SLQT - SelectQuote: Still Risky After Falling 96% From Its Peak

2023-09-01 13:23:14 ET

Summary

- SelectQuote, a publicly listed insurance sales agency, has seen a significant decline in its stock value, losing 96% of its value since its peak in 2020.

- The company has struggled with negative free cash flow and a growing debt level, with debt exceeding its market capitalization by a factor of 3:1.

- SelectQuote's recent financial statements show a decrease in submitted and approved policies, indicating larger business woes and raising concerns about the company's future prospects.

- Stay away from this stock.

One of the first books I ever listened to in the World of investing was Peter Lynch's "One Up On Wall Street" and in hindsight, it was the perfect book to initiate myself into this complex, yet fun World. The book was only about 2 to 3 hours long to listen and was explained in pretty simple, common sensical terms. One of the best advices in this book was to not underestimate your own knowledge as a consumer, thereby suggesting to buy the stocks of companies whose products and services you love.

While we can argue cause and effect, I own stocks in companies whose products or services me or my family use. For example,

- I love Google's suite of products and Android's simplicity. I own shares in Alphabet Inc. ( GOOG ) (GOOGL)

- I've been an American Express ( AXP ) customer for very long time and am generally pleased with their services, offers, and rewards. This encouraged me to buy the stock every time it went on sale, like during the COVID crash.

- Of course, my family ships a ton of products using Amazon.com ( AMZN ) and we enjoy Prime Videos.

Hence, it has long been ingrained in me to look up whether a new company I had a good experience with recently is a public company or not. I recently interacted with SelectQuote, Inc. ( SLQT ) as I was shopping around for better deals on my life insurance. I liked their service in general, in particular the response time and attention to details. I was able to switch my policy like-for-like but saved 30% in premium.

Although I've heard of SelectQuote and even vaguely recalled working with them when I got my original policy 7 years ago, I was surprised to see they are a publicly listed company. I wondered how did I not know this for 7 years. I got my answers upon digging a bit deeper. Just because I liked their service, does the Peter Lynch rule kick in immediately? I am not so sure on this company. Let's find out why.

Introduction

SelectQuote, in their own words , is "America's #1 Term Life Sales Agency" and was founded in 1985. SelectQuote, as the name indicates, helps customers find their best rates on insurance policies, typically on Life insurance but also on Auto and Home.

{kind=link}

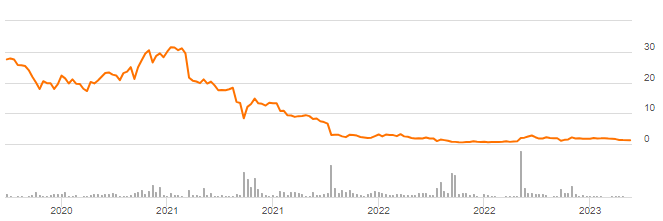

Since a successful "virtual" IPO at the peak of the COVID pandemic in 2020 (this answered my question on why I did not know about it until now) that valued the company at $3.25 billion, SelectQuote's stock has lost 96% of its value from its all-time closing high of $32.28. That puts the company's market capitalization at $213 million as of this writing, which gets even more puzzling when you consider that SelectQuote reported $957 million revenue in 2022. That means, the company is right now trading at a price-to-sales multiple of 0.20. I am presenting a few reasons below why the low valuation is justified. Let us get into the details.

