FDMT - Sangamo Therapeutics: Strong Fabry Data Puts Them In The Lead

Summary

- Shares have fallen by 30% so far in 2022.

- Durability and safety for the Fabry disease gene therapy program continues to look best-in-class and enrollment should accelerate due to investigator enthusiasm.

- Excitement is palpable for CAR-Treg programs as renal transplant data could open the door to multiple expansion indications.

- Pfizer hemophilia A pivotal study readout by late 2023 to early 2024, along with progress for Fabry into pivotal study, could also positively impact valuation and sentiment here.

- SGMO is a Buy, but only appropriate for investors with a 3-to-5 year timeframe or longer. Key risks include near term dilution and competition in areas like Fabry or hemophilia A.

Shares of emerging gene therapy pioneer Sangamo Therapeutics ( SGMO ) have lost over half their value during the past three years. So far in 2022, the stock sports a YTD loss of nearly 30%.

I decided to revisit this name after recent data for its first-generation Fabry disease program showed best-in-class efficacy and potential for achieving a functional cure (5 of 11 patients off of enzyme replacement therapy or ERT). What also struck me at first glance was sheer breadth of partnerships and applications of its zinc finger engineering across cell therapy via Kite/Gilead, neurology and neurodegenerative diseases (Biogen, Pfizer and Takeda).

Shareholders have certainly been long-suffering, but I look forward to revisiting this story to see if it's likely to attain critical momentum in the near to medium term.

Chart

{kind=link}

FinViz

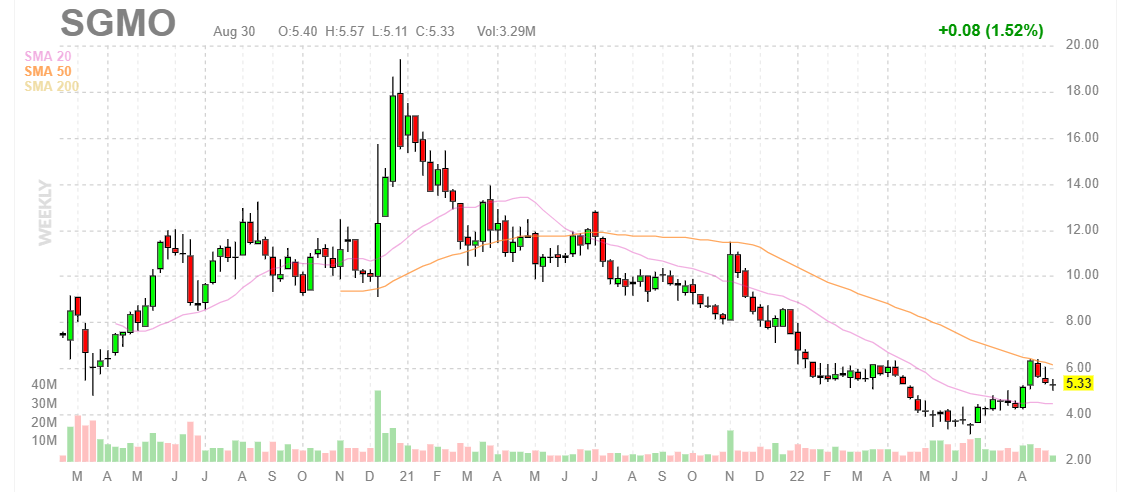

Figure 1: SGMO weekly chart (Source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the weekly chart above, we can see shares hit a high of $18 toward the end of 2020 after partner Pfizer announced promising data for gene therapy candidate giroctocogene fitelparvovec (SB-525 or PF-07055480) in hemophilia A, leaving them on track for pivotal readout in 2022 and potential to get a drug across the regulatory finish line if all goes well. From there, shares experienced a sickening decline to low single digits and bottomed this summer around the $4 level. The recent rebound appears related to the Fabry disease phase 1/2 readout, but I still need to dig deeper to determine whether a continuation and rerating higher is warranted. That said, for readers with a long-term timeframe interested in this story, I imagine a logical strategy would be to acquire dips in the near term ahead of progress for sickle cell disease program into phase 3 and Pfizer's hemophilia A pivotal readout in late 2023 to early 2024.

