SHOP - Shopify: A Top Bet On E-Commerce Growth (Rating Upgrade)

2023-08-08 16:47:30 ET

Summary

- Shopify beat expectations for Q2, but shares declined 15% last week.

- The company's subscription and merchant segments showed strong growth, with total revenues increasing 31% Y/Y.

- Long-term e-Commerce growth, a growing e-Commerce share and AI potential make Shopify an attractive investment.

- Shopify is not cheap, but the firm is an industry leader and has considerable potential for growth going forward.

Shares of Shopify ( SHOP ) have seen three consecutive days of losses after the e-Commerce company presented second-quarter earnings... although Shopify's results were actually quite good. The e-Commerce firm saw double-digit growth in both its Merchant and its Subscriptions business and submitted a strong outlook for the third-quarter in terms of revenue growth as well as gross margins. Considering that Shopify has a huge opportunity to capitalize on artificial intelligence solutions to drive value-add for its merchant base, I believe the share price drop following Q2 earnings creates a buy-the-drop situation.

Previous rating

I rated Shopify as a buy previously: Shopify Q1: GAAP Profitability. I believe Shopify's solid Q2 earnings release, AI potential, strong outlook for Q3 as well as post-earnings share price drop justify a rating upgrade to strong buy.

Shopify beat expectations and continued to deliver double-digit top line growth in Q2

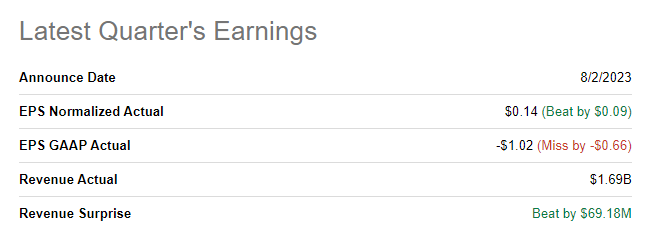

Despite Shopify beating expectations for second-quarter revenues and earnings, shares of the e-Commerce company have lost approximately 15% of their market value after Shopify submitted its Q2 earnings card. Shopify earned an adjusted $0.14 per-share (beating estimates by $0.09 per-share) on revenues of $1.69B (beating consensus estimates by $69M).

{kind=link}

Source: Seeking Alpha

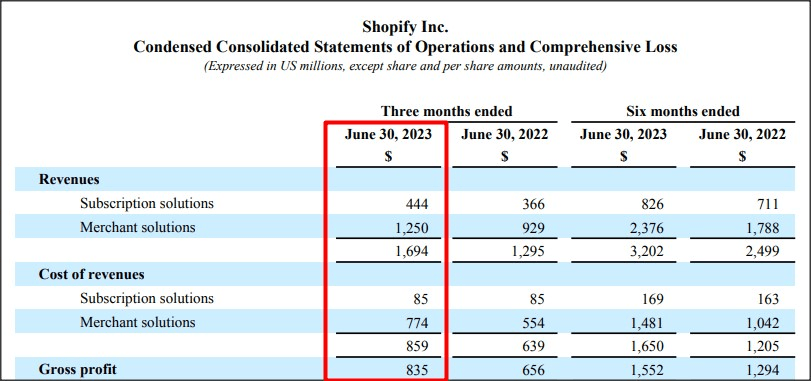

Shopify largely benefits from its strong position in the retail online merchant market where a lot of small businesses are running online stores. The company makes its money in two ways, basically: (1) It sells subscriptions for merchants that want to use Shopify's online store building tools, and (2) It complements its subscription business with complementary services such as payment processing, shipping and the provision of working capital for which Shopify is getting paid a variable fee. In other words, Shopify's core subscription business is supplemented by revenue streams that depend on the merchant's success.

Both segments maintained considerable momentum in the second fiscal quarter as subscription revenues grew 21% year over year to $444M and Merchant Solutions revenues were up 35% year over year to $1,250M. In total, Shopify’s revenues increased 31% year over year to a new record of $1,694M. Shopify’s businesses also generated $835M in gross profits, showing 27% year over year growth and a gross margin of 49.3%.

{kind=link}

Source: Shopify

Revenue drivers, AI potential could lead to the creation of new revenue streams

Shopify’s revenue and gross margin picture has deteriorated after the pandemic which boosted the company’s e-Commerce business in unprecedented ways. After the pandemic, however, Shopify has seen a sharp deceleration of its revenue and gross margin growth no longer experienced the massive tailwinds of the COVID-19 pandemic.