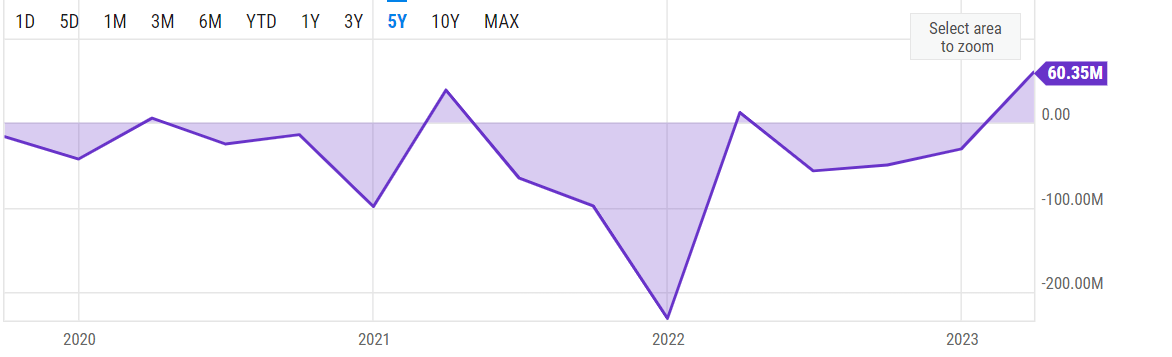

Free Cash Flow Woes

SelectQuote has had just 4 quarters with positive Free Cash Flow [FCF] out of the 15 quarters it has reported the data publicly. The average quarterly FCF in this period stands at -$40 million, while the median is at -$30 million. The mean and median being reasonably close to each other means this is a pattern and not a variation or a one-off in my view.

{kind=link}

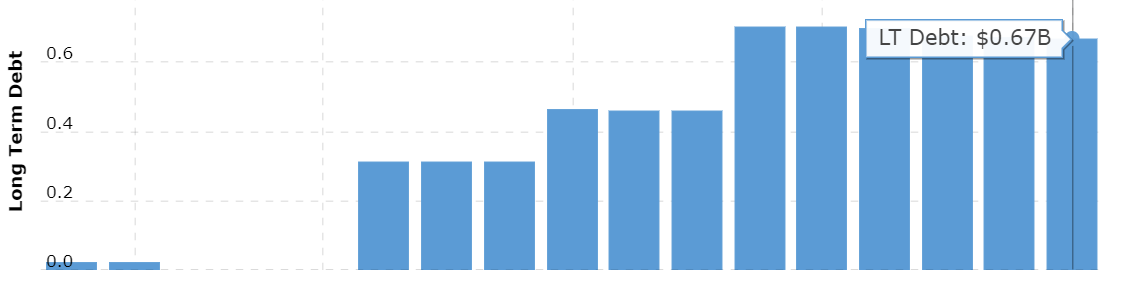

Debt Woes

As bad as the FCF section looks, the debt section below makes things worse for SelectQuote.

- The company's debt level has more than doubled from $310 million in June 2020 to $670 million in 2023.

- SelectQuote's debt exceeds its market capitalization by a factor of 3:1, which is always a warning for companies that maybe drowning in debt.

- With a debt-to-equity ratio of 1.70 , SelectQuote borrows nearly twice as much as it contributes/owns to keep its business running.

- Finally, with interest rates ballooning, it is no surprise that SelectQuote's high debt is getting to be more of a concern. In the March 2023 quarter, SelectQuote's interest expense on debt went up nearly 75% YoY to reach $21 million. That is, SelectQuote is paying 10% of its current total worth in interest expense each quarter.

{kind=link}

Interest Expense in Thousands (ir.selectquote.com)

{kind=link}

Cutting Down The Wrong Expense?

Another problem I noticed in the company's recent financial statement is that while overall operating costs and expenses went down 2% YoY, the bulk of it came from slashing marketing and advertising expense by nearly 30%. On the other hand, Selling and administrative cost went up by 12.50%. In a highly competitive market (which has direct sales channels as well without middle layers like SelectQuote), advertising expenses are a sales agency's lifeblood.

SLQT Expenses (ir.selectquote.com)

