NVTA - Sema4: Restructuring Plan Figures Don't Add Up

Summary

- Sema4's restructuring plan has a number of potential downsides that could affect the company's cash position in the coming few quarters.

- The booting of the CEO signals the start of a strategic focus on short-term survival away from long-term growth.

- Even if management succeeds in fully realizing restructuring goals, it barely has enough cash for the next twelve months.

Investment Thesis

Eric Schadt, Ph.D., a professor at the Icahn School of Medicine, set out to revolutionize medical care by integrating genomic analysis into routine clinical practice. He envisioned an ecosystem where clinicians could use genomic information to personalize treatment and improve patient outcomes. His idea took root in the University's hallways, culminating in the creation of Sema4 ( SMFR ). At its heart is Centrellis®, an AI-powered dynamic database with a powerful analytics engine that links DNA to clinical data to help doctors make better clinical decisions at the point of care.

With the arrival of cheap and effective gene sequencing technologies, many healthcare Key Opinion Leaders "KOLs" attracted investors to fund projects to pursue this ambition. But despite their good intentions, many failed to take genomics beyond the hype, such as iCarbonX ( CRBNX ), the market unicorn once described as the Google of biotechnology which has slowly withered away into obscurity, failing to deliver on its lofty promises of unveiling clinically-valid correlations between a patient's DNA and clinical, psychological, and behavioral data. Others faced a harsh reality riddled with reimbursement and technological challenges too complex to turn the promise of personalized medicine into reality, such as Invitae ( NVTA ) and SOPHiA ( SOPH ). As many have found out, our bodies are very complex, and health depends on much more than our DNA alone, spanning proteomics, metabolomics, epigenetics, and even environmental factors such as diet and lifestyle.

Mr. Schadt's position as a medical community member allowed him to build partnerships with selective hospitals that share his vision, differentiating Centrellis by incorporating real-time patient data from hospitals. Meanwhile, he built a molecular diagnostic lab, which found adequate success in carrier screening (for couples planning to have a baby), enough to appease investors, and fund, at least partially, his research and discovery ambitions. Beyond the molecular diagnostic business, Mr. Schadt also found an immediate market for Centrellis within the biopharma community, monetizing its algorithms by selling access to biopharma companies to generate insights into diagnostics and drug development research. Nonetheless, under Mr. Schadt's leadership, SMFR was far from profitability.

Still, after his departure, SMFR seems to have lost its strategic direction. Centrellis' longitudinal data integration is only possible through the company's partnerships and collaborations that Mr. Schadt has forged with many leading hospitals and research institutions. Thus, investors' panic after his resignation in August is justified. The following paragraphs discuss SMFR's strategic direction under the new leadership, recent developments, and financial outlook.

Recent Developments

When the GeneDx acquisition closed in May, its previous CEO was appointed as a co-CEO of the combined company. It is a rare instance in which two CEOs sit side by side at the same table to address shareholders. Three months later, Mr. Schadt was shown the door of the company he founded and the deal he negotiated, manifesting intensifying corporate politics as growth companies feel the heat as funding becomes tight in a dwindling market for healthcare startups.

Although corporate politics play behind the scenes, the discrepancies between Ms. Stueland's and Mr. Schadt's strategic focus are clear, with the former focusing on immediate market opportunities. At the same time, her predecessor pursued a more futuristic approach in his quest to revolutionize personalized medicine. Beyond the leadership change, I expect changes in the Board in the coming quarters.

SMFR's new CEO quickly implemented changes to address the key challenges weighing on the company's balance sheet. In August 2022, the company announced it was laying off 250 workers, exiting its somatic oncology segment, and closing its Bradford lab in Connecticut. Last month, the company announced it was laying off a further 500 employees and closing its Stamford lab while exiting the reproductive health market. These changes comprise the key components of the strategic plan devised by the new management to extend its cash runway until market conditions improve and equity markets become accessible again. For now, becoming a self-funding business is out of the picture, as one can infer from management's cash burn estimates.

What Happens Next

Management estimates a revenue run rate of $184 million after exiting its reproductive segment in January 2023, representing a 20% decline from the TTM that ended September 2022. From that, it seems that the company will retain some parts of what it reports as the "Complex Reproductive Health" business line on its presentations, which represent 44% of total revenue, and include items such as its Carrier Screening (for couples planning to have a baby), NIPT, for the detection of fetal abnormalities, and finally, prenatal cytogenetic testing, such as Karyotyping and chromosomal microarray analysis, all sub-segments that the company specifically announced it was planning to discontinue at the turn of the new year.

I don't know which components of the Complex Reproductive Segment the company plans to maintain, but what is certain is that the company will become smaller under the new leadership. Whether it will remain a standalone entity or be merged into a larger company remains to be seen. But either way, the company faces an uphill battle to sustain its balance sheet, control spending, and raise capital to continue as a going concern.

SMFR decision to exit the segments mentioned above will benefit its peers, including Invitae ( NVTA ), Natera ( NTRA ), and NeoGenomics ( NEO ), the market leaders in Carrier Screening, NIPTs, and cytogenic testing, respectively.

Going forward, the company will focus on pediatric genetic disease diagnostics leveraging its core assay platform and unique technology patents. This includes tests for the early detection of diseases such as cystic fibrosis and other genetic disorders affecting newborns and children.

