SHOP - Shopify: Still Too Expensive

2023-10-14 03:33:34 ET

Summary

- Shopify is experiencing operational success with re-accelerating revenue growth and has once again become operating cash flow positive.

- The company's exposure to economic forces, particularly for its small and medium-sized business customers, could pose challenges if economic conditions worsen.

- The partnership with Amazon could increase the value proposition of Shopify and addresses concerns regarding competition.

- We believe Shopify's stock remains expensive and the overall risk/reward is unfavorable at this time.

Thesis

Shopify ( SHOP ) has become operating cash flow positive and is continuing to grow revenues in what many consider to be a difficult macroeconomic environment. Despite these positive developments, the company remains unprofitable on a GAAP basis and their SMB customer base could face increasing difficulties if economic conditions deteriorate due to the rapid pace of interest rate increases. We believe that Shopify is a solid company but is currently overvalued.

Operational Successes

Shopify is continuing to re-accelerate revenue growth after the sharp decline in growth experienced in 2021-2022. This demonstrates the staying power of their platform and helps to calm investor fears over a permanent slowdown in growth.

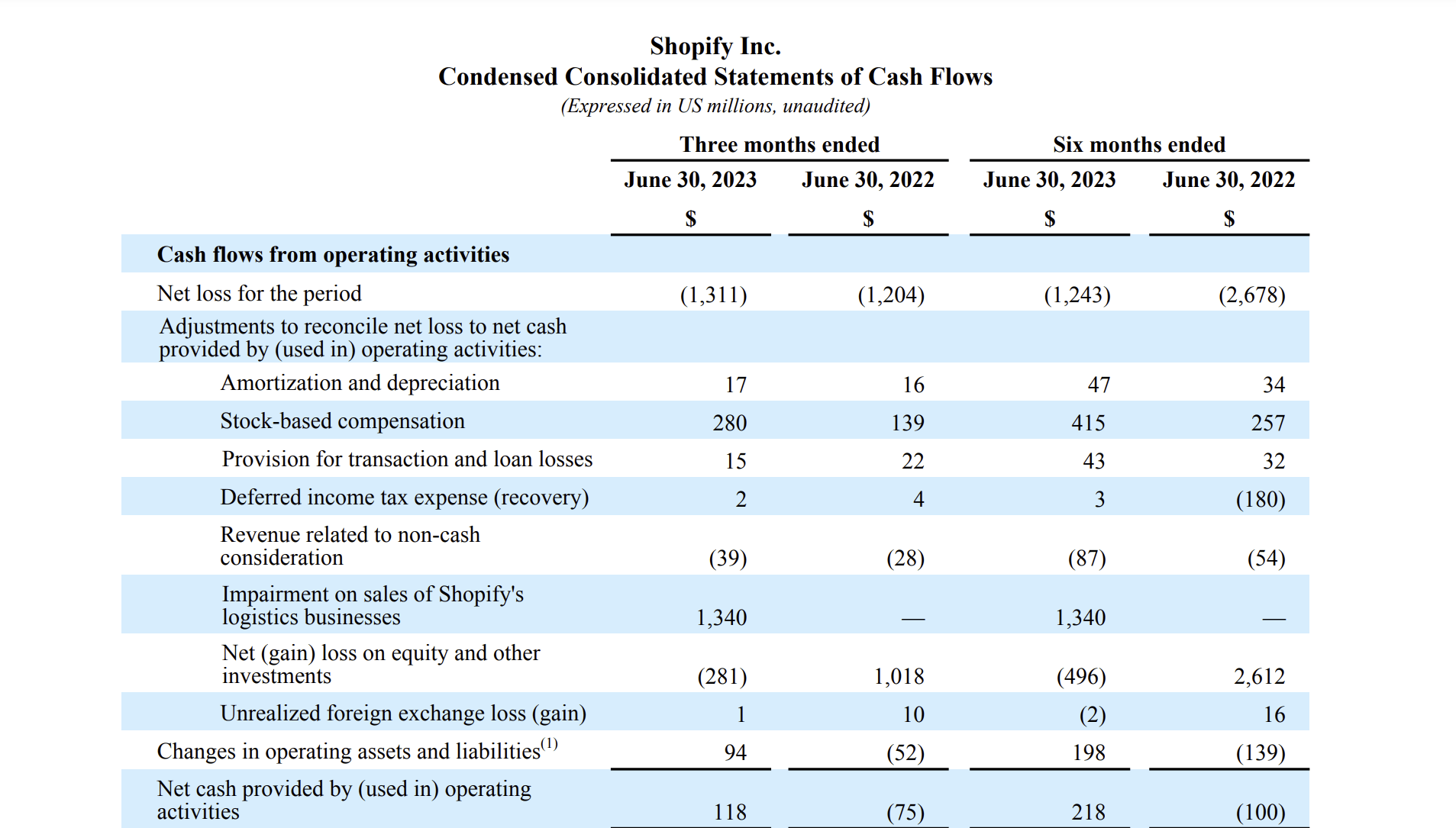

Shopify has become operating cash flow positive once again, which is another welcome development and helps to de-risk the fundamental thesis.

Operating Cash Flows (Shopify's Quarterly Earnings Release)