Overview

Founded in 1995 with headquarters in California (431 employees), Sangamo Therapeutics currently sports enterprise value of ~$500M and Q2 cash position of $363M providing them operational runway for just one year.

While presentation is a bit dated (two months ago), Jefferies webcast is helpful in getting a better idea of corporate overview:

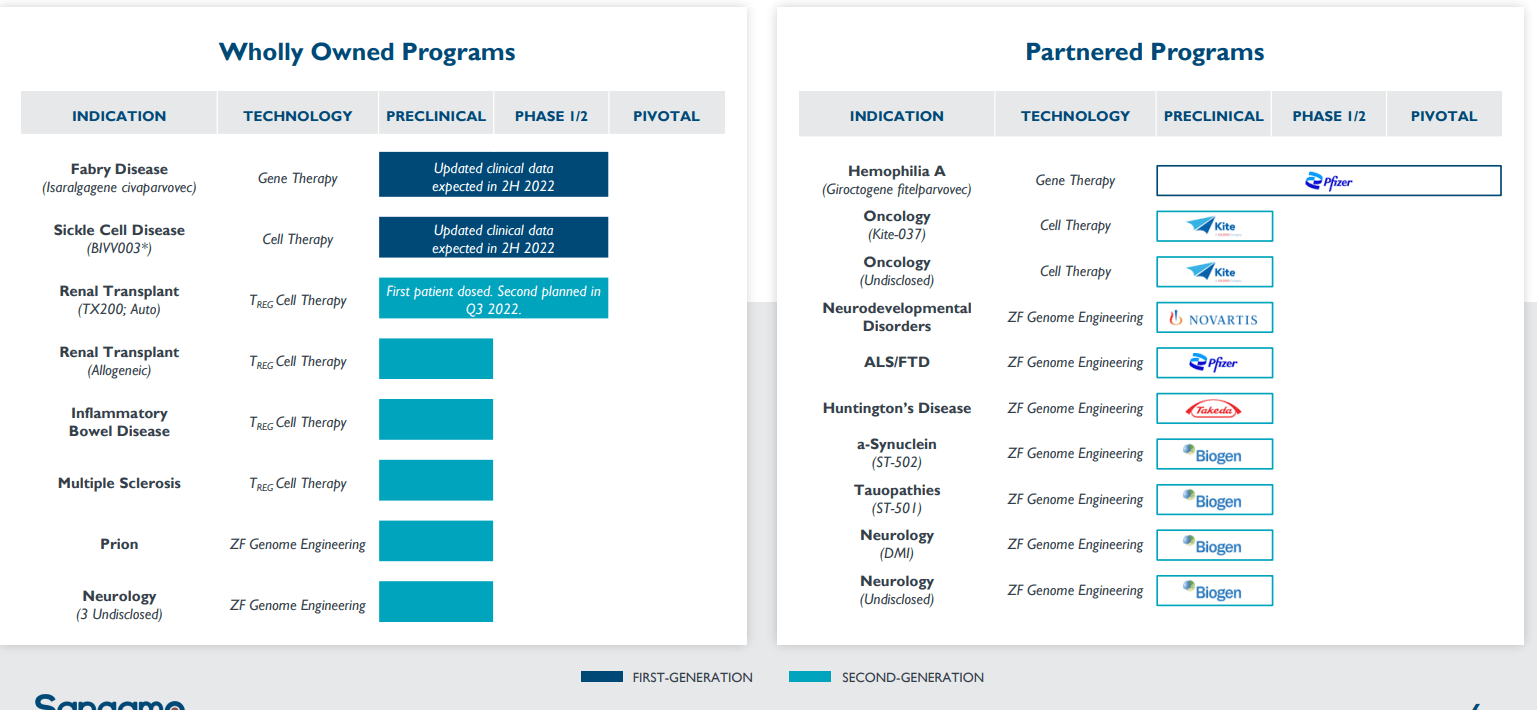

- CEO & President Sandy Macrae starts by describing Sangamo as having three clinical stage assets (in phase 3 or about to go into phase 3 in the coming year). Fabry disease is wholly-owned and the leading candidate for this indication. They are in phase 3 with Pfizer for hemophilia A and completing phase 1/2 study in sickle cell (take into phase 3 next year). Additionally, they've dosed the first CAR-Treg patient in renal transplant. Behind that, they have a portfolio of Treg products and CNS capability with their Zinc Finger platform, underpinned by wholly owned manufacturing in the US and France. Lastly, platform and editing capability is second to none per management (a grandiose claim).

