WTTR - Select Water Solutions: Beat The Smart Money For Once [Maintaining A Buy]

2023-07-05 11:30:00 ET

Summary

- We think Select is underappreciated by the market for a variety of reasons.

- The company has been on a growth streak with 12 acquisitions in the last couple of years.

- New and accretive contracts are being reported each quarter.

- WTTR is attractive at present prices for growth and income.

Introduction

I have covered Select Water Solutions ( WTTR ) on a number of prior occasions. Here's a link to that past work, to which I recommend you read for the sake of due diligence. Select has changed their name to reflect a sharper focus of their core mission, supplying frac water to operators and treating flowback and produced water.

{kind=link}

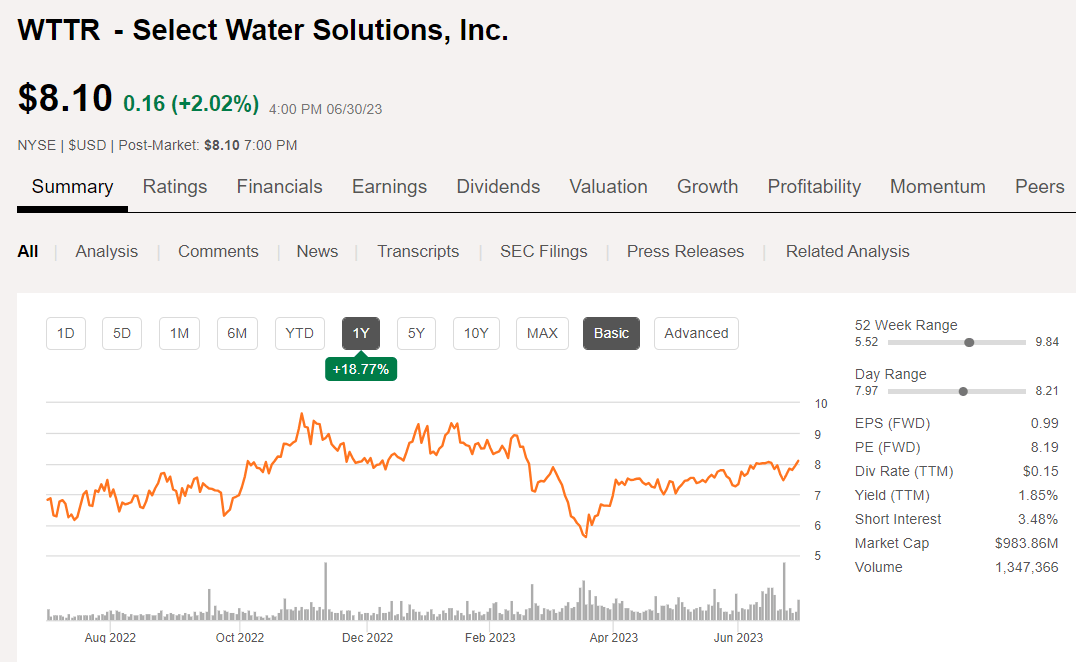

Not much else has changed, including Wall Street's bullish view of their prospects. A point with which, after six bullish buy ratings of my own, I really can't argue. But, it does get boring issuing a buy rating and having the stock just sit there, a point of view with which I am sure many of you will agree. Here's the thing. Water treatment should be a good business and someday it will be . WTTR has traded in the same range for the past year or so, in spite of steadily improving financials, as you can see in the chart below. Something I can only attribute to the generally dour mood of investors toward the upstream industry over this period. We think conditions are ripe for change in this outlook and that could be a driver for WTTR.

{kind=link}

The analyst cadre are as confused as I am with WTTR's lack of progress. There were only 4 on the call last quarter, but they came away impressed as their combined rating on the company rose one notch to buy . Price targets ranged from $8-15.00, with a median of $11.40. That median represents a 40% upside to the present price and gives us something to work with.

Let's review the last quarter and come up with our own estimate.

The case for WTTR

I am not going to go into a great deal of depth and really recommend you read the older articles , where I have built an extensive thesis for the company, if WTTR interests you.