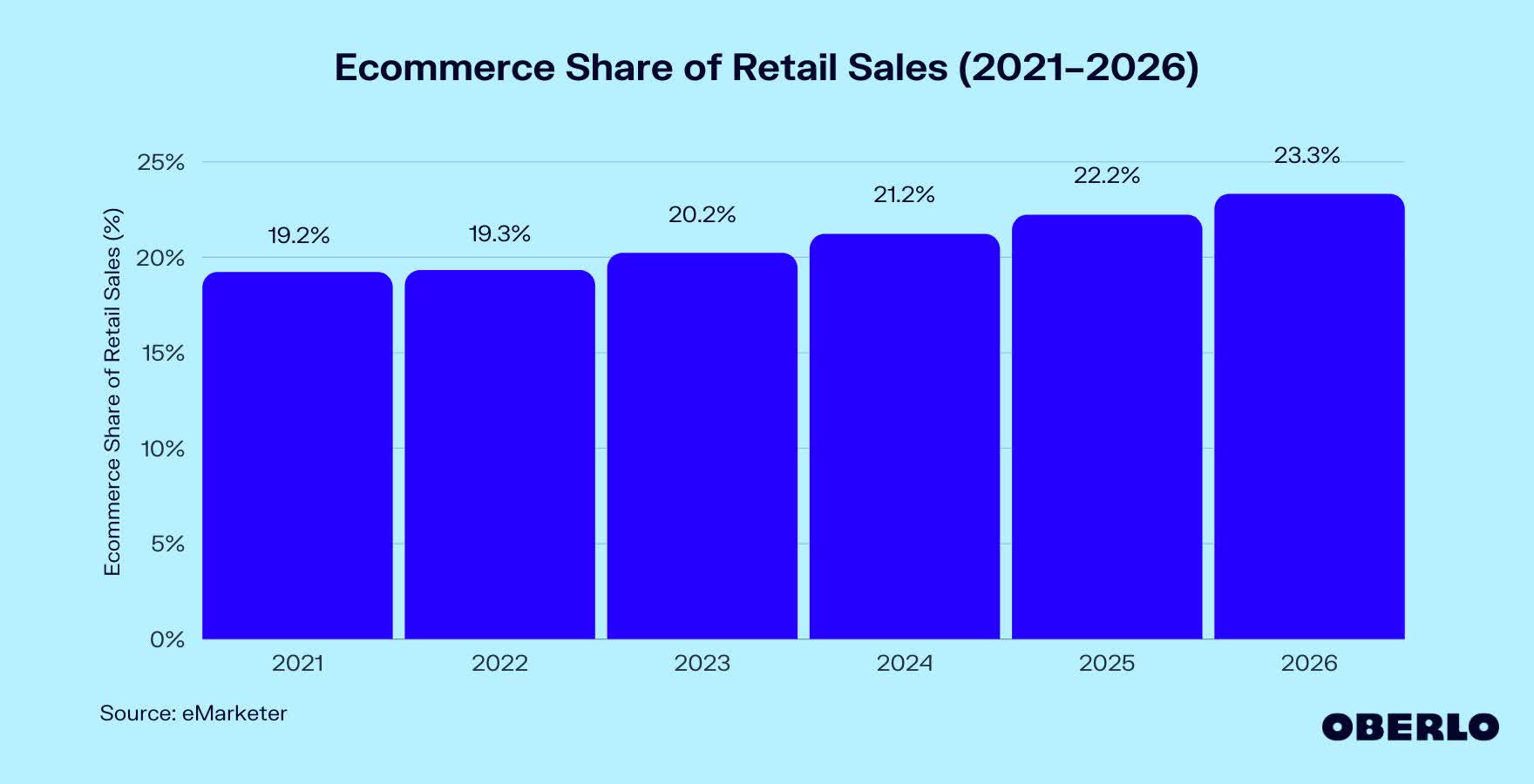

Still, some revenue drivers profoundly work to the benefit of Shopify in the long term. The biggest driver for Shopify’s expansion is the growth of the e-Commerce economy and, specifically, a growing e-Commerce share of retail sales. With people purchasing more goods and services online today than ever before, more retail spending is going to move to online merchants going forward and Shopify has a powerful tailwind in its business that could lead to many years of strong revenue growth. Based off of consensus expectations , Shopify is expected to generate 19% average annual top line growth between FY 2023 and FY 2032.