{kind=link}

Corporate Slides

Figure 2: Pipeline (Source: corporate presentation )

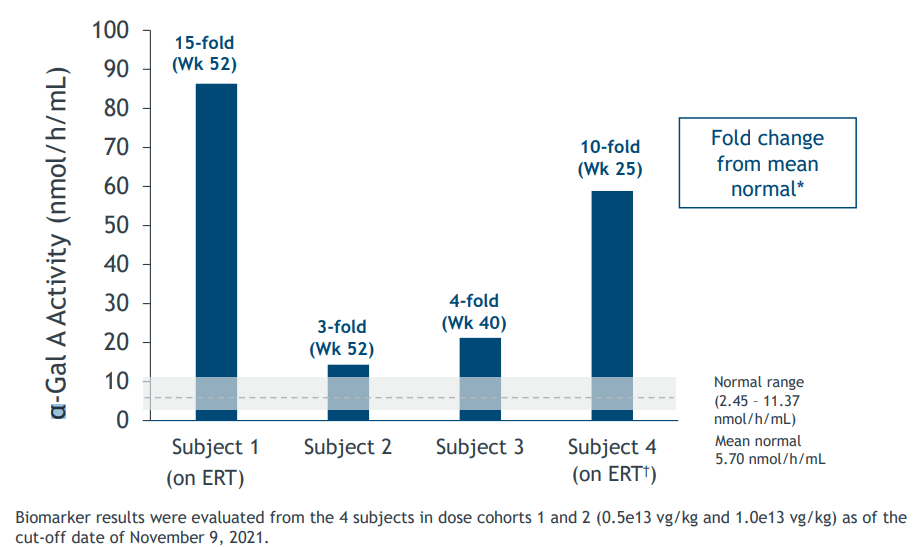

- Starting with Fabry, kidney biopsy data is not expected until early 2023. At the time of this presentation, they'd dosed nine patients including at top dose of 0.5e13 vg/kg (they are not going to escalate further). They only did biopsies on patients that are naive or pseudo-naive because patients who've got ERT the results would be conflicted. Cohort 3 both patients were on ERT, so the first two patients to have kidney biopsy were in Cohort 4 (data won't be available until start of 2023). Overwhelmingly, the story from how patients feel, ?-GAL activity levels and safety is very promising. They've shown 2-to-15-fold increase above normal for ?-GAL in these patients and no adverse events of any significance. Patients are feeling better and say they are sweating again (limits Fabry patients as to what they can do and where they can go). To the physician, it means the ?-GAL is getting into the tissues and resolving some of the tissue damage from Fabry disease (good indicator). Anecdotal stories of patients feeling better, cardiac measurements on MRI stabilizing and in some cases are improved. Competitor Avrobio ( AVRO ) was able to show kidney clearance with much lower levels than Sangamo is showing. At the time, they'd removed three patients from enzyme replacement therapy and more are likely to follow.

{kind=link}

Corporate Slides

Figure 3: ST-920 efficacy data in Fabry disease (Source: corporate presentation )

- As for Cohort 4 (high dose), safety has been unremarkable and previous studies have shown this to be a safe dose for their capsid. Only 2000 patients have been tested with gene therapy across all capsids all programs, so it's still difficult for animal models to translate to humans. That said, animal models showed higher dose is better (higher clearance of lyso-Gb 3 from normal tissue). Typically, patients have 5 to 7 infusions of ERT every second week (not the pharmacokinetic way they should be getting the enzyme). It's much better to get it as a chronic infusion from gene therapy. So far, patients are showing benefit out to 15 to 18 months, steadiness observed so far is encouraging and all data points to being a long-term therapy for patients. Meeting with FDA went well, they understand Fabry and gave great advice for the phase 3 design, but management is keeping information to themselves for competitive reasons. They have not given any patients prophylactic steroids in the time of Covid (unless necessary, which has not occurred so far).

