SPGI - S&P Global: A Collection Of High-Quality Assets With Strong Moats And Long-Term Compounding Opportunities

2023-06-28 17:13:11 ET

Summary

- S&P Global is a collection of extremely high-quality assets that enjoy strong barriers to entry, leading positions, and favorable growth prospects.

- Financial performances have been stellar and should continue in the right direction.

- The integration of IHS Markit is well on track and could deliver more cost synergies than initially expected.

- Although the stock is not cheap, it is not expensive either, making it a potentially attractive investment for those seeking a high-quality company with potential for double-digit earnings growth.

Business overview

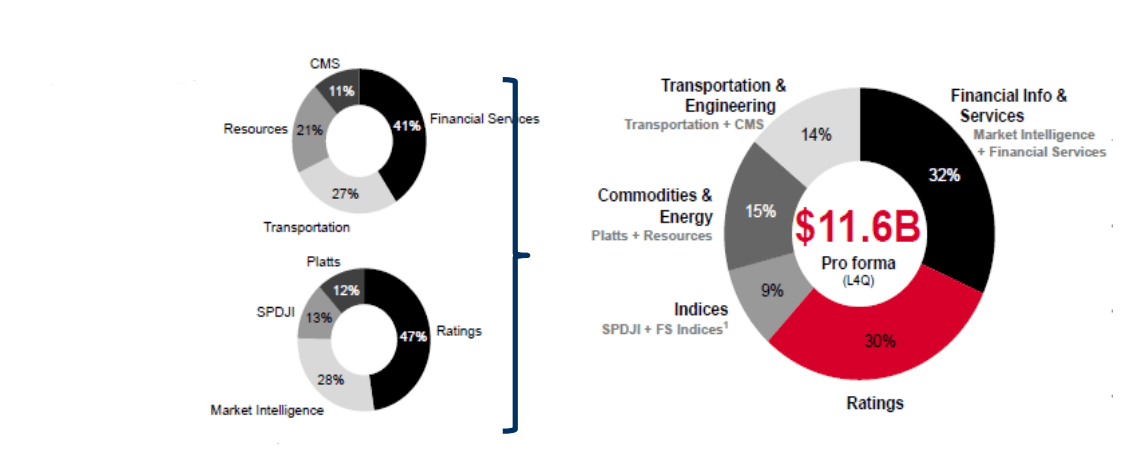

S&P Global Inc. ( SPGI ) operates two distinct businesses: credit rating (28% of revenue) and data & analytics (72% of revenue). From a reporting standpoint, the company reports currently under six segments. However, on May 2023, the company announced the disposal of its engineering solutions business, accounting for 3% of total revenue, to KKR for $975 million in cash. Following this transaction, revenue will be split as follows:

(Source: Annual report)

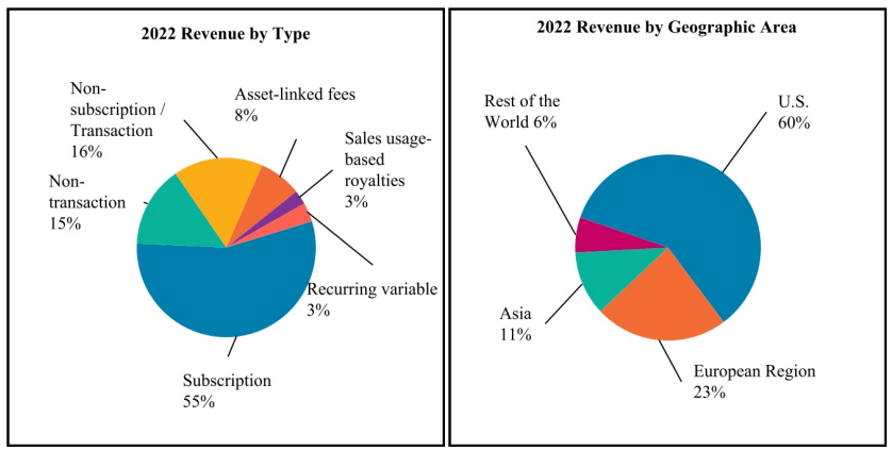

The following charts show the revenue split by categories and regions prior to the disposal of the engineering solutions business. Note that the engineering solutions business consists mainly of subscription revenue.

