EADSY - RTX Corporation: Market Could Be Overreacting To Engine Issue But Still A Risk

2023-07-25 14:30:29 ET

Summary

- RTX Corporation reported strong quarterly results, but a problem with high-pressure turbines in Pratt & Whitney aircraft engines overshadowed the positive news.

- The market sell-off appears to be an overreaction, but management has not yet fully quantified the impact.

- The scope of the problem looks limited, and RTX shares are cheap now as long as that is the case.

Good Quarterly Results With A Big Negative Surprise

RTX Corporation ( RTX ) reported decent Q2 results , beating EPS by $0.11. The company also guided the full year sales forecast up $1 billion and narrowed the full year EPS forecast to the upper part of the range. Both the commercial and military businesses had positive highlights.

Collins aerospace saw commercial OEM sales increase by 14% and commercial aftermarket sales grow by 29%. Passenger miles flown will have fully recovered to 2019 levels and beyond by the end of this year. On the defense side, the Raytheon segments have a backlog of $52 billion total (around 2 years of sales) and a book to bill ratio over 1 on a year-to-date basis. This includes a $1.2 billion order for AMRAAM missiles, along with other new bookings for Javelins and other missiles to support of the conflict in Ukraine and allow allies to restock their inventory.

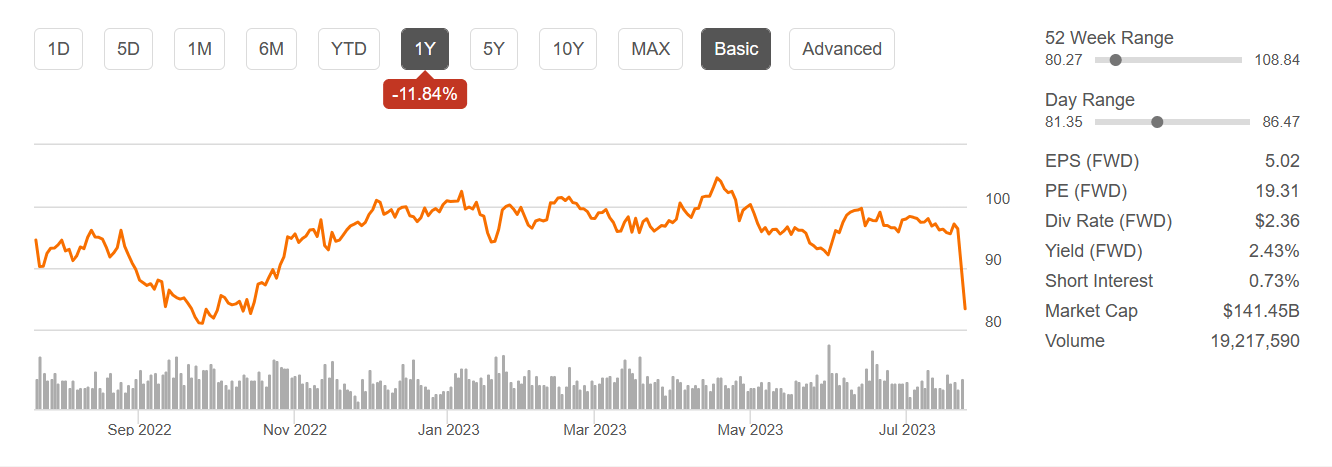

All this good news was completely overshadowed, though, by the disclosure of an issue with high pressure turbine disks on aircraft engines manufactured by the Pratt & Whitney segment. Since I last covered Raytheon Technologies (as it was known then) in April 2022 , the stock took a dip last fall but recovered to trade sideways in the upper $90's, for basically flat performance overall. At least that was true right up until the earnings release, which took the share price down about 15%, back around the September 2022 lows, instantly obliterating about $21 billion of market cap. To put it in perspective, that is about equal to 1 times Pratt & Whitney's annual sales or about 14 times the division's operating profits.

RTX 1-year Price Performance (Seeking Alpha)

{kind=link}

The market response feels like an overreaction. It may very well be, but there are still a lot of unknowns to work through, creating risk for the stock.

What We Know (And What We Don't)

The source of the issue is impurities in powdered metal used in manufacturing high pressure turbine disks. It is not a completely new issue, having first been seen on a disk on the V2500 engine in 2020. The company has isolated the problem to powdered metal produced internally between 2015 and 2021. The impurity issue in the metal has been addressed, and it is not impacting parts made in 2022 and later.

Since the problem was first identified, the severity has been low enough that it could be identified and addressed during scheduled maintenance outages, with only about 1% of the fleet needing to be pulled for further work. This issue was also found on the newer geared turbofan engine, the PW1100G-JM, which like the V2500 is used on Airbus ( EADSY , EADSF ) A320 aircraft.

Recently, the frequency of defects has increased to the point that the company has determined that the affected engines need to be taken out of service for inspection ahead of their normal schedule. This will require about 200 accelerated inspections by mid-September with about an additional 1000 to follow through next year. This is out of an existing fleet of about 3000. While the actual inspection can be done within a shift and there are no issues obtaining replacement parts, the work cannot be done on-wing. This means that engines need to be taken off and disassembled. While management did not commit to a turnaround time on the earnings call, CEO Greg Hayes later said on CNBC that the full maintenance cycle could result in 60 days of down time.