- As for competition, 4D Molecular Therapeutics' ( FDMT ) study is enrolling at similar pace and Freeline Therapeutics ( FRLN ) is steadily making progress as well. Sangamo's CEO can't comment on investigator enthusiasm for others', but notes that after prior data for ST-920 an overwhelming number of patients have enquired about the study (several women coming on). Recruitment is quite different after you have good results, it is a big decision as patients only have one shot at getting a gene therapy. Competitors use different capsids, 4D believes you have to put the capsid in the heart (no indication this is true from animal studies). Freeline found going into the heart gives you the risk of myocarditis (capsid-related as opposed to ?-GAL). Management feels that the established safety record of AAV6 gives them a solid workhorse for delivery. Every time you go into a new capsid you run the risk of something new happening (myocarditis for Freeline, hemolytic uremic syndrome for 4D, etc). Safety is the most important thing.

- For hemophilia A, Pfizer announced a clinical hold on phase 3 lifted and resuming in Q3 (one DVT competitor event). Pfizer is confident. The other 50% of patients to complete the study are already known. Most unusually, patients are still getting benefit despite clinical hold (not losing data as with other studies). They are accumulating months going into years of data for these patients which will help for the long run. BioMarin Pharmaceuticals ( BMRN ) is shooting for a gene therapy approval for this indication and Roctavian recently received conditional approval in the EU with €1.5 net price tag.

- For sickle cell disease, transition from Sanofi (SNY) is nearly complete. They have dosed a fifth patient, and will dose patients 6 and 7 in Q3, look at data from the new process and then take this forward. Data will be shared at the start of next year, believe it is bite-sized so they can take it forward solo assuming data warrants.

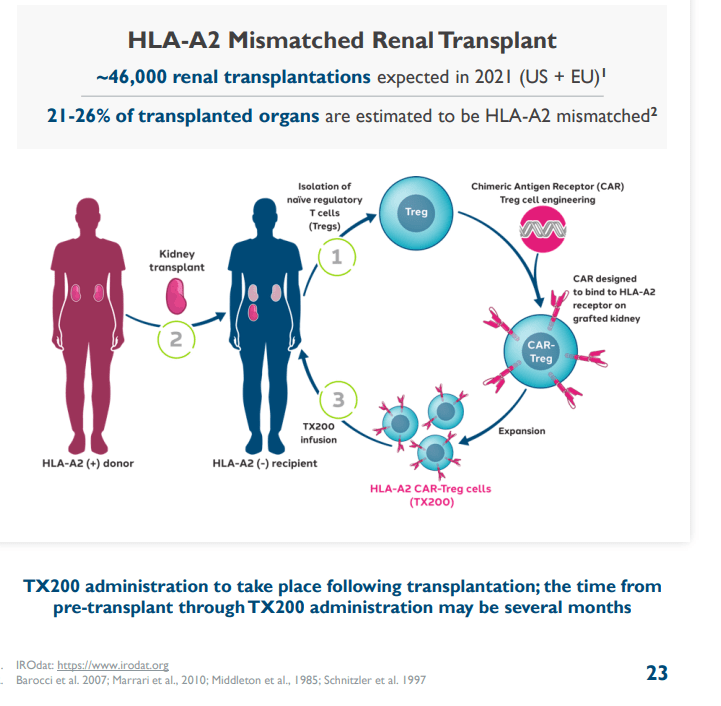

- As for CAR-Treg program and platform, first patient dosed is doing well. This is the first time anyone has taken a Treg, put a CAR on it and put back in the patient. They will share more results into the new year, patient will be biopsied as part of normal renal transplant. The next patient will be dosed this year and potentially complete the cohort this year. They have a whole portfolio of CAR-Treg type programs behind this that are all learning from this program and benefitting from safety learnings. Excitement is palpable here. Data could show this is a new way to treat autoimmune disease.

{kind=link}

Corporate Slides

Figure 4: Renal transplant opportunity and value proposition (Source: corporate presentation )

- As for competitors in this space, there are now 15 CAR-Treg companies (the field is waking up to them but Sangamo remains in the lead). Sangamo's CSO wrote some of the fundamental work on Tregs, also the company has editing capabilities in house which the others don't have, GMP manufacturing and experience (advantage is having all this in house and applied to this problem). Renal transplant study is first with autologous, but they have an allogeneic program to follow. They have another group based in California taking iPSCs and changing them into Tregs (will allow them to pick a single clone, make sure it has all the edits they want, decrease cost of goods and increase accessibility to as many patients as possible).

