DIS - Roku: Time To Downgrade As Competitive Risks Coincide With Rising Stock Price

2023-12-14 07:27:41 ET

Summary

- Roku stock has been a strong performer since the 2022 tech crash.

- The company has seen accelerated revenue growth, finally returning to positive adjusted EBITDA generation.

- Consensus estimates of 13% to 15% revenue growth for Roku look aggressive.

- The smart TV market leader has the most to lose amidst the streaming wars.

While it can be tempting to just stare in amazement as the market soars, value-focused investors are undoubtedly wondering if this latest rally is a little too much, a little too fast. I now carry that view for the stock of Roku (ROKU), which has been a strong performer over the past year. ROKU has seen two consecutive quarters of sequential revenue growth, culminating in the company's first quarter with positive adjusted EBITDA since the first quarter of 2022. The company maintains a net cash balance sheet and is generating significant interest income from the cash balance. Even with the macro environment having the potential to improve on account of projected interest rate cuts, the stock valuation does not look compelling relative to the moderated top-line growth rate. The smart TV landscape is seeing increased competition and the streaming environment is also as competitive as ever. I am now downgrading ROKU stock from "buy" to "hold."

ROKU Stock Price

After peaking well over $450 per share during the pandemic, ROKU stock found a bottom around $40 per share at the end of 2022, and has more than doubled since then.

I last covered ROKU in June where I rated the stock a buy on account of the strong quarterly results. While the company has continued to deliver on strong top-line growth, management commentary suggests that growth rates moving forward may be more moderated.

ROKU Stock Key Metrics

In the latest quarter, ROKU continued to see solid sequential growth in active accounts and streaming hours. Average revenue per user ('ARPU') declined YoY but that has been a typical trend among any advertising name not named Meta Platforms (META).

2023 Q3 Shareholder Letter

That in turn led revenues to grow by 20% YoY. Gross profits grew by only 3% YoY, but excluding restructuring and impairment charges (related to the removal of licensed content from The Roku Channel), gross profit would have grown 22%. It is notable that ROKU was able to generate its first quarter with positive adjusted EBITDA since early 2022.

2023 Q3 Shareholder Letter

Management has committed to generating positive adjusted EBITDA for the full 2024 year "with continued improvements after that." ROKU ended the quarter with $2 billion of cash versus no debt, though this figure might be slightly inflated due to accounts payables having risen from $165 million at the end of 2022 to $312.3 million. I note that adjusted EBITDA does not include interest income - like many tech names with rich cash balance sheets, ROKU has seen some surprise benefit from the higher interest rate environment.

Looking ahead, management has guided for 10% YoY revenue growth to $955 million and $10 million in adjusted EBITDA. On the conference call , management tried to frame the competitive environment quite optimistically, stating that as more and more streaming services add advertisements, it "levels the playing field in viewers' minds with services like The Roku Channel, which are already ad-supported." I am not personally of the view that consumers are likely to make such a jump, and I highlight the possibility that more ad-supported streaming services might reduce the pricing power from ROKU. Management appeared to suggest that 2024 might see similar revenue growth as the fourth quarter, stating that investors should "anticipate low-single-digit growth rates from a run rate basis off that."

Is ROKU Stock A Buy, Sell, or Hold?

