SPY - RVT: Small-Caps Poised To Make A Comeback But Industrial Exposure Is Not Ideal

2023-07-19 11:18:23 ET

Summary

- Since the pandemic, capital has tended to gravitate towards large-cap stocks during times of market risk aversion, causing the large-cap:small-cap ratio to shift significantly to the upside.

- Recent economic predictions suggest a lower probability of a US recession, which could improve sentiment towards small-cap stocks and potentially lower the large-cap:small-cap ratio.

- The Royce Value Trust, a small-cap closed-end fund, is highlighted as a reliable investment option, despite concerns about its high exposure to the industrial sector.

- We also like the risk-reward on the charts.

Time For The Baton To Be Passed On To Small-Caps?

US blue chips have enjoyed their time in the sun for a while now; the chart below juxtaposes the relative strength of the large-cap-oriented S&P500 and the small-cap-based Russell 2000. We can see that until the pandemic this ratio tended to oscillate within a narrow range of 1.5-1.95x.

{kind=link}

However, since the pandemic, what we can see is that there's been a significant shift in that old range (to levels of 2.4x); essentially, what we can glean is that since 2020, when there's been risk aversion in the markets, capital tends to gravitate towards large-caps in a big way, even as small-caps lose favor.

We saw that during the onset of the COVID pandemic, and we've seen that trend play out once again in H1-23, on account of the regional banking crisis with the large-cap:small-cap ratio hitting similar heights. Of course the AI theme has also played an instrumental role in propping up large-caps this year, a lot of which are tech-focused plays.

Having said all that, recent noise coming from the economists' club suggest that things may not be as bad as initially feared. In June, we saw Goldman Sachs, which had previously placed a 35% probability of a US recession (over the next 12 months) in March, bring that down to 25% , and yet again, earlier this week, the odds were scaled down to just 20% . Goldman isn't the only one; in fact a survey carried out by WSJ across 69 economists showed a cut in the probability of a recession from previous levels of 61% to 54% .

It certainly helps that inflationary headwinds appear to be losing steam; whilst we will likely see another hike by the US Fed this month, the Fed Watch tool suggests that we may not be too far away from rate cuts .

This could do a world of good for sentiment towards small-caps, who typically don't have the most robust balance sheets and often feel hamstrung when the cost of money gets dearer.

Given these changing circumstances, and the overbought nature of large caps, small-caps look ripe to garner investor attention. This could result in the large-cap:small-cap ratio dropping closer to its mid-point or back to its old trading range.

Royce Value Trust - Tried and Tested

If you're on the lookout for reliable small-cap products in the closed-end fund space, you may consider looking at Royce Value Trust ( RVT ), one of the oldest products around. RVT has been around since 1986 and is incidentally considered to be the first small-cap closed-end fund in this business.

We like the ethos and stability that this fund offers as it focuses on small-cap stocks with high ROICs (Return on Invested Capital), a metric that is often not given due importance in this industry, but can be very useful in ascertaining the durable strength of these small-caps. RVT's stability quotient is exemplified by the fact that they have a lead manager (Chuck Royce) who has been at the helm of affairs since 1986 and continues to call the shots. This helps bring a degree of stability to RVT's long-term investment plans, quite unlike other fund houses where fund manager churn tends to be more elevated. Crucially, RVT is also one of those rare close-ended offerings where no monthly fees will be charged if the fund fails to generate positive returns over a trailing 36-month period.

{kind=link}

As the image above highlights, RVT has a long history of outperforming the Russell 2000 by 1.32x. It isn't just the relative return differential; RVT has also demonstrated a track record of consistently putting out a portfolio with slightly lower risk qualities than the Russell 2000. Note that it has always showed a lower standard deviation figure, regardless of the time frame in question.

RVT

The lower standard deviation certainly provides the foundation for RVT to produce superior Sharpe ratios (the excess returns over the risk-free rate for every per unit of total risk taken), be it on a short, medium or long-term basis.

