WIX - Shopify: Profitability Plagued By Growing Pains

2023-03-11 10:00:00 ET

Summary

- Investors should note that SHOP is not expected to record GAAP profitability over the next few years, suggesting the need to rely on adjusted numbers instead.

- Despite this, the company continues to prioritize vertically integrated e-commerce offerings and growth, while boasting an extremely healthy balance sheet.

- Combined with SHOP's determination in reducing operating expenses, we may witness moderate tailwinds for recovery in the intermediate term.

- Meanwhile, investors may nibble here, assuming the exercise consequently lowers their dollar cost averages, since it is trading below its 50-day moving average.

The Growth At All Costs Investment Thesis

While we have been and will remain bullish about Shopify Inc. (SHOP), investors must note that the company is not expected to report GAAP profitability for the next few years. Market analysts project that SHOP may only achieve positive Free Cash Flow [FCF] generation of $597.05M by FY2025 and GAAP EPS of $0.31 by FY2027.

In the meantime, any numbers reflected by the company and consensus estimates will be on an adjusted basis, including the projected FY2023 EPS of $0.02. This is partially attributed to the elevated Stock-Based Compensation of $549.14M (+66% YoY), and worsened by the growing operational expenses of $3.22B (+53.7% YoY) in FY2022.

It seems apparent that the rate of growth in SHOP's expenses was not sustainable, since its top-line decelerated to $5.59B (+21.4% YoY) in the latest fiscal year, compared to hyper-pandemic revenue growth of +57.4% in FY2021 and +85.6% in FY2020.

The rising inflationary pressures also impacted the company's profitability in FY2022, with rising cost of goods triggering a lower gross margins of 49.2%, compared to FY2021 levels of 53.8%. Notably, the company had guided for lower gross margins and higher operating expenses in 2023, attributed to the Shopify Payments and Deliverr segments.

Combined with the uncertain macroeconomic environment, it is unlikely that we may witness a quick and sustainable recovery to hyper-pandemic stock prices in the $100s. Nonetheless, with that discussion out of the way, we shall highlight why SHOP remains one of our closely monitored stocks.

