MSOS - Schwazze: A Tiny Titan And Best Of Breed Operator In The Cannabis Space

Summary

- Management is delivering on its acquisition strategy, bringing rolled-up brands to better sales and profitability, despite a general malaise in the sector.

- The company now sports a P/S of .42 and a P/B of .43.

- Its NTM EV/EBITDA of 2.61x is the best in the industry.

- 2023 might be the pivot year.

The cannabis industry is in a cyclical downtown, a purgatorial lull due to consumer weakness, oversupply, and general competition. Investors have stepped away from the once hyped sector and not returned.

Aurora Cannabis ( ACB ) was at $119 in March 2019, but is now trading at 91 cents . AdvisorShares Pure US Cannabis ETF ( MSOS ) is down 72% over a one year period; the themed ETF did not see any of January's risk-on bounce.

Of course, every economic sector sees a secular downtown from time to time, and every investor knows that there is a short period of so-called "maximum pessimism" amid every downdraft which is precisely the right moment to buy those best-of-breed operators that will survive (and later thrive).

The trick is to recognize the signal in the noise: to focus on under-the-hood valuations that say something deep about management execution. Yes, certain companies you buy for management. Schwazze ( OTCQX:SHWZ ) is one of them.

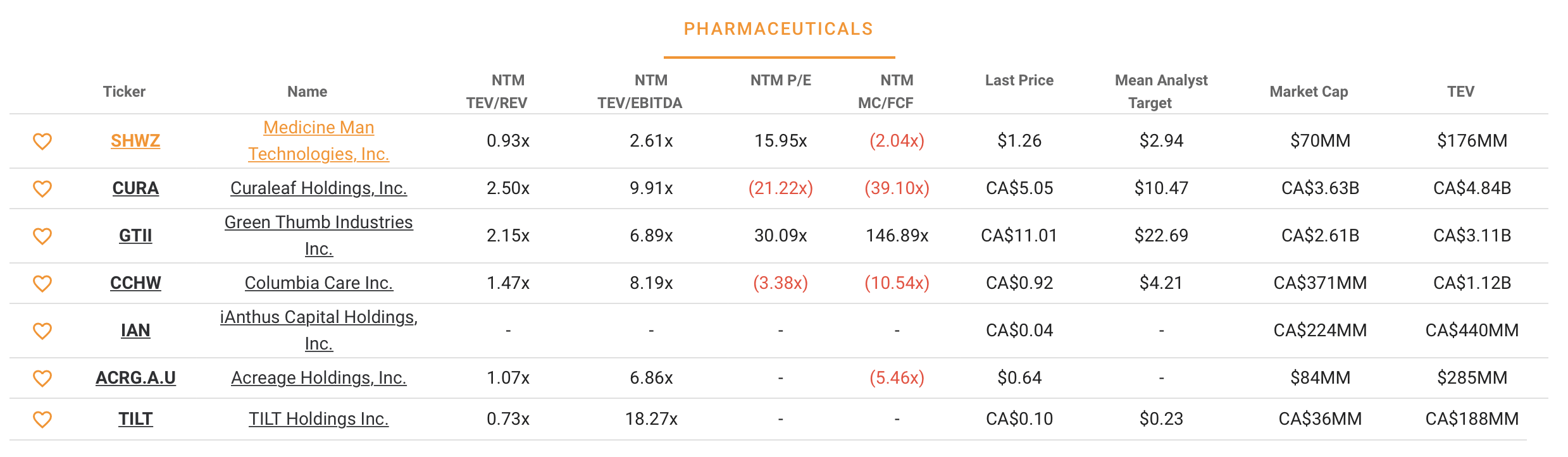

Despite only being down over 20% over a one year period, the company's NTM (next twelve month) EV/EBITDA of 2.61x is the best in the industry.

{kind=link}

SHWZ and competitors --NTM EV/EBITDA (TIKR)

It suggests how strong the stock ticker could swing back as the sector sees less headwinds. As a vertically-integrated MSO with able management, Schwazze is well-positioned to take advantage of a growth industry that is about to be hit with the perdition of a “consolidation” phase.

The Back Story

Schwazze has a long history in the cannabis space, first incorporated in 2014 and going public in 2016 as Medicine Man Technologies. The company’s fortunes changed dramatically in 2020, however, when non-Colorado entities were allowed to participate in the state's cannabis industry and Dye Capital took over.

Justin Dye, head of Dye Capital, looked at the nascent cannabis industry and saw an industry ripe for the same kind of operational discipline he pursued in another inefficient retail segment, the grocery business. He was part of the team that famously transformed Albertsons ( ACI ), the national chain, helping to raise sales from $10 billion to $59 billion and essentially streamlining a once struggling under-performer for its successful IPO.

Looking for a new challenge, Dye clearly sees similar opportunities in the cannabis space. Consolidation and operational expertise will do wonders for the inefficient and fragmented pot sector.