RVT

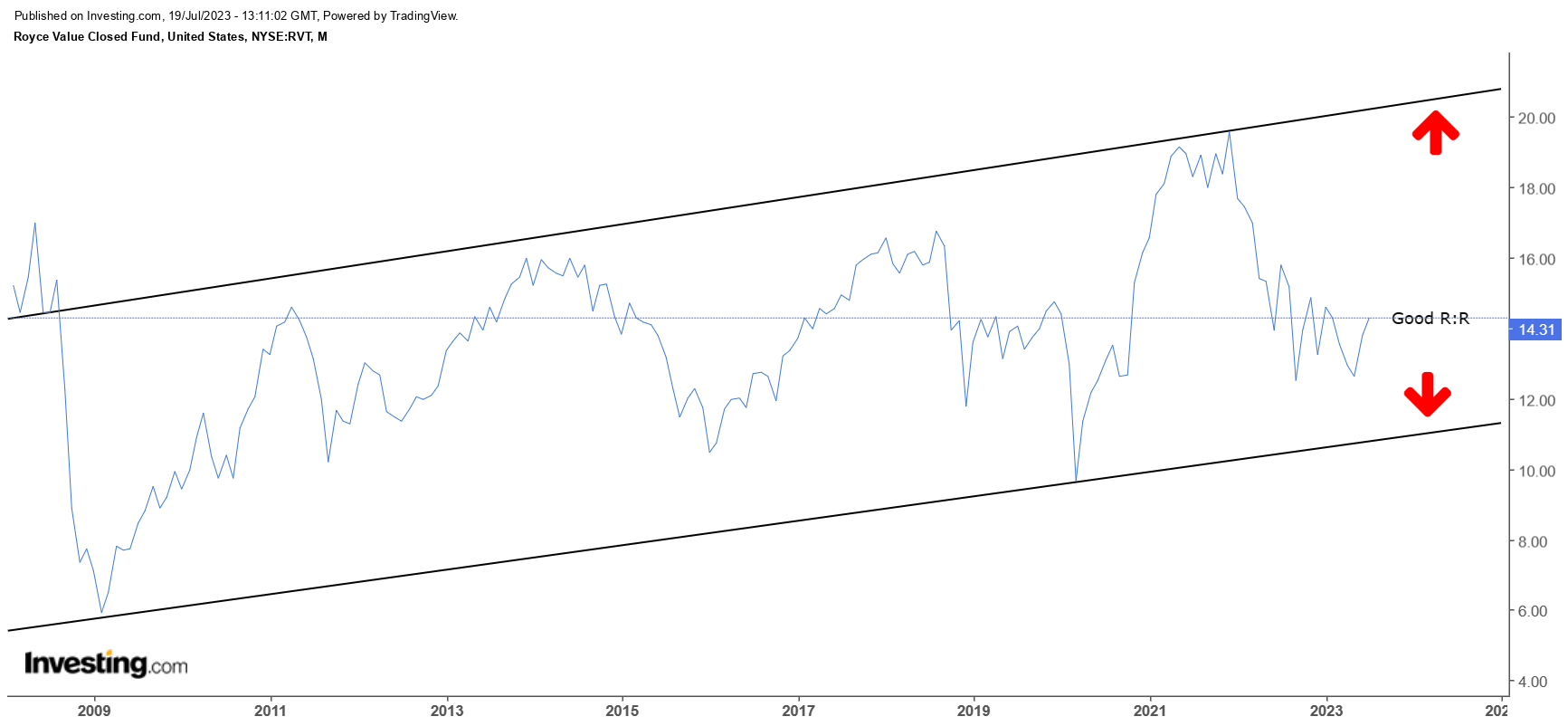

Then if we look at RVT's long-term monthly price imprints since the GFC we can see that after that event, it has been trending up in the shape of an ascending channel. If one were to use the two boundaries of the channel as pivot points and contemplate a long position at this juncture, the risk-reward certainly looks alluring at over 1.8x.

{kind=link}

As far as valuations go, note that RVT's portfolio of small-caps can currently be picked up at 23% discount to the P/E of the S&P500 ( 20X )

Also consider that RVT's relative strength versus IWM is still around ~18-20% off the mid-point of its long-term range, and it could benefit from some mean-reversion.

