LHX - Sell Alert: 2 Overvalued Dividend Sells And 2 Great Replacement Buy Opportunities

Summary

- In this choppy market, taking gains on overvalued dividend stocks protects your capital.

- Reinvesting them in undervalued stocks has many benefits, including an increase in income.

- Here are 2 sells & 2 replacement buys.

Written by Sam Kovacs.

Introduction

A couple weeks ago, I highlighted 3 dividend stocks which in my mind were clear sells, and provided suggestions as to which stocks would provide great alternatives.

The article was well received by most, but some didn't seem to understand the logic or the math, even though I provided extensive resources and articles to fully grasp the content.

Therefore before going into the details of today's article, I will explain the core mechanics of:

- How selling a stock can increase your dividend income.

Without further ado, let's get to it.

Why selling stock can increase your income

Many dividend investors get caught up with the idea of yield on cost.

They'll say things like :

I bought Coca-Cola ( KO ) at $20 in 2009, I have an 8.8% yield on cost, I'm never selling."

This ignores the fact that The Coca-Cola Company yields 2.94% today.

It's an all-too-common mistake.

Yield on Cost is a "vanity metric." It allows you to look back and confirm that:

- You bought a stock at a great price (and thus yield)

- The stock increased its dividend considerably over time.

But this ignores the all-too-common pitfall that your yield on cost does not consider the opportunity cost of holding the stock today.

If KO yields 2.94% today, maybe there are better investments which yield more, or that yield the same but have better dividend growth potential.

Sure you could own KO, or you could do even better by buying something undervalued with better yield and/or growth.

I know if you're not convinced, you're having doubts now: what about tax? What about the replacement investment?

No worries, we will get to those soon.

To get there, let's start with a simple example.

Simple example

Say you buy stock A for $100. It yields 4%. So you get $4 in annual dividends.

Now let's say over the next year it has a phenomenal year and doubles to $200. But the dividend remains the same.

You still only have one stock. It still only pays $4 per year.

The current yield is 2%.

Your yield on cost is 4%.

You're chuffed.

But if you're a dividend investor, how would you feel about getting $8 in dividends per year on your investment rather than $4?

If you're like me, this sounds like an interesting proposition.

Let's say you sell your 1 share of stock A for $200.

You find another stock, let's call it stock B, which trades at $10 and pays $0.4 in annual dividends per share: a 4% yield.

With your $200, you can buy 20 shares of B. You get 20x $0.4 per year = $8.

And the magic is done.

If you ascribe to the idea that it is a market of stocks and not a stock market, that is to say there is always something undervalued and something overvalued, then moving from one quality investment to the next in such a fashion can do wonders for your income and performance.

Ok Sam I get this... BUT WHAT ABOUT TAX?

Ok let's say you need to pay 20% capital gains tax.

You sell for $200, have a capital gain of $100, so you will have to pay $20 in tax.

When all is said and done, you now have $180 to reinvest.

You buy 18 shares of B for $10 a share, and you'll receive 18x $0.4 = $7.2

This is still an 80% increase in your income.

The trade still makes sense if realizing value and increasing your income potential in retirement is your goal.

A real life example

Before going into today's sells and replacement buys, let's just run through a real world example using a couple of stocks suggested in the past article: Walmart Inc. ( WMT ) and Target Corporation ( TGT ).

I'll try and make the example as extreme as possible, with you buying WMT at an extremely low price.

Let' say you bought Walmart 30 years ago for $15 per share.

Walmart now trades at $147 and pays $2.24 in annual dividends. That's a 1.52% current yield.

But your yield on cost is 15%.

How can you ever sell, you might wonder?

If you chose to sell WMT for TGT, here is how it would work out, assuming a 20% capital gain tax.

You'll sell your share at $147, realizing a $132 capital gain, of which you'll give 20% or $26.4 to the government. Let's say you want to help out uncle Sam and round it up to $27 in tax.

Taking out $27, you're left with $120.