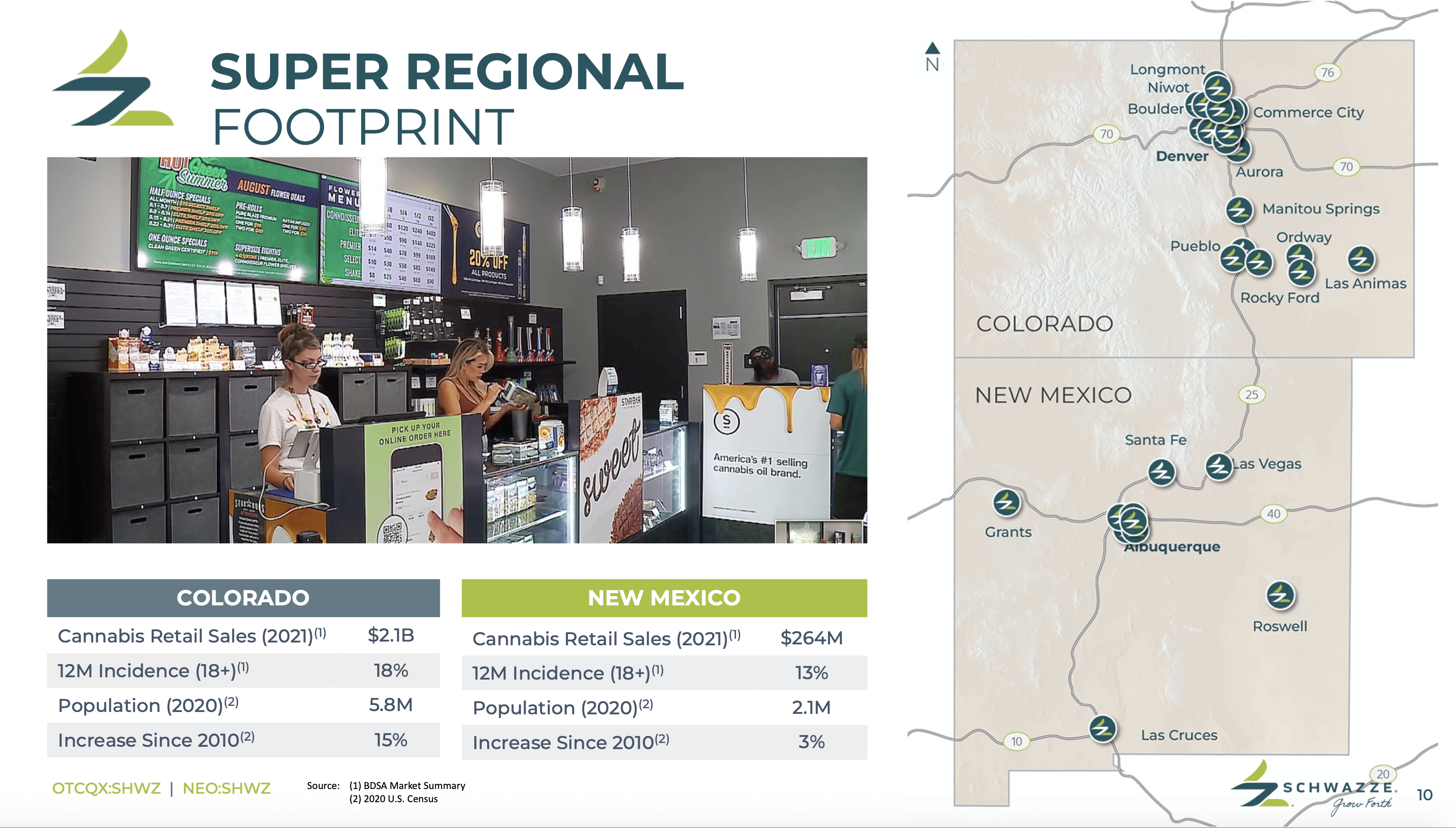

The aim is to acquire small companies with distinguishing products to achieve the kind of scale and cost efficiencies that can ballast a firm through the hard times and reap profits in the good times. The key is addressing the sector with the kind of managerial skill it had never seen before (probably because of the sector’s historical stigma). Another key to strategy is tight regional logistics along a few direct highways: in addition to Colorado, Schwazze operates in New Mexico where recreational use was first legalized in June 2021.

{kind=link}

State map of retail operations (Schwazze)