At a high level, water is needed for fracturing and that business will continue to grow (if you buy the argument that the U.S. is going to stay in the oil production business.) Not necessarily as a function of the rig count. The industry is drilling longer wells and applying ever increasingly concentrated stimulation treatments to them. Water is the key. Next for every well that is turned to sales, there will also be an ever-increasing water cut. Toward the end of their useful lives, wells are producing more than 90% brackish water. Produced water has been traditionally pumped down disposal wells, but that practice is trending down due to seismic activity and the need to minimize the use of fresh water in fracturing. The produced water market is de-linked from the rig count and will only grow in the coming years.

WTTR is a leader in this business with both mobile equipment for remote treatment on location and site-built recycling centers, supported by pipelines. Its business has been built largely through buying market share with strategic acquisitions, the most recent of which was Breakwater Energy Partners, and Cypress Energy Solutions. In each case they entered new markets, acquired new technology and picked up badly needed employees. Over the last couple of years, Select has made a dozen acquisitions. Technology will play a greater role in water recovery in the future with low energy RO units on the horizon.

WTTR also has an integrated business supplying chemistry for well stimulation and EOR recovery, with crossover applications to frac flowback and produced water applications. Supplying chemistry can be a good business if you are selling technology along with the materials. Nick Swyka, SVP and CFO commented on the strategy for chemicals in the Q-1 call:

Throughout 2022 and into 2023, our Chemicals group has continued to grow market share in our higher margin proprietary product offerings. We continue to shift manufacturing capacity towards these customized products, while limiting our production of more commoditized products and lower margin blending operations.

Makes sense to me! I used to sell chemistry (nobody is better at this than Schlumberger ( SLB ), my old employer) to the oilfield. This is an area where many engineers are out of their depth and rely heavily on advice from service company professionals, backed up by amazing lab technology and geochemical professionals. All told the track record for stimulation treatments is mixed. About half the time they deliver the intended result - usually increased production , and the other half they make things worse - less production . Either way the service company has made their money, and in the failure case, if the sales rep is on their game - there is a reason I was called, The Fluidsdoc , they are back in the clients office the next week with a new plan for a new remedial stimulation treatment. Cha-Ching$$$. I've done this a million times.

Q-1, review

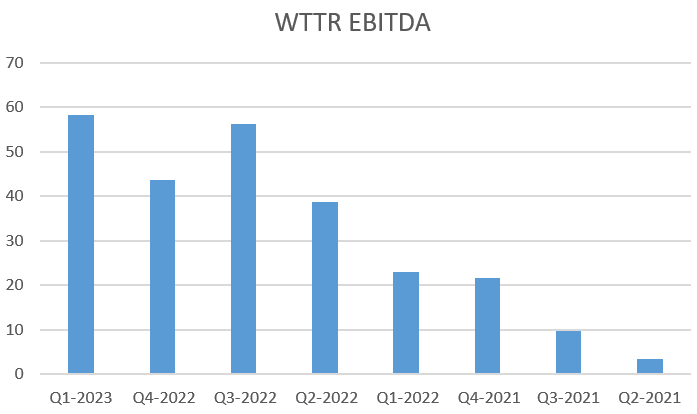

Revenue for the first quarter of 2023 was $416.6 million as compared to $381.7 million in the fourth quarter of 2022 and $294.8 million in the first quarter of 2022. Gross profit was $59.7 million, as compared to $41.6 million in the fourth quarter of 2022 and $24.7 million in the first quarter of 2022. Adjusted EBITDA was $67.2 million in the first quarter of 2023 as compared to $52.2 million in the fourth quarter of 2022 and $32.2 million in the first quarter of 2022. Adjusted EBITDA during the first quarter of 2023 was adjusted for $11.1 million of non-recurring and non-cash trademark abandonment expense in connection with the rebranding initiative. Total gross margin was 14.3% in the first quarter of 2023 as compared to 10.9% in the fourth quarter of 2022 and 8.4% in the first quarter of 2022.

Segment info

The Water Services segment generated revenues of $228.6 million in the first quarter of 2023 as compared to $218.5 million in the fourth quarter of 2022 and $163.6 million in the first quarter of 2022. Gross margin before D&A for Water Services was 20.5% in the first quarter of 2023 as compared to 18.5% in the fourth quarter of 2022 and 16.2% in the first quarter of 2022. Water Services segment revenues increased 5% sequentially.

