RTL - Sell Alert: 5 REITs That Likely Will Cut Their Dividends

2023-03-16 08:05:00 ET

Summary

- Quite a few REITs are struggling.

- Interest rates are way up and debt maturities are approaching.

- I highlight 5 REITs that will likely cut their dividends.

Contrary to what you may commonly hear, most REITs ( VNQ ) are doing just fine today.

Their balance sheets are the strongest they have ever been and so the impact of rising interest rates isn't significant.

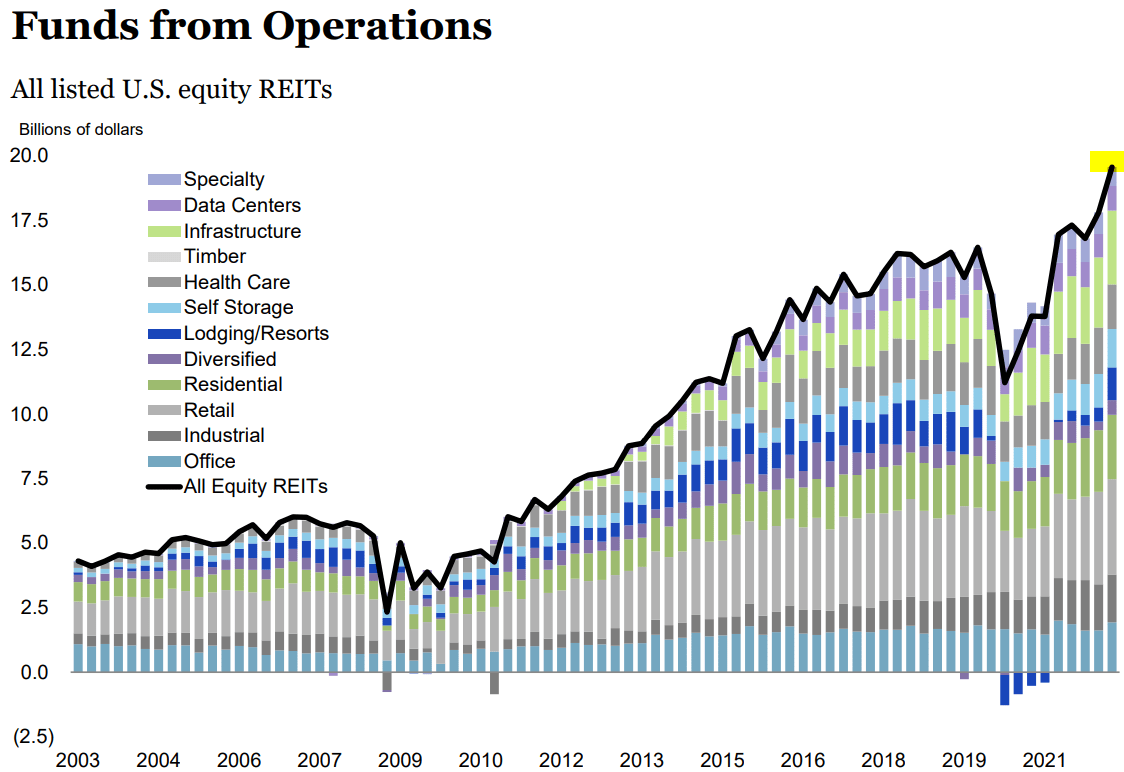

Moreover, the high inflation led to a surge in rents, pushing REIT cash flows to new all-time-highs in 2022:

{kind=link}

This then fueled large dividend hikes across the sector. More than half of REITs hiked their dividend in 2022 and only a few cut their dividend.

But this could change in 2023.

Interest rates have surged a lot higher, little transactions are happening, debt maturities are approaching, and a near-term recession appears very likely. There is also a growing risk of a banking crisis with the recent collapse of Silicon Valley Bank ( SIVB ), the second-biggest bank failure in history. If it leads to more bank runs, things could rapidly get really nasty...

Most REITs should be fine either way because they have been conservative with their finances, but that's not the case for every REIT.

In what follows, we highlight 5 REITs that are at high risk of a dividend cut in 2023. I would avoid these names because a dividend cut could lead to significant downside risk:

Office Properties Income Trust ( OPI )

Office REITs are struggling right now and it has led some to cut their dividend in recent months.

SL Green ( SLG ) and Vornado Realty Trust ( VNO ) both cut it by a third.

The physical occupancy of offices remains very low and it is causing companies to rethink their office footprint.

SL Green

Worst case scenario, this means that the office market is severely overbuilt and rents/occupancy rates will suffer significantly for years to come.

In the best case scenario, people return to the office, and demand bounces back, but even in this best-case scenario, landlords will need to heavily reinvest in their properties. The high capex will eat into the returns of landlords.

And finally, the base case scenario, probably the most likely, lies somewhere in the middle.

But not all office buildings are equal. Some will do worse than others, and I fear that the worst positioned are single-tenant net lease office buildings. These are typically older buildings that are at the mercy of a single tenant and they will require a lot of capex to adapt to the changing world. The tenants hold all the bargaining power because they know that their landlords want to avoid a vacancy at all cost.

Office Properties Income Trust

One REIT that owns a lot of such assets is Office Properties Income Trust ( OPI ). So far, it has managed to maintain its dividend because it has years left on its leases, but it now has 30% of its leases expiring in the next 2 years, and that will likely prove to be too much for the company.

Its dividend may seem safe based on its 66% payout ratio, but I want to remind you that its close peer, Orion Office REIT ( ONL ) only pays out 22% because it knows that capex will be huge in coming years.

It also doesn't help that OPI has a fair bit of leverage and the management is one of the most conflicted in the whole REIT sector.