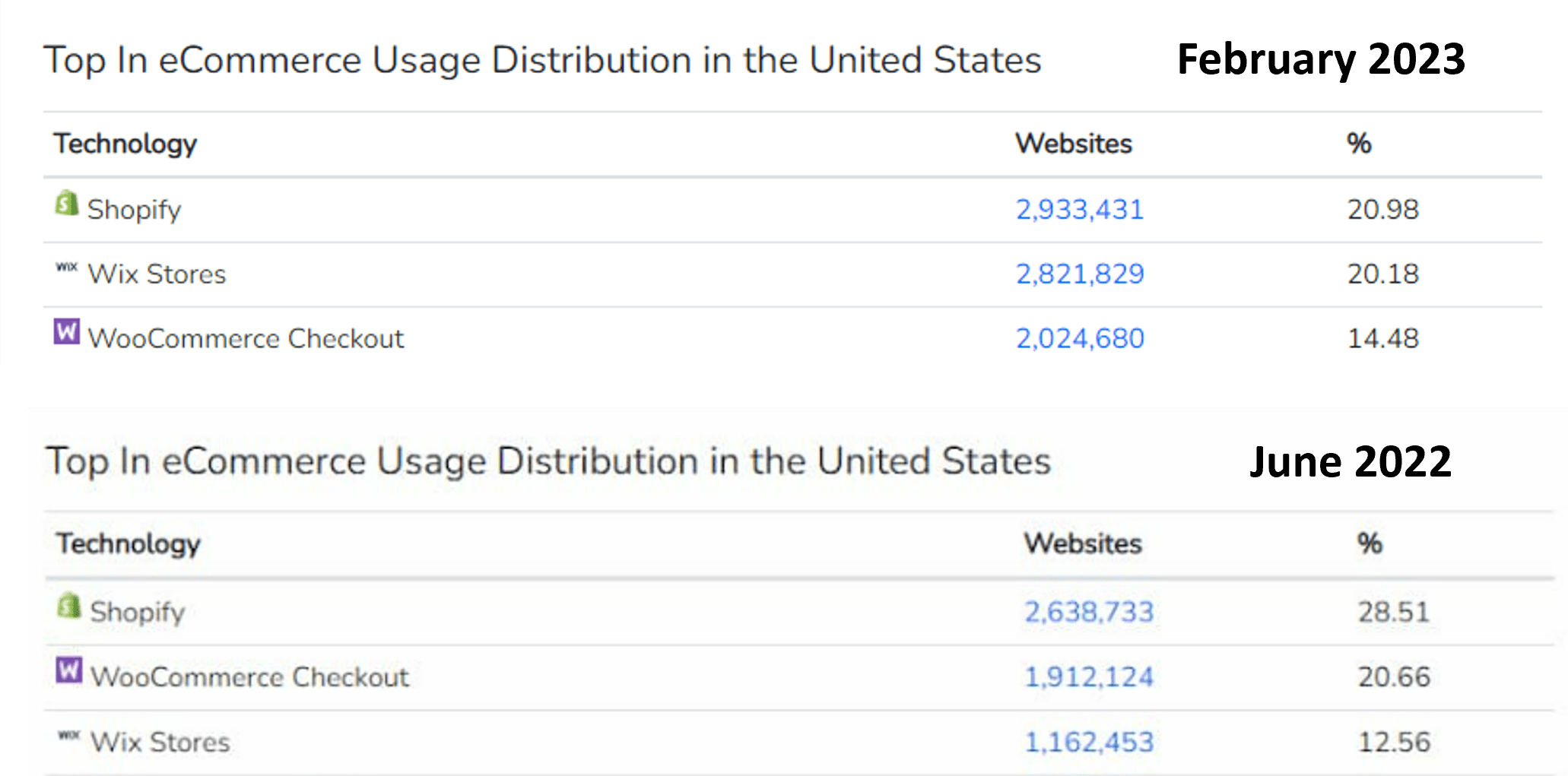

Despite the deceleration post reopening cadence and peak recessionary fears, the company continued to see excellent product adoption. As of February 15, 2023, its usage distribution in the US had grown by + 11.4% to 2.93M , from 2.63M in June 2022. Its GMV-based market share was at 10%, based on $197.2B ( +12.4% YoY ) recorded in FY2022, compared to Amazon's (NASDAQ: AMZN ) e-commerce market share of 37.8% at the same time.

E-commerce Usage Distribution In The US

{kind=link}

On one hand, SHOP's consumer onboarding in the US had slowed dramatically in comparison to WIX (WIX), which boasted tremendous growth of +143.1% between June 2022 and February 2023. On the other hand, the boom in consumer demand for e-commerce technologies by 51.9%, from a total of 9.2M to 13.98M sites in the US, proved that online shopping is here to stay indeed.

Statista also estimates that US retail e-commerce revenue is expected to grow from $905B in 2022 to over $1.7T by 2027, at an excellent CAGR of 13.44%. Therefore, despite the temporary headwinds, we are willing to be a little more patient, due to SHOP's long-runway for growth. It is also important to highlight that its e-commerce SaaS competitors, WIX and Squarespace (NYSE: SQSP ), have yet to achieve positive operating incomes as of FY2022.

SHOP's investors may rest assured that the company remains highly focused on growth, while providing a vertically integrated e-commerce platform, including payment system, logistics services, and inventory storage, amongst others.

At the same time, it seeks to provide value-added offerings to its target audience, given the relatively minimal price increase of +33% in January 2023 (the first time in twelve years), compared to WIX by +255.5% and SQSP by +43.75% since 2019. Since the increase in pricing is not unique to SHOP alone, we reckon there may be a reduced likelihood of churn moving forward, as highlighted by Gil Luria from D.A. Davidson:

What Shopify has done over the last few years is wrap around their customer with all types of offerings, from selling offline to shipping, to logistics, to selling globally - things that some of those smaller competitors can't do, which really differentiates their product. And so they have a very big lead over the alternative. That's part of what gives them the ability to take a price hike without expecting too much churn. ( Insider )

Furthermore, despite the normalization from hyper-pandemic growth, SHOP continued to report excellent top-line expansion of +21.4% YoY in FY2022 (at a CAGR of 52.5% between FY2019 and FY2022), against WIX at +9.3% (22%) and SQSP at +26.2% (20.38%). Its outperformance trumped AMZN as well at +9.4% (22.4%) respectively, demonstrating its accelerated growth cadence.

At the same time, the company recorded a rapid growth in headcount to 11.6K (+132% since FY2019) and net PPE assets of $485.97M (+97.4% since FY2019) as of FQ4'22, while also acquiring Deliverr for $2.1B, and Remix at an undisclosed amount.

Most importantly, SHOP accomplished all of these with an extremely healthy balance sheet in FQ4'22, with $5.08B of cash/ short term investments (+106.5% since FY2019) and $0.91B of long-term debts. There was also minimal share dilution along the way at 11.5%, from 1.13B of diluted shares in FY2019 to 1.26B by FY2022.

Combined with the management's commitment in reducing operating expenses through optimized cloud spending and tighter marketing spend, we reckon SHOP may still outperform in the intermediate term.

