ARCC - Runway Growth Finance: The Runway Is Long Get In Early And Stay A While

2023-04-06 23:19:26 ET

Summary

- Business Development Companies offer nice high yield diversification to your portfolio.

- Make sure you have the right team on your side here. Management quality is crucial.

- With the VC market in turmoil, some great opportunities are surely to arrive for well-run and managed companies.

- With low leverage and large solid shareholders, the time might be opportune for Runway Growth Finance.

- This could be right up your alley if you're looking for high growth high yielding investments and have a higher risk tolerance. Runway is a speculative buy.

Runway Growth Finance (RWAY) is a very underfollowed Business Development Company ((BDC)). In fact, there are just 782 sets of eyes watching this one on Seeking Alpha. Compare this to Ares Capital ( ARCC ) at 67.31k and Main Street Capital ( MAIN ) at 65.02k and you'll see what I'm talking about! So, for people reading this and following RWAY, I'm going to give you a quick primer into what a BDC is and then follow up with who RWAY are and why I think they're interesting! Let's dig in.

BDCs

BDCs were created by the US Congress in 1980. The aim was to help spur job growth and job creation by creating a source of capital or funding for new/small or distressed businesses. In simple terms they raise capital by either listing, issuing bonds or other types of debt and then use that cash to provide capital injections to their customers. Depending on the strategy of the BDC they can focus on funding a small startup or the late-stage business in the VC space or they can provide capital to businesses in distress that need a cash infusion to help them through a turnaround or cash flow crunch.

The capital they provide can be in the form of loans given at attractive rates or they can take an equity stake. It could also be a hybrid in the form of convertible debt and preference shares (prefs) for example. As a result, a BDC's portfolio can comprise of equity, prefs, loans, warrants or any combination of the above. They are like Venture Capital funds (VCs) in that they provide capital to startups et al but are also quite different in that VCs tend to be the abode of a small and limited group of large institutions and wealthy individuals. BDCs on the other hand can be listed and so are available to retail investors too. Over and above this they need to comply with stock exchange and BDC regulations are quite liquid, and so they can offer that additional level of diversification to an investment portfolio.

BDC Risks

As one would imagine investing in companies like this doesn't come without its fair share of risks. For one regulation stipulates that BDCs must invest at least 70% of their assets in private or public US firms of market values that are less than $250m and they must provide managerial assistance to the companies they invest in or lend to.

So, off the cuff, we can see that the companies tend to be smaller and so could be considered higher risk. On top of that even though shares in a listed BDC can be liquid their underlying investments may not be. Higher interest rates serve as a double-edged sword, of course as rates rise the income, they generate rises on the loans they provide (if they're floating rate) but at the same time because they borrow money, they may need to pay higher rates of interest on their debt (unless its fixed). On top of this higher rates may make it more difficult for their customers to repay them. In a recession their underlying clients could also find it hard to remain in business.

Sounds like a hard game to be in and in anything that's this hard the required rewards need to be good to make it worthwhile. This is not a low margin, low risk regulated utility type investment here. This is falls into the higher risk space.

What are the potential rewards?

To justify the risk the reward needs to be worthwhile and in this business they can be considerable. As a regulated investment company, they are required to pay out at least 90% of profits to shareholders so dividend yields are high. They fill a void in the market where traditional lenders don't often participate so are able to charge higher rates than average on the loans they offer. Part of the investment portfolio could be equity in companies that absolutely knock it out of the park and become enormously profitable which could drive portfolio book value up considerably and upon sale generate nice profits for shareholders.

Runway Growth Finance

Now that I've provided a quick synopsis on the BDC stable it becomes clear that in companies like this the number one asset a BDC can and must have is management. It is without a doubt imperative that those running the show are highly competent investors and businesspeople. They must fully understand and comprehend the risks involved in deploying their capital through not just multiple business cycles but also into companies in varying stages of development or financial health. Before going anywhere near this space, one must be sure that you're backing the right jockey.