Financial Position and Valuation

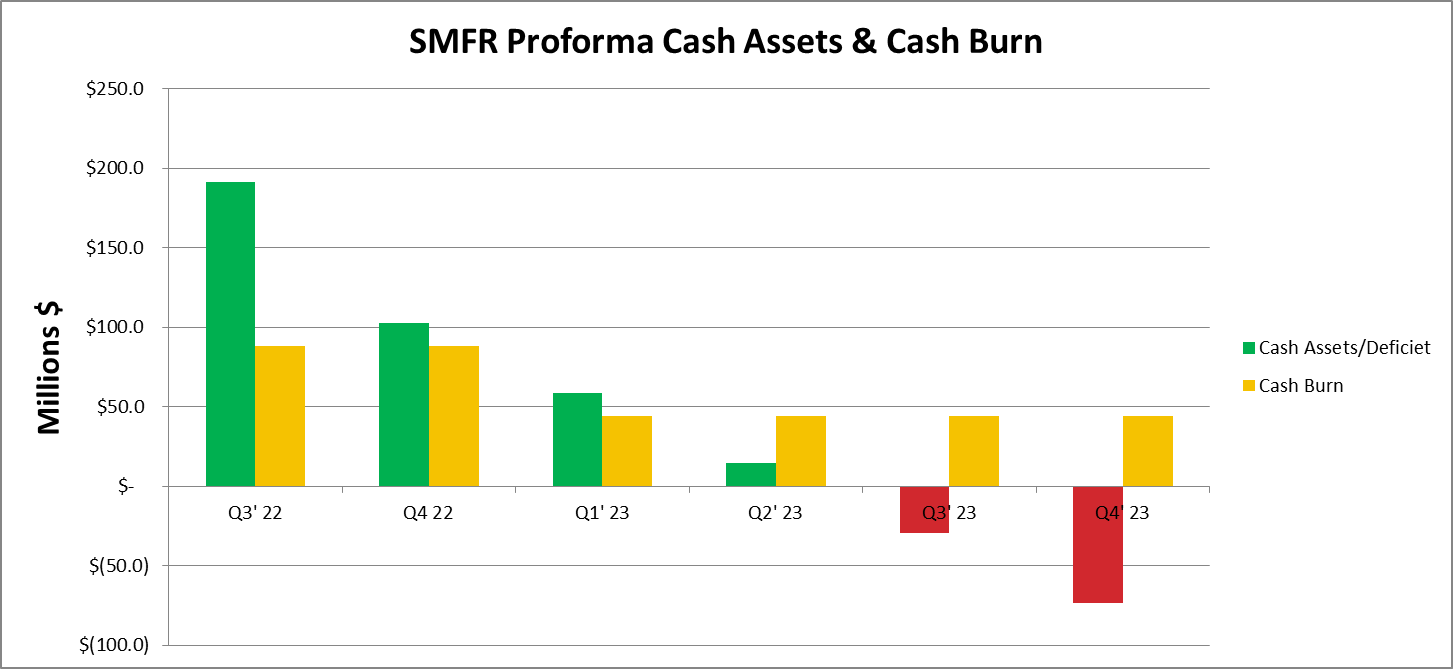

SMFR ended Q3 with a cash balance of $191 million, weighed against a $45 million quarterly proforma cash-burn rate in 2023, based on its restructuring objectives. Thus, the company barely has enough cash for the next 12 months, even if it fully achieves its reorganization targets, which is unlikely. Below I break down some key figures to frame the discussion further:

Cash burn projections predicate continued reproductive segment operations in Q4, pertaining a comparable cash burns as in previous quarters. We reflect management's cash burn assumptions (namely a 50% decrease in cash burn) starting Q1 2023. As shown below, even if management realizes its restructuring objectives, SMFR will be out of cash by Q3 2023.

SMFR Proforma Cash Assets and Cash Burn (Author's estimates)

{kind=link}

The graph above assumes immediate benefits of management's restructuring plans, but in reality, the figures could be much worse. R&D projects don't have a tap switch that can be turned on and off at will, so it's likely that the company will incur significant expenses as it pursues its restructuring strategy. Moreover, management's projected cash burn excludes severance charges, inventory write-offs, and reallocation expenses. Thus, while the company trades below its cash balance, investors should be wary of the downside risk from possible dilution risk and cash burn.

Summary

It has been a rough year for the molecular diagnostic industry, the nascent market that has exploded in recent years thanks to advancements in NGS that made gene sequencing cheaper and more accessible than ever before. With the market plunging, companies are finding it more challenging to raise capital to pursue the many attractive opportunities in the market.

Like many of its peers, SMFR is restructuring its business to adjust to these market conditions. However, unlike many others, it is shutting down one of its primary business segments, amplifying the uncertainty of this reorganization. It also eliminated senior positions, including its co-founder and visionary behind its platform technology. Although on the surface, the company seems to be oversold, the underlying business faces significant challenges in terms of cash burn and dilution risk.

The company is unlikely to raise equity given present market conditions, and even if it did, share dilution at current market prices will send its ticker lower. According to management's cash-burn estimates, becoming a self-funding business is also out of the picture. The company may use its $125 million credit facility to buy some time. Before this happens, I'm fleeing.

For further details see:

Sema4: Restructuring Plan Figures Don't Add Up