Under-the-Hood Valuation

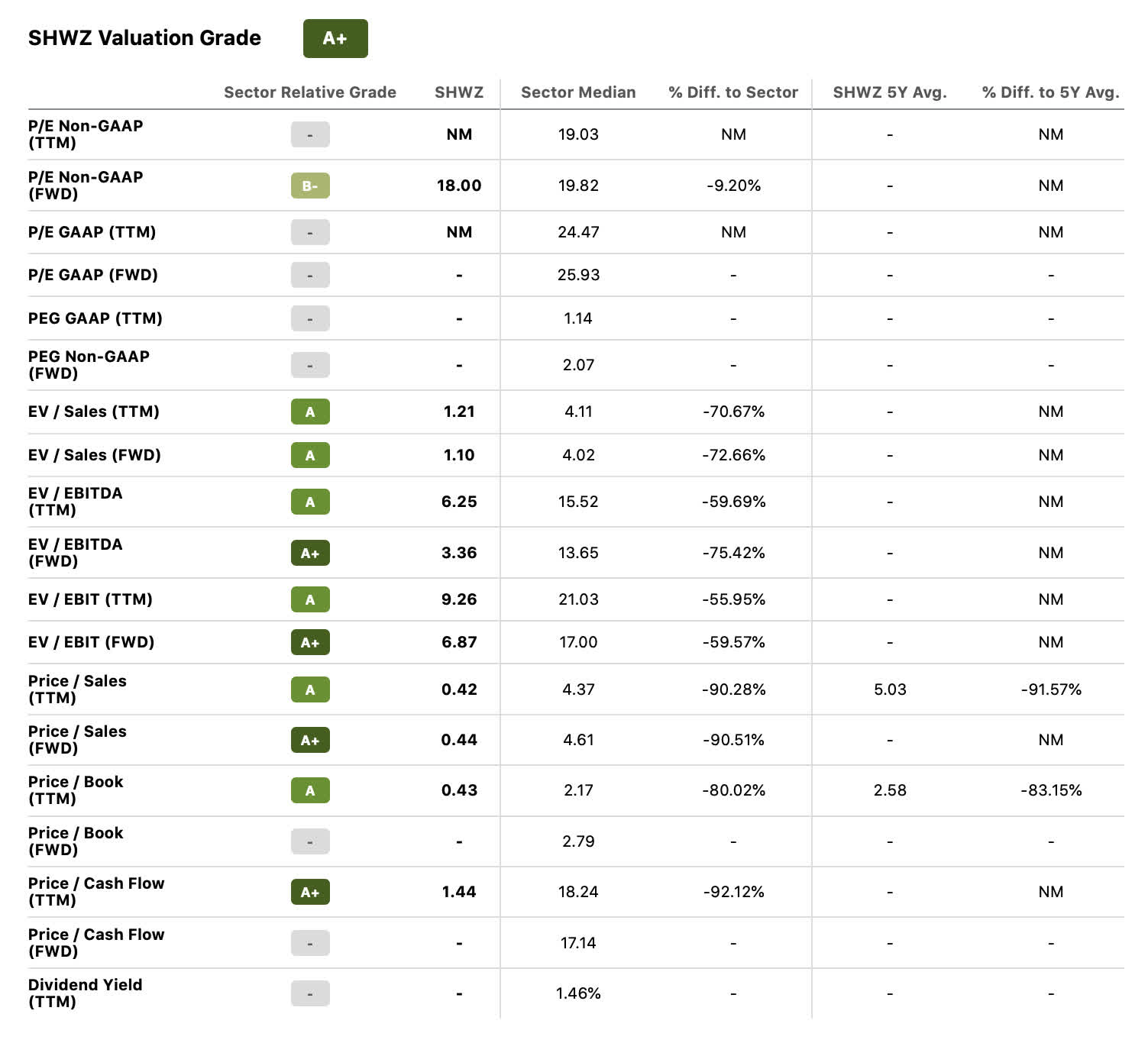

One of the things that really caught my attention with SHWZ was its price to sales ratio of .42. One of the pivotal filters for O’Shaughnessy’s famous Tiny Titans micro-cap screen is to find a stock with a P/S of less than 1.0.

In his What Works on Wall Street , O’Shaughnessy also asserts that all viable companies have sales, that sales are far harder to manipulate than earnings, and that stocks with low price-to-sales ratios have been shown to produce higher future returns.

{kind=link}

SHWZ valuation metrics (Seekingalpha.com)

A P/S of .42 and a P/B of .43 suggest a unique moment. They typically suggest a healthy sustainable company that is being very overlooked by the market but also has the wherewithal to become quite profitable.