$120 will buy you 0.72 shares of Target which currently trades at $166. (Of course in practice you're selling more shares of WMT and likely not buying fractional shares, but let's go along with it for the example).

Target pays $4.32 in dividends per year.

Your 0.72 shares will get you 0.72x $4.32 = $3.11

Your income just went from $2.24 to $3.11, the government's paid, and Bob's your uncle.

That's a 38% increase in income. Sure, it would have been more if you didn't need to give a chunk to the government, but even if you do it can be worthwhile, as is clearly the case here.

Even more so when you consider that WMT is overvalued and TGT is undervalued, but if you want to read about that, check out the article I linked in the intro.

Just think about it, a 38% increase in income is like the difference between $72,000 in annual dividends and $100,000 in annual dividends. Do this time and time again throughout your investment career, you will come out on top.

Right, with that covered, we can move to today's buy and sells.

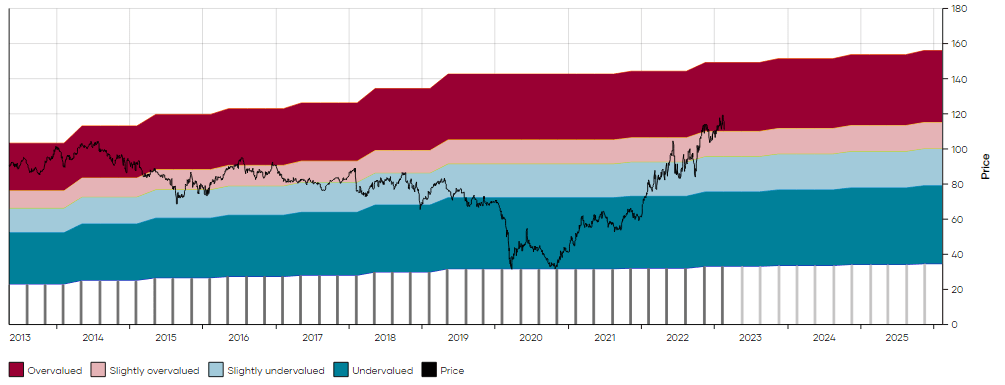

Sell Exxon Mobil

Exxon Mobil Corporation ( XOM ) currently yields 3.12% vs. its 10 year median yield of 3.8%.

The stock has had one heck of a run in 2021 and 2022. From a price of $33 in November 2020, XOM stock has risen to over $117 this year, and currently sits at $111. That's up 236%.

In the High Yield portfolio (a model portfolio available to Dividend Freedom Tribe members) we initially bought XOM in March 2021 at a cost of $45 per share. We eventually exited our position at a cost of $110, which was a nice double.

What's crazy is that we thought we were somewhat late to the game, as we were piling into stocks like Chevron Corporation ( CVX ) as early as the summer of 2020, and stocks like ONEOK, Inc. ( OKE ) as early as spring of 2020.

{kind=link}

Still, it worked out just right.

We bought XOM when it yielded pretty much twice as much as it currently does.

It was much easier to get behind the stock when it yielded over 6% than it is at 3%.

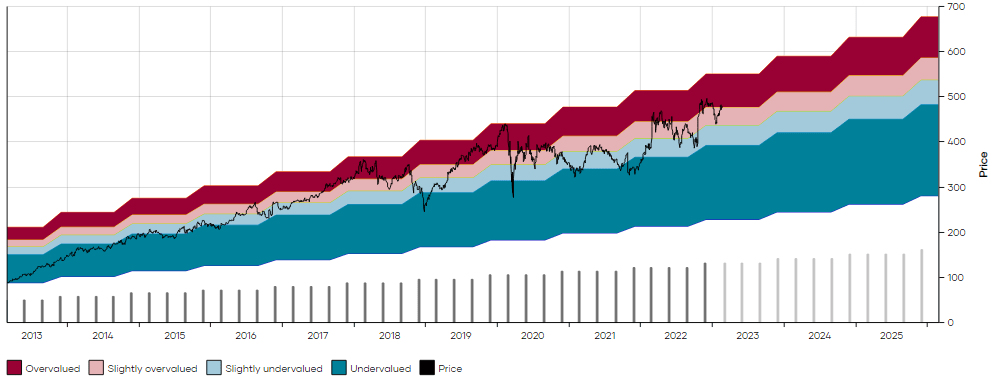

In fact, if you take a look at the 10 year MAD Chart, you can see that right now XOM is in historically overvalued territory.

