WTTR - Select Energy Services Looks Well Positioned For 2023

2023-04-12 16:22:50 ET

Summary

- Select Energy Services provides water management services to oil & gas exploration and production companies in the United States.

- The firm has made a number of acquisitions during a challenging period for the industry.

- Given current supply and demand imbalances, the potential for further growth ahead and stock price appreciation, my outlook on WTTR is a buy at around $7.50 per share.

A Quick Take On Select Energy Services

Select Energy Services (WTTR) provides a range of water management services to oil & gas exploration & production companies in the United States.

WTTR has made a number of acquisitions during a down period in the industry.

Given my discounted cash flow calculation suggesting a value price for the stock, the company's positioning after its recent dealmaking and the potential for additional growth, my outlook on WTTR is a Buy at around $7.50 per share.

Select Energy Overview

Select Energy's predecessor entity was founded as Peak Oilfield Services, LLC and began operations in 2007.

Chairman, President and Chief Executive Officer John Schmitz founded the firm and has been in the oilfield services business for several decades.

Schmitz is also founder and President of B-29 Holdings, a family office that contains privately-held interests in a variety of oil & gas investments.

Select Energy operates three operating segments:

-

Water Solutions

-

Water Infrastructure

-

Oilfield Chemicals

Select Energy's Market & Competition

According to a 2021 market research report by Fortune Business Insights, the global hydraulic fracturing market (as a proxy for the water management segment) was an estimated $11.7 billion in 2020 and is forecast to reach $28.9 billion by 2028.

This represents a forecast CAGR of 9.5% from 2021 to 2028.

The company has said that its water inventory sources are a 'key competitive advantage' by being able to offer the large volumes of water necessary in hydraulic fracturing operations.

Furthermore, the water services part of the support system to E&P (Exploration and Production) customers is highly fragmented and largely composed of many small firms that don't offer an integrated suite of services.

There are major oilfield services firms that provide water services, but do so as a side business rather than their focus.

Major competitive or other industry participants include:

-

Halliburton

-

Schlumberger

-

Baker Hughes

-

Ovivo

-

Aquatech International

-

Veolia

Select Energy's Recent Financial Trends

-

Total revenue by quarter has risen substantially in recent quarters, as the chart shows here:

Total Revenue (Seeking Alpha)

-

Gross profit margin by quarter has trended higher in recent quarters, likely due to an improved pricing environment from higher end-user demand:

Gross Profit Margin History (Seeking Alpha)

-

Selling, G&A expenses as a percentage of total revenue by quarter have dropped as a percentage of revenue:

Selling, G&A % Of Revenue (Seeking Alpha)

-

Operating income by quarter has jumped well into positive territory in recent quarters:

Operating Income History (Seeking Alpha)

-

Earnings per share (Diluted) have also remained positive, although with significant quarter-to-quarter variation:

Earnings Per Share History (Seeking Alpha)

(All data in the above charts is GAAP)