Let's move on to recent data and how it has affected the bull thesis here.

August 30th Fabry Disease Update

Preliminary results from the phase 1/2 STAAR study of isaralgagene civaparvovec (ST-920) continued to be encouraging, perhaps most importantly showing the gene therapy candidate's desirable safety profile with no treatment-related adverse events above Grade 1. The five longest treated patients continued to exhibit elevated alpha-galactosidase A (?-Gal A) activity, sustained up to 15 months as of the last date of measurement. The sixth patient exhibited elevated ?-Gal A activity to within normal range at two weeks post dosing.

{kind=link}

Fabry Poster

Figure 5: Fabry data update shows maintained elevation of ?-GAL activity levels (Source: Fabry poster )

Three patients anecdotally reported improvements in symptoms including ability to sweat, a primary and common Fabry disease symptom. No progression of Fabry cardiomyopathy was observed in those patients who presented with signs of cardiomyopathy on cardiac MRI at baseline. Interestingly enough, since the cutoff date five more patients were dosed bringing total to eleven patients dosed to date (one more in Cohort 3, two patients in Cohort 4 at the 5e13 vg/kg dose level and the first two patients in the expansion phase at the 5e13 vg/kg dose level).

Of the five treated patients in dose escalation, an additional four have been withdrawn from ERT since the cutoff date (beginning to sound like a cure to me). The company expects to provide more data 2H '22 and is planning a potential phase 3 study.

As for market opportunity for this indication, consider that Sanofi's Fabrazyme ((ERT)) did around $223M in Q4 2021 sales (growing 9%) and thus approaching the $1 billion a year mark. Consider that lifetime costs of ERT starting in symptomatic stage are estimated to be between $13M to $14M (per additional year free of end-organ damage and extra costs related to quality of life).

Other Information

For the second quarter of 2022 , the company reported cash and equivalents of $363M as compared to total operating expenses of $75M. Research and development expenses came in flat at $60M, while G&A decreased slightly to $15M. Management is guiding for 2022 total non-GAAP operating expenses of $280M to $310M, so the company appears to have just over one year in operational runway (I would expect a secondary offering in the next quarter or two). Accumulated deficit since inception is ~$1 billion, so it's clear management needs to get a better handle on cash burn and use of resources.

As for the conference call , while BIVV003/SAR445136 for the treatment of sickle cell disease was returned by Sanofi, the data continues to be promising with three of four patients dosed with previous manufacturing process continuing to be free of vaso-occlusive events. During this quarter, the patient who had achieved the lowest level of fetal hemoglobin post infusion experienced the second vaso-occlusive crisis but has now fully recovered. Keep in mind the company is now using an improved methods manufacturing process which has been shown to increase the number of long-term progenitor cells in the final product (could result in superior outcomes to those seen previously).

As for TX200 CAR-Tregs cell therapy candidate for the prevention of immune mediated rejection in HLA-A2 mismatch kidney transplantation from a living donor, first patient dosed continues to show drug candidate is well tolerated four months post infusion with no treatment related adverse events. A second patient will be dosed in Q3 and a final patient by the end of the year, then disclose meaningful data package when able. The European Commission granted Orphan Medicinal Product Designation to TX200 and keep in mind that positive POC data here could have an outsized impact on valuation considering there's an active preclinical pipeline with multiple candidates in development to treat inflammatory bowel disease and multiple sclerosis alongside efforts to progress the allogeneic cell therapy platform.

As noted previously, regarding the Phase III of AFFINE trial evaluating giroctocogene fitelparvovec for hemophilia A, Pfizer advised the company that it continues to expect to resume dosing this quarter and thus is guiding for pivotal data readout toward the end of 2023 or in early 2024.

As for prior financings, April 2019 secondary offering took place at $11.50 per share (representing a double from current levels).

