SCWX - SecureWorks Continues Transition As It Reduces Headcount

2023-05-04 17:43:11 ET

Summary

- SecureWorks Corp. provides endpoint security software and solutions to organizations worldwide.

- The company is exiting legacy businesses in favor of a subscription model through its flagship system Taegis XDR.

- While Taegis has produced strong growth, total revenue continues to decline as SecureWorks Corp. wrestles with its transition.

- Until we see a resumption in top line revenue growth and a material reduction in operating losses, I'm on Hold for SecureWorks Corp.

A Quick Take On SecureWorks

SecureWorks Corp. ( SCWX ) provides organizations with cybersecurity software and services to manage their IT threat environment.

The company has produced continued growth from its Taegis XDR system.

However, while SecureWorks Corp. continues to move away from its legacy business lines, until it can restart total revenue growth while reducing operating losses and cash burn, I’m on Hold for the stock.

SecureWorks Overview

Atlanta, Georgia-based SecureWorks Corp. was founded in 1999 to provide a variety of endpoint protection and vulnerability management and response software to organizations of all sizes.

The firm is headed by Chief Executive Officer Wendy Thomas, who was previously Chief Financial Officer at Bridgevine and VP Finance at First Data Corporation.

The company’s primary offerings include:

-

Taegis extended detection & response [XDR]

-

Managed detection & response

-

Vulnerability management

-

Managed services

-

Security assessments & training.

The firm acquires customers through its direct sales and marketing efforts as well as through partner referrals and technology alliances.

SCWX now counts a total of 2,000 customers for its flagship Taegis XDR platform.

SecureWorks’ Market & Competition

According to a 2021 market research report by Verified Market Research, the global endpoint security market was an estimated $13.4 billion in 2020 and is projected to reach $24.7 billion by 2028, growing at a CAGR of 7.9% between 2021 and 2028.

The growth forecast is due to the expected increased adoption of AI/ML solutions and IoT applications which will drive the need for endpoint security innovations.

Additionally, a growing number of increasingly complex malware attacks force antivirus/antimalware solutions providers to constantly update their detection tools with the latest security patches.

Major vendors that provide or are developing endpoint security solutions include:

-

McAfee (Intel)

-

Symantec Corporation

-

Eset

-

AVG Technologies

-

Cylance

-

Palo Alto Networks

-

FireEye

-

F-Secure

-

Webroot

-

Okta

-

Sophos.