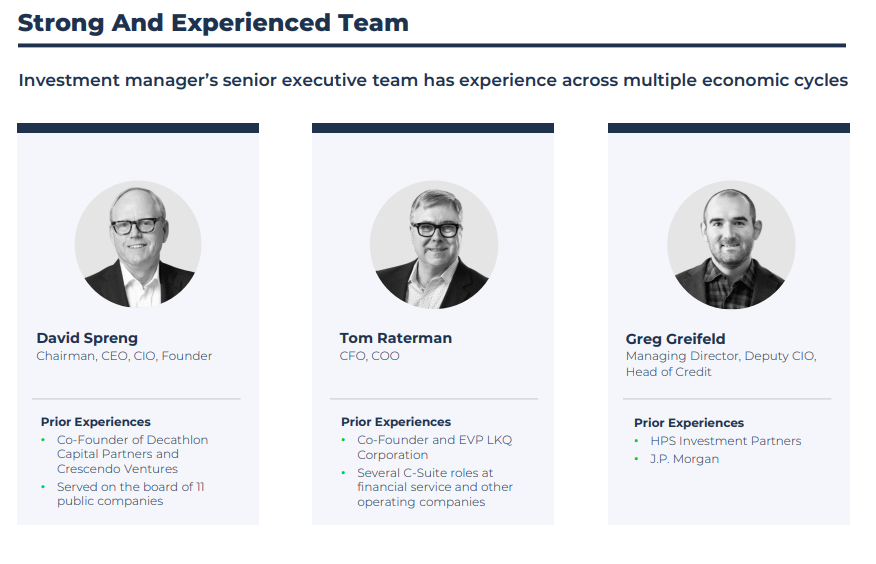

So, who is riding the RWAY pony? The CEO/CIO and founder of RWAY is a person by the name of David Spreng and his CV is impressive. David is 25-year veteran in the VC space has backed over 50 Technology companies with 18 IPO's and 14 trade sales. He has also been named to the Forbes Midas list (a list of the best venture capital investors) four times and has served on the board of 11 public companies. This is an industry pro in my book, and I'd certainly be willing to assume that he knows what he's talking about. The senior executive team has a solid overall CV too. In addition to this the company has a strategic partnership with Oaktree Capital Management who also happens to be a 52% shareholder in the business. Oaktree in turn is owned by Brookfield Asset Management (BAM), So, the bench is deep here.

RWAY Investment managers senior exec team (Company Presentation)

{kind=link}

The business

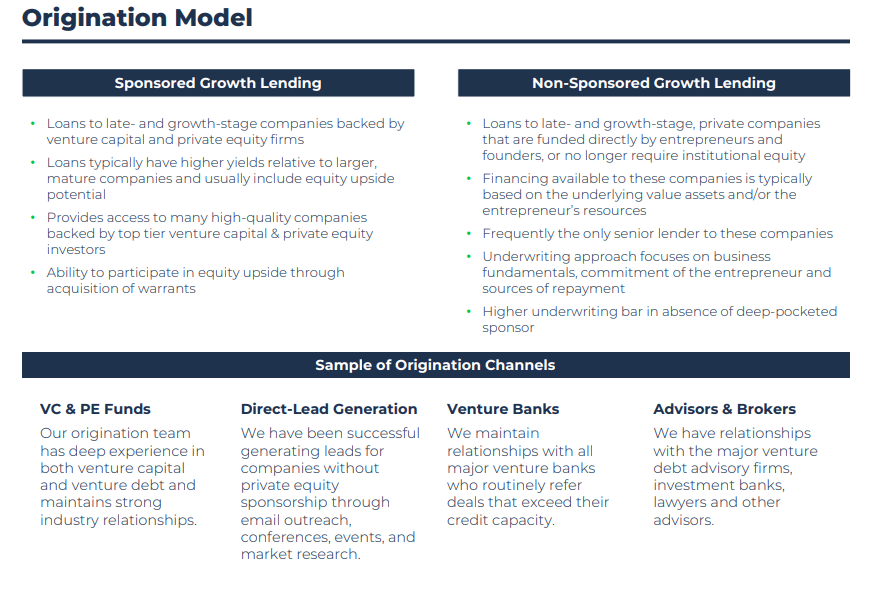

RWAY looks to reduce risk in a few ways, the first is to limit who they take on as clients. They work with growth and late-stage companies which avoids the startup phase (highest risk) and tends to work with businesses that are demonstrating traits of success which increases the odds of survival. They lean into businesses where there is strong equity sponsorship and or high insider ownership to which means solid/driven shareholders. Business is originated as follows.

