RES - RPC: Attractively Valued In A Sector With Robust Earnings Potential

2023-03-15 08:07:36 ET

Summary

- RPC is an under-the-radar gem that provides oilfield services to E&P companies and oil majors.

- The company's recent financial performance has been strong, with surging earnings and revenues.

- The business environment still looks healthy for oilfield service companies like RPC.

Introduction

Sometimes the best investments are the ones that don't get much attention from the media or the hype machine. This is especially true for small-cap companies, which often struggle to get the recognition they deserve. One such company that you may not have heard much about is RPC ( RES ). In this article, we'll take a closer look at this under-the-radar gem.

RPC provides support to E&P companies and oil majors in extracting oil and gas from underground wells. This means that their success heavily depends on the performance of oil producers and, consequently, oil prices.

Keeping it simple is often the best approach when it comes to investment analysis. We could spend hours discussing the various factors that might impact oil supply and demand in the next few years, but that could get pretty convoluted. Instead, let's focus on the basics: RPC helps oil producers extract valuable resources, and as long as oil prices remain high and producers generate robust returns, RPC should continue to thrive.

Robust Earnings Growth

Now let’s get into a bit more detail about what the company does and its recent performance.

RPC offers a range of oilfield services, such as pressure pumping and coiled tubing, to help oil producers with well completion, production, and maintenance. By utilizing RPC's skilled workforce and top-of-the-line equipment, oil and gas producers can improve the flow of hydrocarbons from their wells and tackle various well control issues. The company is based in Atlanta, Georgia, and specializes in providing well completion services to independent oil producers and oil majors. Additionally, RPC offers support services like equipment rental, storage, and training services.

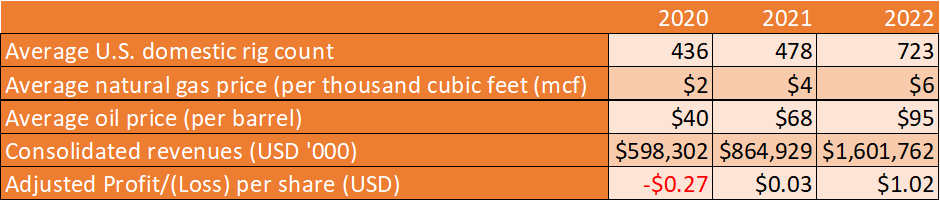

Over the past couple of years, RPC has seen a surge in earnings due to the post-COVID recovery in oil demand that pushed commodity prices higher. In 2022 , the company's revenues nearly doubled from $865 million in 2021 to $1.6 billion. Additionally, RPC's adjusted income increased from $0.03 per share to $1.02 per share, while its GAAP income rose from $0.03 to $1.01 per share. These numbers indicate that RPC has had a very strong year.

Recall that in 2020, the pandemic and subsequent lockdowns and travel restrictions caused a sharp decrease in oil demand, resulting in WTI crude prices averaging less than $40 a barrel. However, demand came roaring back in the following years, with prices averaging $68.13 in 2021 and $94.90 in 2022, according to data from the US EIA.

This was accompanied by a recovery in oil and gas drilling activity that fuelled RPC's turnaround. After a significant drop in 2020, oil and gas producers deployed rigs to maintain or grow production levels, which helped RPC become profitable in the subsequent years, as evident from the table below which shows the rise in rig count, oil prices, and RPC’s earnings. RPC posted an adjusted loss of $0.27 per share in 2020 but has since rebounded.

{kind=link}

Looking Ahead

I believe RPC's solid performance in the fourth quarter is a good indication of the underlying strength of the domestic market and bodes well for 2023. Typically, the fourth quarter can be a difficult one for the service industry, as customers often experience budget exhaustion and cut back on spending. Additionally, drilling activity levels sometimes decline, and unfavourable weather and the holiday season can negatively impact demand. However, this wasn't the case in the previous quarter for RPC.

In the fourth quarter, RPC's oil producer clients had ample financial resources to continue drilling, and there was no indication of spending cutbacks. In fact, the business environment was so favourable that the company's revenues, adjusted EBITDA, and adjusted profit per share all increased by 4.9%, 22.4%, and 28.1% respectively on a sequential basis. This is an impressive feat that highlights the company's ability to capitalize on favourable market conditions and gives us a glimpse of what could happen in the future’s high oil price environment.