SecureWorks’ Recent Financial Trends

-

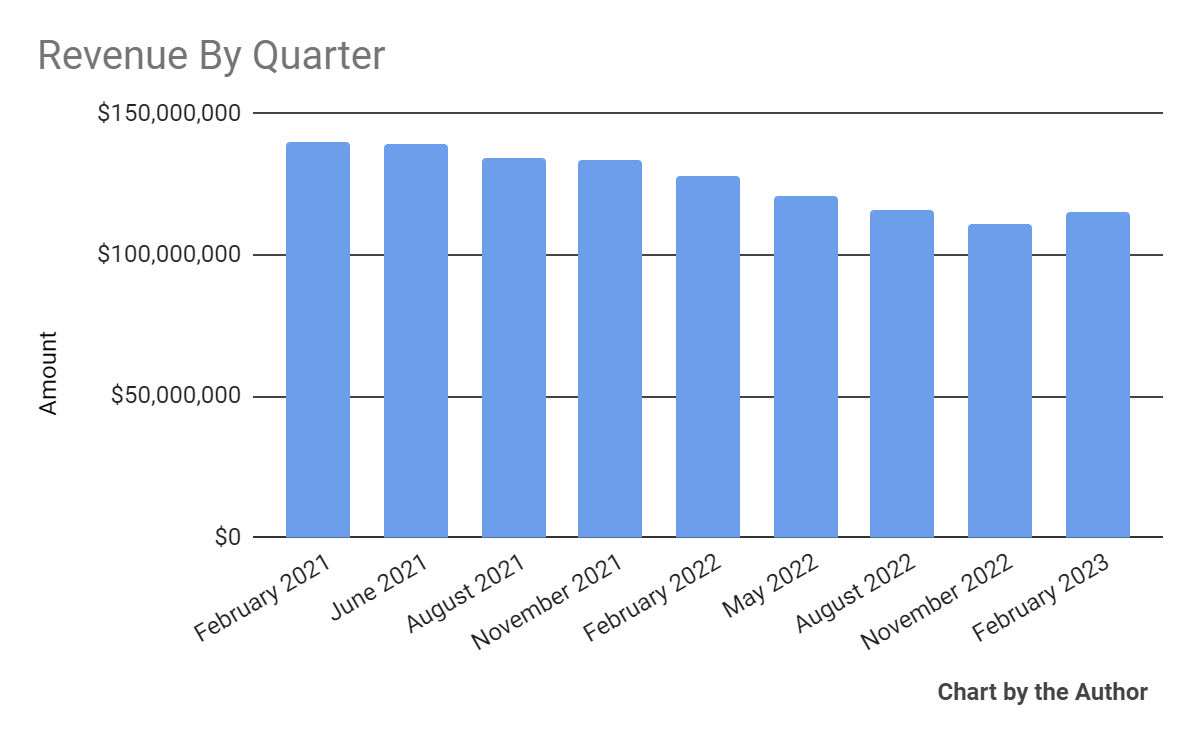

Total revenue by quarter has trended lower as the chart shows here:

{kind=link}

-

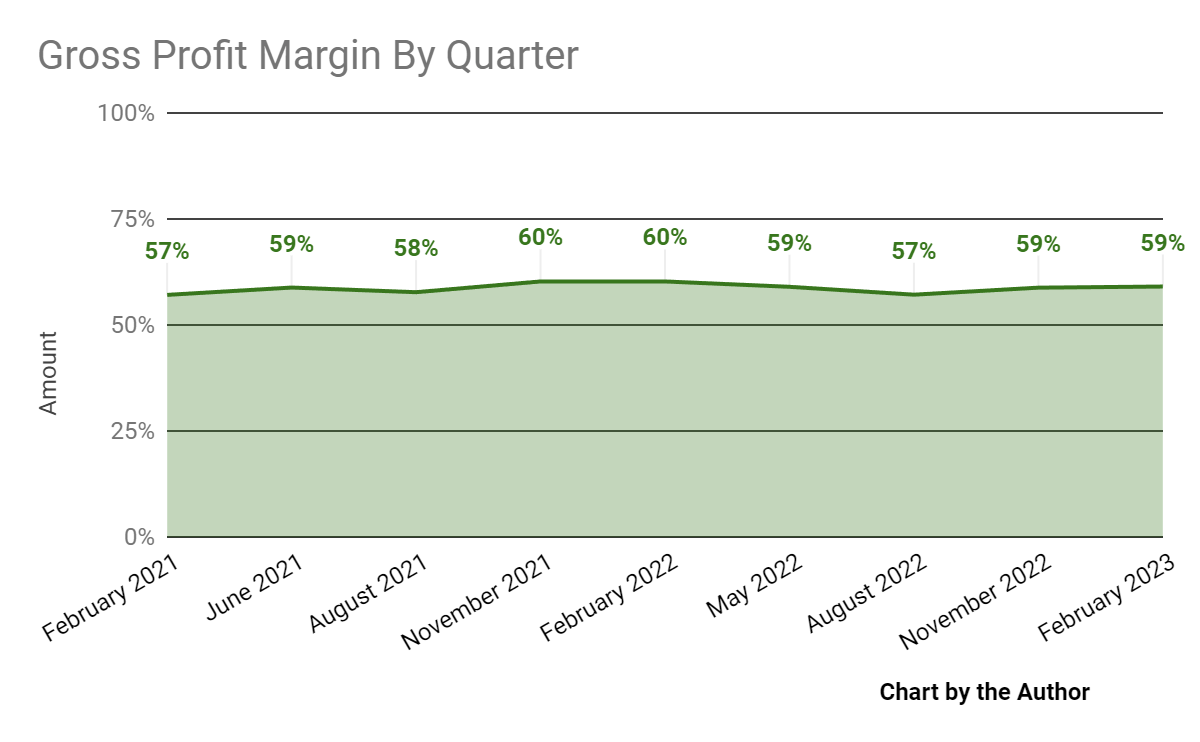

Gross profit margin by quarter has varied within a narrow range:

{kind=link}

-

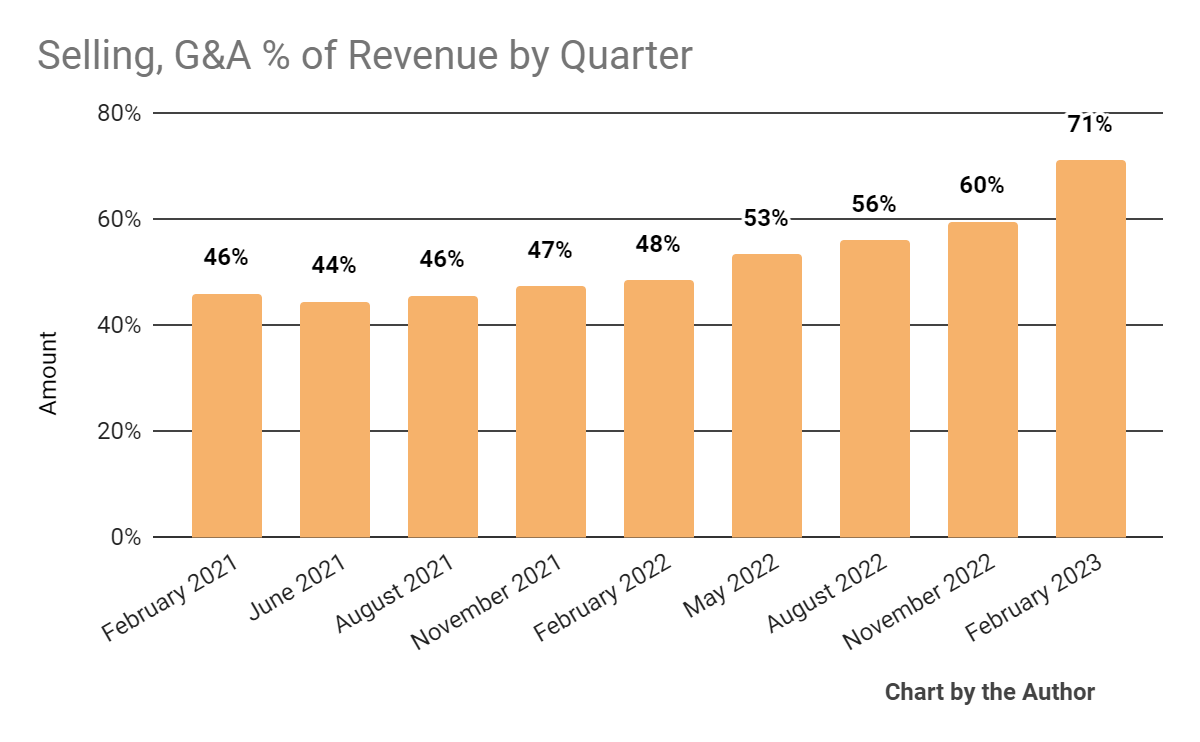

Selling, G&A expenses as a percentage of total revenue by quarter have risen materially in recent quarters, a negative signal:

{kind=link}

-

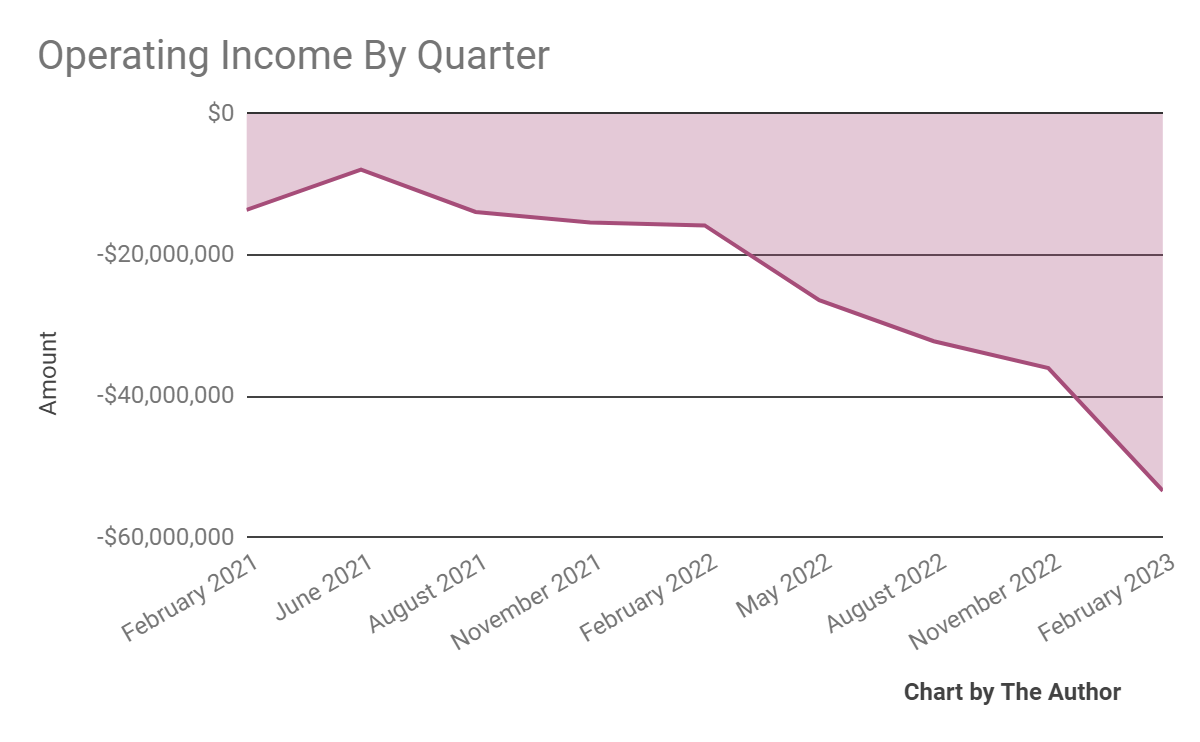

Operating losses by quarter have worsened substantially recently:

{kind=link}

-

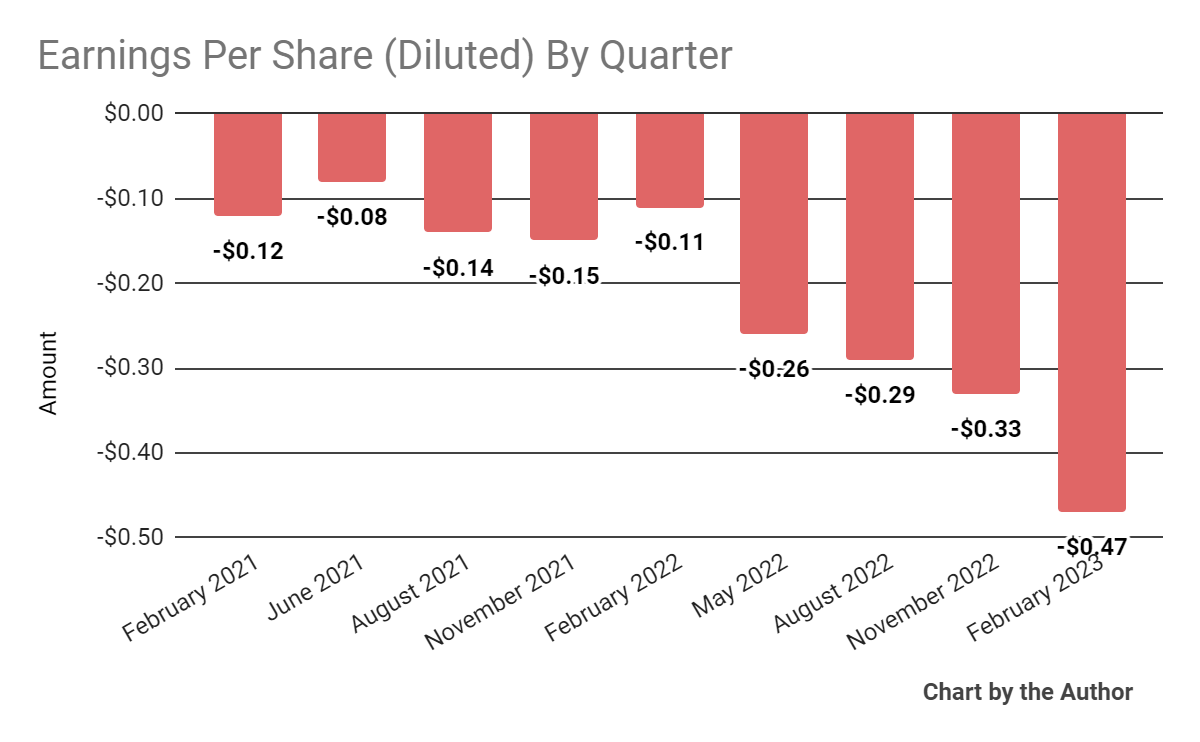

Earnings per share (Diluted) have worsened much further into negative territory recently:

{kind=link}

(All data in the above charts is GAAP.)

