RLLCF - Rolls-Royce: Improvements Are Already Priced In

2023-07-07 16:00:00 ET

Summary

- Rolls-Royce is a leading engineering business that has struggled in the last decade. We believe fortunes are improving, with scope for consistent growth.

- Improvements in the commercial airline industry will contribute to increased demand and margin improvement.

- Its Defense and Power Systems business units are facing tailwinds that should drive revenue growth, supporting a consistent upward trajectory.

- Rolls-Royce's investment in Sustainable industries has scope to generate substantial gains as it invests in the future energy capabilities.

Investment thesis

Our current investment thesis is:

- RR has had a difficult decade but its fortunes are changing. The company has deleveraged and demand looks to be returning to the commercial travel industry, driving growth and margin improvement.

- Defense and Power Systems continue to perform well, with tailwinds in both industries expected to improve growth.

- RR shows its potential when compared to peers, as its profitability is comparable but the company lacks growth, which is the characteristic that looks to be returning.

- RR's valuation implies no upside, as the execution risk for improvement is priced in.

Company description

Rolls-Royce Holdings plc ( RYCEF ) is an industrial technology company that operates both in the United Kingdom and globally.

The company is divided into four segments:

- Civil Aerospace - manufacturing and sale of aero engines for various aircraft markets.

- Defense - manufacturing and sale of military aero engines, naval engines, and submarine nuclear power plants.

- Power Systems - manufacturing and sale of integrated solutions for onsite power and propulsion.

- New Markets - manufacturing and sale of small modular reactors and new electrical power solutions.

Share price

RR has had a disastrous decade, losing almost 90% of its value during this time. This has been driven by a range of factors, primarily financial weakness and the inability to achieve a consistent and positive trajectory, resulting in uncertainty.

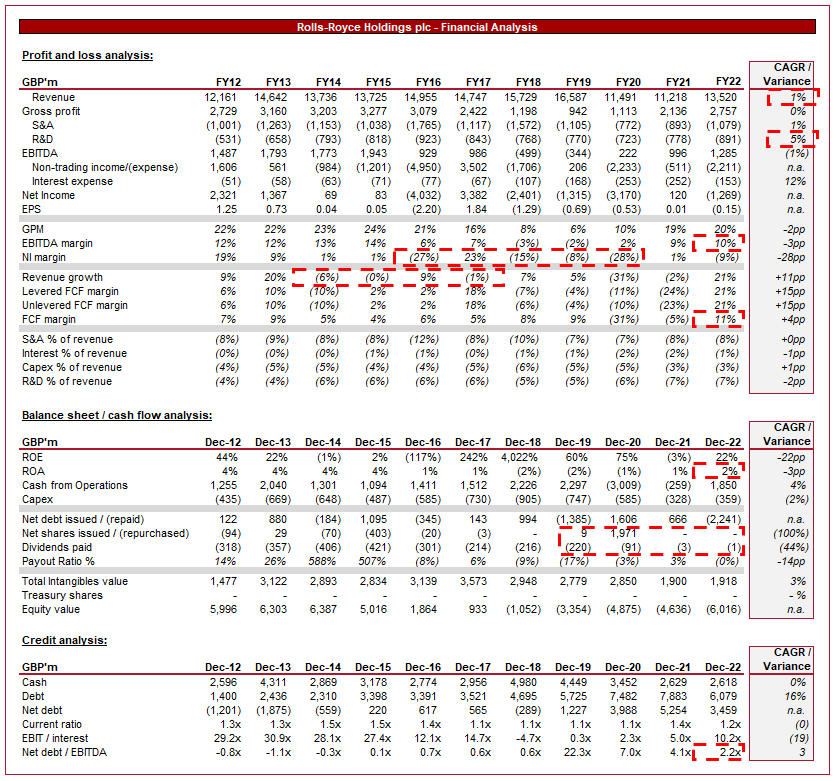

Financial analysis

Rolls-Royce Financials (Capital IQ)

{kind=link}

Presented above is RR's financial performance for the last decade.

Revenue & Commercial Factors

RR's revenue has grown at a CAGR of 1% but this does not illustrate the journey the business has been on. Revenue growth has been highly volatile, with acquisitions and divestitures materially contributing to this.

