SHOP - Shopify Q3: A Good Company But Not A Good Stock

2023-11-07 12:52:30 ET

Summary

- Shopify's stock has rallied over 20% after strong 3Q FY2023 earnings, with positive GAAP operating income and rebounding top-line revenue.

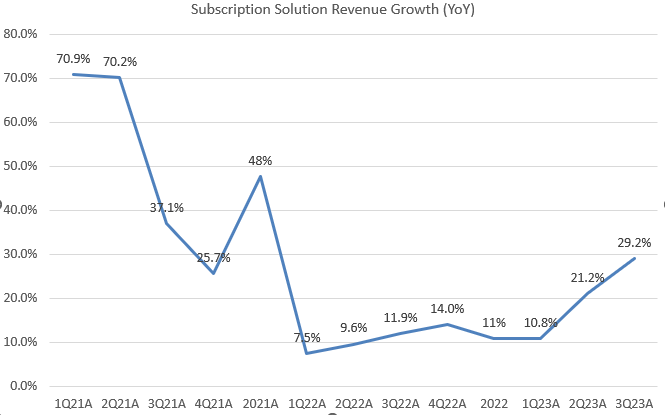

- Subscription solutions revenue grew 29.2% YoY, indicating successful pricing changes and attracting more merchants to the platform.

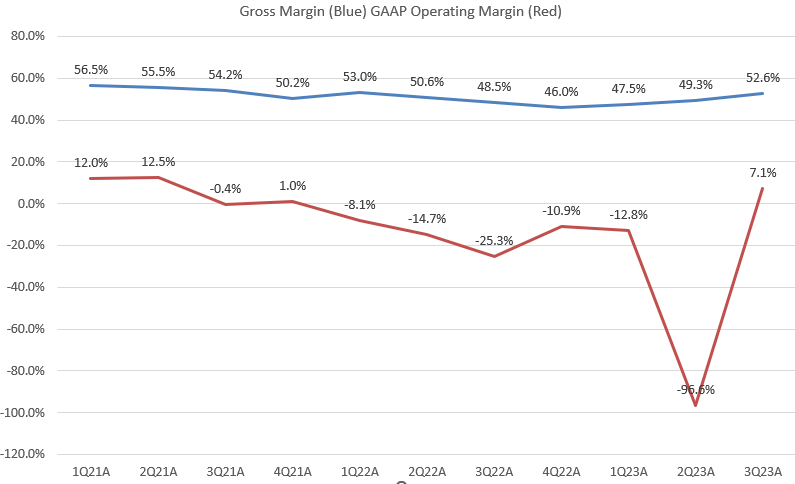

- Shopify's gross margin reached 50% and GAAP operating margin reached 7.1%, signaling a positive outlook for GAAP EPS in FY2024.

- However, the stock is currently trading at a premium valuation with an EV/sales Fwd 10.8x, indicating a significant downside risk given the current rates backdrop and potential economic slowdown.