{kind=link}

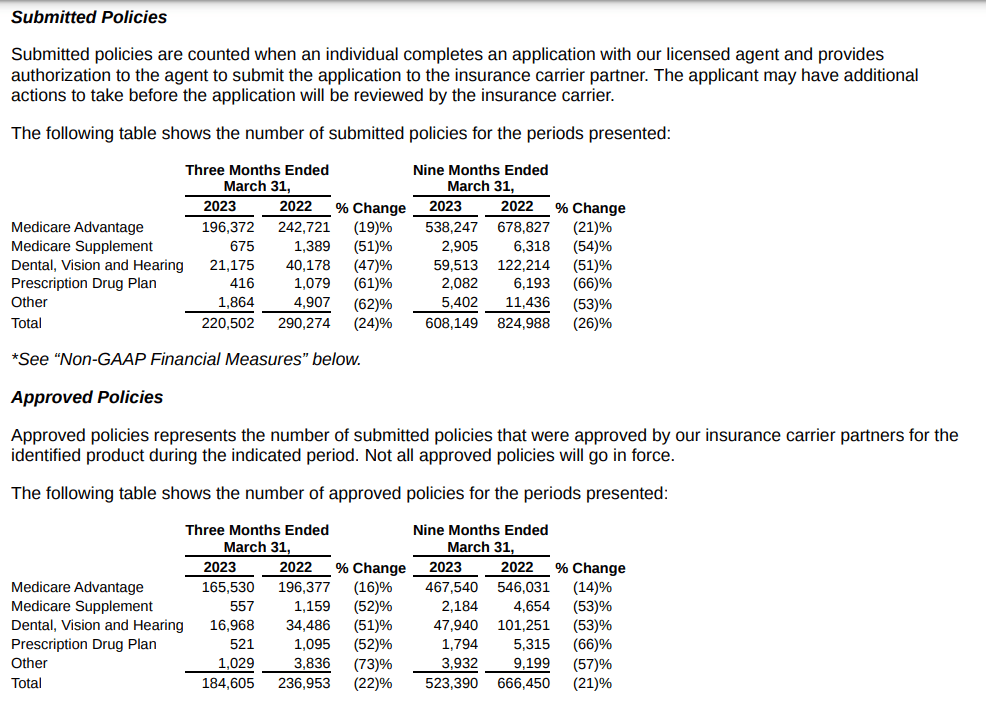

Business Woes

All the three sections above are effects of a larger problem, which is described below. In the most recent earnings report, SelectQuote's submitted and approved policies both showed substantial decreases across all categories, as shown below. Although the lifetime value of commissions per approved policy went up marginally in some cases, like Medicare Advantage, the overall volume decline was too large to be offset by small gains here and there.

Policies Count (ir.selectquote.com)

{kind=link}

Where Could My Thesis Go Wrong?

Although I am skeptical about SelectQuote's ability to survive in this mode, much less turnaround, I am presenting a few reasons where my thesis could go wrong.

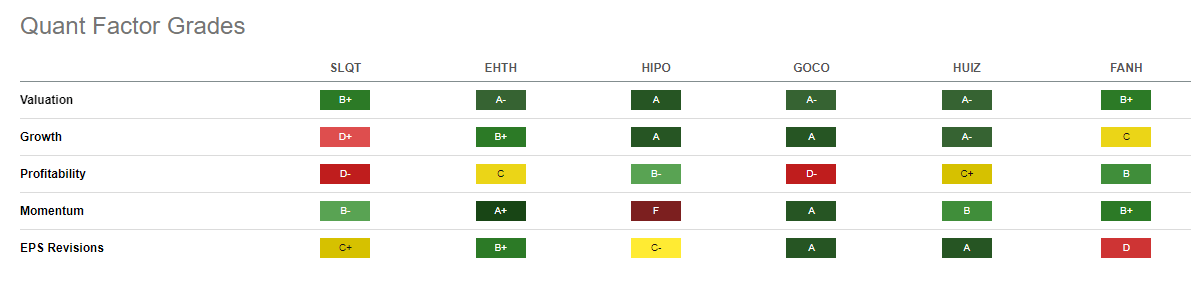

- Valuation: The stock appears attractive enough on a valuation basis, especially when you consider sales related metrics like EV/Sales and Price/Sales, as Seeking Alpha has noted here . But this appears like an industry-wide trend, as 4 out of 6 competitors identified below have a better rating than SelectQuote on valuation. In addition, likely due to the reasons discussed above, SelectQuote also has the worst rating on Growth and Profitability. If the Financial sector in general, and insurance industry specifically, start to get a bid from the general market, I can see SLQT stock running up primarily on the valuation thesis.