{kind=link}

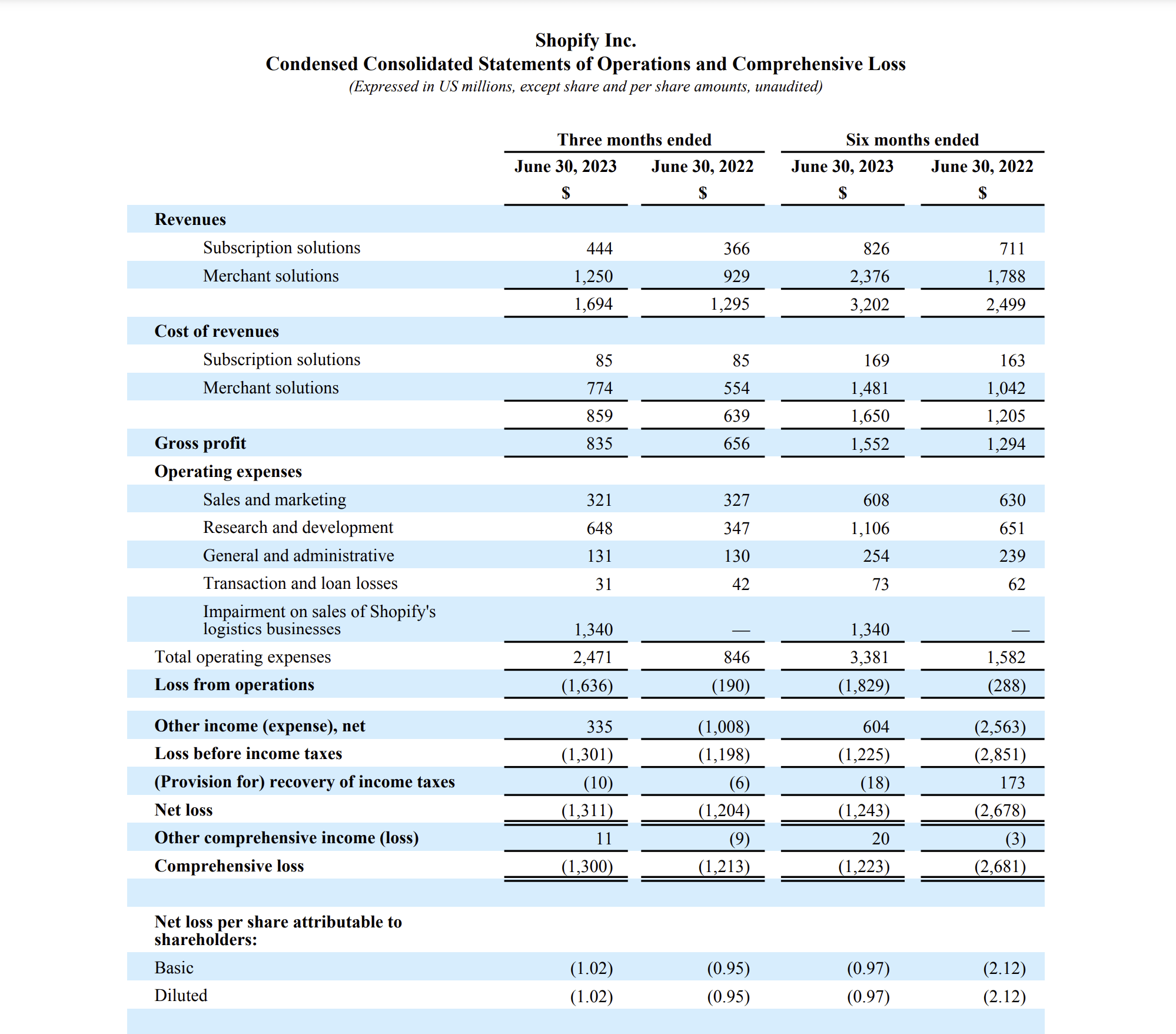

In their most recent quarter, Shopify would likely have generated positive net income absent the impairment on the sale of their logistics business. It's entirely possible that the company will become GAAP profitable in the next couple of quarters, which could attract additional investors to the stock.

Income Statement (Shopify's Quarterly Earnings Release)

{kind=link}

Shopify is executing well, but due to the nature of their business, they have an above average exposure to macro-economic conditions. This risk factor could cause them to experience difficulties in the future.

Exposure to Economic Forces

The majority of Shopify's customers are small and medium-sized businesses. This means that their customer base is likely more exposed to economic conditions than larger firms. Rising interest rates have increased the cost of capital for all businesses, and firms may face increasing financial pressure if they have to borrow at these new rates. Shopify could lose some of their customers permanently if economic conditions deteriorate. At the very least, a weak economy may serve to slow revenue growth. Fortunately for investors, Shopify has a pristine balance sheet and capital light business model. These difficulties would not threaten the businesses viability and would simply reduce the present value of the firm.

Amazon Partnership

A potential catalyst for the business comes in the form of a partnership with Amazon. You can read Amazon's press release here and Shopify's press release here . In Shopify's words:

Amazon will be releasing an app in Shopify’s app ecosystem that will give US-based merchants who use Amazon’s fulfillment network the option to add Buy with Prime into their Shopify Checkout processed by Shopify Payments.

Shopify merchants will have the choice to offer their products to Prime members on Shopify for the first time ever while continuing to maintain 100% control of their brand and their customer data in Shopify’s admin.

This partnership further increases the value proposition of Shopify and helps their customer's businesses run more smoothly. While it might not seem like a lot, this goes a long way towards addressing some of the concerns that SMBs have with using Shopify. This also shows an increased level of cooperation between Amazon and Shopify, which helps to reduce fears that Amazon is seeking to run Shopify out of business.

Price Action and Valuation

Shopify's stock has done well this year but has declined in recent months. Investors who are bullish on the company can use this as a buying opportunity, but we believe the stock remains expensive.

Shopify continues to trade at a high forward PE ratio but is making continued progress in improving profitability. In light of a 30% revenue growth rate, we believe a forward PE of over 100 is too high. Amazon is currently trading at a forward PE of 60, and we believe that this would be a good valuation to take another look at Shopify. While not a perfect analog, Shopify lacks the cloud computing division but has a higher growth rate and lower capital intensity. These factors can roughly cancel each other out. We would note that a forward PE of 60 for Shopify is still aggressive and would merely be the point where we would consider taking a position. We would likely wait for it to go even lower before pulling the trigger, as there are currently better opportunities out there.