Business model and market position

RR is fundamentally a design and engineering business. Given the various segments within the business, there is no single "business model". The company's approach is to invest heavily in research and development to create new and innovative solutions within its core markets, as well as improve the productive value of its current product suite.

RR's revenue is currently materially apportioned between the following three segments, with Civil Aerospace being the largest business. This diversification between business units provides the company with reduced downside risk, as it is not heavily reliant on any one segment. This is critical given the size of its contractual arrangements.

Most recently, the Covid-19 pandemic was a disaster for the business as the aviation industry ground to a halt. Although this significantly damaged the business, Power Systems and Defense were resilient.

Underlying revenue by business (Rolls-Royce)

Civil Aerospace:

Civil Aerospace (Rolls-Royce)

The Civil Aerospace business unit continues its post-Covid recovery, with 25% organic growth in FY22. Further, the margin improvement has been significant, with GPM up 4.3%, driving a return to operating profitability.

We believe further improvement is possible, as its investment in R&D over the last few years should drive improved economics.

{kind=link}

We expect an upward trajectory in the industry, as the demand for travel continues to increase following the end of the pandemic, especially now that China looks to be past its issues. This will signal to airliners that investment in their fleet can return.

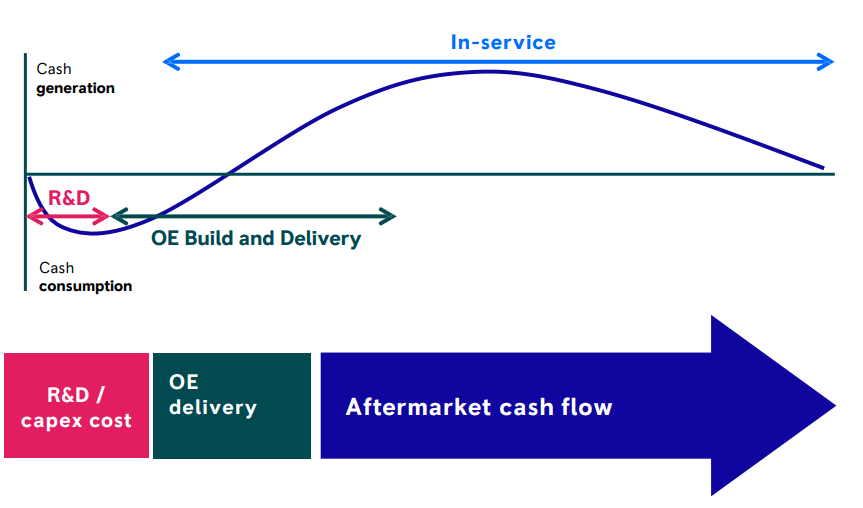

Further, the industry is approaching a lucrative phase for RR, where Management expects cash flows to improve as large upfront build costs decline in favor of servicing and support.

Investment cycle (Rolls-Royce)

