SERA - Sera Prognostics: The Pregnancy Company On A Hot Streak

2024-01-10 00:07:14 ET

Summary

- Sera Prognostics aims to become a global leader in women's health diagnostics, with a focus on pregnancy.

- It went public in July 2021 with promising prospects, but its revenues have been disappointing.

- The PreTRM test is Sera's principal revenue driver.

- Investors misread the recent DSMB decision as highly positive for the company, when it was in fact an unfortunate result.

This is my first take on Sera Prognostics (SERA). It bills itself as "The Pregnancy Company". Its lofty goal is to become a global leader in high-value women’s health diagnostics.

In this article I evaluate how it is pursuing this goal and importantly for investors how its ambitions look to play out for shareholders.

A company overview shows promising prospects although it is a bit tricky.

Sera was founded in Utah in 2008. It went public in 07/2021. On 0714/2021 it announced :

- the pricing of its initial public offering of 4,687,500 shares of its common stock;

- a price to the public of $16.00 per share with gross proceeds expected to be approximately $75.0 million;

- shares expected to begin trading on the Nasdaq Global Market on July 15, 2021 under the symbol “SERA”.

The Sera prospectus described its technology in glowing terms, listing key strengths as its:

- differentiated approach to understanding and addressing major conditions of pregnancy;

- proprietary and scalable proteomics and bioinformatics platform technology creating clinically meaningful and economically impactful predictions for pregnancy;

- proprietary PreTRM test which it characterized as the only broadly validated, commercially available blood test proven to predict the risk of an individual woman to deliver prematurely;

- innovative and strategic partnership with Anthem providing it early PreTRM test reimbursement with initial commercialization launched in H1 2021 — envisioned to open broad penetration of Anthem's network covering 10% of annual US pregnancies within a few years.

It characterized its Anthem arrangement as significantly derisking early PreTRM test reimbursement and opening the way to expedited PreTRM test reimbursement by other major payers.

To date as I write on 01/07/2024 this has not panned out as shown by the section below,

Sera has sufficient near term liquidity however its revenues are disappointing.