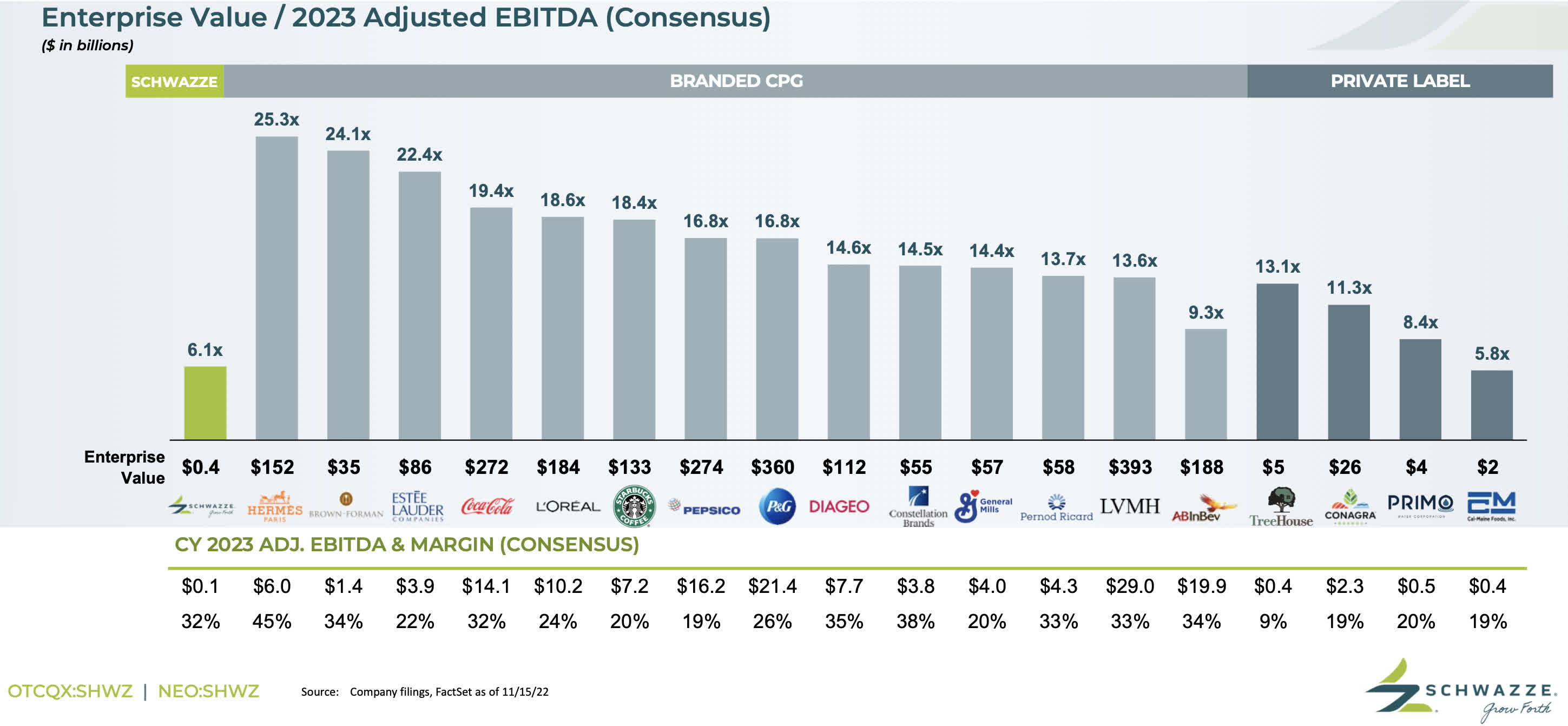

In one of its recent powerpoints, the company itself highlighted is its EV/2023 adjusted EBITDA in comparison to major public and private brands:

{kind=link}

EV/EBITDA: Public and Private Brand Comparisons (Schwazze website)

Of course, the enterprise value (EV) to the “earnings before interest, taxes, depreciation, and amortization” (EBITDA) ratio varies by industry. However, this chart is very revealing. EBITDA measures a firm's overall financial performance, while EV determines the firm's total value. The average EV/EBITDA for the S&P 500 was 17.12 in early 2022. As a general guideline, an EV/EBITDA value below 10 is commonly interpreted as very healthy and above average . SHWZ's 6.1x is impressive.

Turnaround Artists

The reason that Schwazze’s under-the-hood ratios are looking so good is that:

- The cannabis sector is out-of-favor at the moment, letting multiples compress.

- Management seems to be quietly delivering on its acquisition strategy, bringing rolled up brands to better sales and profitability.

According to its own website , Schwazze sees itself as:

“ A regional, data-driven retail growth operator driving brand development and customer engagement by leveraging best practices.. . Our operational playbooks demonstrate how we intentionally grow by design to outpace the market."

It is clear that Schwazze is led by a team of professionals with a lot of mainstream industry expertise (from Fortune 500 companies in mature low-margin retail, alcohol, groceries, etc) which is now being brought to bear on a far less competitive, rather soft-target industry. The company's deep bench expertise --which includes M&A specialists Todd Williams and Collin Lodge and veteran retail operator Ken Diehl-- has been ignored in the industry's general malaise.