(Check out this article for more details on MAD Charts.)

When you have a 3% yielding stock, you're generally looking to get 8%-9% annual dividend growth to get quality returns (our rule of thumb based on some more complex calculations which I'm not gonna dive into here).

XOM's dividend growth of 3.4% this past year, and at the same CAGR during the past 5 years isn't in sync with its current yield.

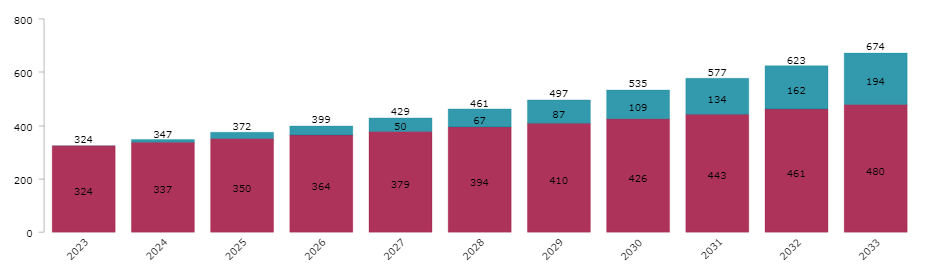

Let's say you have $10K worth of Exxon today, and the dividend grows at 4% per year for the next ten years. Let's also assume you reinvest dividends at the current yield.

{kind=link}

Then in 10 years you'll receive $674 in annual income, or 6.74% of your current investment.

Keep this number in mind when you compare it to EOG. If you think it's pretty good, let me tell you it is underwhelming.

Investors would be well served by cutting their exposure to XOM stock, and reinvesting it in another Oil & Gas stock which is undervalued and has a lot better growth potential.

...Buy EOG Resources

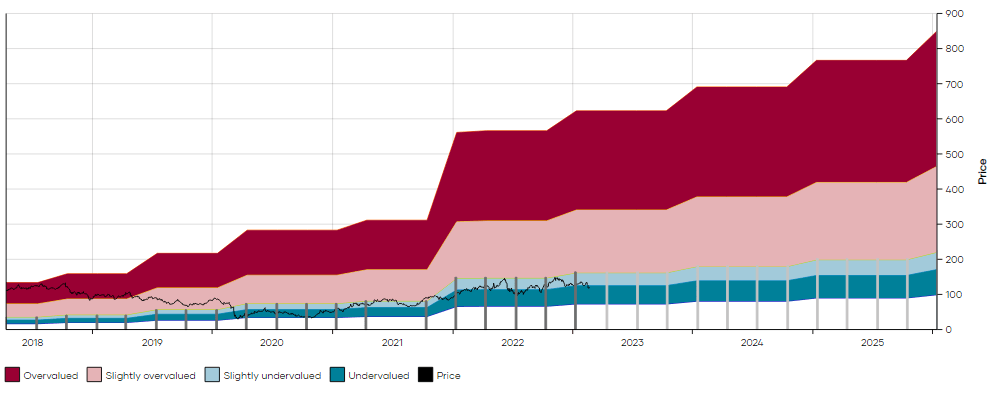

EOG Resources, Inc. ( EOG ) is, I believe, the most undervalued high quality U.S. energy dividend stock out there;

The stock yields 2.8% vs. it 5 year median of 2% and 10 year median of 0.8%.

Now, I'm not saying that EOG should yield 0.8%. I don't think it should.

It is clear by looking at the 10 year MAD Chart that the rate of dividend growth changed drastically after 2017.

{kind=link}

Therefore, looking at 10-year ranges of dividend yields doesn't make much sense, and narrowing in on the past 5 years can give us a better picture.