{kind=link}

(Source: Annual report)

S&P Global strengthened its data & analytics business with the merger of IHS Markit ($44B all-stock deal closed on February 2022). IHS Markit offers complementary assets such as fixed income indices and bring additional scale while diversifying customer base, increasing recurring revenue mix (from 69% to 76%) and creating $350 million cross-selling opportunities and $600 million cost synergies.

{kind=link}

(Source: Company presentation)

The credit rating business

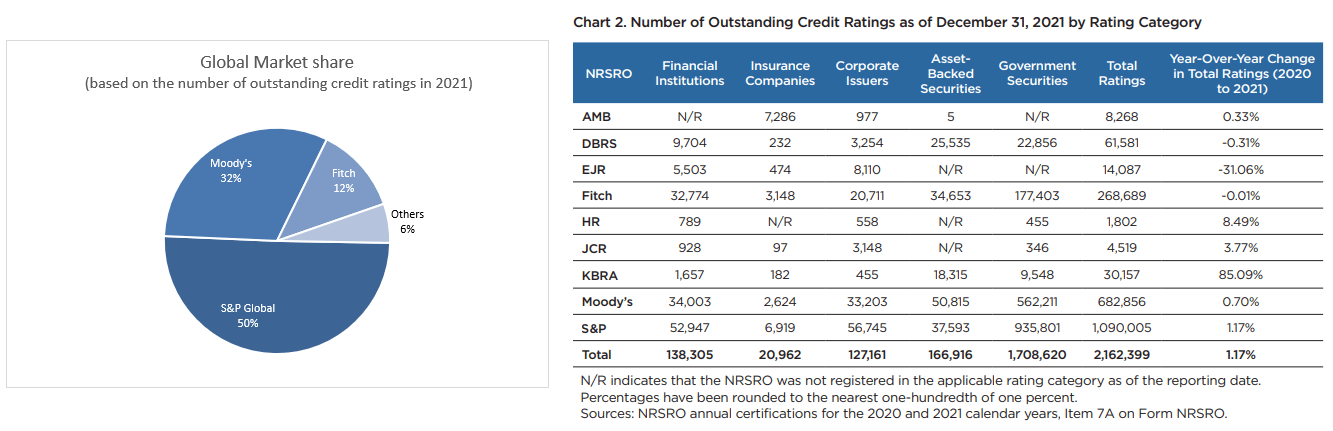

S&P Global provides unbiased credit ratings expressing the ability and willingness of an issuer to meet its financial obligations. The customer value proposition is extremely strong, probably one of the strongest among all industries. Indeed, issuers pay around 7 bps to obtain a credit rating whereas it enables them to reduce borrowing costs by at least 30 bps and up to 65 bps per year over the life of the bond.

S&P Global is the largest credit rating agency with 50% market share globally. The credit rating industry is highly consolidated as highlighted by the 95% market share controlled by the three largest players.

{kind=link}

(Source: www.sec.gov/files/2023-ocr-staff-report.pdf)

The company generates transaction revenue from ratings related to debt issuance and non-transaction revenue from frequent issuers arrangements (annual fee covering a certain number of debt issuance), rating surveillance, royalties from the market intelligence segment (that resells credit research) and rating evaluation services (evaluating the impact of different scenarios on a credit rating).

After accounting for ~55% of segment revenue in 2020 and 2021, transaction revenue accounted for only 41% of segment revenue in 2022. Transaction revenue benefited from strong debt issuance in 2020 and 2021 while it suffered from a strong decline in debt issuance in 2022 (war in Ukraine, recession fears, increasing rates…) Prior to 2020, they were relatively stable around 50%, which is probably close to a normalized level (which is also in line with the 50% average over the period 2020/2023).

{kind=link}

(Source: Full-Year 2022 Earnings Call)

The data & analytics business

S&P Global has a strong positioning with leading positions in commodity insights, mobility and indices. Even though the competitive landscape is fiercer than in the rating business, these businesses offer many positive attributes. First, they provide strong switching costs since most products are highly integrated into customer workflow. As a result, SPGI enjoys high customer retention (mid-to-high 90% renewal rates) and pricing power. In addition, recurring revenue accounts for most of the revenue, which offers business stability and supports valuation multiples.