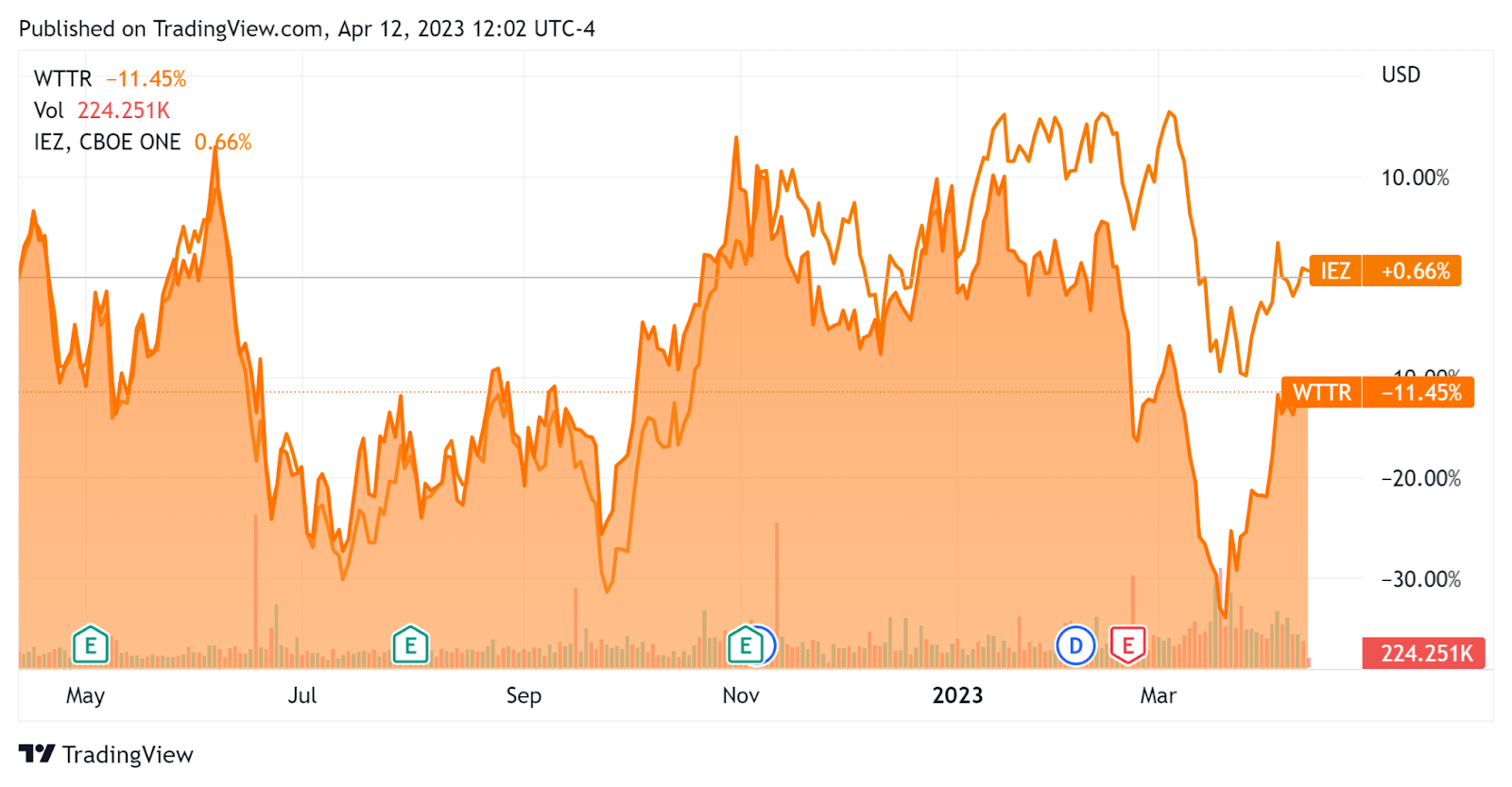

In the past 12 months, WTTR's stock price has fallen 11.45% vs. that of the iShares U.S. Oil Equipment & Services ETF's ( IEZ ) drop of 0.66%, as the chart indicates below:

{kind=link}

For the balance sheet, the firm ended the quarter with cash and equivalents of $7.3 million and total debt of $16.0 million.

Over the trailing twelve months, free cash used was $38.7 million, of which capital expenditures accounted for a hefty $71.9 million. The company paid $15.6 million in stock-based compensation in the last four quarters, which represents a strong upward trend in SBC in recent quarters.

Valuation And Other Metrics For Select Energy

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 0.7 |

| Enterprise Value / EBITDA |

| 6.2 |

| Price / Sales |

| 0.5 |

| Revenue Growth Rate |

| 81.5% |

| Net Income Margin |

| 3.5% |

| GAAP EBITDA % |

| 11.8% |

| Market Capitalization |

| $950,760,000 |

| Enterprise Value |

| $1,020,000,000 |

| Operating Cash Flow |

| $33,230,000 |

| Earnings Per Share (Fully Diluted) |

| $0.49 |

(Source - Seeking Alpha)

