SIX - SeaWorld Entertainment: Gauging The Impact Of Inclement Weather Remains A Buy Long Term

2023-09-20 04:18:10 ET

Summary

- SeaWorld Entertainment's shares have been negatively impacted by bad weather, causing a decline in revenue, profits, and cash flows.

- Despite the temporary setbacks, some metrics have held up relatively well, such as revenue and a marginal increase in total revenue per capita.

- The company's future performance is uncertain, but long-term investors may see an opportunity to buy a high-quality company at a discounted price.

One of the things that makes investing difficult is the fact that you never know what outside conditions might arise that could impact the companies you are investing in. When it comes to theme park operators, for instance, financial performance might be robust and shares might look cheap. But when you factor in weather and how large a role that can have in future performance, uncertainty arises that could hurt your return prospects for some time. Bad weather seems to be the cause of some pain over at theme park operator SeaWorld Entertainment ( SEAS ). And in response to this, shares of the enterprise have taken a beating over the past several months. Although painful, this could also be a great time for those who are long term focused to really step in and pick up a high-quality company at a very good price.

Temporary issues

When I last wrote about SeaWorld Entertainment in an article published in early November of last year, I found myself impressed with how quickly the company had recovered from the COVID-19 pandemic and how strong overall financial results were leading up to that point. Attendance was strong and robust spending at the company's parks all mixed together to create strong revenue, profits, and cash flows. Add on top of this how cheap shares were, and I could not help but to rate the business a ‘buy’ to reflect my view that shares should outperform the broader market for the foreseeable future. Unfortunately, Mother Nature had something else in store. Inclement weather has pushed revenue, profits, and cash flows, all down year over year. And in response to that, shares are down 17.7% compared to when I last wrote about the business. By comparison, the S&P 500 is up 17.8% over that same window of time.