Investment Thesis

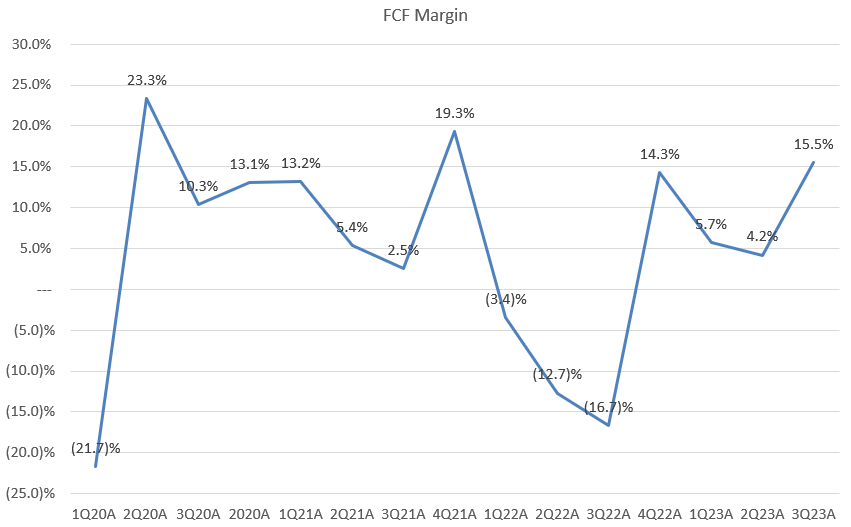

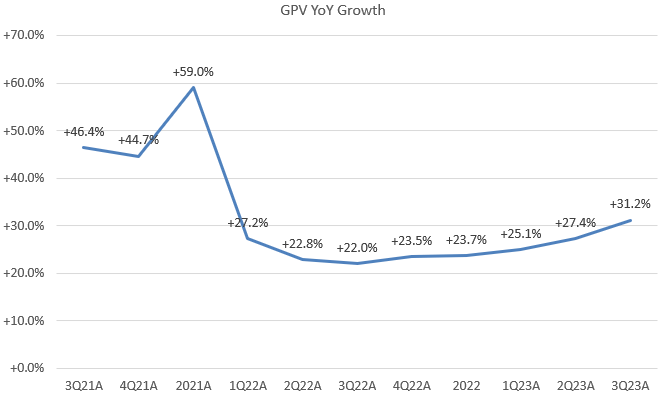

Last week, Shopify's ( SHOP ) stock made a strong comeback, cheering investors with a rally over 20% following the release of 3Q FY2023 earnings. I believe this quarter could mark an inflection point, with its GAAP operating income entering positive territory for the first time since 4Q FY2021. Additionally, SHOP has experienced a continued rebound in top-line revenue, primarily driven by the strong growth of its Subscription Solutions. It's very encouraging to see that Gross Payment Volume (GPV) has continued to accelerate on both a quarter-over-quarter (QoQ) and year-over-year (YoY) basis, in contrast to a decline in GPV for Block ( SQ ) in the recent quarter. Lastly, there is clear evidence of a reacceleration in its FCF growth from the last quarter as well.

Despite these positive developments, I've issued a hold rating on the stock as it's currently trading at a premium valuation. While I admit that the recent drop in long-duration yields can benefit high-valuation stocks, including SHOP, I'm still concerned that the current rates backdrop is too high for a stock with a 10.8x of EV/Sales Fwd.

3Q FY2023 Takeaway

{kind=link}

Company model

SHOP finished its 3Q FY2023 with impressive earnings results , surpassing consensus in both revenue and adjusted EPS. We can see that the company's business model demonstrated remarkable resilience, showing a rebound in growth following a significant slowdown in FY2022. Notably, the revenue from Subscription Solutions saw a strong YoY growth of 29.2%, a substantial jump from the 11.9% YoY in 3Q FY2022. This suggests that the company's pricing adjustments have successfully attracted more merchants to join the platform. Moreover, the management noted that 3Q FY2023 marked the first quarter of the impact from pricing increases on the Standard plans, which has suggested fewer negative reactions from merchants, resulting in an increase in the number of merchants on both the Standard and Plus plans.

{kind=link}

Company model

Additionally, in 3Q FY2023, the company continued to improve its margins, crossing the 50% threshold for its gross margin for the first time since 2Q FY2022. Its GAAP operating margin turned positive at 7.1%, marking a significant turning point with the potential to boost its bottom line. This indicates a positive trajectory for the company's GAAP EPS in FY2024.

Regarding its forward guidance, the company is projected to achieve high-teens YoY growth in 4Q FY2023, which implies a slight decrease compared to the previous quarter. This guidance translates to approximately 25% YoY growth for FY2023, showing a rebound from the 21% YoY growth seen in FY2022. Furthermore, the company anticipates its gross margin to be 300 to 400 basis points higher than in 4Q FY2022. This implies a gross margin of 49.5% in 4Q FY2023, in line with the historical trend of a QoQ decline compared to 3Q FY2023, attributed to the seasonality of the holiday selling season.

{kind=link}

Company model

Lastly, the company guided a high-teens FCF margin in 4Q FY2023, which is very encouraging as well, indicating an expansion of the FCF margin compared to the 15.5% in 3Q FY2023. Furthermore, the management expressed confidence in sustaining this upward trend for the benefit of investors.