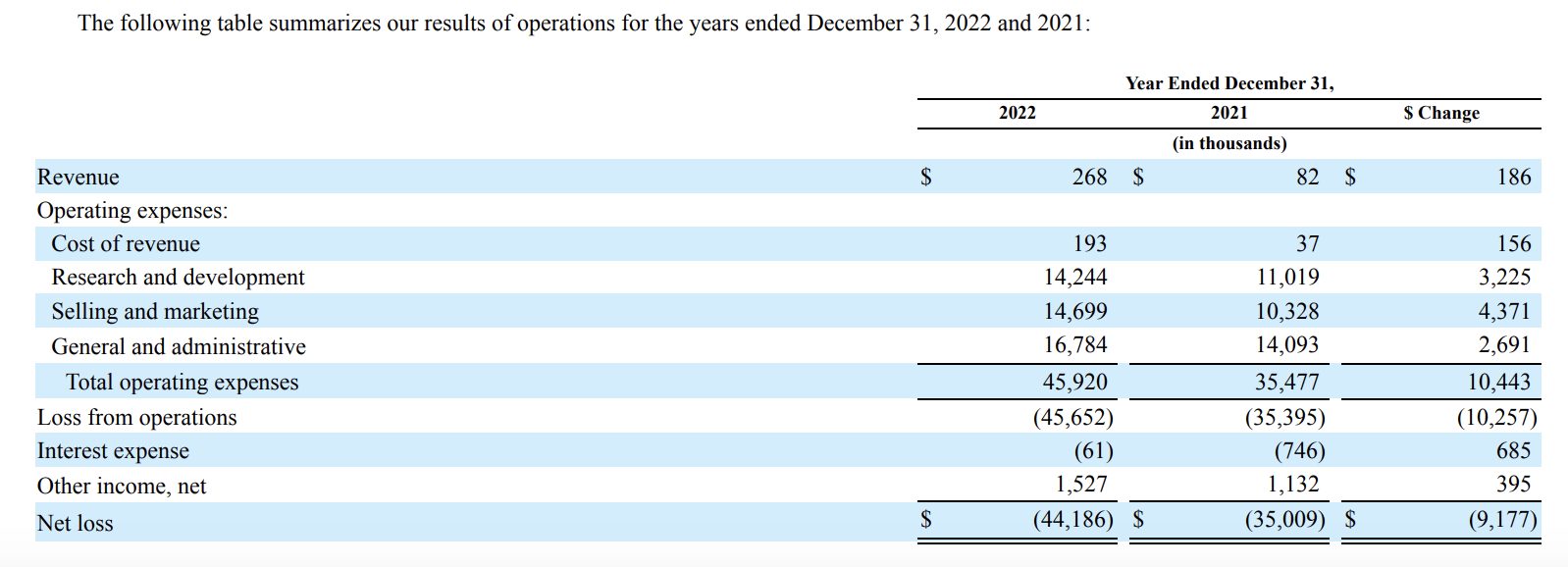

Sera revenues as reflected by its statement of operations in its 10-K filed 03/22/23 have been modest particularly when compared to its expenses:

{kind=link}

Moving forward to its revenue as shown by its Q3, 2023 10-Q shows little to cheer about:

{kind=link}

If you annualize the $265,000 in nine month revenue, you get ~$353 thousand which is a nice ~31% increase; however it is minuscule compared to expenses. Although Sera has a pipeline of other products in development, its above referenced 10-K (p. 40) advises that it expects substantially all of its near term revenue from sales of the PreTRM test.

In terms of revenue growth over the near term it will look to possible:

- price increases;

- sales volume increases as it continue to engage with payers and health systems to close payment contracts.

During Sera's Q3, 2023 earnings call (the "Call") CFO Aerts provided a financial overview for Sera and its near term future expectations. He advised:

... 2023 gross cash expenses are expected to be approximately $34 million for the year compared to approximately $39 million for the year in 2022, an approximate $5 million or 14% decrease. Our gross cash expenses for 2024 are expected to be less than $29 million as we fully recognize the impact of the streamlining efforts we’ve made in 2023. This represents an additional annual decrease of approximately $5 million or 15%. We believe our plan for managing operating expenses in the future should enable us to operate into 2027 given our very strong cash position.

Previously during the Call Aerts had advised that at the close of Q3, 2023 Sera had cash, cash equivalents and available-for-sale securities of approximately $85 million. In other words its runway into 2027 is a short one depending on actual revenues and expenses.

There is little margin for error and the runway into 2027 may not extend very deep into the year. Unless revenues surge it is likely in order to keep a comfortable cash cushion, management will elect to raise cash in some way long before the Times Square ball drops for 2027.

In its 10-K (p. 93) Sera advises that its principal sources of working capital to date have been:

- proceeds from the sale and issuance of convertible preferred stock and convertible notes;

- bank loans; and

- the sale and issuance of Class A common stock in an initial public offering (“IPO”), which was completed in July 2021.

The process of readying Sera's PreTRM test for market is ongoing.

Preparing diagnostic tests for market is not as cut and dried as preparing remedial therapies. With therapies, a company works under supervision of the FDA, designing a series of clinical trials culminating in one or several pivotal trials. After successful completion of a pivotal trial it moves forward to apply for formal FDA approval.

Diagnostic tests are different. Sera's 10-K (pps. 28-29) characterizes its PreTRM test as a laboratory developed test [LDT] that it processes in its single CLIA-certified laboratory. It goes on to explain that while the FDA has authority to regulate LDT's:

... it has historically exercised enforcement discretion and is not otherwise regulating most tests developed, manufactured and performed within a single high-complexity CLIA-certified laboratory.

There is pending federal legislation, the so-called VALID Act, which would tighten this regulatory regime imposing requirements for:

- registration and listing;

- adverse event reporting; and

- quality control.