{kind=link}

Source: Oberlo

Additionally, the use of artificial intelligence products provides a huge opportunity for Shopify and could even result in the creation of new revenue streams. AI chatbots obviously are already used at scale in the customer service market, but Shopify also has an opportunity to bring AI-powered solutions to different parts of its business. Shopify is already offering AI-delivered product descriptions through a tool called Shopify Magic, but there are many more opportunities for monetization. AI-powered business solutions could be used in product research and competitor analysis, and deliver analytics insights. AI-supported analytics services could be offered on a subscription basis, for a low-fee, as an example. I see AI has a huge lever for incremental revenue growth for Shopify and investors can look forward to hearing more announcements in this regard going forward.

Guidance for Q3'23

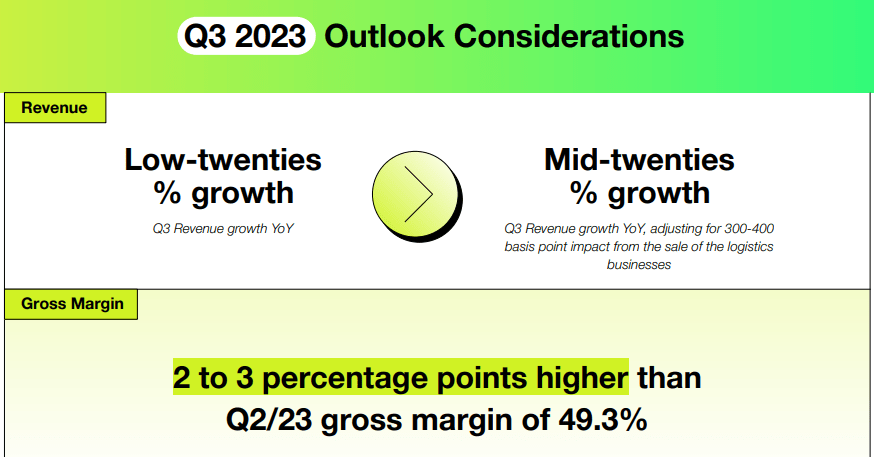

Shopify confirmed that it expects top line growth of 20% or more in the third-quarter while also projecting a sequential improvement in its gross margin of 2-3 PP. Shopify's outlook for Q3'23 was strong and should have provided some support for the company's shares last week...

{kind=link}

Source: Shopify

Shopify’s valuation vs. BigCommerce

Shopify is not a cheap, despite a 3-day sell-off after earnings, but shares have never really been cheap... in large part because of Shopify's massive potential in the online store market. As a growth company with a considerable opportunity in the e-Commerce industry, Shopify is valued at a high sales multiplier factor.

Shopify is currently trading at a price-to-revenue ratio of 9.1X which is still considerably above the firm's 1-year average P/S ratio of 7.4X. BigCommerce ( BIGC ), a rival to Shopify which is more focused on the enterprise market, trades at 2.6X forward revenues. However, Shopify has a market capitalization 82X and a revenue volume 23X larger than BigCommerce's. Shopify is the largest e-Commerce company in the sector and has been a leading innovator in the space as well. As a result, Shopify has by far the largest revenue volume in its niche.

Risks with Shopify

Shopify did generate a relatively large loss of $1.3B in the second-quarter (which was fully due to an impairment charge related to the sale of its logistics business to Flexport earlier this year) and a lack of profitability is still a concern that I believe keeps many investors away from Shopify. What would change my mind about Shopify is if the company failed to move towards profitability and saw a near term deceleration of its top line growth.

Closing thoughts

Shopify has seen a 3-day sell-off after the e-Commerce company reported better than expected results for the second fiscal quarter. However, giving the momentum in Subscription and Merchant revenues, I don’t see a real reason why investors should sell. Shopify also submitted a rather strong guidance for the third-quarter and the company has a huge opportunity to bring AI-powered solutions (possibly as a subscription offer) to its merchant base and provide additional value. I continue to believe that Shopify has an enormous opportunity in the e-Commerce market as more and more people shop online. While shares of Shopify are not cheap, Shopify’s shares essentially are a bet on the continual growth of the e-Commerce economy!

For further details see:

Shopify: A Top Bet On E-Commerce Growth (Rating Upgrade)