SHEN - Shenandoah Telecommunications Needs Breakthrough Growth

2024-01-09 17:28:54 ET

Summary

- Shenandoah's fiber investment may not yield a sufficient return on investment due to competition and slow customer acquisition.

- The acquisition of Horizon Telecom has weakened Shenandoah's balance sheet, with financing for the deal not yet secured.

- The stock is overvalued without breakout growth, and the current pricing is difficult to justify based on projected financials.

I am following up on my previous thesis on Shenandoah Telecommunications (SHEN).

In my previous analysis, I rated Shenandoah a hold for the following reasons:

- The major investments into fiber were driving volume growth, but not pricing.

- Maintaining fiber at such a high growth rate would be challenging given the competitive environment.

- Their balance sheet was weak following years of underperformance.

Since my last analysis, Shenandoah is up roughly 6%. However, my concerns on the business continue to grow.

{kind=link}

In my opinion, Shenandoah is building fiber as if they have no competition and getting an ROI on the investment will be challenging. The balance sheet is also weakened further by the Horizon acquisition, for which financing hasn't even been finalized. And based on DCF analysis, Shenandoah would need breakout growth in fiber, while maintaining existing businesses, to justify the current pricing.

With the above in mind, I lower my rating from hold to sell as risk now materially outweighs upside potential.

ROI For Fiber Questionable

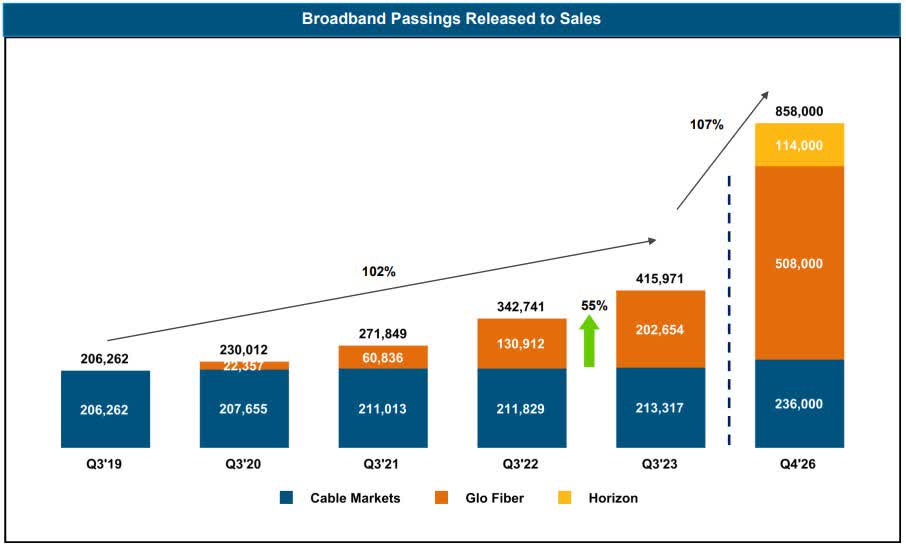

Shenandoah has been rapidly expanding its fiber footprint, doubling passing since 2019 and planning to double again by 2024.

{kind=link}

This sounds great on paper, however, I am concerned that the competitive environment doesn't support this plan. And management seems to be proceeding as if competition is not a factor.

The first constraint is the US telecom market as a whole. The 2022-2027 CAGR for US telecom is forecasted at just under 1%. Certainly, products like fiber will grow faster, while products like video decline. However, this still sets up a need to take market share to grow, and all of the telecoms will be competing for the same customers.

To that point, Shenandoah can only grow so far outside of its current market. Verizon (VZ) and T-Mobile (TMUS) are both major players in the region with cable, fiber, and now 5G fixed access products. While Shenandoah will continue to do well in converting its existing cable customers, Verizon and T-Mobile will likely compete in their territory.

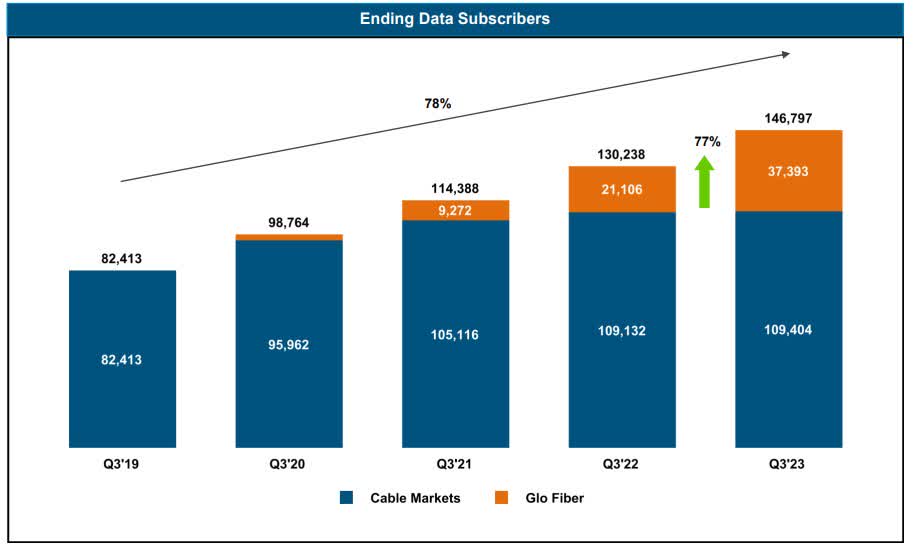

And as the fiber investment continues, customer acquisition is not keeping up. While fiber passings are up 102%, data subscribers are only up 78%. Not to mention that the cable business stagnated.