As for the financial impact, the company so far has only reduced the free cash flow estimate for 2023 downward by $0.5 billion to $4.8 billion total. This is driven by the costs to gear up maintenance sites to handle the added workload. No revisions were made to sales or earnings estimates for 2023 or later years, however this was because management does not yet have a good estimate, not because the impact will be minimal. The company expects to provide more clarity by the next earnings release, but in the meantime, the uncertainty is a headwind for the stock. There will be operating cost impacts to conduct the inspection as well as the requirement to compensate the airlines for the added down time.

In addition to these uncertainties, analysts on the Q2 earnings call asked about some larger issues. For example, there was concern that regulators could ground these engines until repairs are made out of an abundance of caution. Others questioned the culture and reliability of the company given earlier problems with the GTF engine including excessive vibration and wear on various engine parts as well as operating issues in hot, dusty environments. Over the longer term, there is also worry that these issues could cause loss of market share to competitors such as General Electric ( GE ), trading up 5% after the RTX disclosure.

My own view is that these larger risks are low probability. With the root cause already identified, the proactivity of the company in scheduling inspections, and the lack of actual safety incidents so far, I believe the impact of the problem is bounded. I expect shares to recover by next quarter as the full costs of the issue become clearer and an upper bound is communicated. Nevertheless, the potential severity of these larger risks is high, even if the probability is low. This will create volatility for the share price for the next few weeks. The shares are now cheap, but there is no need to buy all at once for investors who are comfortable with these new risks.

Earnings Model Update

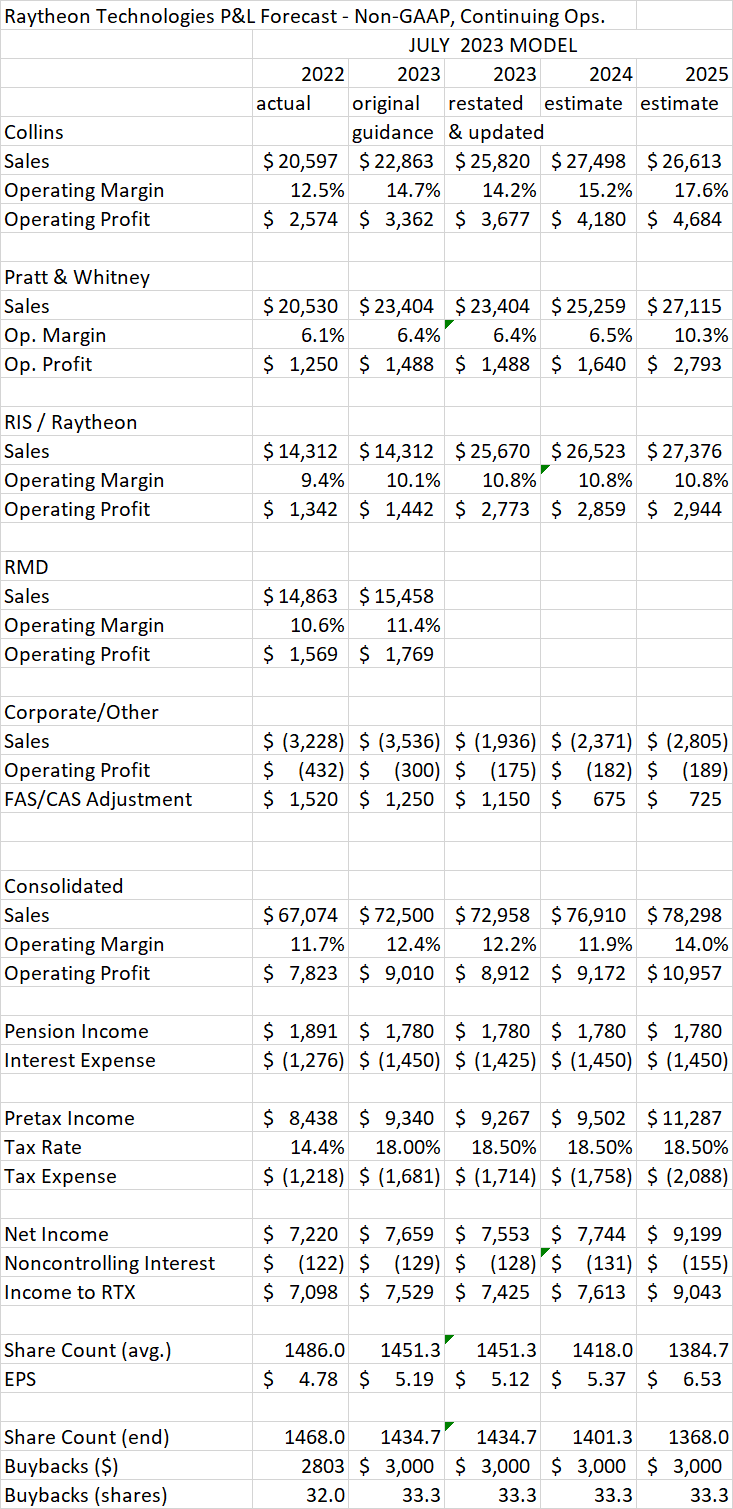

I have updated the earnings model I used in my last article with assumptions developed from the company's outlook provided at the June 2023 investor day . I also made some adjustments for the new information that came out in the 2Q earnings release. The first thing to note is that the company is restructuring, combining its two Raytheon segments into one and moving the Command and Control and Air Traffic Management businesses (~$2.7B annual sales) into Collins. The restructuring also reduces intercompany eliminations.