{kind=link}

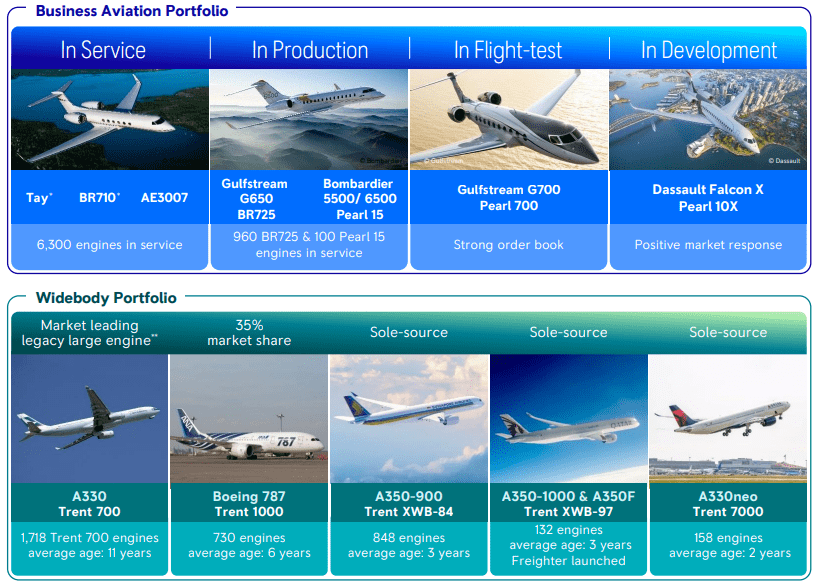

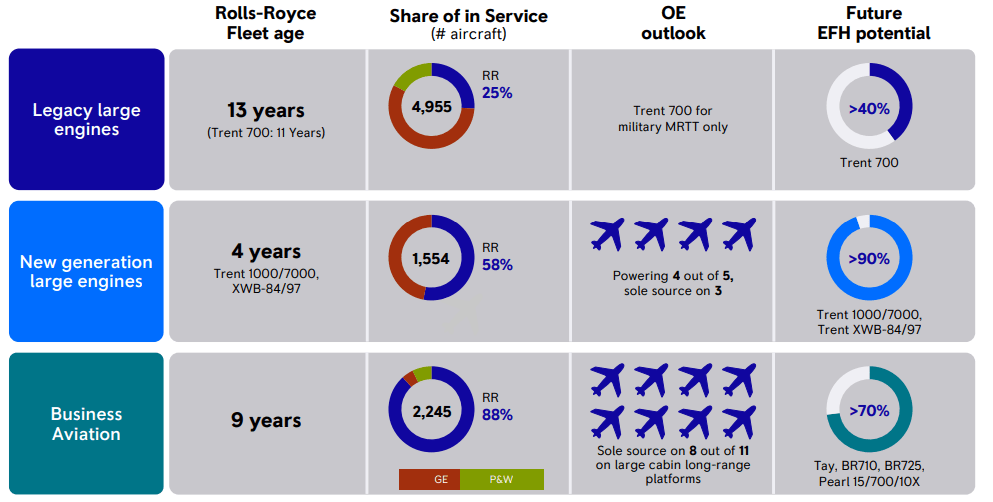

The average age of RR's fleet is >9 years for its legacy engines and business aviation, markets within which RR has a strong position.

Fleet age (Rolls-Royce) Market leading integration (Rolls-Royce)

{kind=link}

Defense:

Defense (Rolls-Royce)

RR is a market leader in the aero engines space, as well as supporting the Royal Navy with its Nuclear Submarines. 50% of Defense's revenue is generated from the US DoD, with a further 25% from the UK MoD.

This revenue stream is resilient, with 2% growth in the most recent period. We are expecting continued growth in the coming years, as Defense has agreed to a new program with the US DoD and the UK continues to invest in its fighting capabilities through GCAP (a partnership to develop stealth fighters between the UK's, Japan's, and Italy's Air Force), as well as its own next-generation fighter program.

Current geopolitical tensions globally represent an opportunity for RR's defense business unit, as global superpowers continue to invest in defense capabilities. The UK Government remains committed to defense, with an announcement that it would increase spending by c.£5bn , targeting 2.5% of GDP.

Finally, the Export Market remains strong due to legacy products, with involvement in Australia's nuclear submarine program ( Supported by the UK and US ) representing a potential upside if RR can win participation. This is a reasonable expectation given its involvement thus far in the UK program.

Power Systems:

Power Systems (Rolls-Royce)

Rolls-Royce designs and manufactures power systems for a range of applications, including commercial and military aircraft, marine vessels, and industrial power generation.

This segment represents a key area of development for the business, as impressive R&D investment has contributed to a market-leading proposition. In 2022, RR achieved a record order book, with 40k+ customers and 23% YoY revenue growth.

This segment looks to be on an upward trajectory, as economic recovery post-Covid contributes to increased infrastructure spending, such as on data centers. Further, the development of low-carbon solutions has the potential to rapidly accelerate growth as the push for sustainability encourages infrastructure development. RR believes it could be a global leader in this market in the coming decade, given its superior market position and the developments made thus far.

New Markets:

New Markets (Rolls-Royce)

New Markets represents early-stage businesses and innovative developments outside of its core businesses. It leverages RR's deep expertise to develop sustainable products, focused on the transition to net zero. With Governments around the world committed to the transition, RR is looking to position itself as a key supplier.

This segment is currently focused on two areas in particular, all-electric/hybrid propulsion systems, as well as Small Modular Reactors (SMRs).

The SMR segment has the potential to be highly lucrative, as the UK seeks to diversify its energy generation, with a commitment to approve 9 SMRs by 2030 . The current expectation is for official approval to be provided in 2024 to RR, having passed the first stage . The SMR funding is primarily from the UK Government and external investors, reducing the cash commitment to RR.

