ROOT - Root Inc. Is At A Crossroads

2023-09-21 08:21:47 ET

Summary

- Root is an innovative insurance company that operates as a direct-to-consumer provider using mobile technology.

- The company has the potential to disrupt the industry and become a major player, but it has never turned a profit and faces industry headwinds.

- Valuation signals are mixed, with insiders believing the stock is undervalued, but Wall Street analysts and short interest suggesting overvaluation.

Root, Inc. ( ROOT ), based in the United States, is a leading innovator in the insurance industry. The company offers a range of insurance products and services, including automobile, homeowners, and renters insurance. Root, Inc.'s unique business model sets it apart - it operates as a direct-to-consumer personal automobile insurance provider, leveraging mobile technology to acquire customers.

Root is a complicated stock, up over 17% from the last year but still hundreds below its IPO price. Root has the potential to leverage its proprietary model and lower fixed-cost structure to disrupt the industry and become a major player. However, they have never turned a profit and are facing the worst auto insurance environment in 30 years.

With valuation signals pointing up and down and the potential for significant gains or significant losses, I rate Root a hold and will keep a close eye on next quarter for the risk/reward balance to swing one way or another.

Upside Potential From Disruption

Root has looked to disrupt the insurance industry in two ways. First, by leveraging a propriety segmentation model that improves pricing accuracy, and second by operating digitally and director to consumer to reduce overhead.

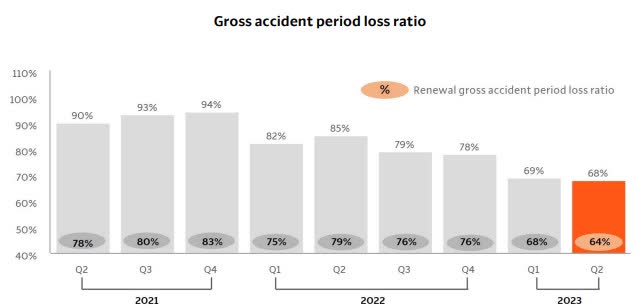

Over the last few quarters, the proprietary pricing model has started to yield results. In Q2 2023 , Root posted its lowest loss ratio ever. Most of this benefit was on the pricing side, with the remainder on the claims side.

{kind=link}

At a 68% loss ratio, Root beat the industry average of 76% by a wide margin. Despite lower policies and revenue, the loss ratio improvement led Root to post its strongest EBITDA and Net Loss performance.

Historical Profitability (ROOT Investor Relations)

In just two years, Root has gone from lagging the industry by 20 percentage points in losses to beating it by 8 percentage points. This is even more impressive as other carriers lost an average of $0.12 on the dollar for every premium written . Management noted in the earnings call that this model is not yet rolled out across all markets, so there may be additional upside in future periods.

Root's low overhead and digital model also yield benefits as the industry struggles. Year-over-year, Root decreased SG&A expenses by more than 50% in Q2 and expects the savings to continue. This gives greater flexibility to ride market waves moving forward.

It has also allowed unique distribution methods like selling through Carvana - a major driver in reduced marketing expenses.

Continuous improvement on the segmentation model and maintaining low overhead sets Root up to be nimble and flexible in the years to come, potentially driving value to shareholders.

Downside Risk From Industry Headwinds

Offsetting the potential upside from disruption are industry headwinds that Root may not be able to overcome.

The auto insurance industry is being squeezed by more frequent claims and higher losses as COVID trends come to an end, and inflation drives new auto and repair prices higher. Of note, Root saw an 8% increase in claim severity but was saved by a 6% decrease in frequency.

Auto Insurance Headwinds (Beinsure)

To offset this, carriers are pushing for rate increases as high as 40%. This makes Root's rate increase of 26% from $1,077 to $1,353 paltry by comparison. In addition, regulators are starting to push back on rate increases, which could limit their ability to offset higher claims.

While the balance sheet is strong today, Root has never been profitable and is highly exposed to a swing in claims, given its ongoing losses. Despite its best quarter ever, the net loss ratio is still 93%. Management also noted in earnings that they don't believe current growth can be extrapolated forward, and they believe customer acquisition costs will double in the back half of the year. This does not bode well for turning profitable in the near term.

Mixed Signals On Valuation

On the bull side, insiders believe that Root is significantly undervalued. Not only have insiders increased their position by 355,677 shares in the last three months, but they turned down a June offer to sell for $19.34.

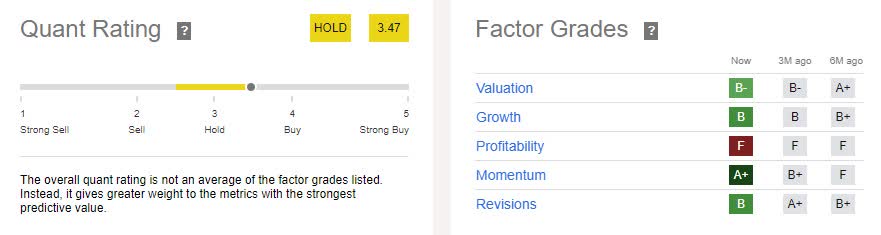

On the neutral side, the Quant rating is a hold, weighed down heavily by the lack of profitability.

{kind=link}

On the bear side, short interest is currently at 14.5%, suggesting the stock is overvalued. Wall Street agrees, with analysts' average price target of $9.61 down more than 12% from the current trading price.

{kind=link}

My thesis is neutral, especially given the mixed valuation signals. It is worth half the price if the company fails to turn profitable. If the company succeeds in disruption, it is worth double the current price or more. However, I believe risk and reward offset each other until we get more data.

Verdict

Root can potentially disrupt the insurance industry and drive higher yields than its competitors. This was shown in Q1 and Q2 results. However, Root's profitability is a significant area of concern, as the net loss ratio remains high at 93% even after its most profitable quarter. Management anticipates customer acquisition costs will surge, potentially doubling in the next half of the year, and profitability is not immediately in sight.

Valuation signals are also mixed. Company insiders have displayed confidence by increasing their holdings, which hints at potential undervaluation. The Quant rating advises holding the stock, mostly due to the current absence of profitability. There is also a considerable bearish sentiment, evidenced by the 14.5% short interest. Wall Street analysts seem to agree, with a lower-than-current average price target.

Given this signal mix, I feel it best to remain neutral for now. My verdict would be to hold the stock until we have more data or a major break-up or down. The future valuation of Root could swing drastically in either direction based on the company's ability to deliver on its promises and navigate a challenging industry environment.

For further details see:

Root, Inc. Is At A Crossroads