What this chart shows, is that since 2020, the stock has yielded mostly between 2% and $4.61.

{kind=link}

But those numbers mask the real dividends received by EOG in past years.

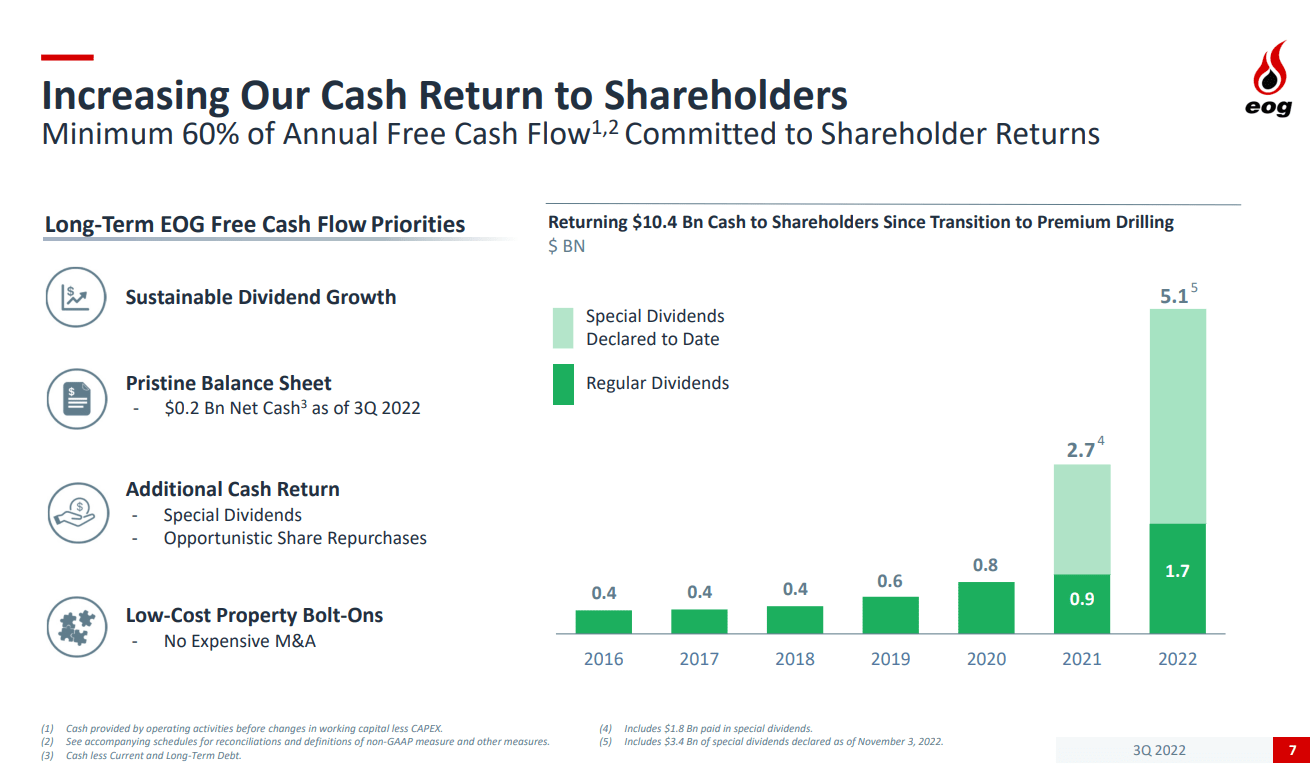

As you can see in the chart below, which was taken from the 3rd quarter earnings presentation, EOG has been returning large amounts as special dividends.

{kind=link}

This is an interesting way to return excess cash to shareholders without having to maintain an extremely high dividend, which could not be afforded in a market downturn.

In 2022, investors received $3 per share of regular dividends, and $5.8 of special dividends.

This year, the dividend was increased by 11%.

Investors can look forward to further special dividends, as the company has a very low cost of drilling and provides significant positive returns when WTI is at $40 per barrel. It's currently at $76.