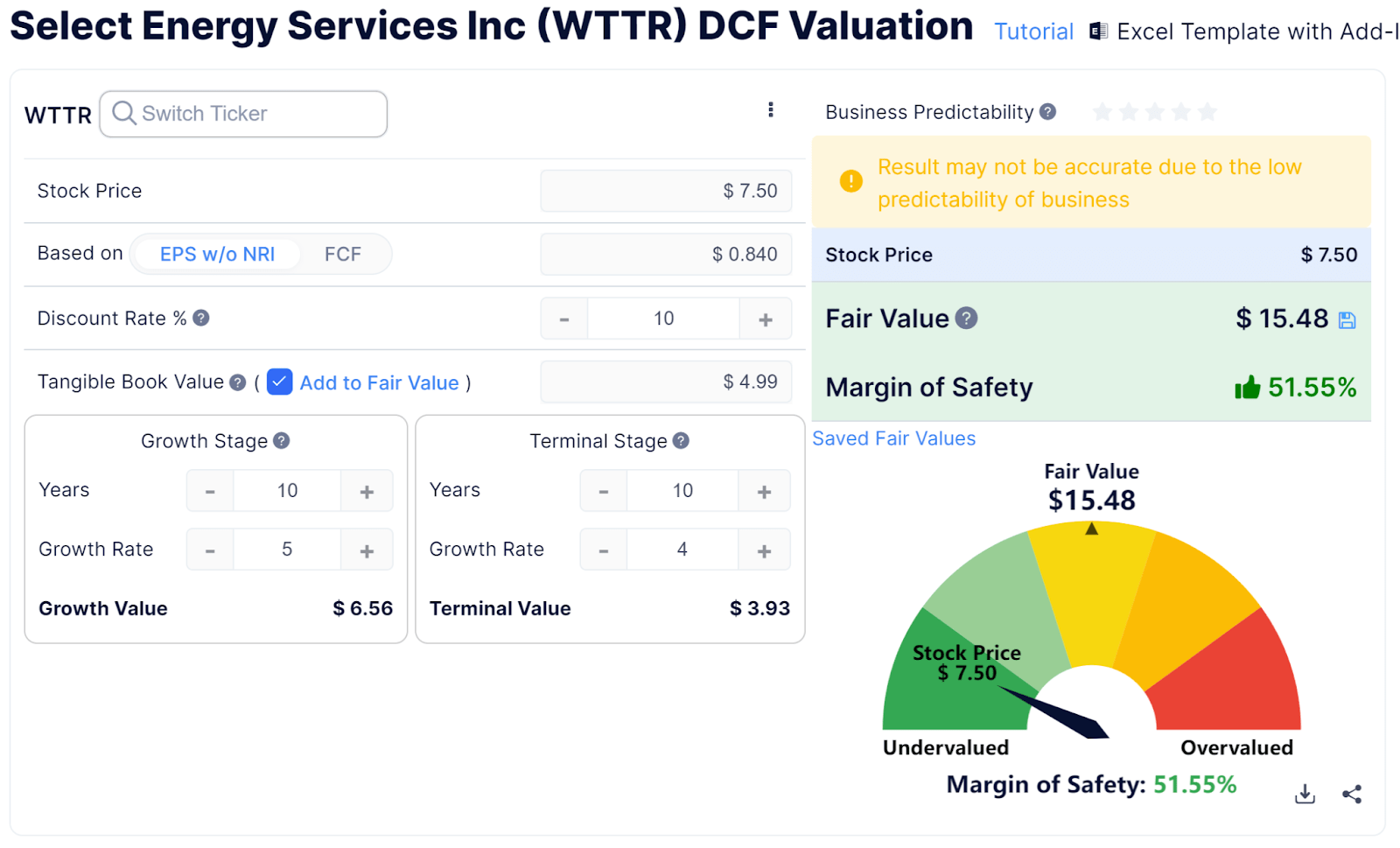

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm's projected growth and earnings:

{kind=link}

Assuming generous DCF parameters, the firm's shares would be valued at approximately $15.48 versus the current price of $7.50, indicating they are potentially currently undervalued, with the given earnings, growth, and discount rate assumptions of the DCF.

Future Prospects For Select Energy

In its last earnings call (Source - Seeking Alpha), covering Q4 2022's results, management highlighted the record results for its Water Infrastructure and Chemicals segments.

During 2022, the company also closed on several acquisitions due to its strong balance sheet, positioning itself for improving industry dynamics after a challenging two-year period brought on by the global pandemic.

Leadership also noted the recent start of paying a quarterly dividend, which is currently generating a 2.68% forward yield versus the industry median of 3.47%, per Seeking Alpha's Dividend Yield calculations .

Looking ahead, management expects 2023 CapEx to be around $110 million at the midpoint of the range, depending on market conditions and customer requirements.

From an operational standpoint, in 2023, the company will be focused on 'taking out costs in the system, on integrating operations, on putting together what we've acquired on a unified basis throughout the Lower 48 shale basins.'

Regarding valuation, my conservative discounted cash flow calculation suggests that WTTR may be significantly undervalued at its current price of around $7.50.

The primary risk to the company's outlook is a softening macroeconomic environment. Even major Middle East producers are cutting output, indicating they see economic softness in the near future.

The recent U.S. bank crisis is apparently already filtering through to reduced lending by banks as they lower risk, look more closely at their lending portfolios and 'hunker down' for the time being.

However, as 2023 wears on, further growth in the industry may be around the corner, as the potential for future growth in the Permian Basin (50% of WTTR's operations) rig count below suggests:

Permian Basin Rig Count (Baker Hughes)

Given my discounted cash flow calculation suggesting a value price for the stock, the company's positioning after several acquisitions, and the potential for additional growth, my outlook on WTTR is a Buy at around $7.50 per share.

For further details see:

Select Energy Services Looks Well Positioned For 2023