SPGI - S&P Global: Reiterate Buy Rating On Outperformance

2023-05-26 09:52:13 ET

Summary

- SPGI Ratings segment performed better than expected, with a modest 5% revenue drop compared to Moody's 11%.

- SPGI is making notable progress in achieving cost synergies from the merger with IHS Markit. That said, revenue synergies are picking up slowly.

- The Market Intelligence segment faced difficulties in the current uncertain banking industry.

Summary

S&P Global ( SPGI ) had a successful 1Q23 , in my opinion, with revenue, EBITDA margins, and EPS all exceeding consensus estimates. This was largely due to the Ratings business, which did much better than expected. The Ratings segment revenue dropped by only 5%, a significant improvement from the previous quarter and 600 bps better than Moody's ( MCO ) Investors Service segment's 11% revenue drop. Considering SPGI's increased refinancing and M&A deal flow, as well as the fact that last year was an easy comparison, I remain optimistic that ratings will improve in the coming quarters. Things would be even better for SPGI if interest rates dropped in 2H23. My thesis that SPGI is among the best businesses in the world remains unchanged. I reiterate my Buy rating .

Ratings

Although the Ratings segment fell by 5%, it significantly outperformed both consensus estimates and MCO this quarter. Within this, Transactional ratings revenue, which accounted for just under half of Ratings revenue, dropped by a relatively modest 6% in 1Q23. SPGI's strong execution and outperformance in Structured products helped contribute to this impressive result, I believe, as revenue dropped by only 3% compared to MCO's 31%. The rest of SPGI's segment revenue comes from sources other than transactions, and those revenues fell by 4%. This revenue stream is weaker in nature due to its cyclicality; thus, a decline in the low single digits was much better than I expected. I think the market is already way past the weak IR environment, judging by the valuation and share price movement, both of which have recovered over the past 2 months. The focus here is 2H23 and beyond, where I expect to see an improvement in full year transaction revenues as I think the market will see a recovery in M&A deals (valuation get cheaper), and more refinancing activities (as rates stay flattish or down). My view is also reinforced with management confidence that on the transactional side, where billed issuance guidance for FY23 has been increased to 3-7% y/y from an initial guide of 2-6% y/y.

Synergies

Additionally notable is the fact that SPGI is pushing ahead on expected synergies from the merger with IHS Markit . The run-rate cost synergies reached $552 million in 1Q23, which is almost 90% of the total cost savings (FY23 target of $600 million) planned, demonstrating incredible focus from management on delivering the expected synergies, especially on the cost front. There is a high probability that synergies will be realized in 2Q23 at this rate. On the revenue side, however, things are still picking up rather slowly, a trend I attribute in part to the sluggish macro. In comparison to the $350 million goal set for FY26, run-rate revenue synergies have now reached $52 million. I don't think the slow pace of realizing run-rate revenue synergies is a weakness. In particular, when it is being driven primarily by cross-selling products. I expect SPGI to fully realize its cost synergies ahead of its timeline, and revenue synergies to go into accelerated mode when the macro environment turned for the better.

Negatives

The Market Intelligence segment has not performed as well as it should this quarter, and I expect that to continue as the market applies more pressure. EBIT totaled $343 million on revenues just over $1 billion in 1Q23. Given the current climate of uncertainty in the banking industry, management has the most pessimistic projections for both revenue and EBIT. Customers are obviously being more cautious in light of the volatile macro, which has resulted in a slightly lengthened sales cycle, in my opinion. Nonetheless, it was comforting to learn that the vast majority of deals are still turning into revenue; this indicates that demand is merely being delayed rather than disappearing altogether.

Guidance

My focus this quarter has been on whether or not management changes its outlook for FY23. Mid-single digit revenue growth is still anticipated, as is an adjusted EBIT margin of 45.5% to 46.5% and adjusted EPS of $12.35 to $12.55. In what appears to be a simple restatement of previous guidance, but I believe they are implicitly increasing it. The thing to note here is that SPGI sale of its Engineering Solutions unit is now expected to close in early May rather than June. So if we account for that 1-month difference of contribution loss, but guidance still remains the same, we can infer that management is guiding for 1 more month of performance contribution from other segments.

Valuation

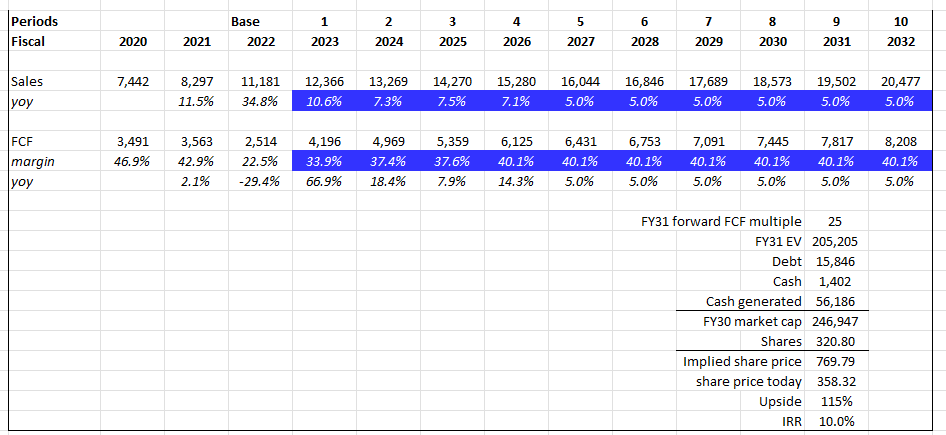

I have updated my model to reflect the latest numbers, consensus estimates over the next 5 years, and also the IRR one should expect today. Following my initiation post, which used a DCF to value SPGI, I believe SPGI continues to offer at very stable 10% IRR over the next 10 years. The big difference between my updated model vs. previously is that I expect SPGI to trade at a FCF multiple of 25x. This translates to a 4% FCF yield (1/25x), which I think is fair given that rates are unlikely to revert back to 0%, and SPGI should trade at FCF yield that is higher than the prevailing interest rates (as it has higher risk and volatility, compared to treasury bills).

{kind=link}

Risks

The big risk I am seeing with SPGI, at least in the near-term, is that growth is contingent on recovery in refinancing and M&A activities. While I am positive on this, the risk of the economy flipping into a very bad recession is not something that is off the table yet. Especially with the debt ceiling narrative floating in the market, if the US does default on its debt, I think it will be a major disaster for the economy.

Conclusion

SPGI performance in 1Q23 was commendable, surpassing consensus estimates and demonstrating strength in its Ratings business. Additionally, SPGI's progress in achieving cost synergies from the IHS Markit merger is impressive, with run-rate cost savings reaching almost 90% of the target. While revenue synergies are picking up slowly, the focus on cross-selling products bodes well for future growth. However, challenges persist in the Market Intelligence segment due to cautious customer behavior in the uncertain banking industry. Nonetheless, management maintains a positive outlook for FY23, anticipating mid-single digit revenue growth. Overall, my belief in SPGI as an excellent investment opportunity remains unchanged, and I reiterate my Buy rating.

For further details see:

S&P Global: Reiterate Buy Rating On Outperformance