SHOP - Shopify: Riding High On Promising Future Growth

2023-10-13 10:26:09 ET

Summary

- Shopify Inc.'s strong market position and growth potential are evident.

- Concerns arise regarding the recent valuation as Shopify enters a more mature growth phase.

- The challenge lies in maintaining a hypergrowth premium amid moderating revenue growth rates.

Investment Thesis

Shopify Inc. ( SHOP ) provides a comprehensive platform for businesses of all sizes to manage their retail operations, offering tools for product management, order processing, and customer relationship building across multiple sales channels. With a strong emphasis on simplicity and reliability, Shopify empowers merchants to build their brand, expand globally, and handle significant online traffic.

I make the case that over the next year, Shopify's revenue growth rates will moderate to around 20% to 25%. If we presume that Shopify's free cash flow line jumps by 50% next year, and Shopify ends up delivering $850 million of free cash flow in 2024, this would leave this stock priced at 80x forward free cash flow.

I believe this is a rich multiple for what Shopify offers in terms of growth rates. Therefore, I'm neutral on this stock.

Shopify's Near-Term Prospects

Shopify is a provider of essential internet infrastructure for commerce, offering tools for businesses of all sizes to start, grow, and manage their retail operations. With a focus on simplicity and reliability, Shopify's platform enables businesses to manage products and inventory, process orders and payments, and build customer relationships. Additionally, Shopify empowers merchants to build their brand, leverage mobile technology, and handle high traffic with flexible infrastructure, all while prioritizing sustainability initiatives.

Shopify's near-term prospects remain promising, with the company continuing to experience consistent growth across various product lines. The partnership with Amazon ( AMZN ) through Buy with Prime presents an opportunity for expanded GMV, although specific impacts have yet to be precisely determined. Meanwhile, the emphasis on offering merchants more choice, such as the Shop Promise badge, serves to enhance consumer confidence and drive conversion rates.

The introduction of Shopify's B2B solution has been well received, and the company's efforts to strengthen its enterprise offerings appear to be gaining traction. Cross-selling initiatives within the customer base are being approached with greater strategic focus, contributing to increased overall value for merchants. While the company has made recent adjustments to subscription pricing, the emphasis remains on delivering unmatched value to its customer base.

On the other hand, challenges for Shopify include potential shifts in the competitive landscape, as the e-commerce market continues to evolve. The company's focus on differentiating itself through value-added services and innovative solutions is crucial to retaining its market position.

Additionally, continued monitoring of customer retention rates and ensuring sustained merchant satisfaction are vital for long-term growth. As the company continues to expand its product offerings and penetrate the enterprise market, maintaining a balance between scalability and operational efficiency will be key. Also, ensuring seamless integration with existing ecosystem components for larger enterprise customers and ongoing improvements in the B2B sector will be critical for sustained success in the evolving e-commerce landscape.

With that in mind, let's delve into Shopify's financials.