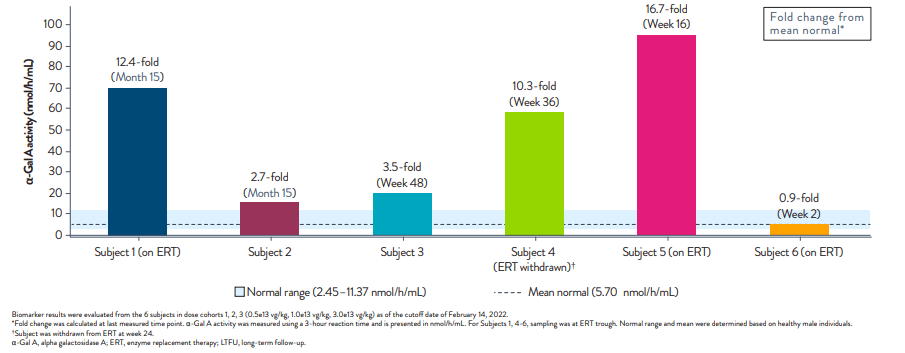

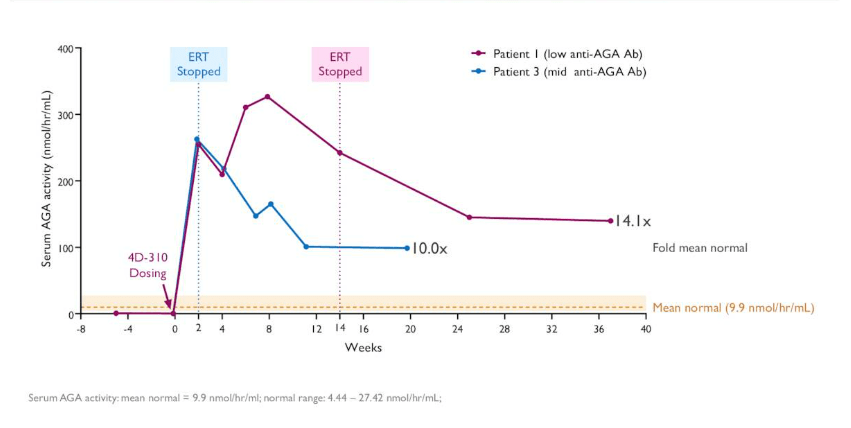

Moving on to competition in Fabry disease (most relevant as it's their lead wholly-owned candidate), 4D Molecular Therapeutics' 4D-310 tries to achieve clinical differentiation via dual mechanism of action to target organs including heart and high serum AGA. So far, the gene therapy candidate has shown no evidence of cardiac effects (ECG, cMRI, echocardiography) and likewise stable high levels of AGA were observed following discontinuation of ERT (all three patients treated so far achieved normal or significantly above normal AGA activity level).

{kind=link}

Corporate Slides

Figure 6: Fabry data for FDMT shows high level AGA activity after discontinuation of ERT (Source: FDMT slides )

As for institutional investors of note, I see more in the way of generalist biotech investors here versus specialty funds (BlackRock increasing its stake to 8%, Vanguard increasing its stake to over 6%).

As for insiders, EVP and Chief Commercial Officer David McClung owns 175,000 shares. Chief Scientific Officer Jason Fontenot owns 103,000 shares.

Moving on to relevant leadership experience, CEO and President Sandy Macrae served prior as Global Medical Officer of Takeda Pharmaceuticals. EVP Chief Operating Officer Mark McClung served prior as General Manager of Global Commercial Oncology at Amgen. Chief Scientific Officer Jason Fontenot served prior as Head of Exploratory Research at Juno Therapeutics (bought out by Celgene for $9 billion).