But even if "all we got" was a continuation of 11% dividend growth for the next 10 years, it would be so much better than holding onto an Exxon investment.

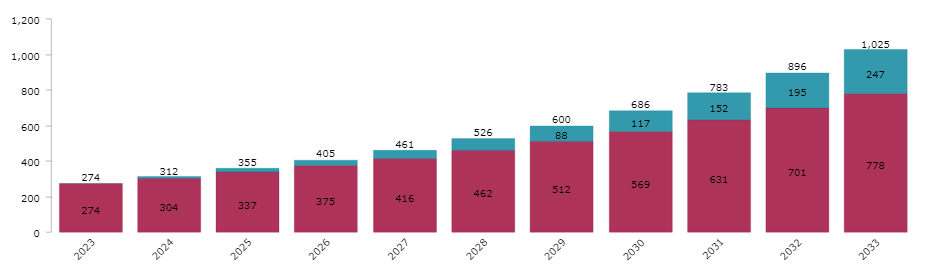

Say your $10K was in EOG instead.

Say your reinvested dividends every year at the current yield while the dividend grows at 11% per annum.

{kind=link}

10 years from now you'd be looking at $1,025 in annual income, or 10.25% of your current investment.

Down the line, that's a 52% difference from what you'd likely get from Exxon 10 years from now.

At scale, that's a difference between a $100K dividend income and $150K dividend income in 10 years.

This stuff matters, fellas!

This is a great example of how selling a stock with a slightly lower yield can still be a better decision for your income down the line.

Of course, here with EOG, you get your cake and eat it too, because the high special dividends more than make up for the slightly lower yield today.

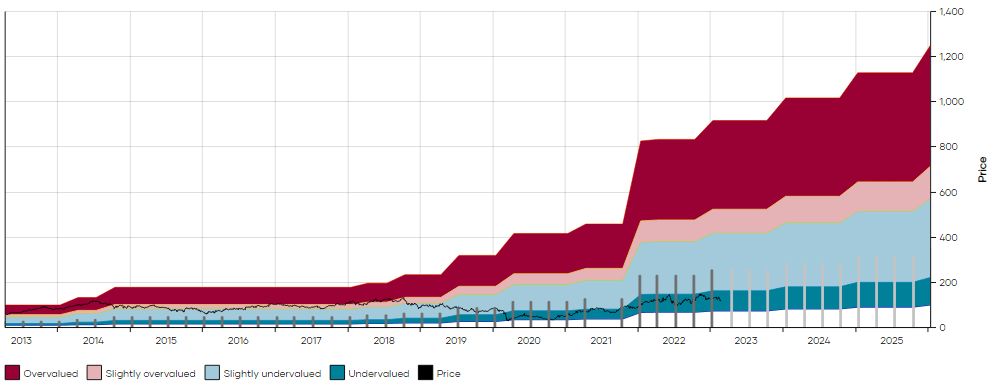

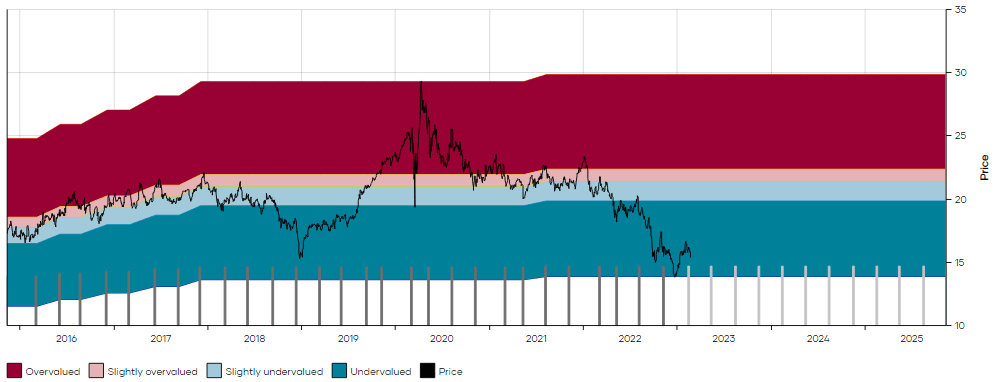

Sell Lockheed Martin

This second example will be a classic case of "yielding up." I don't know if you watched how I met your mother (I mean, the TV show...). Barney always tells Ted it's time for him to "Suit up."