I am using midpoint company sales growth projections for the 2020-2025 CAGR of each new segment: 6.5% for Collins, 9.5% for Pratt, and 4% for Raytheon. These values set my estimated 2025 sales. The company also provided operating margin growth estimates by 2025 for each segment which you can see in the model below. Below the operating income line, I used recently updated company guidance for items like corporate costs, interest, and taxes.

Having set 2025, I assumed 2024 results would be an average of the latest 2023 guidance with 2025 with one exception. I reduced Pratt & Whitney operating income by $500 million for 2024 to reflect the added engine inspection and repair costs. I assumed these added costs go away in 2025 and did not assume any sales reduction. This could be an optimistic forecast, but we will know more next quarter. To calculate EPS, I am also assuming $3 billion per year of share buybacks at an average price of $90.

{kind=link}

Valuation

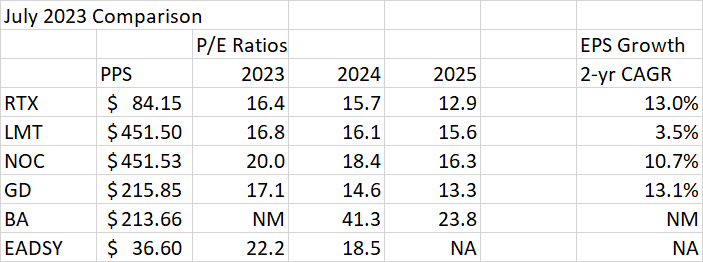

I calculated P/E's for RTX using the earnings estimates above and for peers using Seeking Alpha's Peer Comparison tool. The drop in RTX following the earnings release puts the 2023 P/E at the bottom of the range of 16.4-20.0 for the defense-oriented companies including Lockheed ( LMT ), Northrop Grumman ( NOC ) and General Dynamics ( GD ). Ahead of the earnings release, RTX was valued second highest of the group. Similarly, based on 2025 EPS estimates, RTX is still at the low end of the range of 12.9-16.3. This is despite the earnings growth being at the high end of the group.

Because RTX is a mix of commercial and defense, it should also be compared to more commercial aviation-oriented companies. The Boeing Company ( BA ), which has had its own profitability issues, has negative expected earnings in 2023, but recovers by 2025 to a P/E of 23.8. Airbus is also valued above the defense-oriented companies in 2023 in 2024, the years for which estimates are available.

{kind=link}

The higher growth forecast and the commercial aviation business both suggest RTX should trade at the high end of the range of its defense peers, rather than the bottom. As long as the engine issue remains a manageable problem, RTX is a bargain in the low $80's.

Capital Management

RTX bought back $1.16 billion worth of shares in 1H and remains on track to buy back $3 billion total in 2023. As we saw in 2022, seasonal issues limit free cash flow ("FCF"), which was low in 1H. Despite the negative FCF of -$1.19 billion year-to-date, the company is still forecasting $4.3 billion of free cash flow in 2023, down from $4.8 billion prior to the engine issue, and $4.9 billion achieved in 2022. The dividend was raised 6.7% this year to $0.59 per quarter from $0.55 previously. That amounts to $3.4 billion of dividends in calendar 2023. The $6.4 billion of total capital return to shareholders exceeds projected FCF by $2.1 billion.

Most of this can be covered by the sale of the actuation and flight control business to Safran ( SAFRF , SAFRY ) for $1.8 billion, but the company has also issued incremental debt. Interest coverage (operating profit/interest expense) is projected to be 6.25 in 2023, up only slightly from 6.13 in 2022. The 2023 EBITDA estimate of $12.87 billion implies a net debt/EBITDA leverage of about 2.2.

Assuming RTX gets back on track following the engine issue, they expect free cash flow to increase to $9 billion in 2025. This would cover capital returns to shareholders without the need for further asset sales or debt issuance.

Conclusion

The Pratt & Whitney engine issue is not the type of bombshell we expect out of RTX, and the market was clearly shocked with a 15% drop at the open. This is likely an overreaction, and shares have even rebounded slightly as I write this, now down about 12.5%. Still, the lack of clarity from management so far on the exact scope of the problem has given traders the ability to assume the worst. It may take several weeks or even until the next earnings release to better quantify the issue. Shares could remain volatile during this time.

In the low $80's, RTX Corporation shares are a bargain, as long as the engine problem remains contained. I believe that will be the case, but investors need to be aware of the risks mentioned here.

For further details see:

RTX Corporation: Market Could Be Overreacting To Engine Issue But Still A Risk