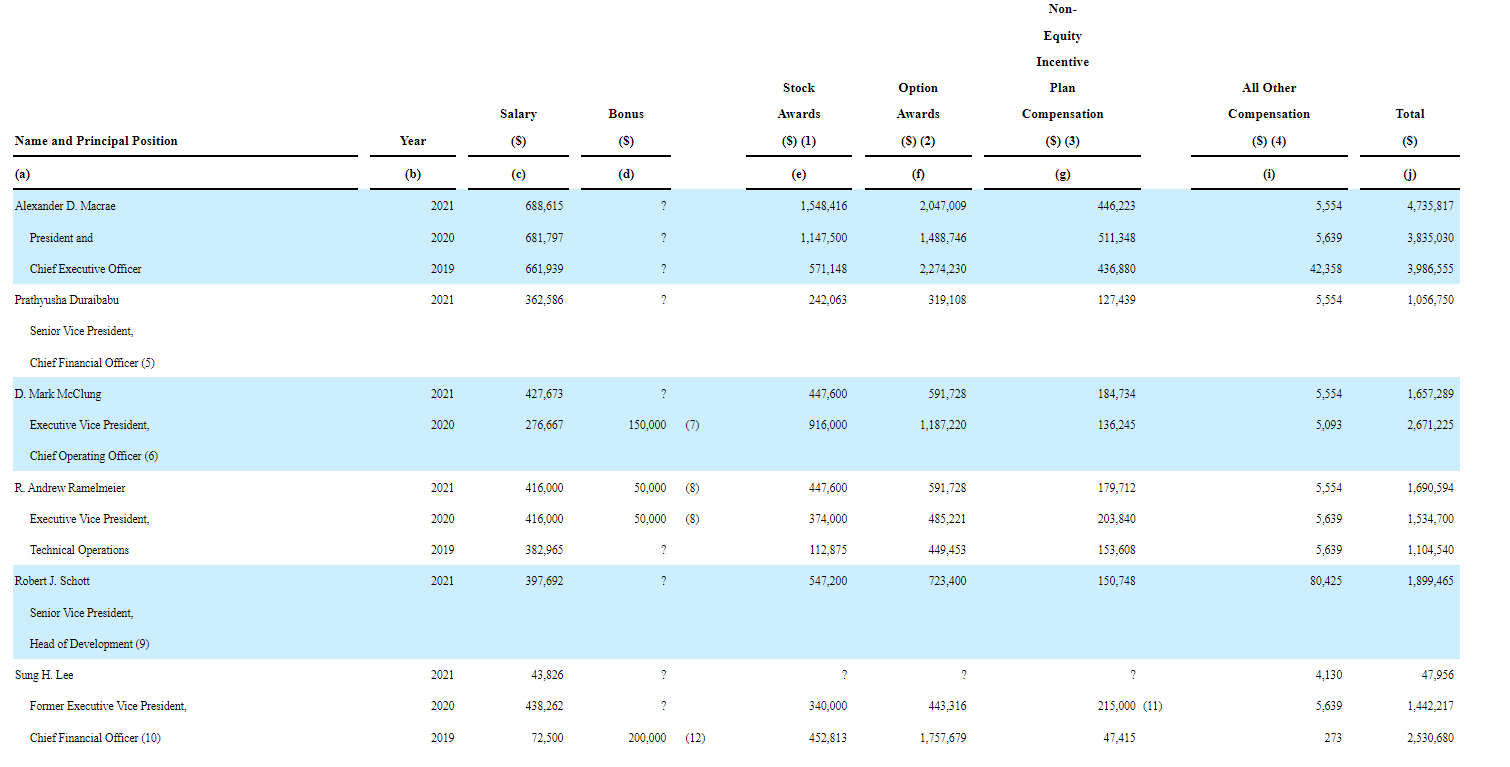

As for executive compensation, cash portion of salaries including nearly $700k for the CEO is too high considering what they should be doing to reduce burn and manage costs as much as possible. On the other hand, levels of stock and options awards are more than reasonable.

{kind=link}

Proxy Filing

Figure 7: Executive Compensation Table (Source: FDMT slides )

The important thing is to avoid companies where the management team is clearly in it for self-enrichment instead of creating value for shareholders, and looking at compensation is one of several indicators in that regard.

As for additional nuggets of interest, here are a few from Guggenheim Treg Conference :

- Chief Scientific Officer Jason Fontenot highlights the promise of regulatory T cell-based therapies. Wealth of preclinical and translational data show they play a fundamental role in preventing and controlling autoimmune disease, so there is a real opportunity to transform treatment from immunosuppressive, systemic therapies (ie in MS and RA) to a one-and-done targeted, immunomodulatory treatment with potential to be a long term solution to these diseases. Excitement around low dose IL-2 is because it's the leading edge of therapies that are targeted at regulatory T cells and looking at their ability to modulate pathology in many of these diseases. There is opportunity with IL-2, but there are downsides such as being largely systemic as opposed to targeted approach.

- TX200 is the lead program, starting with a naive Treg that's isolated from the patient who will receive the transplant (autologous). They engineer them to express chimeric antigen receptor ( CAR ) specific for HLA class one molecule A2 and treating patients that are HLA A2 negative and receiving an A2 positive kidney. Three months after receiving transplant, they will be infused with those CAR Tregs. They have 20+ years of data showing these cells have potent immunoregulatory properties (should be phenotypically stable and durable).