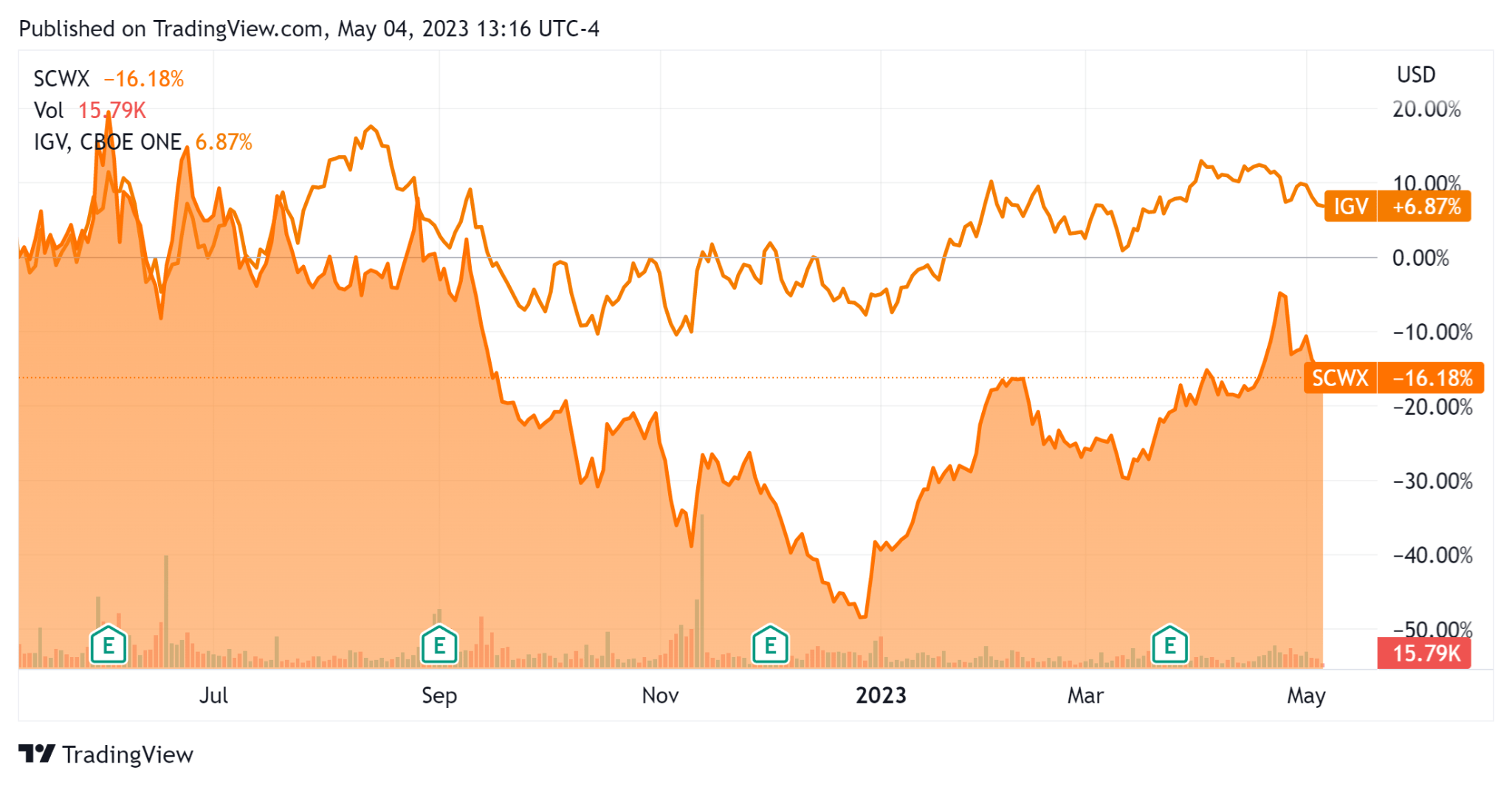

In the past 12 months, SCWX’s stock price has fallen 16.18% vs. that of the iShares Expanded Tech-Software Sector ETF’s ( IGV ) rise of 6.87%, as the chart indicates below:

{kind=link}

For the balance sheet , the firm ended the quarter with $143.5 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash used was a very high $64.5 million, of which capital expenditures accounted for only $1.9 million. The company paid a hefty $36.9 million in stock-based compensation, or SBC, in the last four quarters, the highest in the past eleven-quarter period.

Valuation And Other Metrics For SecureWorks

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 1.4 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 1.6 |

| Revenue Growth Rate |

| -13.4% |

| Net Income Margin |

| -24.7% |

| EBITDA % |

| -24.0% |

| Market Capitalization |

| $765,570,000 |

| Enterprise Value |

| $634,200,000 |

| Operating Cash Flow |

| -$62,600,000 |

| Earnings Per Share (Fully Diluted) |

| -$1.35 |

(Source - Seeking Alpha.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

SCWX’s most recent Rule of 40 calculation was negative (37.4%) as of FQ4 2023’s results, so the firm’s results have worsened significantly in recent quarters, per the table below:

| Rule of 40 Performance |

| Calculation |

| Recent Rev. Growth % |

| -13.4% |

| EBITDA % |

| -24.0% |

| Total |

| -37.4% |

(Source - Seeking Alpha.)

Commentary On SecureWorks

In its last earnings call ( Source - Seeking Alpha ), covering FQ4 2023’s results, management highlighted the strong growth from its Taegis XDR solution, with annual recurring revenue growth of 58% year-over-year, reaching $261 million.

The company announced a 9% headcount reduction in February as it continues its transition away from its legacy business segments to a pure SaaS play.

If all goes well, leadership expects "to exit fourth quarter fiscal 2024 near breakeven EBITDA…"

However, management did not disclose any company or customer retention rate metrics.

Total revenue for FQ4 2023 fell 9.85% and gross profit dropped 1.2 percentage points.

SG&A as a percentage of revenue rose sharply, growing by 23 percentage points and operating losses widened substantially, although that was before the headcount reduction announcement.

Looking ahead, management expects full-year fiscal 2024 revenue to be $275 million at the midpoint of the range and adjusted EBITDA loss of $34 million at the midpoint.

The company's financial position needs improvement, with only about 2.2 years of cash runway at its trailing twelve-month cash burn rate. I suspect the headcount reduction will help reduce burn as will sunsetting other company segments over time.