{kind=link}

Over and above this the lending criterion is strict; it is built on the premise that the company can withstand all economic environments. The loan book is 100% floating rate, so higher interest rates are great (all things being equal). Ninety-nine percent of debt is first lien (secured by collateral), and the company insists that its customers have low 'loan to our value' balance sheets. They really try to reduce the risk as much as is possible or feasible and because they've 'been around the block' a few times the vast experience of the team makes me think that this strategy has been honed and tweaked over the years into what it is today.

History

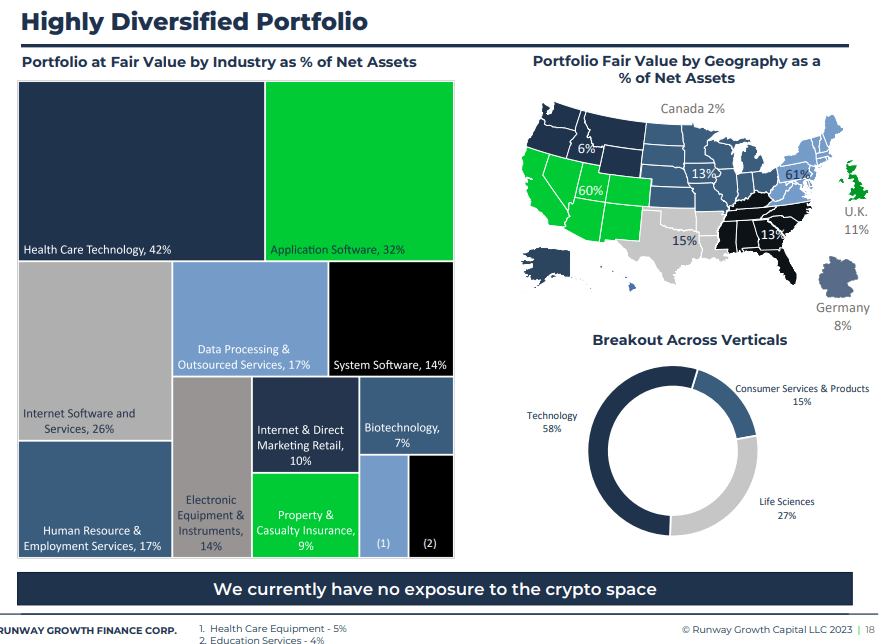

The company was founded in 2016 and then IPO'd in 2021 so its new to markets but has been around for just on 6yrs or so. What attracts me to the business is how conservatively it's been managed. Despite all the hubris in tech over the last few years the company has been very conservative in its capital deployment strategy. It looks to me like they are building a slow and steady asset base and being deliberate about it too. In fact, coming into 2023 the company had below target and peer group leverage which means it has huge potential to ramp up its activities if the right opportunities come along. The portfolio is also quite diversified and covers various industries, geographies, and sponsored/non sponsored companies. This does not look like a high risk concentrated loan book to me.

{kind=link}

Despite this pretty timid posture growth has been chugging along quite nicely and so has the dividend. The dividend was first initiated and paid in November 2021 at 25c per quarter and has ratcheted higher on a quarterly basis since to its current rate of 40c. The dividend has risen by 60% since its IPO and this despite the business running its balance sheet conservatively and with plenty of room for growth.

{kind=link}

On the 13th of March, the company released a statement post the Silicon Valley Bank ( OTC:SIVBQ ) collapse and highlighted the following:

WOODSIDE, Calif., March 13, 2023 (GLOBE NEWSWIRE) -- Runway Growth Finance Corp. (Nasdaq: RWAY) ("Runway Growth" or the "Company"), a leading provider of flexible capital solutions to late- and growth-stage companies seeking an alternative to raising equity, provided a business update in response to recent industry events concerning Silicon Valley Bank ("SVB").