{kind=link}

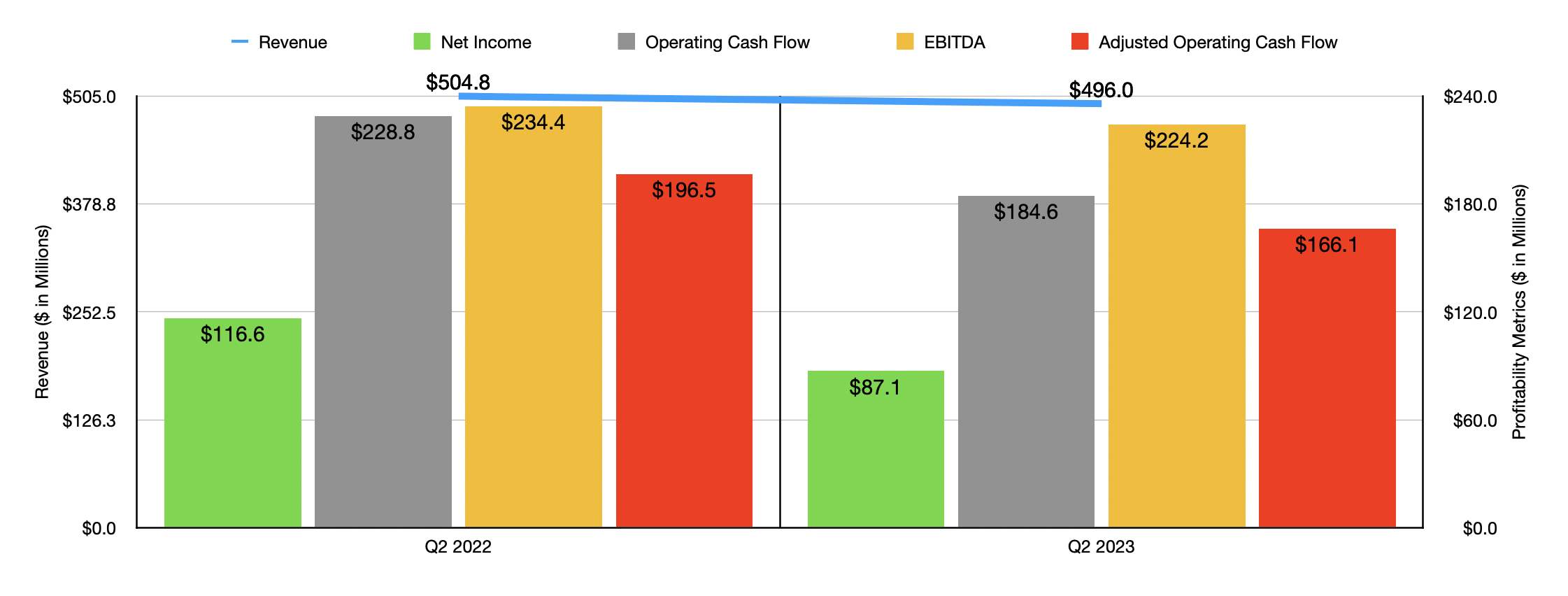

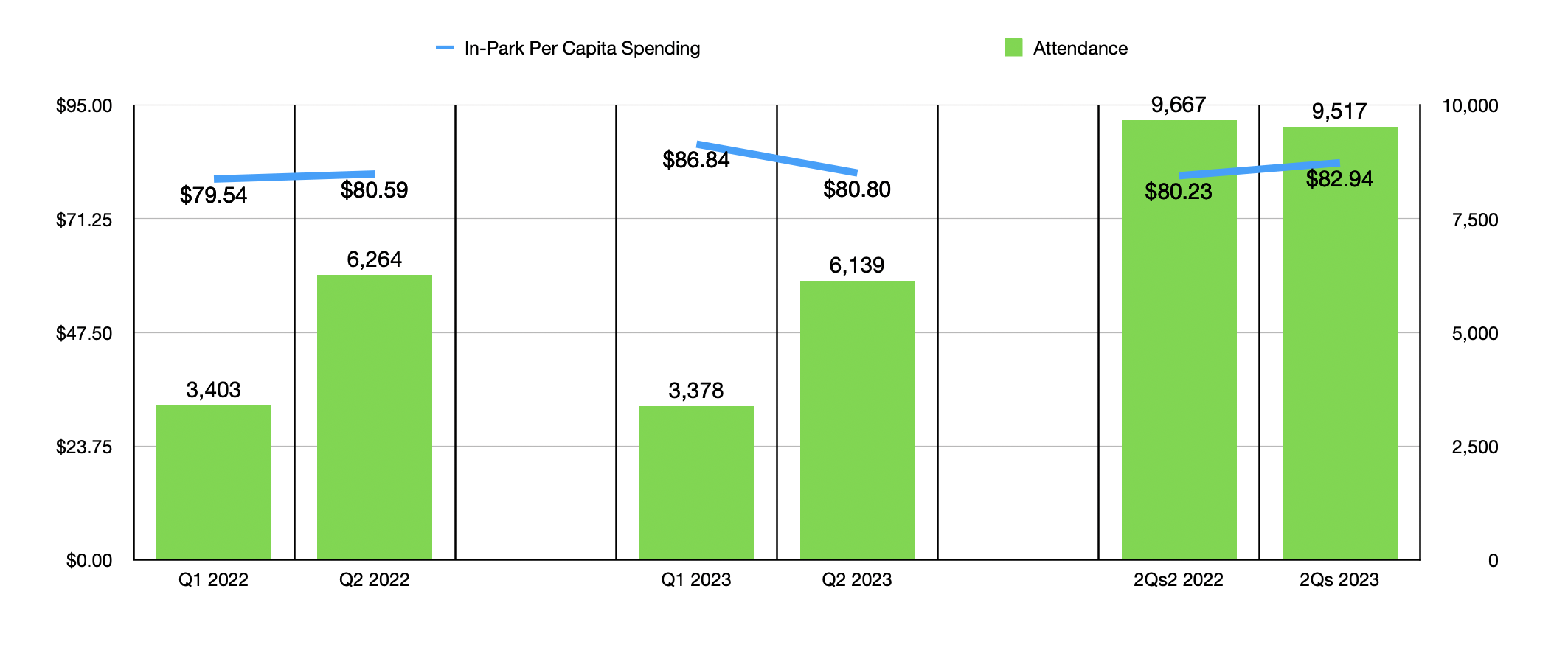

When I talk about bad performance, it's important to note that some metrics have held up better than others. If we look at the second quarter of the 2023 fiscal year as an example, overall revenue has dipped only modestly, falling from $504.8 million last year to $496 million the same time this year. That's a drop of only 1.7% year over year. According to management, this decline in revenue was driven by a 2% drop in attendance, with the number of visitors at the company's parks falling from 6.26 million to 6.14 million. Management attributed this decline in revenue to significantly worse weather than what the company had seen the year prior. This included both unusually hot weather and cold weather, as well as rain and issues associated with the wildfires in Canada. This was offset marginally by a rise in total revenue per capita from $80.59 to $80.80. Even though this may not seem all that significant, when applied to the number of visitors the company saw in the second quarter, that increase offset the revenue decline of the business by nearly $1.3 million.