Gears turn and legislation moves exceedingly slowly in Washington under the best of circumstances. The VALID Act has been caught up in a series of disputes over regulation of COVID tests. I do not expect any resolution until at least after smoke clears following the 2024 election cycle. For the time being Sera's laboratory CLIA compliance is its principal regulatory burden.

However the market also judges its PreTRM test by the quality and extent of its validation which is critical for payer reimbursement. As described in its 10-K validation for the PreTRM test consists of several aspects:

- analytical validation of the testing platform, or measurement validity;

- clinical validation, or test validity; and

- clinical utility of using validated predictions, or positive health benefits.

This validation is ongoing with its recently completed AVERT trial data readout on 02/15/2023. During the Call CEO Lindgardt was highly enthusiastic about the AVERT readout. She summarized it from a preprint manuscript that was submitted to a peer reviewed journal:

A total of 1,463 women were screened and tested ... and 3 women were subsequently deemed ineligible after screening. Of these, roughly 35% or 507 patients were deemed high risk with roughly 56% or 286 of these accepting interventions. Pregnancies identified by the test to be at elevated risk for preterm birth were offered 81 milligrams of aspirin daily, 200 milligrams of vaginal progesterone daily and care management.

The study goal was to compare risks for women who were screened low or high risk and accepting treatment with a historical study arm of 10,000 pregnancies. she noted:

PreTRM test impact showed driving 2.5-week improvement in gestational age of infants, most at risk for early delivery. 21% reduction in neonatal hospital length of stay, 18% reduction in severe neonatal morbidity and mortality, and an impressive 28-day reduction in neonatal intensive care unit length of stay for infants born before 32 weeks.

DSMB decision wrongfoots Sera investors.

Sera's PRIME study originally planned to enroll 6,500 was recently stopped by its DSMB for efficacy. During the Call CEO Lindquist had discussed the various approached the DSMB might take. He had anticipated that it most likely would allow the study to proceed to full enrollment and study completion. Indeed that seemed to be his preferred result.

As he said:

We would be very pleased with the scenario number one, which would result in full enrollment, deliverable babies and their outcomes available and recorded, which we anticipate will all be known, analyzed and reported in 2025.

Instead he has a less desirable situation, with less patients. Ironically during the Call Lindquist advised that following the AVERT readout Sera had been planning to increase PRIME enrollment by 1,000 patients. Doing so would give Sera a sufficient number of high-risk treated patients to enhance statistical power of the PRIME results.

Thanks to the DSMB decision Sera now will not only have data from fewer of its original 6,500 patients, and also from none of the 1,000 increase as thought helpful. I submit that this is an instance where the market has misread the situation; Sera stock skyrocketed by 150% on initial reaction to news that PRIME was being stopped for efficacy.

Shares had closed 12/04/2023 at $2.10. On 12/06/2023 they reached a high of $9.86, closing 12/06/2023 at $5.49. Its most recent close as I write on 01/07/2023 is at $5.30, still more than double its closing price before the DSMB's PRIME decision.

As a microcap Sera poses extra risks for investors.

Perhaps the most daunting challenge for Sera investors arises because of its scale as a microcap company. While it has succeeded in launching its preTRM test into the market it has yet to succeed in achieving meaningful revenues. Its challenges include:

- building an effective sales force from scratch;

- building physician awareness of the preTRM tests

- building patient awareness of the preTRM test;

- getting added to payer formularies as a single product situation.

Sera has a comfortable cash situation in the context of a small company that is working to control its costs. It lacks resources to sponsor an effective national marketing campaign that could jump-start revenues

Conclusion

Sera's position as a small company working to commercialize a new technologically advanced blood test brings tears to my eyes as former T2 Biosystems ( TTOO ) bull . T2 dropped hugely in a short span of time despite marketing just such a technologically advanced, potentially life saving blood test for sepsis.

This is not to say that Sera will follow the same rocky path. However its failure to generate meaningful sales from its PreTRM test which has now been on the market over two years is highly concerning to me. I rate Sera as a "hold".

For further details see:

Sera Prognostics: The Pregnancy Company On A Hot Streak