Market intelligence

The market intelligence business is composed of four business lines: desktop, data & advisory solutions, enterprise solutions and credit & risk solutions. Desktop distributes financial information and analytics through its Capital IQ platform. Data & advisory solutions offers a broad range of market and ESG data, economic research, country risk research and pricing/valuation services delivered through flexible feed-based or API delivery mechanisms. Enterprise solutions provides a broad range of software and workflow solutions that help customers to manage their front to back operations while offering risk management solutions. Finally, the company sells credit ratings and related research produced by the ratings division under the credit & risk solutions business line.

Recurring revenues account for 96% of the segment revenue, of which 86% comes from subscriptions and 10% from recurring variable revenues (fee based on the number of trades processed, assets under management, or the number of positions valued).

Commodity insights

This segment generates 33% of its revenue from price assessments, 34% from data and insights, 23% from upstream data and insights and 10% from advisory services. Platts is the leading provider of price assessments (15K+ daily price assessments) for nearly every commodity class. In other words, Platts provides benchmarks that are used in most contracts related to commodities and the energy market. For instance, they are the reference for the pricing of futures contracts. The company also provides large datasets and insights for all commodities and energy markets such as demand-supply dynamics, technical information on oil and gas fields (6M+ wells across E&P databases), pipeline and mineral rights documents… Finally, they deliver tailor-made advisory services.

Subscriptions account for ~90% of segment’s revenues while the remaining 10% are composed of non-subscription revenues from conferences and sales-based usage royalties from licensing proprietary price assessments (e.g.: commodity futures).

SPGI's index franchise

S&P Global provides indices spanning a broad range of categories, geographies, investment styles and themes. It includes equity indices (S&P 500, Dow Jones Industrial Average, S&P value and growth, S&P MidCap 400, S&P SmallCap 600, S&P 500 Low Volatility Index, S&P 500 Dividend Aristocrats…), fixed income indices (S&P 500 Bond index, S&P International Corporate Bond Index, S&P U.S. TIPS 0-5 Year Index…), commodities (S&P GSCI, S&P GSCI Industrial Metals…) and ESG indices (S&P Global Water Index, S&P Global Clean Energy Index…) and the VIX index. IHS Markit strengthened the fixed income index franchise with cash bond indices (iBoxx) and CDS indices (iTraxx, CDX…).

Two thirds of revenue are asset-based fees in which the company collects royalties based on the AUM of ETFs, mutual funds and structured products tracking the different indices. It also generates ~15% of revenue from transaction royalties related to the trading volume of on-exchange derivatives (mainly S&P 500 index futures on CME and S&P 500 index and VIX options on CBOE). Finally, ~20% of revenue comes from subscriptions that give clients access to index data (composition, weightings…) and rights to use them in their day-to-day operations.

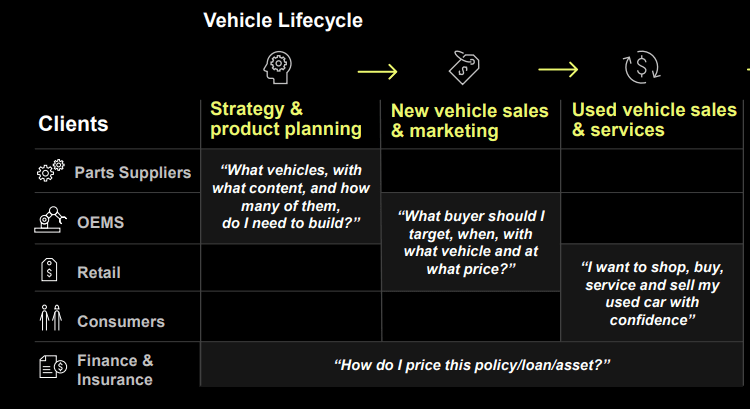

Mobility

This segment has been created following the IHS merger. It provides data and insights to all participants of the automotive value chain such as OEMs, auto suppliers, dealerships and insurance companies... Historical data and forecasts on vehicle production, technology and components, vehicles sales and sales rates, vehicle history reports (30+ billion vehicle history records with CarFax), used car listings are some examples of the vast product offering. Besides, it also sells a range of services to help clients to support their marketing and loyalty programs, vehicle recalls, insurance underwriting and claims management activities. This segment also provides data and analysis on ships operating in international waters and import and export statistics.

{kind=link}

(Source: 2022 Investor day)

The company generates ~80% of revenue through subscriptions while the remaining 20% is related to consulting and advisory services and one-time transactional sales that are tied to underlying business metrics such as OEM marketing spend or safety recall activity.