{kind=link}

Although the revenue drop was modest, the same cannot be said of the decline in profits. Net income plunged from $116.6 million to $87.1 million. The biggest chunk of this increase was $12 million of additional selling, general, and administrative costs. This metric worsened so much because of a $7.1 million increase in non-recurring third-party consulting costs as the company explored strategic initiatives aimed at improving long term performance. Higher marketing costs of an unspecified amount were also part of the problem. Unfortunately, other profitability metrics for the business also dropped during this time. Operating cash flow, for instance, went from $228.8 million to $184.6 million. If we adjust for changes in working capital, it still fell, declining from $196.5 million to $166.1 million. And finally, EBITDA pulled back modestly from $234.4 million to $224.2 million.

{kind=link}

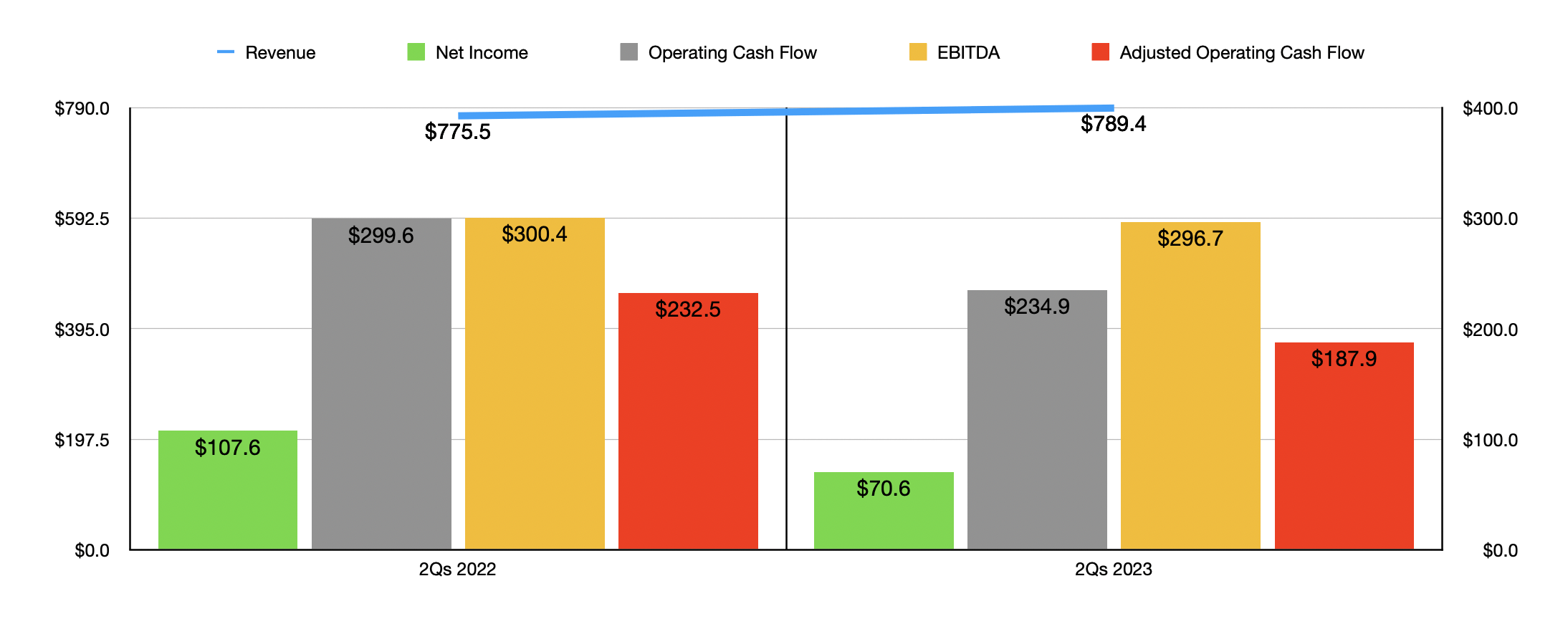

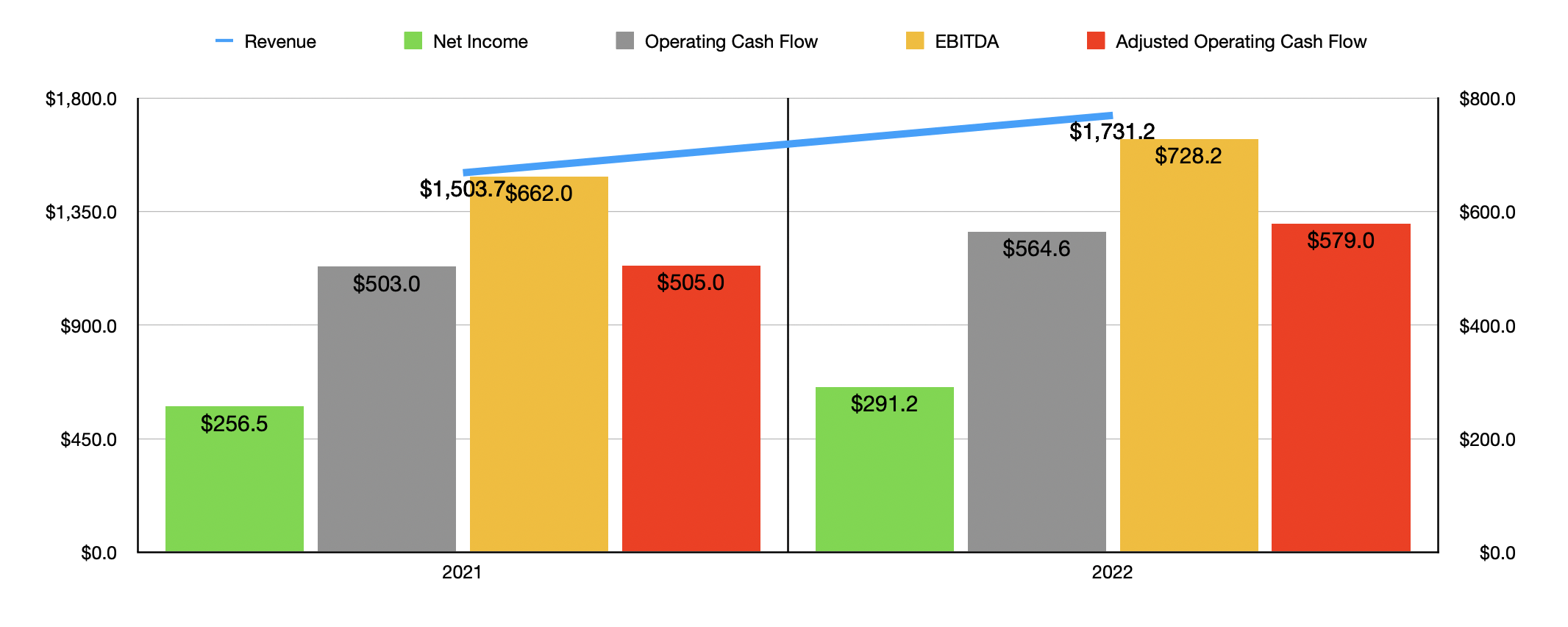

To be very clear, the second quarter of this year on its own was particularly bad. When you look at the first half of the year in its entirety and compare it to the same time last year, there are still ways in which the company held up relatively better. Revenue, for instance, actually rose from $775.5 million last year to $789.4 million this year. Even as attendance dropped by 1.5%, total revenue per capita jumped 3.4%, or $2.71. This all comes off of a rather stellar year that was 2022. As you can see in the chart below, in that year, revenue and all profitability metrics for the company came in notice of a stronger than they were in 2021.

{kind=link}

In terms of what the future holds, we don't know entirely what to expect. Management has not provided any real guidance for the year. But if we annualize results experienced so far, we would expect net profits for 2023 of $191.1 million, adjusted operating cash flow of $467.9 million, and EBITDA of $721.2 million. Using these figures, I was able to value the company as shown in the chart below. I also, in that chart, priced the company using data from last year. Even though the firm looks the same when it comes to the EV to EBITDA approach, it does look more expensive on a forward basis when it comes to the other two profitability metrics. But again, we are dealing with inclement weather and the aforementioned consulting costs. Both of these should be considered one-time events. Or at least in the case of weather, it won't be a recurring event every year.