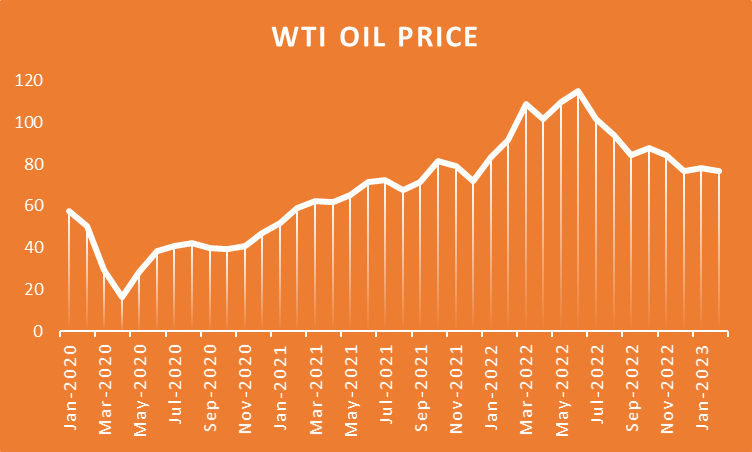

The US oil price averaged well over $100 a barrel from March to July 2022, but it has gradually decreased since then and is currently hovering around $73 at the time of writing. While this might seem like a negative trend, it's important to remember that we're comparing against last year when oil prices surged to multi-year highs. Despite the recent decline, oil prices remain well above the levels seen in 2020 and 2021.

{kind=link}

The great thing is that the business environment still looks healthy for both oil producers and oilfield service companies like RPC. Oil producers are enjoying high oil prices and have been reporting record profits, while oilfield service companies continue to see strong demand for their services, as evident from RPC’s fourth-quarter performance.

With oil prices remaining strong, it's likely that shale oil drillers will keep their spending levels high and continue deploying rigs to maintain or grow oil and gas production. According to Evercore ISI, E&P expenditure in the US is expected to climb by 19% in 2023, which is great news for service companies like RPC. This increase in drilling expenses will provide a solid foundation for the company to grow its revenues and earnings.

It's important to keep in mind that there are always risks and uncertainties that could impact RPC's performance. For example, if there were to be a greater-than-expected deployment of pressure pumping equipment in the US market, it could potentially drive down prices for service companies, including RPC. This could result in lower earnings and margins, even if oil prices remain high. However, we haven't seen any indications of this happening at the moment.

On the contrary, service companies like RPC are being cautious with their spending and are prioritizing maximizing returns from their existing equipment. Rather than competing with one another on price to gain market share, they're showing capital discipline to shareholders. That’s evident from the fact that although RPC is upgrading its equipment, overall, it will continue working with 10 horizontal pressure pumping fleets throughout 2023, the same as last year. This approach is in line with a broader theme in the energy industry, where capital discipline has become increasingly prevalent. This bodes well for RPC and the company might continue attracting favorable prices.

One of the great things about RPC is its clean balance sheet, which includes $126.4 million in cash and no debt. This puts the company in a strong financial position, allowing it to weather any potential market weaknesses or take advantage of M&A opportunities that may arise. Additionally, without any debt overhang or interest expenses to worry about, RPC can fully utilize its free cash flows to reward shareholders with dividends and buybacks.

Takeaway

Looking ahead, it seems like 2023 could be another promising year for RPC, and there's reason for investors to be excited about the company's future prospects. Data from Seeking Alpha shows that the company's shares are currently trading at 7.9x trailing twelve months earnings and just 5.2x forward earnings estimates, which is attractive compared to the sector median of 6.41x ttm earnings and 8.03x forward earnings. In particular, RES stock looks like a great deal when it comes to forward earnings.

That being said, the stock has been under pressure in recent days due to broader weakness in the stock market and lower oil prices. As such, it may be wise for investors to wait until things settle down a bit before buying in. If you're patient, you may be able to get the stock at an even better price. In any case, RPC's strong financials and promising future prospects make it a company worth keeping an eye on for those interested in the energy sector.

For further details see:

RPC: Attractively Valued In A Sector With Robust Earnings Potential