{kind=link}

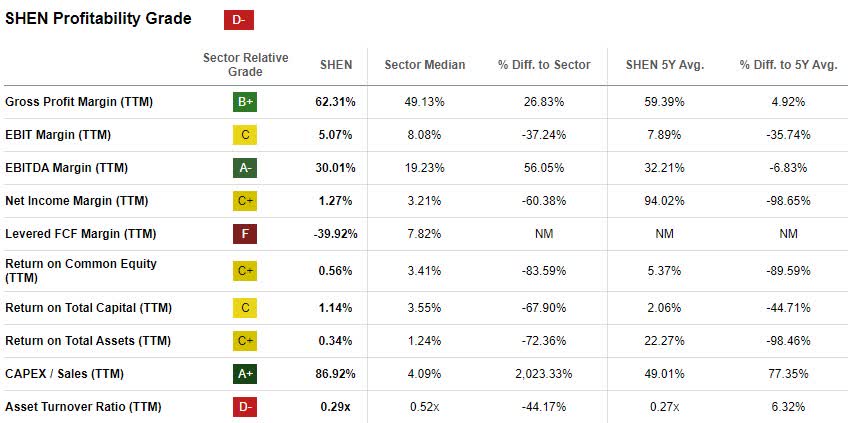

Shenandoah is also generating disproportionately low returns on capital as they rapidly invest but slowly grow revenue. Return on capital of 1.14% is 68% below the industry and return on total assets of 0.34% is 72% below the industry. Also, note that they are currently spending 87% of sales on Capex.

{kind=link}

Balance Sheet Weaker On Horizon Acquisition

In October, Shenandoah agreed to acquire Horizon Telecom in a deal worth $385 million, $305 million of which is cash consideration. This purchase price represented a 12.9x multiple on EBITDA. This strategic acquisition was intended to allow Shentel to expand its commercial fiber capabilities. According to Shentel's announcement, the deal to acquire Horizon equates to a monetary value of $51,000 per fiber route mile .

From a fiber standpoint, this was a steal as the average cost per mile in the US is running between $60,000 and $80,000. It was less of a deal on the overall company, with the 12.9 EBITDA multiple well exceeding the sector average of 9.68.

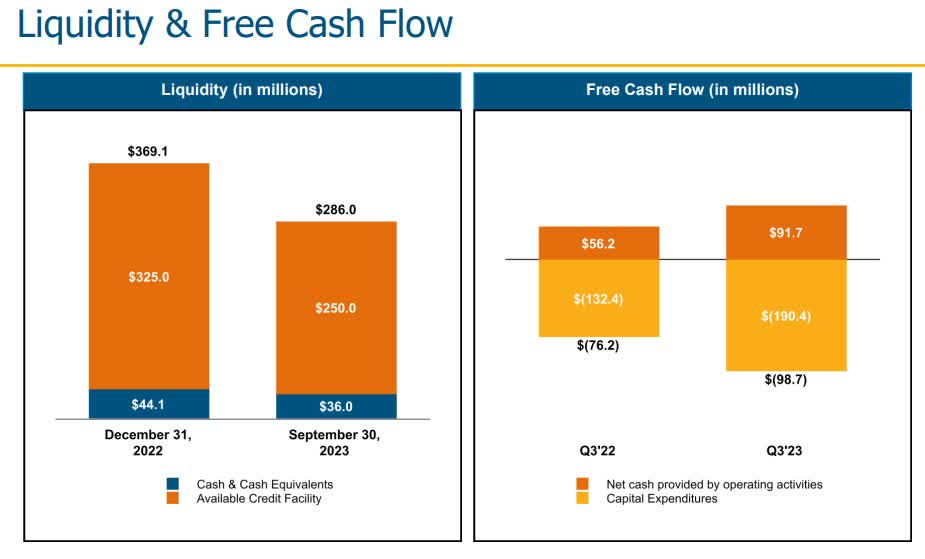

Regardless of the deal terms (which I think was "fine" but not great), the cash consideration further weakens an already challenged balance sheet. Liquidity continues to decline as capital investments far outpace operating cash.

{kind=link}

Average net debt to EBITDA in the telecom industry runs around 2.5x. Currently, Shenandoah is running just under 2.0x.

In the earnings call , management discussed the plan to generate the $305 million in cash for the Horizon purchase. At the moment, the financing has not been secured. Option 1 would be selling some tower assets now that T-Mobile is ending contracts. Option 2 would be debt financing.

If Shenandoah took the debt financing route, the ratio would increase from 2.0x to 5.5x which would require cash flow to be redirected away from shareholder returns and towards debt.