{kind=link}

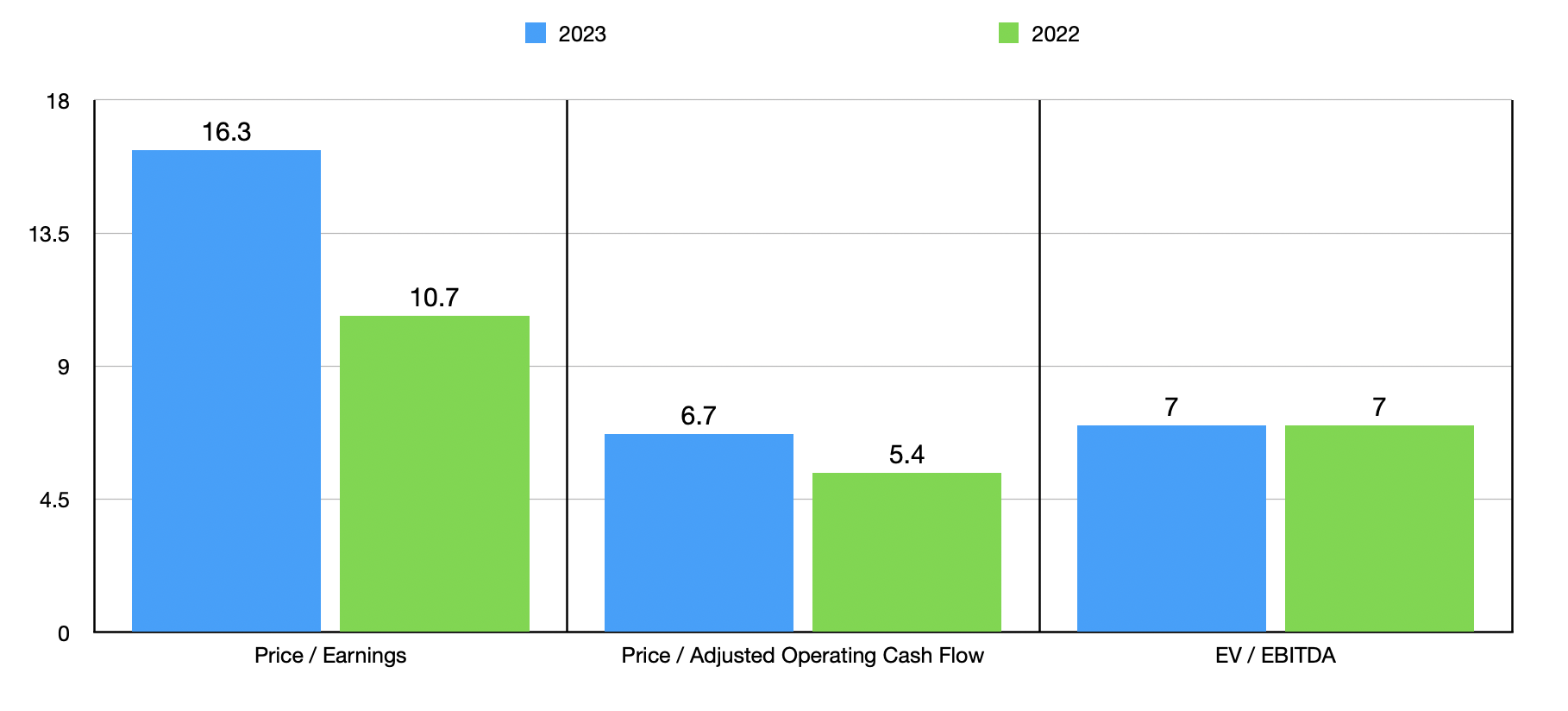

Relative to similar firms, shares of SeaWorld Entertainment look to be quite attractive. As you can see in the table below, I compared our prospect to Six Flags Entertainment ( SIX ) and Cedar Fair, L.P. ( FUN ). On a price to earnings basis, one of these companies was cheaper than our prospect, while the other was more expensive. But when it comes to the other two profitability metrics shown, SeaWorld Entertainment ended up being the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| SeaWorld Entertainment |

| 16.3 |

| 6.7 |

| 7.0 |

| Six Flags Entertainment |

| 24.9 |

| 6.9 |

| 11.4 |

| Cedar Fair |

| 8.7 |

| 7.7 |

| 7.1 |

In the long run, I have no doubt in my mind that SeaWorld Entertainment will be just fine. However, there is some risk that the weather-related pain will persist well beyond the most recent completed fiscal quarter. I say this because of some other reporting that is out there. You see, the second quarter for 2023 ended on June 31st of this year. However, as one source indicated , July of this year saw additional weakness in theme park traffic, not only because of continued bad weather, but also due to a reduction in consumer discretionary spending. And even in August, weather conditions have worsened, with one example of this being Tropical Storm Hilary. Given that this covers two of the three months in the third quarter, it would not be surprising in the least bit to see this pain result in additional top line and bottom line pressure, not only for SeaWorld Entertainment, but also for its competitors.

Takeaway

At this moment, things are not looking particularly pleasant for SeaWorld Entertainment and its investors. Due to factors completely outside of what most people would have expected, shares have taken a beating because of top line and bottom line weakness. Very likely, the market is also working to price in additional weakness moving forward. For those who can't stomach the volatility that this will bring, it might be best to stay away from a company like SeaWorld Entertainment. But for long-term, value oriented investors, I would argue that the picture for the enterprise should be fine and that now might be a great time to get in while shares are cheap.

For further details see:

SeaWorld Entertainment: Gauging The Impact Of Inclement Weather, Remains A Buy Long Term