R&D investment (Rolls-Royce)

The aviation industry is witnessing a growing interest in electric propulsion systems. This trend is driven by the need to reduce carbon emissions, improve fuel efficiency, and address noise pollution concerns. RR's innovation looks to bearing fruit, having broken the electric speed record in 2022 . The belief is that this will have applications in both the civil aerospace and defense industries.

Margins

RR's margins have fluctuated wildly in recent years, seemingly normalizing below its FY12-FY15 levels. This is due to the Civil Aerospace business unit, which is materially less profitable than Defense and Power Systems. As Civil Aerospace growth improves, it will pressure margins, even if the other business units grow well, also.

Balance sheet

RR has deleveraged in recent years, following the disposal of non-core assets and the utilization of cash. This puts the company in a relatively strong position from which to invest in R&D and growth.

Despite the poor profitability, RR has generated consistent cash flows, allowing the business to accumulate a strong cash position.

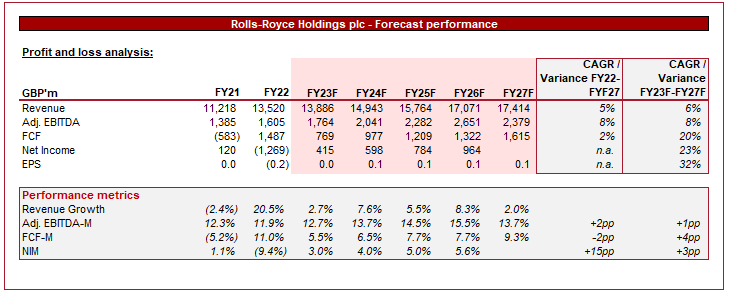

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting an improvement in revenue growth, alongside an improvement in margins. Both assumptions look reasonable based on our assessment, as improving fortunes and innovative opportunities enhance returns.

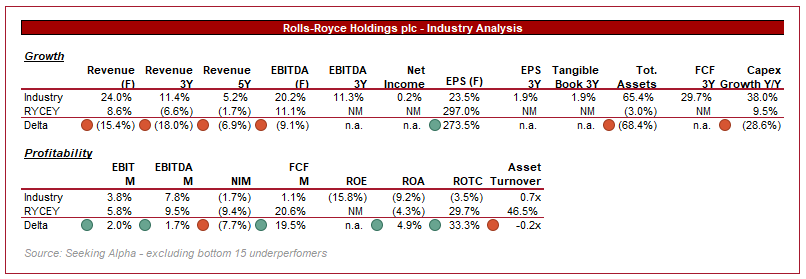

Industry analysis

Aerospace & defense industry (Seeking Alpha)

{kind=link}

Presented above is a comparison of RR to a cohort of Aerospace & defense businesses.

RR's key area of weakness is growth, with its peers generating impressive returns over a 3-5Y period, compared to a decline with RR. This is a reflection of the company's weighting toward Civil Aerospace relative to defense, which has grown at a better rate than the market average.

Despite the margin weakness, RR is in a comparable position to the market, implying improvement could take the business into an attractive position.

Based on this analysis, RR looks well-placed. The company is far from perfect but is on a trajectory to be above average.

Valuation

Valuation (Capital IQ)

RR is trading at 12.5x LTM EBITDA and 9x NTM EBITDA, which represents a premium to its historical average.

The last decade has been difficult. FY12 to FY14 was strong, whereas FY15-FY22 was poor. For this reason, we would suspect a premium only if the company's fortunes had materially improved. This does not look to be the case.

RR has significantly improved and is on an upward trajectory, however, the company has yet to wholly its fortunes. Operational improvement is still required, as is time. At its current share price, execution risk is essentially unpriced, assuming a perfect transition.

Final thoughts

RR is an innovative powerhouse, reflected by the number of times we have mentioned RR's leading position in a particular market. With its deep expertise and penetration into various industries, we expect a healthy growth trajectory on fundamentals alone. Innovation and tailwinds look to be enhancing this. Finally, margin improvement looks likely as the Civil Aerospace division returns to a normalized level.

RR's improvement is already priced in, with the stock trading at a premium to its historical level

For further details see:

Rolls-Royce: Improvements Are Already Priced In