Stock Overvalued Without Breakout Growth

I first ran a DCF incorporating management guidance balanced against existing growth/decline trends in the business. I assumed the following:

- 12% discount rate with elevated risk premium due to sustained low profitability

- 4% long-run growth rate (management believes they can beat the market with fiber)

- 8% revenue, 3% cost (based on current fiber growth and margin expansion)

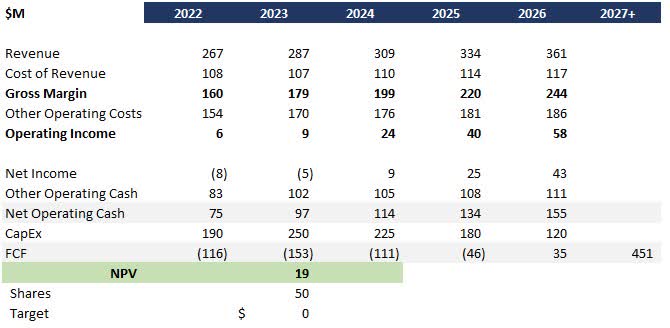

This DCF results in a price target of $0 due to the heavy near-term capital investment.

{kind=link}

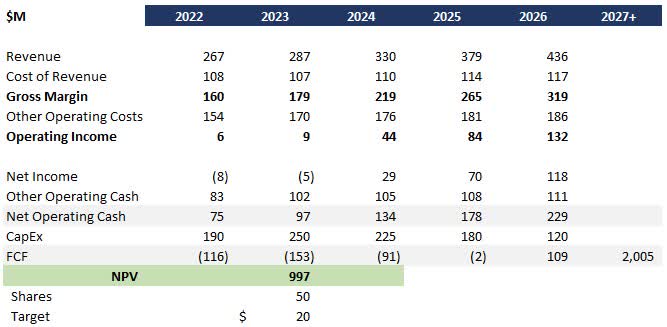

From there, I wanted to see what had to be true to justify today's current pricing near $20. To get to $20 I had to assume the following:

- 12% discount rate with elevated risk premium due to sustained low profitability

- 6% long-run growth rate, well above telecom CAGR

- 15% revenue, 3% cost near-term growth, which would be more aggressive than Shenandoah has ever delivered

{kind=link}

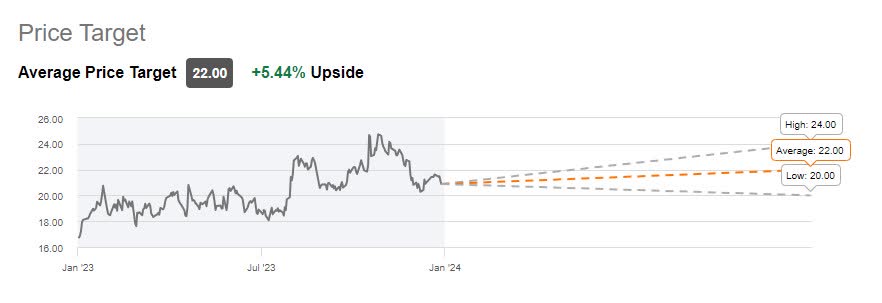

Seeing upside potential, Wall Street actually supports the aggressive growth case with an average price target of $22, although they were rating sell until as recently as July.

{kind=link}

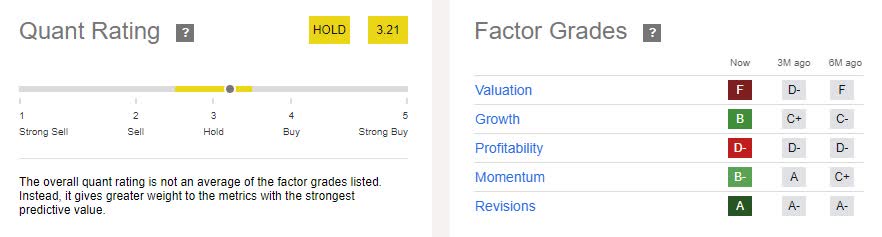

The quant rating is a hold driven by overweight valuations and low profitability. I would argue that it's actually too optimistic due to the growth rating. The growth % is high because the nominal profitability is so low.

{kind=link}

Regardless of where Shenandoah lands between my $0 and $20 scenario, all three ratings agree that Shenandoah is at or near the top end of its value.

Verdict

Shenandoah's future profitability and value depend on breakthrough growth. My base case DCF analysis presents a bleak picture, projecting a price target of $0, largely due to heavy near-term capital investment.

Despite this, market prices hover around $20, a value that can only be justified under an aggressive growth scenario. This scenario, however, requires well-above-average telecommunications CAGR and revenue growth significantly higher than Shenandoah has previously achieved. Notably, Wall Street seems to align with this high-growth view, maintaining an average price target of $22.

Regardless of the scenario, Shenandoah appears to be at the upper end of its value, with downside risk significantly outweighing upside potential. Given the above analysis, I rate Shenandoah a sell.

For further details see:

Shenandoah Telecommunications Needs Breakthrough Growth