Continued Traction with Merchants

{kind=link}

Company model

As shown in the chart, SHOP has consistently accelerated its growth in GPV since 4Q FY2022, reaching a notable 31.2% YoY growth in 3Q FY2023. This trend indicates that the company has been gaining momentum in acquiring new merchants. In contrast, SQ's GMV only grew by 10.5% YoY in 3Q FY2023, a decline from the 12.4% YoY growth in 2Q FY2023 and the 19.7% YoY growth in 3Q FY2022.

During the earnings call , the management discussed several factors contributing to the higher GMV results for the quarter. These factors include the strong performance of merchants using Shopify Payments, with an increasing percentage falling into the Shopify Plus category, as well as new merchant adoption globally. Furthermore, there was greater penetration of Shop Pay and continued growth of their integrated point-of-sale solution in physical retail stores. The robust growth in GMV has also played an important role in maintaining the company's growth trajectory, which reached 25.5% YoY, marking an acceleration from the 21.6% YoY growth seen in 3Q FY2022.

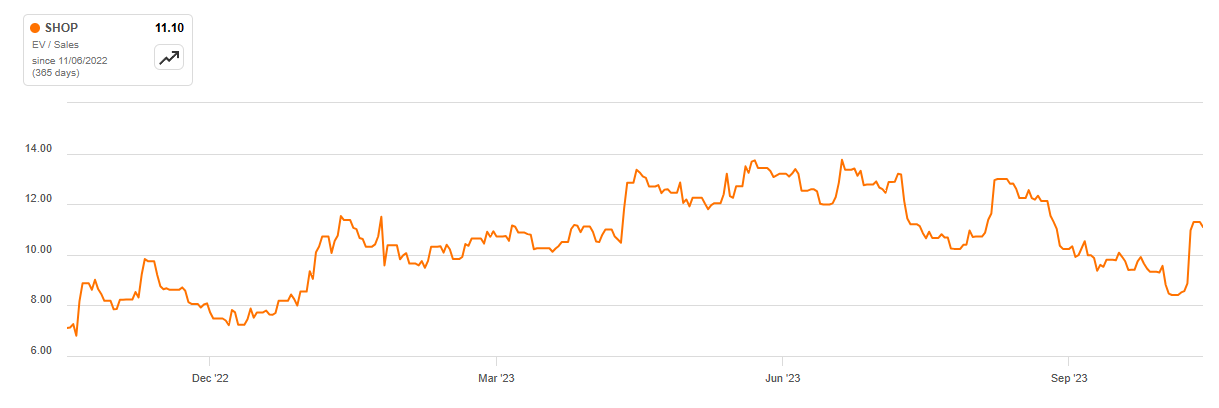

Valuation

{kind=link}

Seeking Alpha

However, SHOP is currently trading at a premium multiple of 11.1x EV/Sales TTM. If we take its forward sales into consideration, the stock is still trading at 10.8x. Generally, a ratio exceeding 10x is considered lofty and potentially unsustainable. I believe that, given the current high interest rate environment, particularly following a 100 bps increase in long-term rates over recent months, SHOP appears to be very expensive.

Investors may observe that its P/E non-GAAP Fwd stands at 90x, which is more than double that of NVIDIA ( NVDA ) at 41x. While some investors might argue that this high multiple reflects SHOP's robust growth prospects and significant improvements in its profitability and FCF for FY2023, it's important for investors to remember an old adage: a good company does not necessarily equate to a good stock.

Therefore, I hold the view that the stock may carry a substantial downside risk from a valuation perspective if the current growth momentum were to stall, especially as economic conditions show signs of deterioration .

Conclusion

In summary, I admit that SHOP has demonstrated significant strengths in its recent performance, characterized by robust revenue growth, improving margins, and a continued rebound in GPV. The company's ability to attract more merchants, driven by pricing changes and enhanced subscription solutions, is evident, with the positive trajectory in FCF margin and operating margins suggesting a promising future and a potential inflection point in its GAAP EPS. Nevertheless, concerns arise from the stock's current premium valuation, trading at 10.8x EV/Sales Fwd and a P/E non-GAAP Fwd of 90x, which appears very lofty, especially in the context of high interest rates environment. While a high multiple may reflect growth prospects and improved fundamentals, once again, we should be mindful that there's always the risk of buying a good company's stock at the wrong time.

For further details see:

Shopify Q3: A Good Company But Not A Good Stock