A well-managed company

Doug Peterson has been at the helm of the company since 2013 and has delivered outstanding results. Revenue grew ~10% CAGR (and mainly organically) between 2013 and 2021 whereas operating margin improved from 28.9% to 50.9%. Invested capital and NOPAT increased by $2.8B and $2.2B, respectively, suggesting an 80% return on incremental capital. As a result, ROIC improved from 40%+ to 65%.

The recent decision to dispose of the Engineering Solutions business strengthened our view that the company is careful regarding its capital allocation decisions. Indeed, this business is not complementary to the legacy SPGI business, has significantly lower margins and lower growth profile (Engineering solutions was included in the Consolidated Markets & Solutions segment of IHS Markit and accounted for the largest part of that business).

{kind=link}

(Source: Annual reports)

{kind=link}

(Source: Annual reports)

In November 2020, while S&P Global announced the IHS Markit merger, it targeted $480 million cost synergies (with 80% achieved by 2023) and $350 million revenue synergies (with 50% achieved in 2024). On March 1, 2022, they upgraded cost synergies from $480 to $600 million. During full-year 2022 results , the company mentioned that it has already realized $276 million cost synergies versus its internal 2022 target of $210/$240 million. As a result, it now expects to achieve 85% (versus 80% initially) of the $600 million run rate cost savings by 2023 (equivalent to $510 million). In Q1 2023 , S&P Global has achieved $552 million run rate synergies (92% of the $600 million target), which suggest potential upside in the cost synergies guidance.

On the revenue side, S&P Global delivered $ 52 million run-rate revenue synergies during the first quarter 2023 whereas it targets $85 million for the full-year 2023 and still expects $350 million by 2026.