{kind=link}

Risks - High Industrial Segment Exposure Is Not Too Conducive At This Juncture

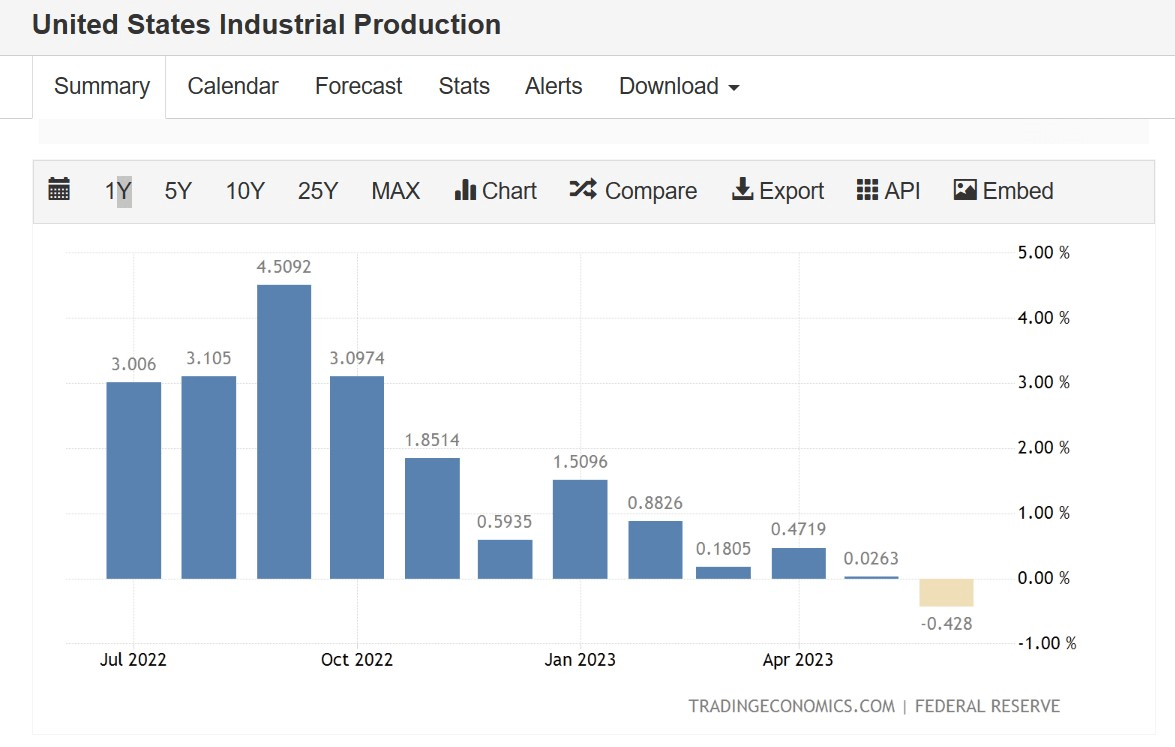

One of our concerns about pursuing RVT at this juncture is its top sector exposure - the Industrial segment, which accounts for 29% of the total portfolio, a good 1100 bps higher than the next largest segment. As things stand, underlying metrics don't look too great. Last month, YoY industrial production in the US dropped for the first time in close to two and a half years.