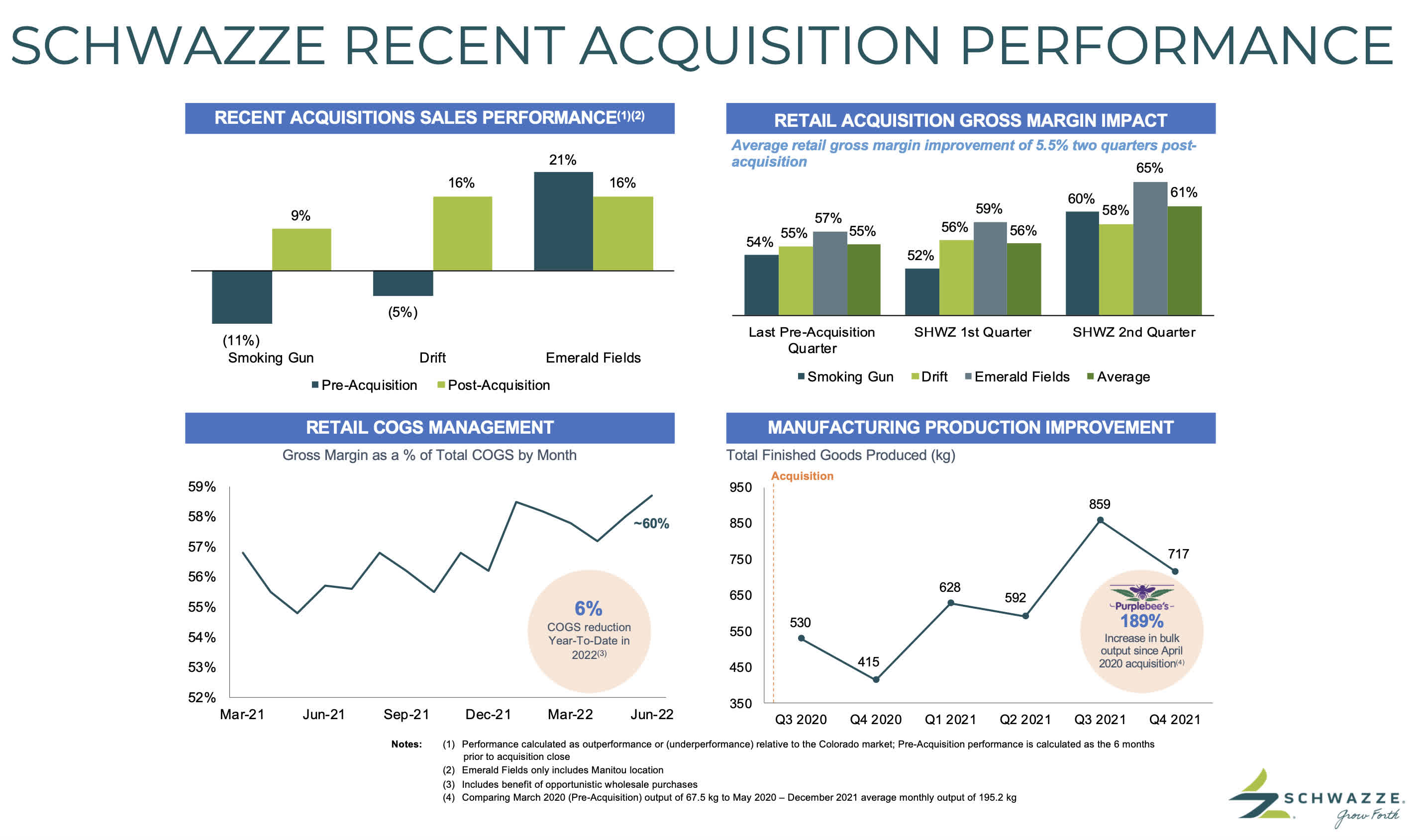

Despite tough economic conditions, Schwazze has been able to maintain growth among retail customers – a key competitive advantage because of higher pricing power and wider margin. The following slide is an example of their turnaround results for recently bought brands:

{kind=link}

Post-acquisition brand performance (Schwazze website)

