it has indeed been on that path. It has been exploring to appeal to a broader user base while the spending patterns of its users have changed. It still emphasizes greatly on R&D but is perhaps pushing close to the edge of where it can actually afford. We reiterate our previous valuation that its fair value currently should be around $7 per our bullish case. We still deem the current price to be too high.

Conclusion

Roblox remains an interesting social and technological experiment in the immersive metaverse. However, while it has been trying to adapt to the post-pandemic world of growth, its spending on compensation, especially for R&D, has become a huge burden for the company to be profitable in the near term. It is still a sell at the current price, which is not far from where it was ten months ago.

For further details see:

Roblox: Re-Iterate Our Sell Rating