The Water Infrastructure segment generated revenues of $101.5 million in the first quarter of 2023 as compared to $77.2 million in the fourth quarter of 2022 and $58.6 million in the first quarter of 2022. Gross margin before D&A for Water Infrastructure was 28.5% in the first quarter of 2023 as compared to 22.4% in the fourth quarter of 2022 and 24.2% in the first quarter of 2022. Water Infrastructure revenues increased significantly by 32% sequentially from an already record-high fourth quarter with strong 48% incremental gross margins driving meaningful consolidated segment margin improvement.

The Oilfield Chemicals segment generated revenues of $86.4 million in the first quarter of 2023 as compared to $86.0 million in the fourth quarter of 2022 and $72.6 million in the first quarter of 2022. Gross margin before D&A for Oilfield Chemicals was 19.4% in the first quarter of 2023 as compared to 17.4% in the fourth quarter of 2022 and 14.4% in the first quarter of 2022. They continue to see strong demand for their higher-margin, proprietary chemical technologies resulting in improved product mix driving further margin improvements across the segment.

Balance sheet

Total cash and cash equivalents were $6.0 million as of March 31, 2023, as compared to $7.3 million as of December 31, 2022. The Company had $75.5 million and $16.0 million of borrowings outstanding under its sustainability-linked credit facility as of March 31, 2023 and December 31, 2022, respectively.

As of March 31, 2023 and December 31, 2022, the borrowing base under the sustainability-linked credit facility was $257.3 million and $245.0 million, respectively. The Company had available borrowing capacity under its sustainability-linked credit facility as of March 31, 2023 and December 31, 2022, of approximately $159.2 million and $206.1 million, respectively, after giving effect to $22.6 million and $22.9 million of outstanding letters of credit as of March 31, 2023 and December 31, 2022, respectively.

Guidance

For the second quarter of 2023, the Company expects to see relatively stable revenue with gross margins before D&A improving by 100–200 basis points, as they continue to capture additional operational efficiencies in a relatively stable activity environment.

Supported by the recent robust revenue growth seen during the first quarter of 2023, the Company anticipates relatively steady revenues in Water Infrastructure during the second quarter of 2023 with gross margins before D&A improving 200-300 basis points supported by the accretive margin contributions of our recent organic projects.

For the second quarter of 2023, the Company anticipates mid-single digit percentage revenue improvements and steady margins for the Oilfield Chemicals segment as the segment continues to advance from its all-time high-water mark levels.

Business Development updates for Q-1

Haynesville Gathering Expansion & Acreage Dedication

During the first quarter of 2023, Select signed a multi-year gathering and disposal agreement with a minimum volume commitment ("MVC") in exchange for a capacity dedication with a large independent operator in the Haynesville Shale. Select is in the process of constructing a 5-mile produced water pipeline that would connect the operator's water infrastructure system to Select's existing 60-mile underground twin pipeline network in the Haynesville Shale in Texas and Louisiana. The operator has agreed to a 15 million barrel MVC over a five-year term with a total contract term of ten years. Additionally, the $5 million project is supported by an approximately 30,000-acre dedication under which the operator has dedicated all future produced water volumes generated within the dedicated area to Select's interconnected produced water gathering and disposal systems, providing significant long-term upside to the existing MVC agreement. They expect for construction to be complete and for the pipeline to be operational by the end of the third quarter of 2023.

MidCon Gathering & Disposal Project

During the first quarter of 2023, Select signed a multi-year gathering and disposal agreement with a large public operator in the MidCon region. The $4 million project is supported by an MVC in exchange for a capacity dedication and the construction of a 6-mile produced water pipeline connecting the operator's water infrastructure system to an existing Select wastewater disposal facility. We expect for construction to be complete and for the pipeline to be operational by the end of the third quarter of 2023.

DJ Basin Water Distribution Pipeline

Select recently signed a multi-year water sourcing and delivery agreement with an MVC in exchange for a reserved volume commitment with a major integrated oil and gas company in the DJ Basin in Colorado. During January 2023, Select completed construction and commenced operations on the $8 million project, consisting of a 6-mile 24" pipeline to connect a nearby water source to the operator's leasehold. To support the project, the operator agreed to an initial up front capital commitment of $10 million and a 35 million barrel MVC over a three-year period.