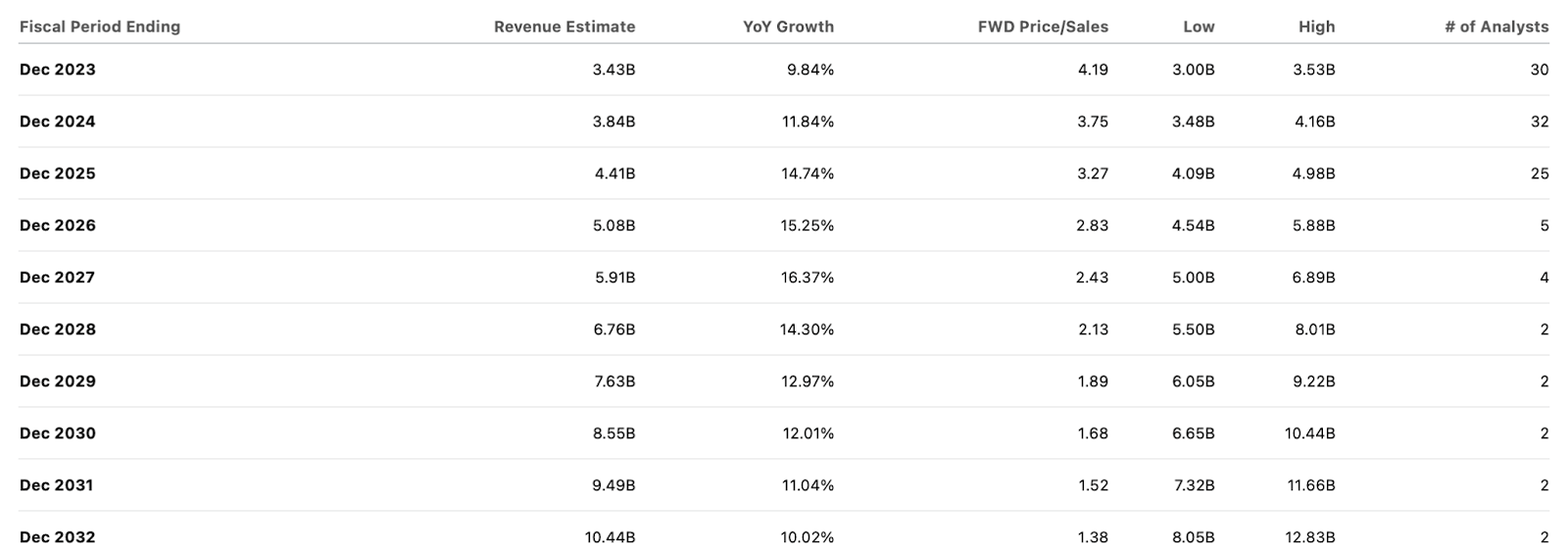

That forecast appears to differ from consensus estimates, which essentially call for healthy double-digit growth over the next decade.

{kind=link}

ROKU is expected to realize substantial operating leverage, with analysts projecting a 12.9% net margin by 2032.

{kind=link}

Based on the 42% gross margin rate, that implies a 30.7% net margin based on gross profits. I had previously modeled fair value using 13% projected growth, 50% net margins based on gross profits, and 1.5x price to earnings growth ratio ('PEG ratio'), leading to a valuation of 10x gross profits or around 4x sales. After ROKU's run-up, the stock is now priced right around that level, meaning that forward returns might come in-line with top-line growth. If ROKU had GAAP profitability and a more dominant market positioning, then I might have been content with this kind of return proposition. But ROKU has barely started generating positive adjusted EBITDA, and I have concerns regarding the competitive environment. ROKU has long been the market leader in smart TVs, but I expect competitors like Google (GOOGL) to commoditize the market. ROKU might have some first mover advantage, but its large market share does not give it "network effects" to help it earn new business. If anything, ROKU looks particularly exposed with the most to lose in the smart TV space. Granted, ROKU might continue to post solid growth due to smart TVs taking share from the TV space overall, but my point is that consensus estimates of 13% to 15% revenue growth over the coming years look full, if not aggressive. Meanwhile, ROKU appears to be counting on increased investment in their original content to help differentiate them from competitors, but such an endeavor looks ill-advised as I am doubtful that the future streaming environment can allow for more winners beyond the Netflix's (NFLX) or Disney's (DIS) of the world. ROKU is the kind of higher risk stock that I would prefer to have a comfortable margin of safety, with significant multiple expansion potential. At current prices, I do not see a legitimate case for multiple expansion barring increased investor optimism or a huge acceleration in underlying growth rates. I am downgrading the stock from buy to hold.

For further details see:

Roku: Time To Downgrade As Competitive Risks Coincide With Rising Stock Price