Growth

Rating business

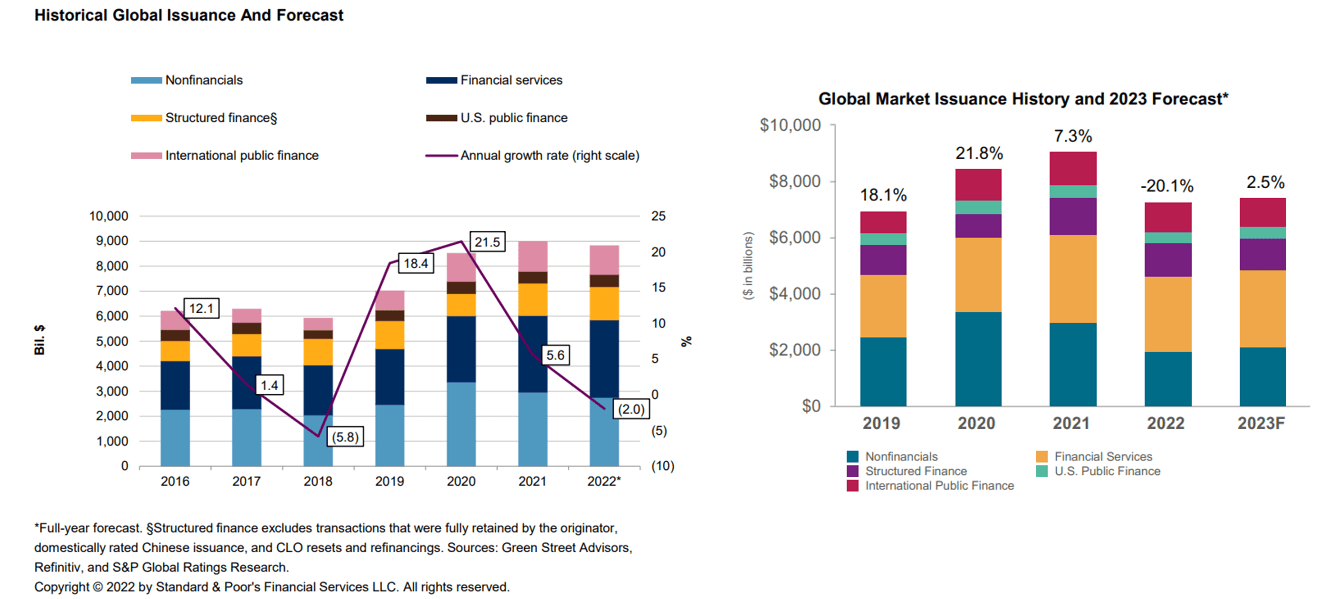

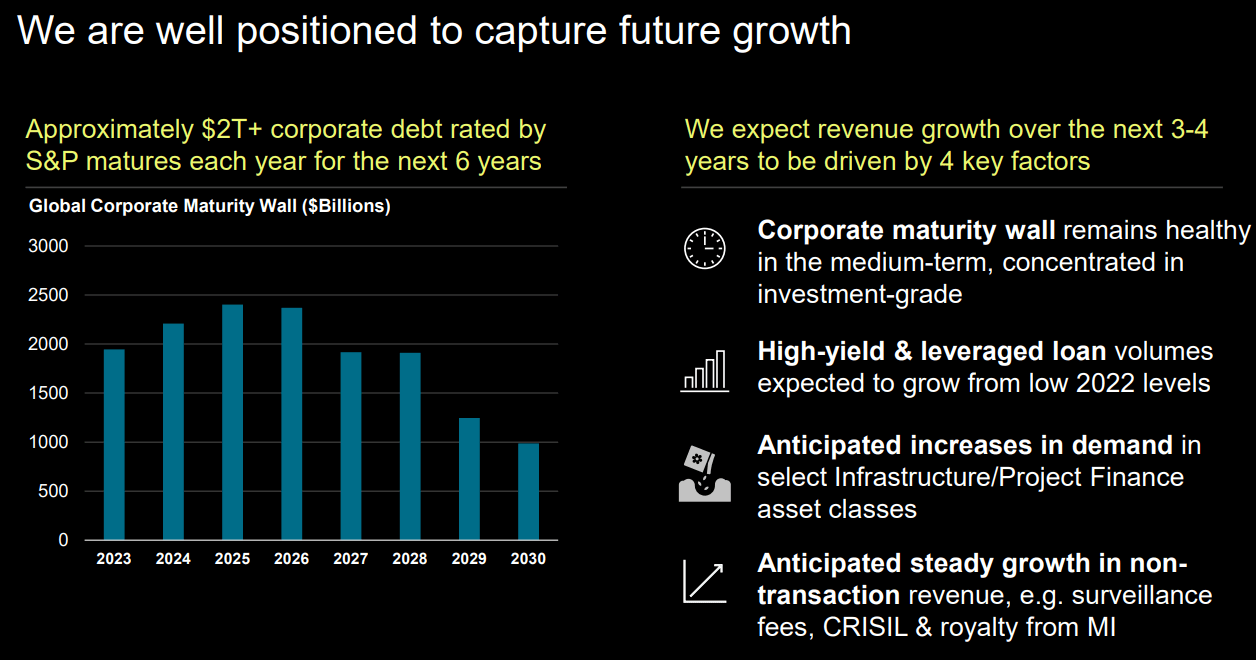

While the debt issuance can be lumpy in the short-term, approximately $2 trillion (2,000 billion) corporate debt rated by S&P matures each year for the next several years, providing a tailwind for refinancing activity (debt refinancing is the main driver of debt market activity).

{kind=link}

(Source: Company presentation)

In addition, debt outstanding grew steadily over the last few decades and should keep growing, driven by economic expansion, inflation, bank disintermediation, the development of private credit markets and more stable interest rates. SPGI continues to expect an average growth rate of 5% in total debt outstanding over the coming years. Finally, most substantial rate hikes are most likely in the rear-view mirror, which should enable global bond issuance to stabilize.

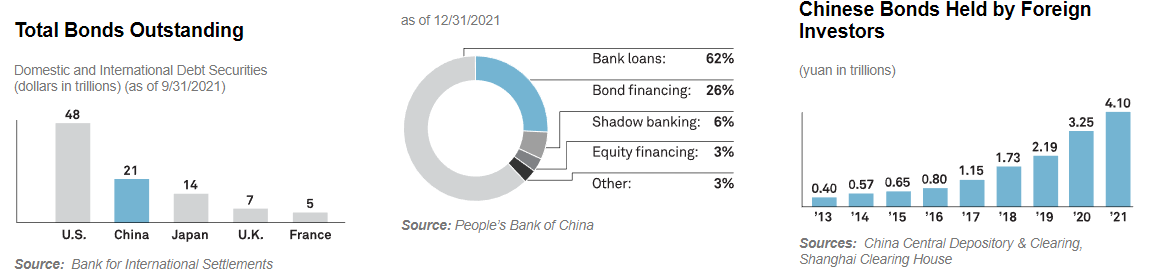

The Chinese market also represents a very large opportunity for SPGI in the long-term, given that it is the second largest market in the world despite being significantly under-penetrated (banks still account for a very large share of funding).