East Texas Gathering & Disposal Projects

Select recently signed two multi-year gathering and disposal agreements with the same public operator in the Haynesville Shale region in East Texas supporting a combined $5 million of capital projects. Both agreements have ten-year terms and wellbore dedications in exchange for disposal capacity dedications from Select. The first agreement contemplates the construction of a 5-mile pipeline that connects the operator's infrastructure assets to a newly constructed wastewater disposal facility in East Texas, and the second agreement contemplates construction of a 2-mile pipeline that connects the operator's infrastructure assets to an existing Select wastewater disposal facility in East Texas. The company expects well completion and pipeline construction to be completed and for the facilities to be operational by the end of the second quarter of 2023.

Risks

The principle risk I see for WTTR is dead money. They have managed to avoid every upstream rally since 2020. Some of this could be the perception of investors that water is old technology and is not properly compensated for by operators. Too much competition in the sector has probably also been a reason. Much of that has been true, but it is rapidly changing.

Midstream operators recently received an upgrade from Citi analyst Spiro Dounis citing-

Shale growth has slowed and become more ratable, which in turn has moderated capital spending; midstream companies have spent the last three years de-levering and have largely achieved leverage targets, which releases capital back to equity holders; and companies are able to maintain growth rates due to brownfield expansions which are highly capital efficient.

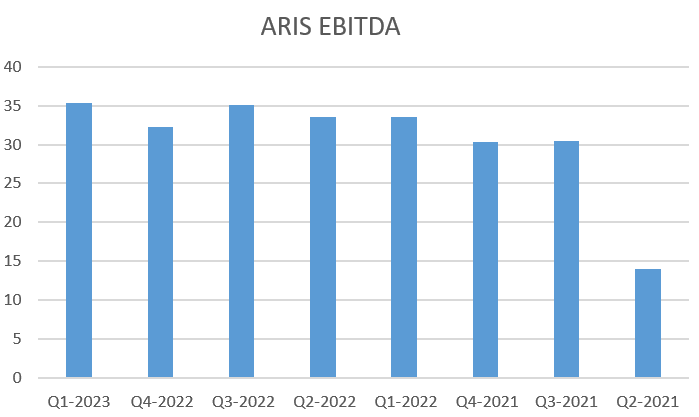

WTTR was not included in this cadre, but I think it should have been. It's EBITDA metrics show more growth that one who was, Aris Water Solutions ( ARIS ) - down to $10 from $17 in November of last year. As a reminder, WTTR has been on a growth acquisition binge the last couple of years. And, that takes capital. Add in the capex for new projects listed above and you can see the company is building for the future.

{kind=link}

Your takeaway

WTTR is undervalued at current prices for the growth they are experiencing. They may continue to be, but sooner or later the market will re-rate this company higher.

On a technical basis, WTTR is trading above their 50 and 200 Day SMAs, and has recently bounced off support at $7.40 per share. There are no signs of big institutional buys...yet, so we could be ahead of the Smart Money on this one.

On a one year TTM basis, WTTR trades at 5X EV/EBITDA. Not super cheap, but we are interested in the growth they have demonstrated. On an NTM basis, they trade at 3.78X, which is more in the range of where we might make a speculative buy. A share price of $11 would take them to 4.2X and I think should be easily obtained. Now to throw a little more grease on the fire, ARIS is trading at 7.14X EV/EBITDA. If the market were to re-rate them to that multiple, the share price would be ~$21. All that is speculation but one day investors will sniff this one out.

WTTR has recently introduced a capital returns program that includes a $.05 quarterly dividend and a share repurchase program. CEO John Schmitz commented in the call in this regard-

The board of directors has reactivated our share repurchase program with an additional $50 million authorization. This gives us a total authorization of $58.5 million when taking into account the remaining $8.5 million left on the prior authorization. I believe this targeted repurchase program provides an attractive incremental return opportunity for our shareholders and great supplement to our existing base dividend program.

Taking down the share count makes total sense at these prices.

For further details see:

Select Water Solutions: Beat The Smart Money For Once [Maintaining A Buy]