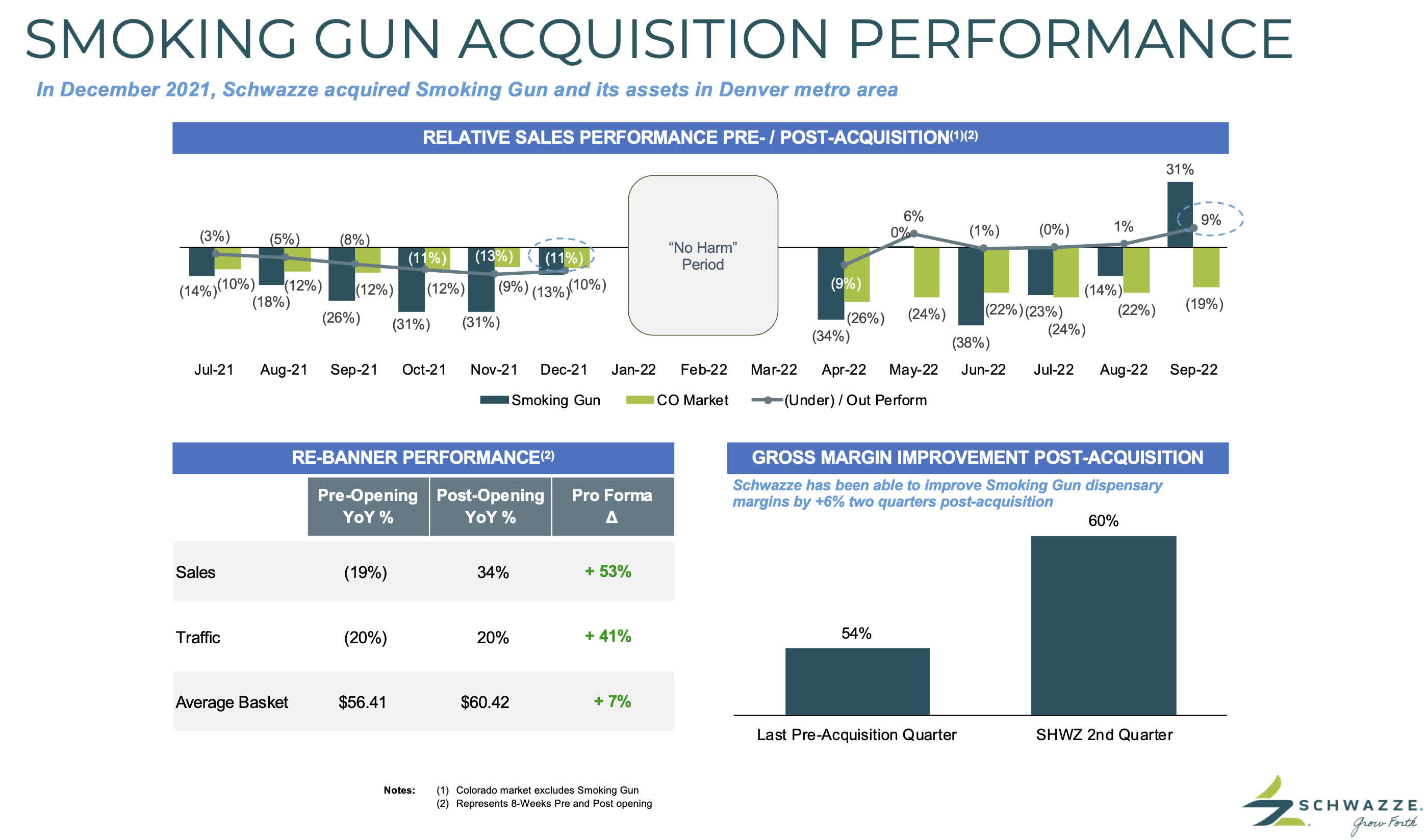

This specific monthly sales performance chart of one acquired brand (benchmarked by the Colorado state average) is also revealing:

{kind=link}

Smoking Gun monthly sales --pre and post acquisition (Schwazze website)

Earnings

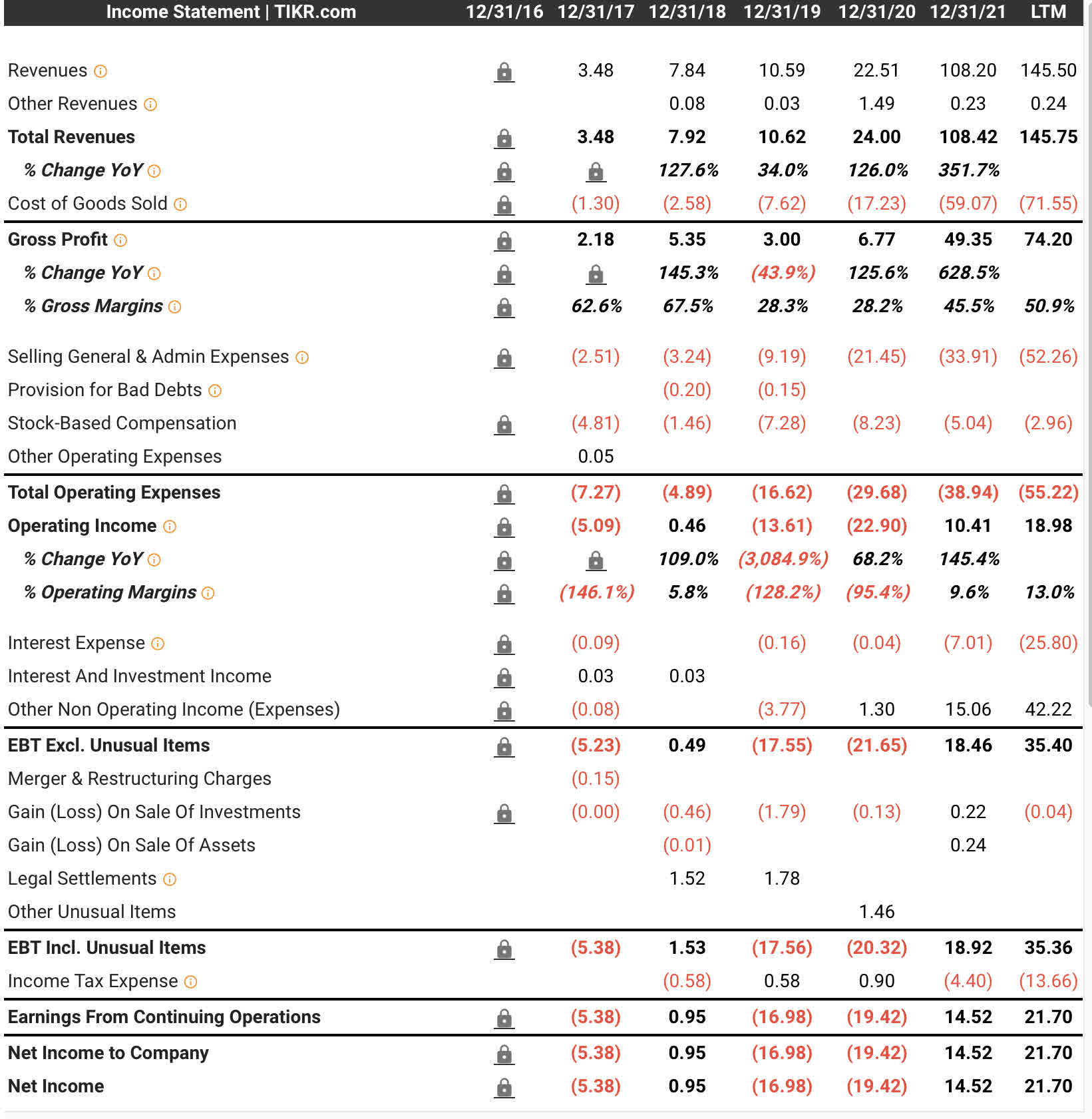

SHWZ has seen impressive annual revenue growth over the past four years with widening gross margins. Dye Capital’s takeover in 2020 is best seen in the dramatic lurch from, say 2019 revenues of $10 million to 2021’s $108 million. Earnings from continuing operations have been seeing a steep uptick over the past two years:

{kind=link}

SHWZ --Revenue Statement (Tikr)

Revenue for the first nine months of 2022 was $119.2 million, a sizable increase from the $81.9 million in revenue from 2021 in the same period.