Well, my friend, I don't care if you're wearing a 3-piece suit or, like me, donning board shorts and a linen short sleeve, I want you to "Yield up."

Yielding up is the more classic case of selling a low-yielding stock and buying a higher-yielding stock to increase your income instantly and in the future.

Lockheed Martin Corporation ( LMT ) has been on quite the run during the past 2 years.

Following Biden's election in 2021, we wrote an article when defense stocks were being bashed because "Democrats would cut the DoD budget." That hasn't happened. We suggested it wouldn't happen because of the geopolitical threats. I was more concerned with China than Russia at the time, but anyone who hasn't been living under a rock for the past 2 years now has come to appreciate that a strong defense program will be essential for the U.S. to maintain a strong leadership position in a multipolar world.

The report which we wrote for DFT members in January 2021 led us to successful investments in Northrop Grumman Corporation ( NOC ), which we exited before the stock tanked, and L3Harris Technologies, Inc. ( LHX ), which we are still holding.

In so far as LMT is concerned, we initiated the position in our Hybrid Yield portfolio at a price of $320 in 2021 and exited at an average cost of $470.

It's fine to leave some upside on the table, when you're shifting to value.

Today, the stock yields 2.5% vs a 10-year median yield of 2.75%.

This places it in its overvalued range, as you can see in the MAD Chart below.

{kind=link}

Remember that being overvalued doesn't mean that the stock can't go up more.

Heck, LMT could go up to $550 before topping.

But it is just as likely for the stock to go back down below $400.

You don't need to buy at the bottom and sell at the top, only close enough to the bottom and close enough to the top, for this to work.

LMT has dividend growth of 7.1% this last year and an 8.4% CAGR over the past 5 years.

What is worrying with LMT is that the dividend increases have been slowing down over the course of the past decade, from double-digit growth 10 years ago to 7% growth now.

I believe 6-8% growth is possible for the stock over the next decade. Let's split the difference and call it 7% growth going forward.

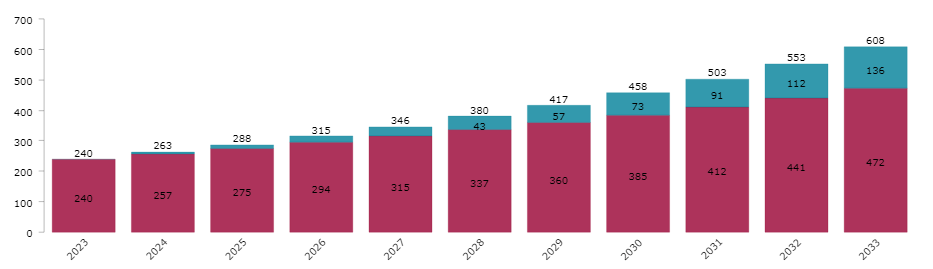

Once again, let's suggest that you have $10K invested in LMT (disregarding your purchase price and whatnot).

This is the year-by-year income you can expect from LMT if you reinvest dividends and the dividend grows at 7%.

{kind=link}

In 10 years, you'd be looking at receiving $608 in annual income.

This is subpar, and you should consider selling it and buying another stock.

The only problem is that, unlike with the Exxon / EOG exchange, there is currently no good alternative among LMT's direct peers.

General Dynamics Corporation ( GD ) is overvalued and on our sell list. So is Northrup Grumman. LHX is on our watch list. Booz Allen Hamilton Holding Corporation ( BAH ) is also on the Watch list.

Nothing which is obviously worth buying.

So we're going to have to be a little more creative.

...Buy Easterly Government

Easterly Government Properties, Inc. ( DEA ) doesn't sell arms to the American government's various military branches.