I would avoid this name. If you want to invest in the office space, then SLG, VNO, or even Boston Properties ( BXP ) are much better options. At least, they own Class A multi-tenant properties.

Global Net Lease ( GNL )

GNL is similar to OPI, but its portfolio is a bit more diversified. It is not just a pure play on single-tenant office buildings as it also owns some industrial properties. This seems to reassure some investors because the industrial sector has done really well in the past years. The rents of REITs like Prologis ( PLD ) have been growing at a very rapid pace.

Global Net Lease

But here are the issues:

It still owns a lot of single-tenant office buildings, representing about 40% of its portfolio.

Global Net Lease

Its industrial properties are not comparable to those of Prologis. These are high cap rate / higher risk assets that could suffer in a coming recession.

The payout ratio is not sustainable at 93% of its FFO.

The management has a very poor track record, respectively raising equity at dilutive prices, and later cutting the dividend.

Another cut is likely.

Easterly Government Properties ( DEA )

DEA is also an office REIT that specializes in single-tenant office buildings and so it is impacted by the same issues.

But DEA is somewhat better positioned because most of its tenants are government agencies that are less likely to vacate their buildings.

Easterly Government Properties

Moreover, its lease maturities are still quite far out and the management is far better than that of OPI and GNL. In that sense, I think that DEA offers much better risk-to-reward and it has better chances of maintaining its dividend.

But even then, I fear that a cut will be inevitable because the payout ratio is today very high at ~90% and I doubt that the company will manage to retain enough cash flow to pay for all the capex that's coming its way in the coming years.

The government agencies will demand significant tenant improvements and some may even vacate their properties. Government agencies don't worry as much about the productivity of their workers (as private companies would) and so a larger portion of them may stay permanently remote.

Necessity Retail REIT ( RTL )

This one is simple so I will keep it short.

Too much leverage. Conflicted management team. Cyclical assets. High payout ratio.

I don't know how they could possibly escape a dividend cut.

They could push it a year or two, but the current payout does not seem sustainable in the long run and the company would likely be better off cutting it now to pay off debt.

One Liberty Properties ( OLP )

I am the least certain about this one.

I like the management and they have a pretty good track record.

Insider ownership is also significant so they are well aligned with shareholders and it surely isn't in their interest to crash the stock.

But here are the few things that cause me to worry about its dividend.

Firstly, this is a net lease REIT with just 6 years left on average on its leases. That's much lower than that of Realty Income ( O ), Essential Properties Realty Trust ( EPRT ), VICI Properties ( VICI ), and its other peers. It has nearly 30% of its leases expiring in the next few years:

{kind=link}

Secondly, the company owns a lot of retail properties that could become problematic. These are office supply stores, which are struggling in the day and age of remote work, and furniture stores, which are negatively impacted by the surge in interest rates. Few people are buying homes these days...

The industrial property exposure is significant, but just like GNL, these are mostly higher cap rate / higher risk properties that are more cyclical.

{kind=link}

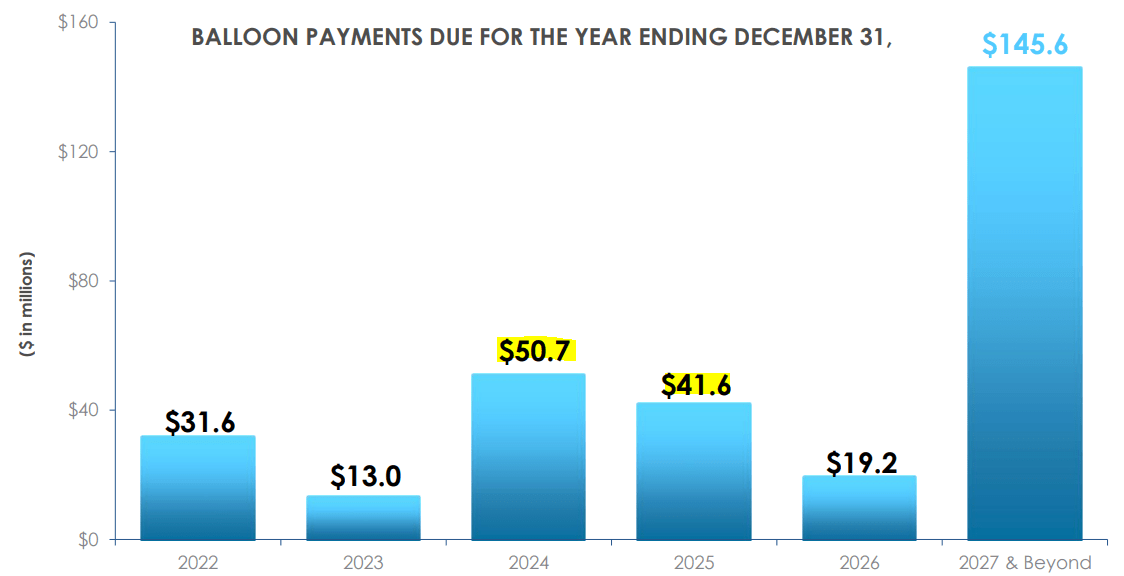

Finally, they have more debt than average and quite a lot of maturities in the next years:

{kind=link}

If the payout ratio was low, this wouldn't be a problem, but they are today already paying nearly all of their cash flow.

Their AFFO payout ratio was 92.3% last year. Can they sustain it? Maybe. But is the risk high? Yes, it is.

Bottom Line

Most REITs are doing just fine, but there are over 200 REITs out there and so it shouldn't come as a surprise that some are suffering.

The key here is to be selective.

At High Yield Landlord, we invest in just one REIT out of ten that we analyze on average:

High Yield Landlord

For further details see:

Sell Alert: 5 REITs That Likely Will Cut Their Dividends