So, Is SHOP Stock A Buy , Sell, or Hold?

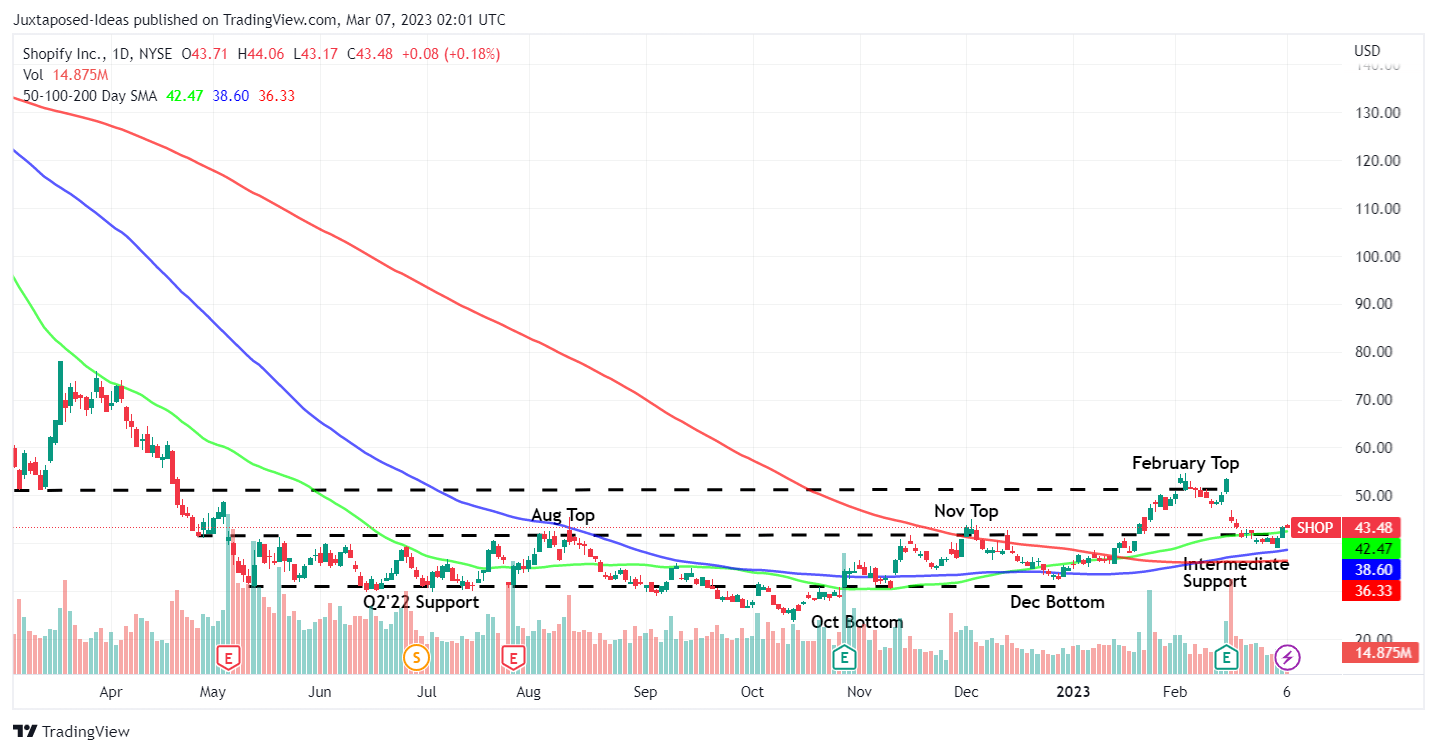

SHOP 1Y Stock Price

{kind=link}

It appears that the SHOP stock has found sufficient support levels here, after the drastic -18.5% plunge post FQ4'22 earnings call. The pessimism was surprising indeed, given the promising results then and the tailwinds for top and bottom line growth through the raised subscription fees from FQ2'23 onwards.

Nonetheless, these declines may also result in a more attractive entry point moving forward, assuming that the stock's weakness persists over the next few weeks prior to the Fed meeting on March 22, 2023. The recent minutes suggest that " ongoing rate hikes will be necessary," with market analysts already projecting a worst case terminal rate of up to 6.5% by September 2023.

Assuming so, we may see SHOP retest the December 2022 bottom in the low $30s. The stock may also remain volatile for the foreseeable future, attributed to its lack of GAAP profitability. As a result, existing investors may only add here if it consequently lowers their dollar cost averages.

For further details see:

Shopify: Profitability Plagued By Growing Pains