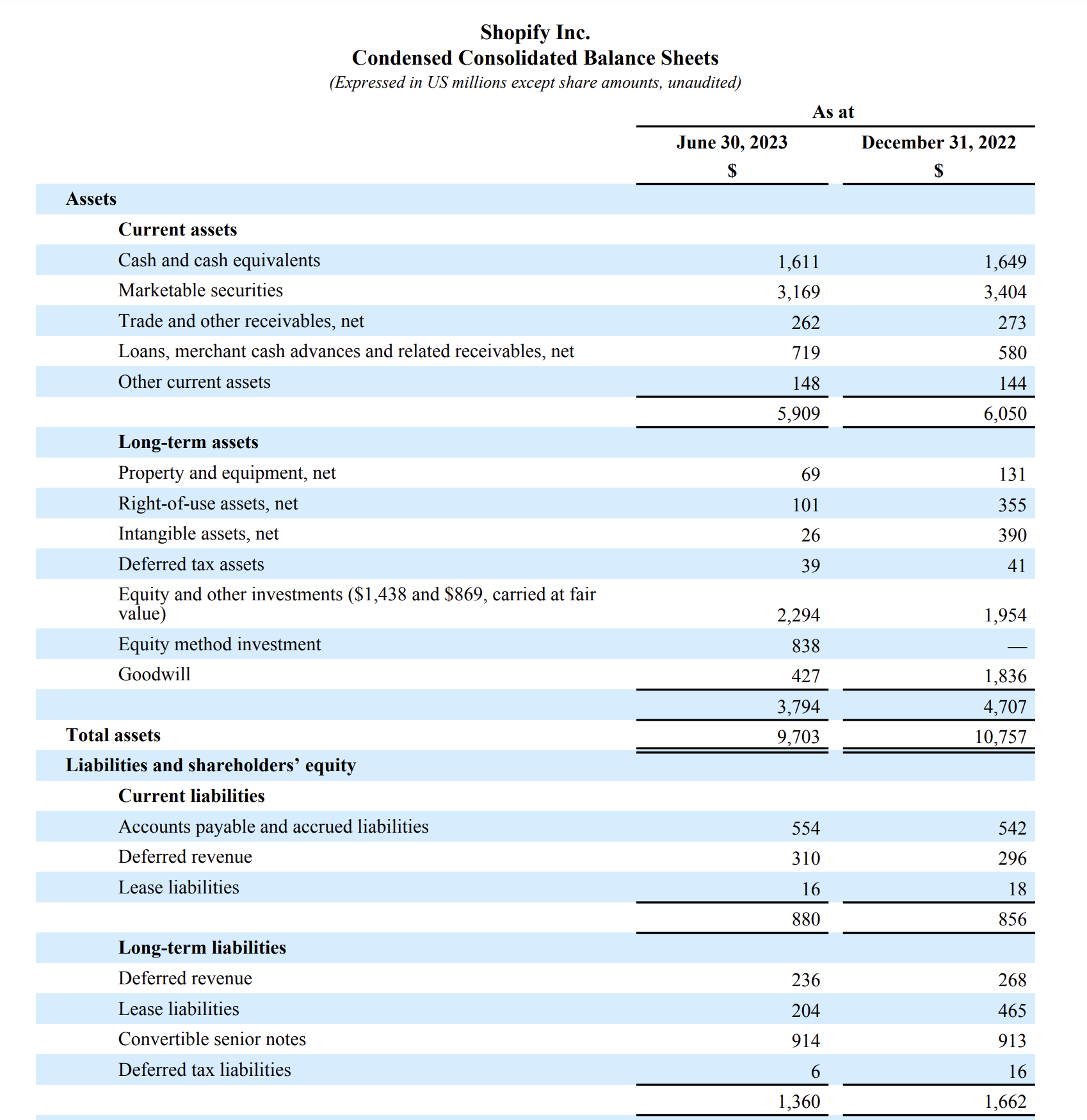

The company has a clean balance sheet, which helps to significantly de-risk the business. Their total liabilities are less than their cash on hand, which is about as good as an investor can expect from a company. A potential area of concern is their substantial investments in other companies ("equity and other investments" and "equity method investment"), but an impairment of those assets wouldn't threaten the viability of Shopify itself due to the overall structure of their balance sheet and would simply reduce their book value. While such an impairment is never great, it's unlikely that investors are taking a position here based on the book value of equity.

Balance Sheet (Shopify's Quarterly Earnings Release)

{kind=link}

Shopify is an example of a high quality business that is trading at a rich valuation. We believe investors can wait for the valuation to become more palatable before taking a position here.

Risks

A risk to the bullish thesis is the potential for higher interest rates to send the economy into a prolonged downturn, which would pressure Shopify's primarily SMB customer base.

A risk to the bearish thesis is the potential for the company to continue re-accelerating revenue growth and for the economy to grow at a fast pace at the same time as interest rates decrease. If all three of these things were to materialize, the company could have much stronger business fundamentals and see a sharp increase in share price as a result.

We believe the overall risk/reward is currently unfavorable. Staying on the sidelines appears to be a good idea at this juncture. Bullish investors may decide to use recent price weakness as a buying opportunity. At the end of the day, Shopify is a high quality business that could end up justifying their current valuation, it's just a question of whether an investor is comfortable with the risk.

Key Takeaway

Shopify's business fundamentals are continuing to improve, but questions remain about whether the trend can continue. We view the company as being overvalued at this time, but will keep an eye on it.

For further details see:

Shopify: Still Too Expensive