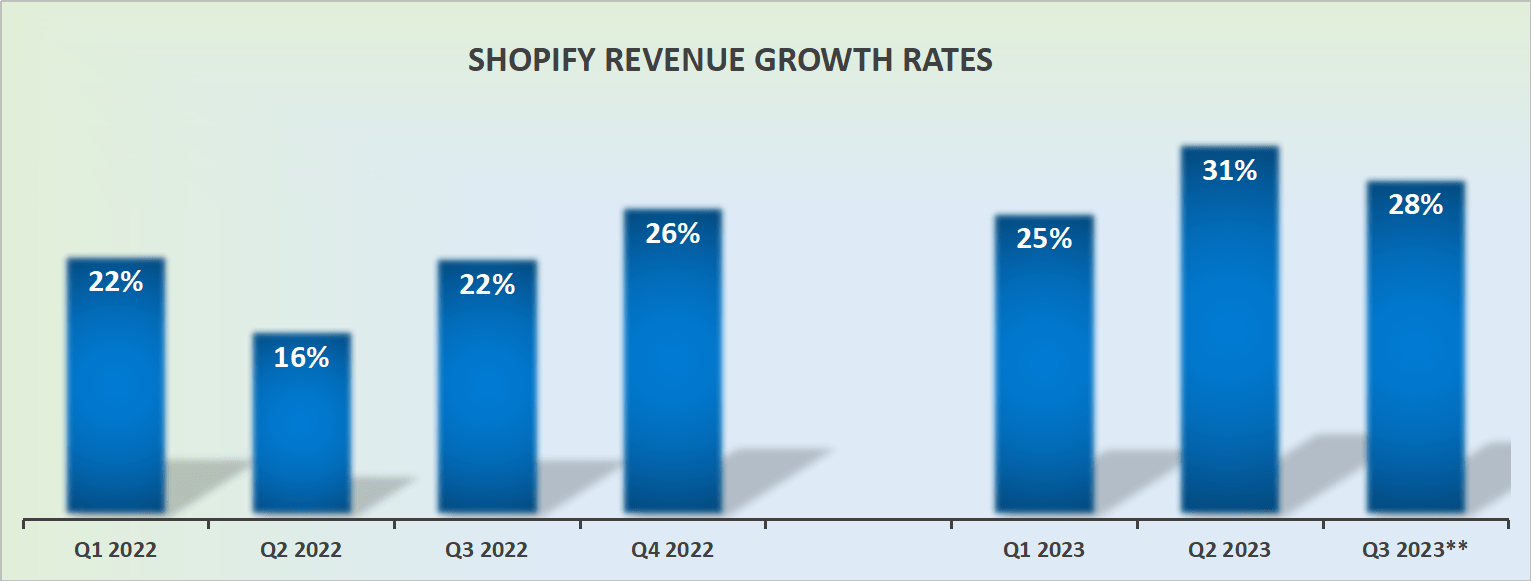

Revenue Growth Rates Point to Mid-20s% CAGR

{kind=link}

Shopify's growth rates point towards the low 20s for the quarter ahead. However, adjusting for the sale of its logistic business, its growth rate is expected to come close to the mid-20s% CAGR. That being said, for the most part, Shopify has a history of being conservative with its guidance.

SA Premium

Accordingly, this means that Shopify's growth rates will probably end up coming in close to 28% CAGR. Next, looking further into Q4 and Q1 2024, it appears to reinforce the overall trajectory that Shopify is moving towards.

SA Premium

As you can see above, analyst expectations point towards Shopify delivering very high-teen growth rates. Even if it happens to be the case that these estimates are on the low side, and Shopify's growth rates end up beating these estimates by 300 or 400 basis points, I believe that it's fair to say that Shopify is unlikely to return to +30% organic CAGR anytime soon. This means that investors' attention will soon start to increasingly focus on its underlying profitability.

Profitability Profile in Focus

As I've made the case already, Shopify's profitability will soon start to garner more attention to support its valuation. To be clear, I'm not saying that investors are today looking at its bottom line profitability. Rather, I contend that over the next 2-3 quarters, once investor expectations that Shopify is not delivering 30% CAGR any longer get cemented, at that point , investors will look beyond its narrative and bring intensive focus on its profitability.

We know that Shopify's Q2 results delivered 6% free cash flow margins. If we assume that Q3 delivers 7% free cash flow margins and the all-important Q4 quarter delivers 8% free cash flow margins, this would see Shopify's free cash flow run-rate exiting 2023 of around $550 million.

Then, if we make a generous assumption that in 2024, as the business grows its top line at somewhere around 20% to 25%, its free cash flows rapidly outgrow its top line by 50%, this would see Shopify's free cash flow in 2024 reaching $825 million.

This would leave Shopify priced at 80x next year's free cash flow. That's clearly nowhere near as shocking as it once was. But it's difficult to expect Shopify's multiple to expand further.

Let me put this another way; the graphic above depicts Shopify's multiple in 2023, which has significantly expanded from 6x to 8x forward sales, despite persistently high-interest rates in 2023.

It's not that Shopify's multiple-to-sales or free cash flow cannot return to previous levels. Instead, it is more the case that as its revenue growth rates begin to moderate, it will become increasingly challenging for the company to command a hypergrowth premium on its stock.

The Bottom Line

As I assess Shopify Inc.'s near-term trajectory, I acknowledge its strong market position and ongoing growth potential. However, the recent stock valuation remains a concern.

Shopify's transition to a more mature growth phase suggests that its premium valuation may face challenges as revenue growth rates gradually moderate. The current multiple expansion from 6x to 8x forward sales signifies an optimistic outlook, but the potential difficulty in commanding a hyper-growth premium prompts caution.

While Shopify continues to innovate and expand its product offerings, maintaining a balance between sustained growth and realistic valuation remains crucial.

I remain watchful of Shopify Inc.'s evolving narrative and the implications for its market positioning in the coming quarters.

For further details see:

Shopify: Riding High On Promising Future Growth