{kind=link}

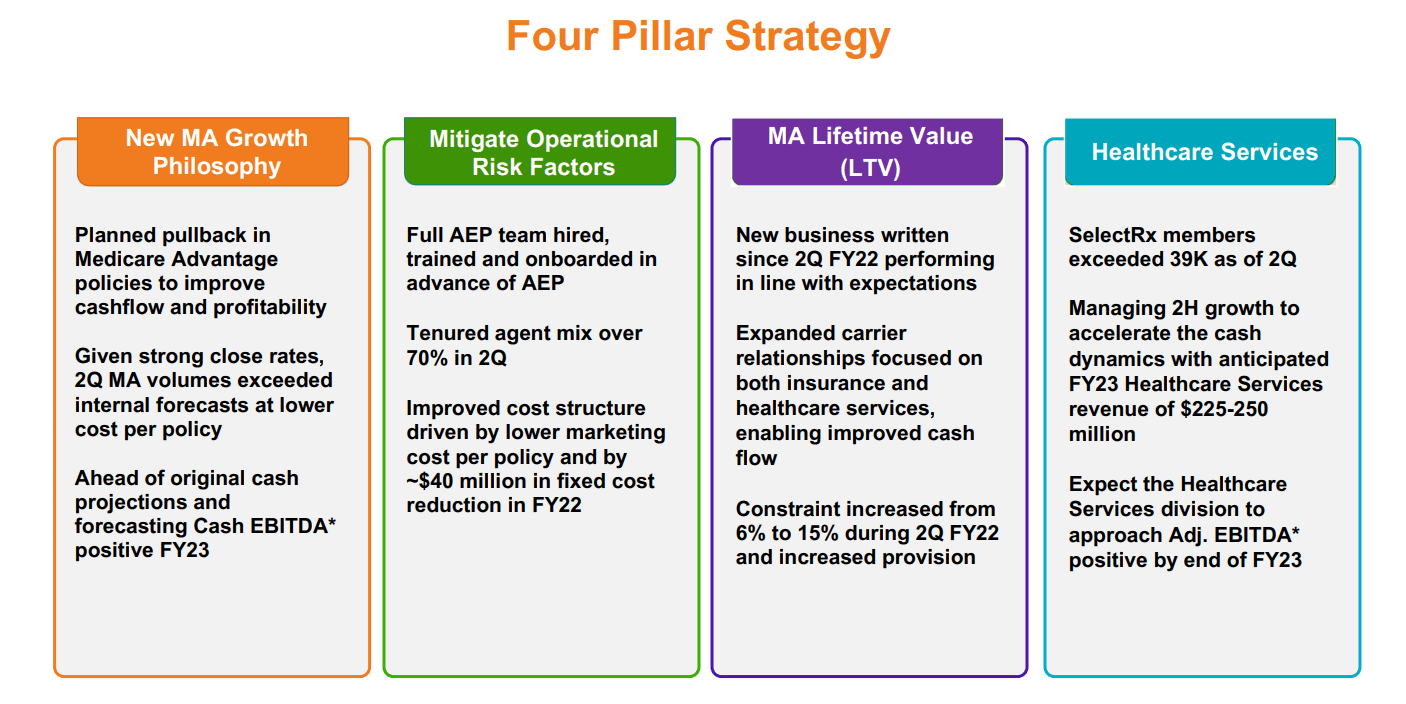

- Turnaround Story: In its December 2022 earnings presentation , SelectQuote highlighted the need for a turnaround in its business by highlighting 4 new strategic pillars. This strategy includes lowering cost while increasing agent tenure and being more selective in policy approvals with an aim of helping the company meet its EBITDA goals. As a sign of confidence in the new strategy, at least 5 different insiders, including the CEO, recently purchased shares directly. As Peter Lynch professed, insiders sell for a variety of reasons but buy only for one reason: they believe the stock is undervalued.

{kind=link}

Conclusion

I did not follow SelectQuote when the company went public in 2020, so this is more of a rhetorical question. How did this stock breach $30 in 2021? I am aware we were in a post-COVID bubble fueled by The Federal reserve's monetary policies, but that alone does not answer it. The company's own admission about being going-concern did not help things when the overall market was deflating in 2022, but the numbers since then have not been exactly appeasing either. This is one of the few instances where I wish Seeking Alpha has a "stay away" rating, as the stock is too risky to suggest even a "Hold" rating and current holders may be too deep in their losses for the exit to make any sense. As for Peter Lynch, I am sure he didn't buy the stock of every company he liked, but merely intended to use that technique as the starting point in doing further analysis. Some stocks are cheap for a reason, and I believe SelectQuote is one of them.

For further details see:

SelectQuote: Still Risky After Falling 96% From Its Peak