{kind=link}

(Source: investorfactbook.spglobal.com & Bank for International Settlements)

SPGI expects 6%/9% revenue growth over the medium term while Moody’s ( MCO ) guides for a low to mid-single digit revenue growth rate for its rating business.

Data and analytics business

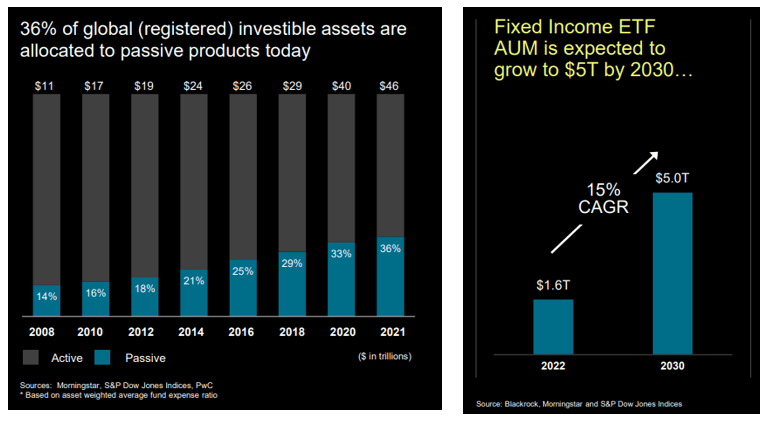

Even though all these businesses will benefit from the secular trend of increasing data consumption and pricing power, they also enjoy different growth drivers that enable to smooth business volatility at the group level. Capital IQ should capture a higher share of the total market as the platform is priced more competitively than peers while offering a strong value proposition. Besides, new product development in growth areas (combination of data, ESG, private markets…) and cross-selling opportunities will also fuel topline growth. According to management, revenue synergies are coming in over a period of three to five years, about 45% cross sell, which is more than the first two years and then 55% coming from new products, which is more year three to five. The indices business will benefit from the continued growth of passive investing, especially in fixed income, and the increasing demand for ESG products. For instance, SPGI developed an electric vehicles metal index with Commodity Insight’s datasets around electric vehicles. According to Blackrock, the AUM of fixed income ETFs are expected to reach $5 trillion by 2030, implying a 15% CAGR.

{kind=link}

(Source: S&P Global Investor Day 2022)

In addition, the volume of index derivatives grew strongly over the last few years, driven by a growing user base, the development of new retail-friendly products such as nano/e-mini products , extended trading hours, and the strong adoption of 0DTE options.

(Source: S&P Global Investor Day 2022)

Valuation

During the last four quarters of IHS Markit as a standalone company, the combined entity generated $4.7 billion FCF. At the time of the acquisition, SPGI guides for ~$5 billion FCF by 2023. This assumption seems realistic given that the combination of both businesses generated $4.7 billion and that the company plans to realize cost and revenue synergies. Nevertheless, this guidance has been downgraded in 2022, mainly because of a strong deterioration in the level of debt issuance. This activity is cyclical and will most likely recover. Therefore, $5 billion FCF will be reached soon (consensus expects to be there in 2024).

(Source: Author and quarterly financial results)

SPGI guides for ~7-9% organic annual revenue growth in FY25/26, which is considered as a normalized growth rate under normal circumstances. On top of that, operating margin should expand given that the data and analytics business offers high incremental margins. Finally, the company will return at least 85% of net income to shareholders (mainly through share repurchases) because the model is asset-light.

{kind=link}

(Source: Annual reports and author)

{kind=link}

(Source: Annual reports and author)

As a result, SPGI is probably trading around 4% FCF yield (based on a $5B FCF and a $126.8B market cap.) which is not cheap. However, it is not expensive either for a high-quality company that can compound earnings at a double-digit rate for the foreseeable future. We own the company as we believe it is a structural winner but we will be more inclined to increase our exposure when valuations become more attractive.

For further details see:

S&P Global: A Collection Of High-Quality Assets With Strong Moats And Long-Term Compounding Opportunities