"We are encouraged by the decision of the Treasury, Federal Reserve, and FDIC to fully protect all SVB depositors," said David Spreng, Founder and CEO of Runway Growth. "This action directly impacts our portfolio companies for the better. As we navigate the difficult waters ahead, management believes our focus on the latest stage companies will prove to be a differentiator in the venture debt space. Our 99% concentration in first lien loans protects our portfolio, as we are unencumbered by the complications of dealing with a senior lender. Further, our focus on first lien loans protects our investors from situations in which a second lien lender might find itself subordinated to the FDIC and precluded from taking action to preserve the value of a loan. Runway Growth will continue to prudently deploy leverage to fuel non-dilutive growth for our portfolio companies and returns for our shareholders."

The Runway Growth management team is monitoring the venture market extremely closely. The Company does not have any deposits or loans with SVB, nor does the Company participate in any credit facilities agented by, or that include SVB as a lender.

Runway Growth continues to be focused on preserving the quality of its portfolio and has a strong track record of mitigating risk in all market environments.

I'm not sure if this statement had any impact on the market but the share price has remained steady. It's down just 1.3% YTD despite all the chaos in the space it operates in.

Opportunity and Valuation

This is the opportunity in my view. The current venture capital market is in turmoil and was so even pre the collapse of SIVBQ as markets and growth stocks tanked last year. Stories can be found of Venture Capital funds taking massive losses and write downs. Of the market for funding drying up and how new startups and even some growth stage and late-stage firms are battling for capital. Provided RWAY has been as conservative as they say they have and that the investments they've made to date haven't deteriorated much this could provide them with some choice pickings over the next few quarters. Anyone that's willing and able to finance now will be inundated with requests for capital and where some firms stumble others will see wonderful opportunities. With such low leverage the company could find itself in the right place at the right time with asymmetric opportunities to the upside. This could be a boon for well capitalised well run BDCs and RWAY could benefit just as much as any other.

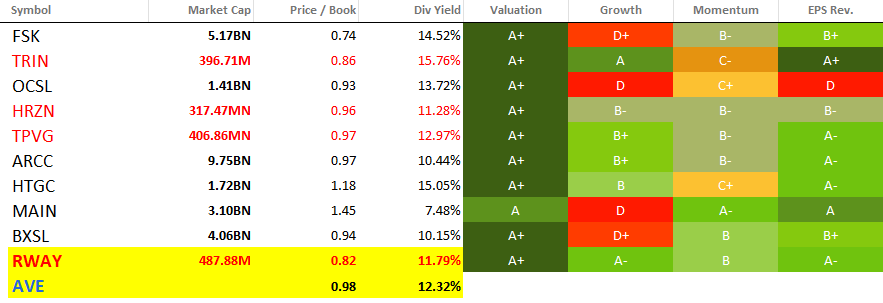

There are quite a few BDCs listed out there so I've narrowed down the list to those I think are most comparable - forgive me if I've missed one you think should be on the list, but this is what I've come up with.

{kind=link}

What's immediately noticeable is that these companies have monstrous dividend yields. Secondly there is definite 'big' and 'small' cohort here, just four companies operate at the sub $1bn market cap of which RWAY is one. The other thing that sticks out is that they all seem cheap from a valuation perspective. It thins out a bit when we get to growth though. The smaller companies are growing faster than the larger ones which intuitively makes sense as the base is lower. Also, just two trade at a premium to book value.