{kind=link}

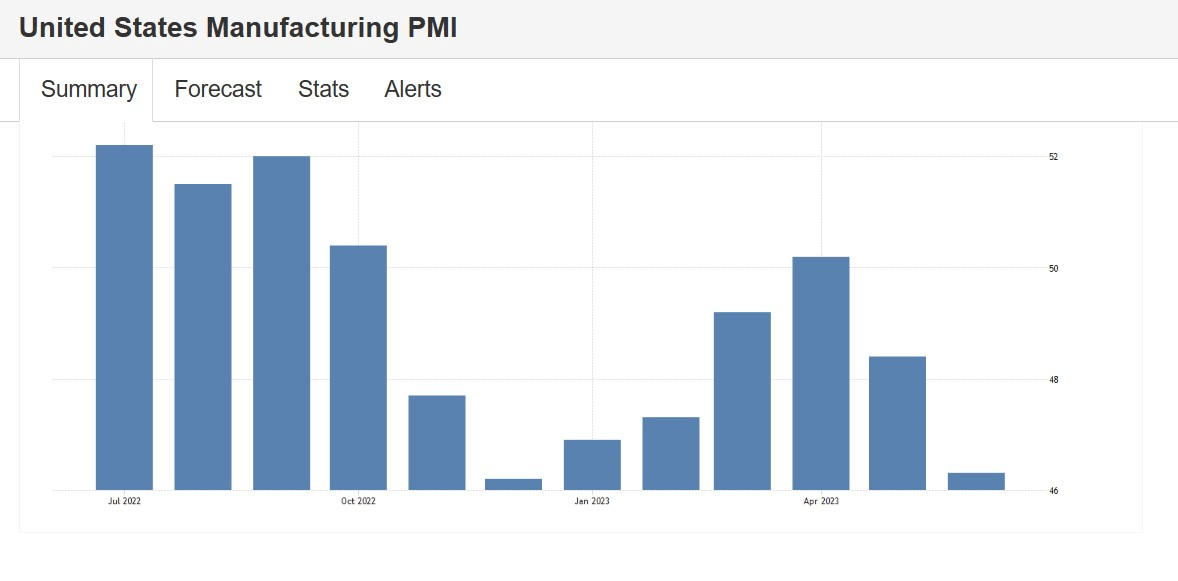

Secondly, the forward-looking manufacturing PMI index dropped for the second successive month, falling to its lowest point in six months. The report suggested there was a sharp decline in new orders, impacted mainly due to high inflation and interest rates. Whilst inflation could be on the way out, the impact of rate hikes could be expected to linger for a few more quarters.

{kind=link}

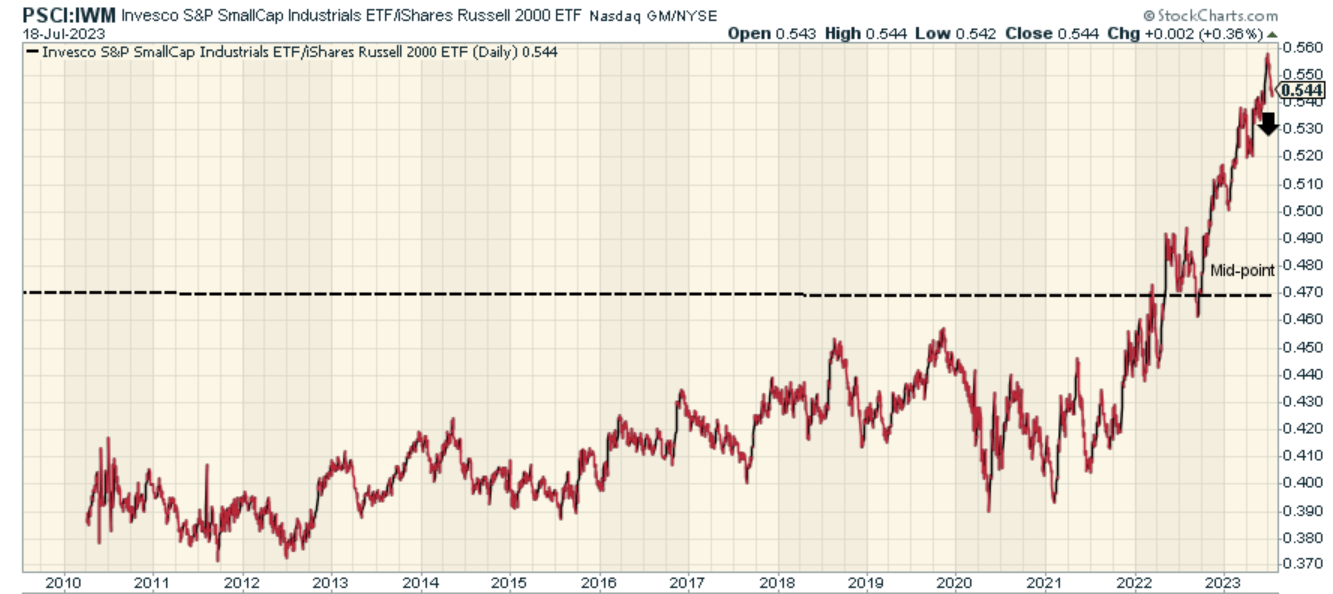

Finally, if we look at the charts, it is concerning to discover that within the small-cap landscape, industrials are currently one of the most overbought trades. The current small-cap industrial ratio to overall small-caps is not far from record highs, and trading around 15% higher than the mid-point of the long-term range.

{kind=link}

For further details see:

RVT: Small-Caps Poised To Make A Comeback, But Industrial Exposure Is Not Ideal