Management has guided full-year 2022 revenue to be in the range of $155 million to $165 million, with adjusted EBITDA from $51 million to $56 million. Analysts, on the other hand, expect the full year 2022 to come in at $159.8 million, up from $108.4 million in 2021, with full EPS dropping to $0.03 from $0.06.

Looking at quarterly numbers: 3Q revenue was $43.2 million, up 36% year over year from $31.8 million in 3Q 2021. 3Q Net income was solid coming in at $1.8 million, up from $1.0 million 3Q 2021. Adjusted EBITDA was $15.9 million (36.7% of revenue) compared to $8.8 million in adjusted EBITDA last year in the third quarter.

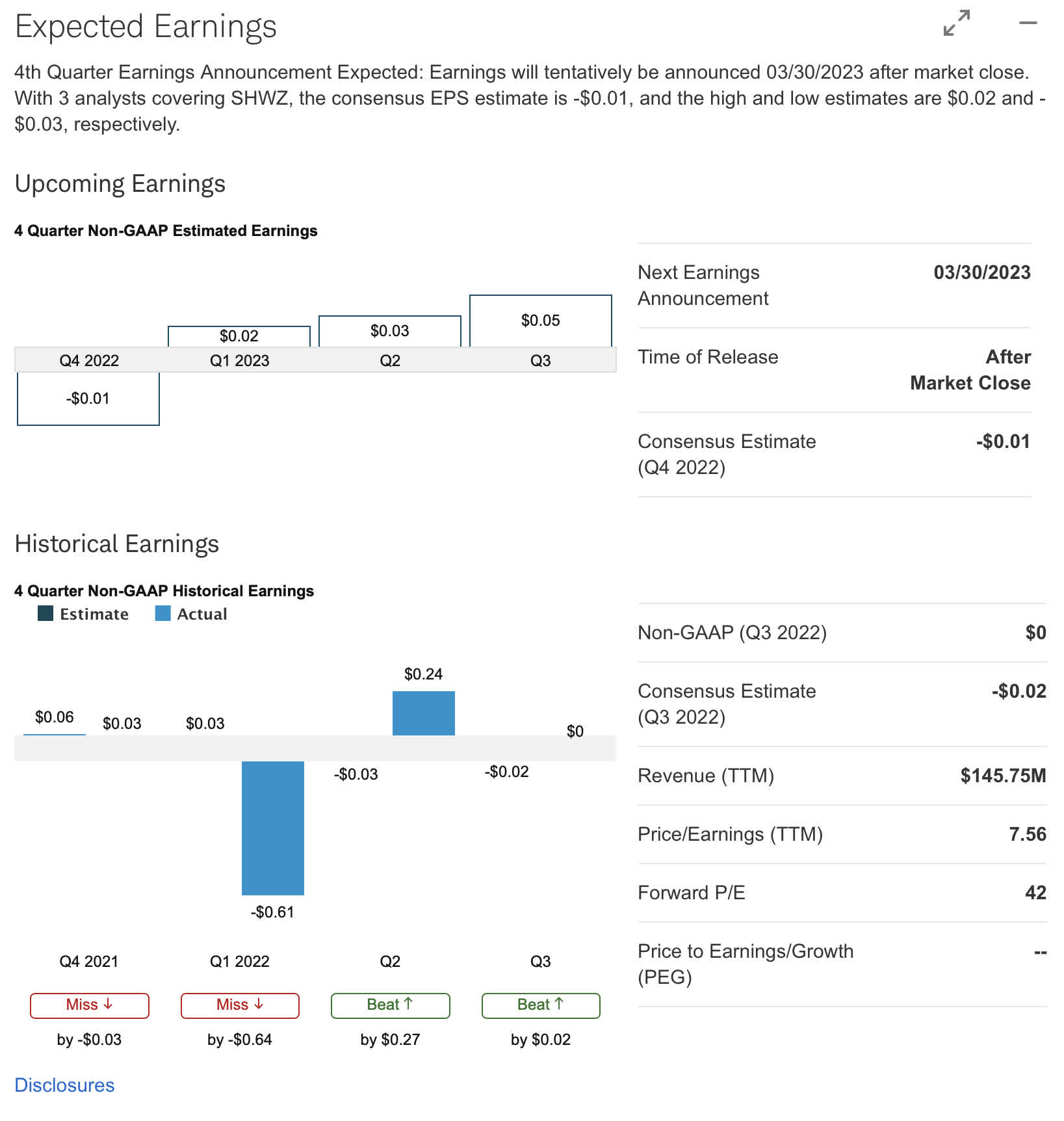

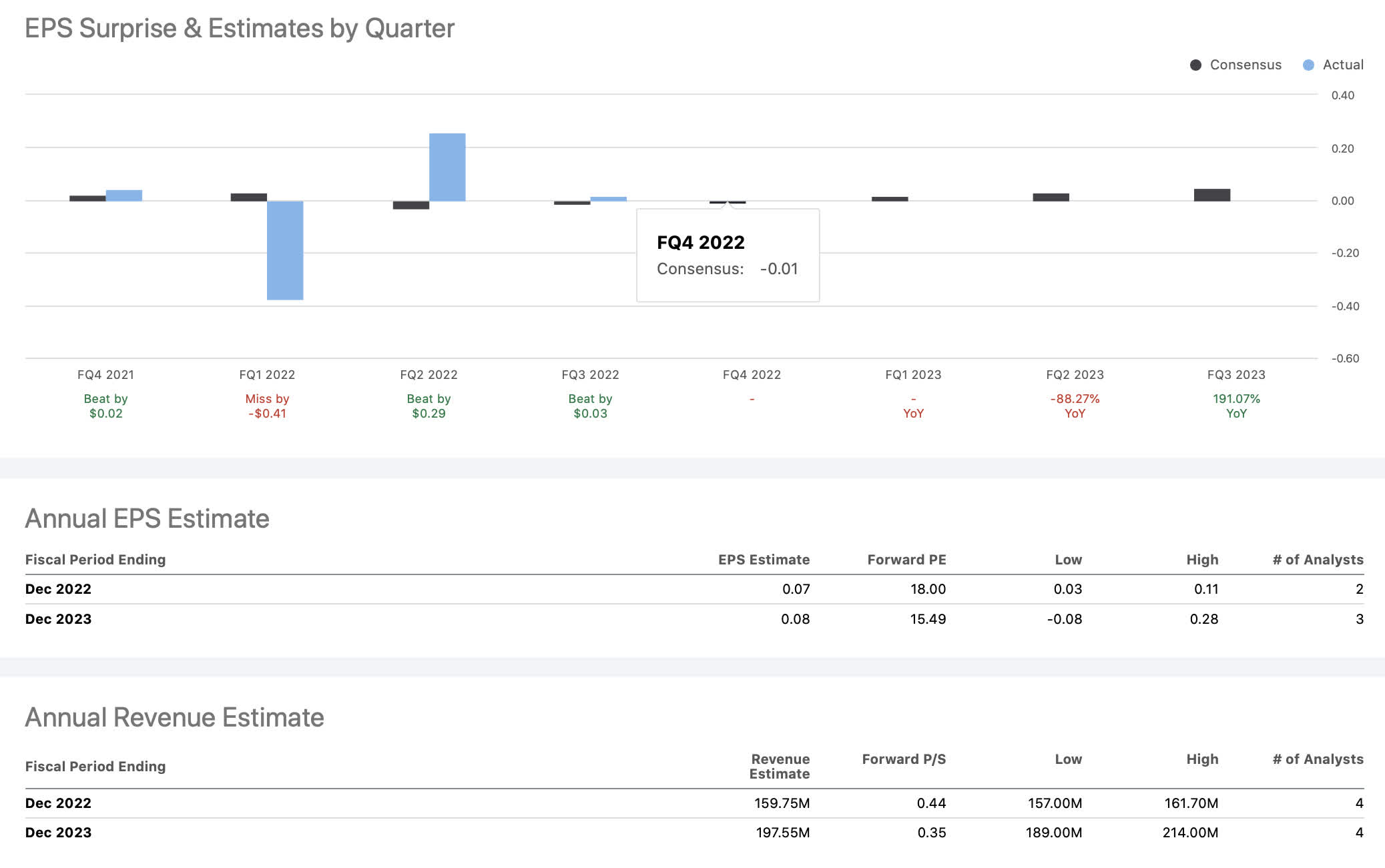

Fourth quarter earnings are expected to be announced on March 30 after the market close. With 3 analysts covering SHWZ, the consensus 3Q EPS estimate is -$0.01, and the high and low estimates are $0.02 and -$0.03, respectively.

{kind=link}

Future quarterly expected earnings (Schwab)

Though 4Q estimates are for a penny loss, analysts are seeing profitable 2023 quarters marching up to .05 EPS in 3Q 2023 with a full year EPS of .08. Full revenue for 2023 is projected to be $197.5 million. This might be the pivotal year.

{kind=link}

EPS estimates --2023 (Seekingalpha.com)

Conclusion

Operating as a vertically-integrated MSO with a tight regional focus, Schwazze now has 41 dispensaries (25 in Colorado and 16 in New Mexico) with numerous cultivation and manufacturing facilities. Though Colorado is a mature market, New Mexico's legal cannabis sales are expected to see nearly 200% growth by 2026 --from just over $200 million to near $800 million within three years.

SHWZ is driving down expenses and costs even as it invests in growth in the Colorado and New Mexico markets. It is clearly a growth company within the sector – with 36% YoY Revenue Growth last quarter--due to its operational approach. It is generating cash from operations --one of only 6 MSOs doing so at present. And in 2023, it is looking to generate free cash flow before acquisitions.

Nationally, the total addressable market for U.S. legal cannabis was $28.3B in 2022 and expected to grow to $46.2B by 2026 (a 13% CAGR) and $100B by 2030. But despite these grandiose projections, the actual industry is swollen with difficulties that only a good management team can navigate.

With a market cap is only $68.97 million (despite having an EV of $154.19M), you are --at the moment-- getting that management team rather cheap.

For further details see:

Schwazze: A Tiny Titan And Best Of Breed Operator In The Cannabis Space