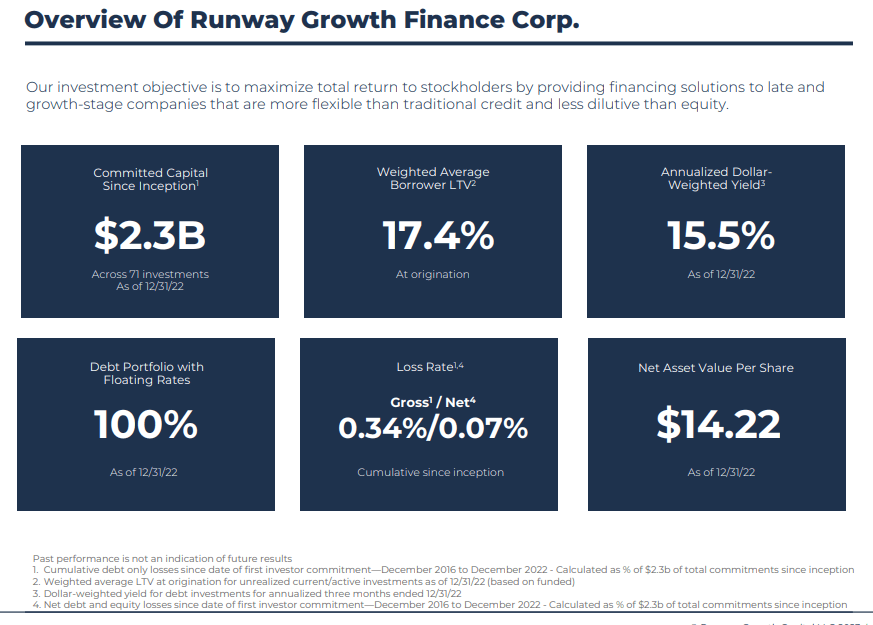

So, RWAY slots in quite well, as you can see it has all 'green' on the screens. The trick here lies not in its current form though but in its future form. At recent results leverage increased to 0.97x which is below its target and the peer group average of 1.3x. The increase to peer group average and its target is real optionality to both earnings, book value and dividend growth.

That sort of growth can and should allow the valuation to move closer to and even above book value which at last numbers is $14.22. From current prices of $11.80 that points to 21% upside. However, as the leverage moves higher, I'd also expect the book value to move higher and the dividend to move higher too. So, you could find some sort of compounding take place here. On top of this the company has announced that it will pay supplemental dividends this year too of 5c per share per quarter.

Your current $11.80 start price with a base div of $1.60 yields you 13.6% today. That is supplemented by an additional 5c per quarter currently so the effective div is $1.80 for an actual yield of 15.3%. At this rate you'll get what you paid for the shares back in dividends in just over 6 years (assuming they don't grow from here!). Over and above this the company is still in growth mode, it's small, it's underleveraged and it's potentially entering an excellent time for opportunistic deal flow as the VC markets splutter and the US potentially enters recession. With large quality backers like Oaktree (and ultimately Brookfield), there shouldn't be any reason why this company shouldn't reach a market cap north of $1bn over time. Assuming that does happen, the upside from here could be pretty impressive.

RWAY risks

The risks here are covered earlier in the article from a BDC perspective on a high level. However, for the company itself, I'd point to the following.

Firstly, I'm backing the jockey on this one, I believe that Mr. Spreng is a top-notch leader with vast experience and enormous credibility in this space. If for some reason, he left the business I'd look to exit.

Secondly because the VC market is in turmoil, you'd expect the company to be extra vigilant on how it deploys its capital right now. Opportunities could be massive but so are the risks. This makes the CEO even more important here. A small company like this has no margin for error.

Higher interest rates and the possibility of a recession need to be considered as a potential headwind to funding of the business and its ability to have the loans it granted paid back. Also, because they do take some equity in companies the potential of a market crash or severe derating in the markets could mean lower asset values for the equity stake they hold.

The company doesn't trade huge volumes on a daily basis as most of its free float is held by larger strategic shareholders. This needs to be considered when deciding on the position size in your portfolio.

Conclusion

RWAY is a smaller cap BDC operating in an exciting market with many growth verticals. It has a well-diversified portfolio, an underleveraged balance sheet, and an attractive dividend yield.

This coupled with a very experienced highly rated and accomplished founder/CEO alongside large deep pocketed strategic shareholders set the company up to be aggressive in the funding market when many other companies and competitors might be looking inward.

Its small cap nature, less liquid shares and, of course, the current state of the US and global economy may put conservative investors off; however, for those with a higher risk appetite and a penchant for growth, this could be just what you're looking for!

I personally own RWAY shares and rate it a speculative high yield buy.

For further details see:

Runway Growth Finance: The Runway Is Long, Get In Early And Stay A While