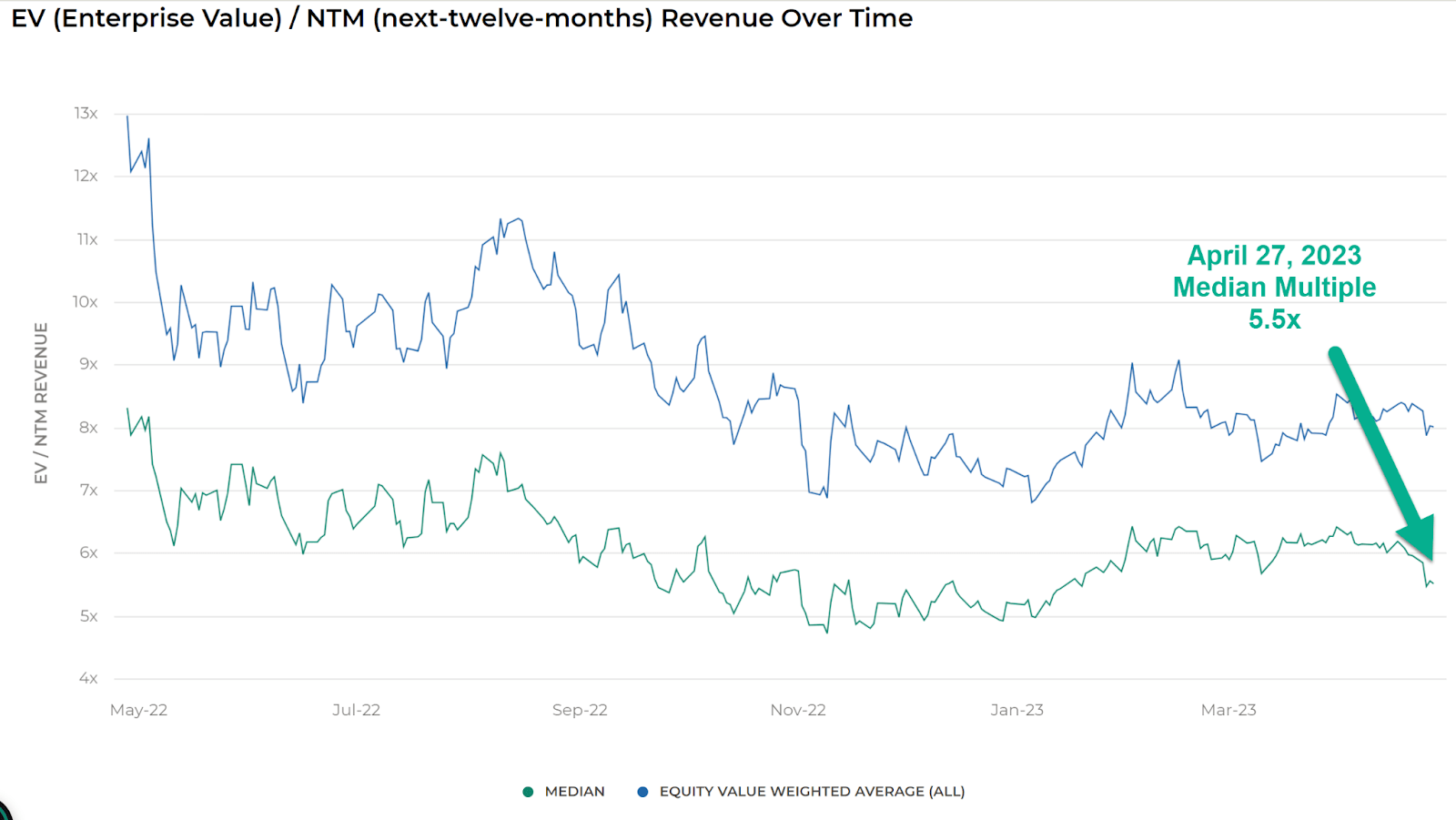

Regarding valuation, the market is valuing SCWX at an EV/Sales multiple of around 1.4x on contracting top line revenue due to the transition to a Taegis-centric approach.

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 5.5x on April 27, 2023, as the chart shows here:

{kind=link}

So, by comparison, SecureWorks Corp. is currently valued by the market at a substantial discount to the broader Meritech Capital SaaS Index, at least as of April 27, 2023.

The primary risk to the company’s outlook is the potential for a macroeconomic slowdown, which can lengthen sales cycles and reduce its revenue growth trajectory.

Management is pinning its future approach on Taegis, which appears to get generally good reviews from users and is producing strong revenue growth.

However, the company is still managing the transition to a pure SaaS firm and that will take time and result in further revenue decline and the potential for continued operating losses.

Until management can reignite revenue growth while reducing operating losses and cash burn, I’m on Hold for SecureWorks Corp.

For further details see:

SecureWorks Continues Transition As It Reduces Headcount