- Again, this is the first time anyone has given a CAR Treg, so has to be done intentionally and carefully. As for market opportunity, 20% of renal transplants are HLA A2 mismatched. For liver transplants, you don't HLA match them. Additionally, they are developing an allogeneic platform to expand this more easily to more patients.

- For MS, they have two CARs selected for different antigens and two for Crohn's as well. Three disease states is sufficient for now in a company of this size. These are long term inflammatory diseases with expensive IV treatments available for them. Patients are looking for an immunological answer to the auto-immunity they exhibit. Perhaps dosing once or infrequently with CAR Tregs they could retolerize to what's causing their disease (need to know the localizing antigen).

As for other useful nuggets from the 10-K filing (you should always scan these in your due diligence as many companies like to sweep undesirable elements under the rug), one aspect of the story it's easy to miss is just how extensive the company's partnerships are for its technology platform. The Novartis July 2020 agreement centers on developing gene regulatory therapies for three neurodevelopmental disorders (Sangamo received $75M upfront and is eligible for up to $720M in milestones plus high single digit to sub-teen double digit royalties on sales). A February 2020 agreement with Biogen centers on developing gene regulation therapies for treatment of neurological diseases (Biogen bought $225M worth of common shares at $9.21 price point, also paid $125M upfront and Sangamo is eligible for up to $2.4B in milestones plus high single digit to sub-teen royalties). A Kite Pharma (Gilead Sciences company) agreement was inked back in 2018 to design zinc finger nucleases and viral vectors to disrupt and insert certain genes in T cells and natural killer cells including insertion of genes that encode CARs, TCRs and NKRs to mutually agreed upon targets. For this, Sangamo received $150M upfront and is eligible for up to $3B in milestones plus tiered royalties in single digits on annual worldwide net sales.

Final Thoughts

To conclude, at the current $500M enterprise value, the science with this platform technology play in the genome engineering space is quite fascinating and multiple pipeline candidates contribute to this "sum of the parts" story. As multiple programs approach key milestones in the years ahead, it looks like long term investors have a good rationale for maintaining exposure here (hemophilia A phase 3 readout, Fabry moving to phase 3, CAR Treg programs moving forward with POC data, etc). While perhaps incremental in nature, Pfizer-partnered hemophilia A program has best-in-class potential and could generate $1.5B or more in peak sales in a blue sky scenario (keep in mind Sangamo stands to receive 20% royalties so that would equate to $300M annually at peak). Conversely, in Fabry they are facing stiff competition with other companies including Freeline Therapeutics' FLT190 and 4DMolecular's 4D-310 (but remains in the lead so far). Also, I'm not sure there's enough clinical momentum to maintain my interest here in the near term (a good opportunity at the moment, but perhaps not great or overly compelling). I consider the CAR Treg aspect of story to offer significant optionality for investors, as this would represent an entirely new way to treat autoimmune diseases and eventually they will have allogeneic to follow.

For readers who are interested in the story and have done their due diligence, SGMO is a Buy and appropriate only for long term investors with a 3-5 year timeframe at the least. A potential strategy could be to patiently accumulate dips in coming quarters as we await progress for key programs including hemophilia closer to pivotal readout, Fabry moving into phase 3 and CAR Treg program reporting initial data.

From an ROTY perspective (focus on next 12 months), I have other ideas on radar including of the platform technology nature that provide us a more efficient pathway to market and more in the way of near-term upside drivers. Thus, I think the appropriate move for me here is to stay on the sidelines and revisit perhaps in the middle of next year.

Key risks include dilution in the next quarter or two (my estimation as I believe it's better for companies to raise sooner rather than later) and fierce competition in certain areas they are pursuing (BioMarin in hemophilia A, Freeline and 4D Molecular in Fabry, etc). Disappointing data (particularly pivotal for hemophilia A or longer term follow up for Fabry) as well as possible setbacks or delays in the clinic would also weigh on share price.

Author's Note: I greatly appreciate you taking the time to read my work and hope you found it useful. I look forward to your thoughts in the Comments section below.

For further details see:

Sangamo Therapeutics: Strong Fabry Data Puts Them In The Lead