Instead, it rents real estate to government agencies, which are indirectly impacted by large defense programs: think CIA, Veterans Affairs, that sort of institution.

DEA currently yields 6.9% after having rallied somewhat since we reiterated our buy rating for members of the Dividend Freedom Tribe in January, at the request of one of our members. (Yep, our members get to vote for what we cover.)

{kind=link}

One thing to be considered is that DEA currently hasn't grown its dividend more than once since 2017.

As far as I'm concerned, you can expect exactly 0% dividend growth from DEA.

DEA is not a stock without its challenges. There is a justification for the high yield, but not one you should be alarmed by.

As I said to members of the Dividend Freedom Tribe in an update in January:

Structurally, DEA isn't perfectly set up for the current environment.

Whilst its tenant quality is as high as possible (the government), it bears the full cost of inflation.

Government leases are generally full service, meaning the owner pays all the expenses.

Unlike triple net REITs which pass on most expenses, DEA is stuck footing increasing bills.

What's more, is that only 5% of DEA's leases have inflation ladders, whereas the rest are fixed.

This means that revenue isn't indexed to inflation.

So while they have a fixed cost of capital, they don't have the ability to grow much.

And this somewhat puts in question my long term assumption of 2% dividend growth.

DEA has an FFO payout ratio of 85%, which while on the higher end, is not unusual.

I have no doubts that the dividend will be kept constant: there is no real pressure to cut it, and there is no real opportunity for growth.

But when you can get a 7.16% yield, you don't really need to get any growth.

If you're still accumulating, the reinvestment of a high yield leads to higher dividends each year.

Well, the stock currently yields 6.9%, not 7.1% as it did then, but the thesis is pretty much unchanged.

In November, the company sold 10 of its 95 properties to redeem a significant piece of floating rate debt. It now has a floating rate debt exposure of 1%, meaning that virtually all of its debt is fixed.

This is good in the current environment, which is squeezing cap rates.

Even a flat dividend when as high as 6.9% can compound brilliantly if you reinvest it year after year.

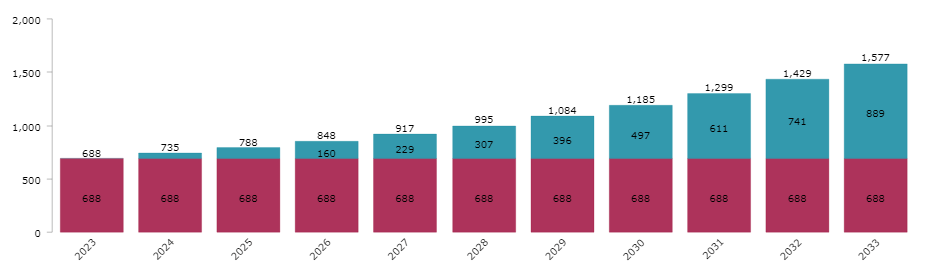

Let's say that your $10K in LMT got reinvested in DEA (no tax assumed, but I've showed you how to adjust for your personal tax estimate in the intro) today.

If you just reinvested the 6.9% every year, and the dividend never grew, this is what your income would look like in 10 years.

{kind=link}

In year ten you'd be looking at $1,577 in annual income.

This is 2.75X more than with an LMT position.

What's more is that if the market readjusts DEA's yield downward and LMT's upward, there might be an opportunity or two to flip back and forth a few times in the next decade (or even move to yet another stock) and considerably increase your retirement income prospects.

2.75X more is the difference between having $36K in annual dividends and having $100K.

Which would you rather have?

Conclusion

Buying low, selling high does wonders for your portfolio. It allows you to capitalize on opportunities to the downside and to the upside. You're a more versatile investor.

This versatility boosts your income and returns in good times, makes up for any errors of judgement you might make at some point, and overall leaves you ahead of the pack.

Buy low, Sell High. Get paid to wait!

For further details see:

Sell Alert: 2 Overvalued Dividend Sells And 2 Great Replacement Buy Opportunities