KD - Should You Buy The IBM Turnaround?

2023-04-13 18:58:54 ET

Summary

- International Business Machines Corporation is in the middle of a turnaround, streamlining its business after many years of aggressive acquisitions.

- IBM Revenue forecasts, however, remain depressed.

- We believe that a successful IBM turnaround is possible, but that patience is likely to be rewarded.

Overview

The current macro environment of high interest rates and persistently high inflation has been tough for most industries, but especially difficult for some. For tech and, more specifically, companies that support data storage and the personal computing market, the environment is turning downright painful.

Against this backdrop, we have been assessing the largest players in the space, and how their prospects appear going forward. Today we review International Business Machines Corporation ( IBM ) and assess whether or not the company is attractive to potential investors today.

Backdrop

IBM operates in four segments across more than 175 countries: Software, Consulting, Infrastructure, and Research.

Software is the IBM largest business segment, generating $25 billion in revenue for the company in 2022. While the software segment spans a dizzying array of functions and industries, we think it's informative to note that IBM's open-source enterprise software application Red Hat (part of the Software segment), is, according to IBM's most recent 10-K , "one hundred percent of commercial banks, telecommunication, media and technology companies in the Fortune Global 500 rely on Red Hat."

Consulting and Infrastructure generated $19 billion and $15 billion, respectively, for the company in 2022.

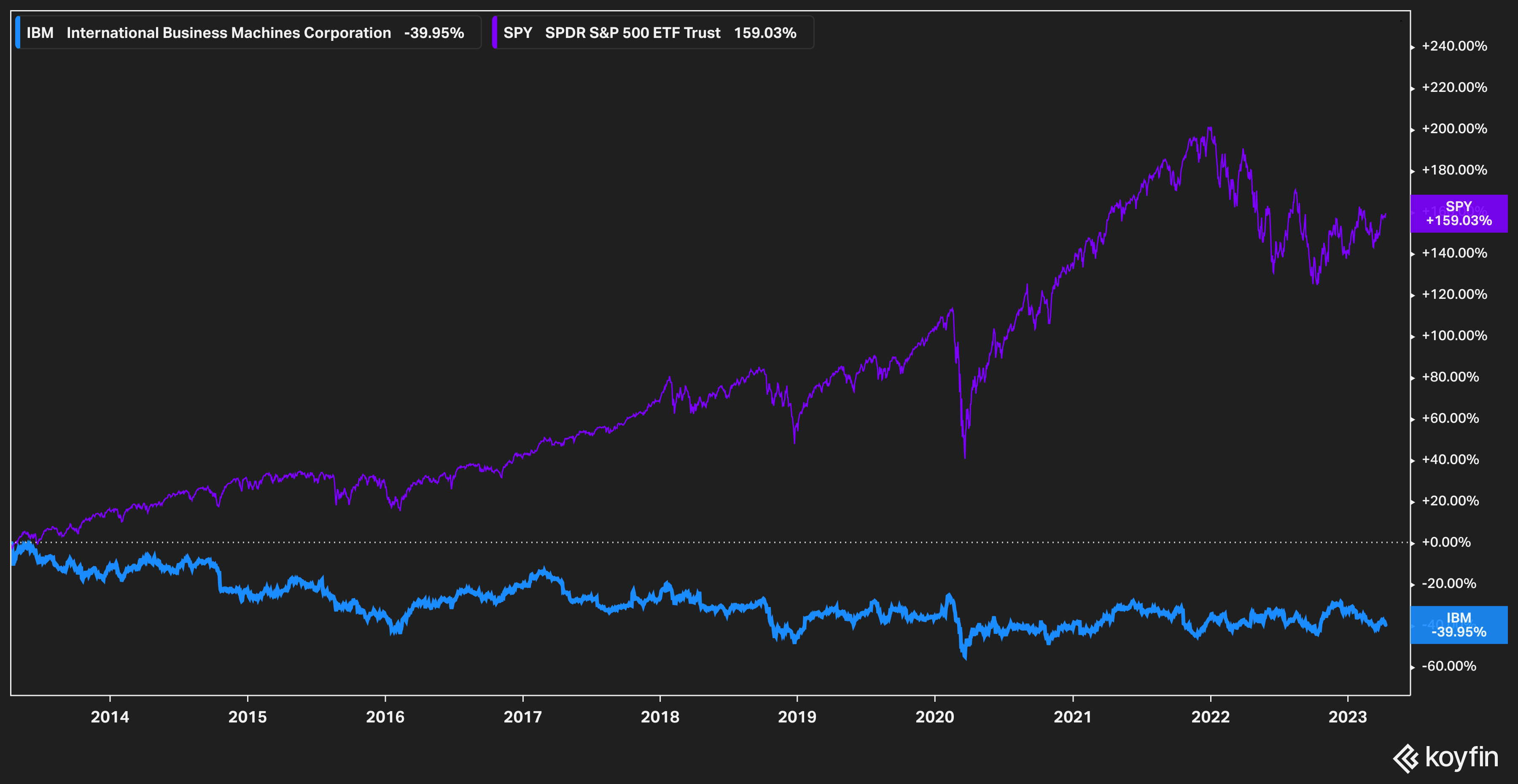

Given the company's size (it has a $115 billion market capitalization), as well as its ubiquity throughout the business landscape (most businesses rely, whether they know it or not, on IBM technology in some form or fashion), it is surprising then to see how the stock has performed over the last ten years, losing 40% of its value while the SPDR® S&P 500 Trust ETF ( SPY ) has rallied over 150% in the same time frame.

{kind=link}

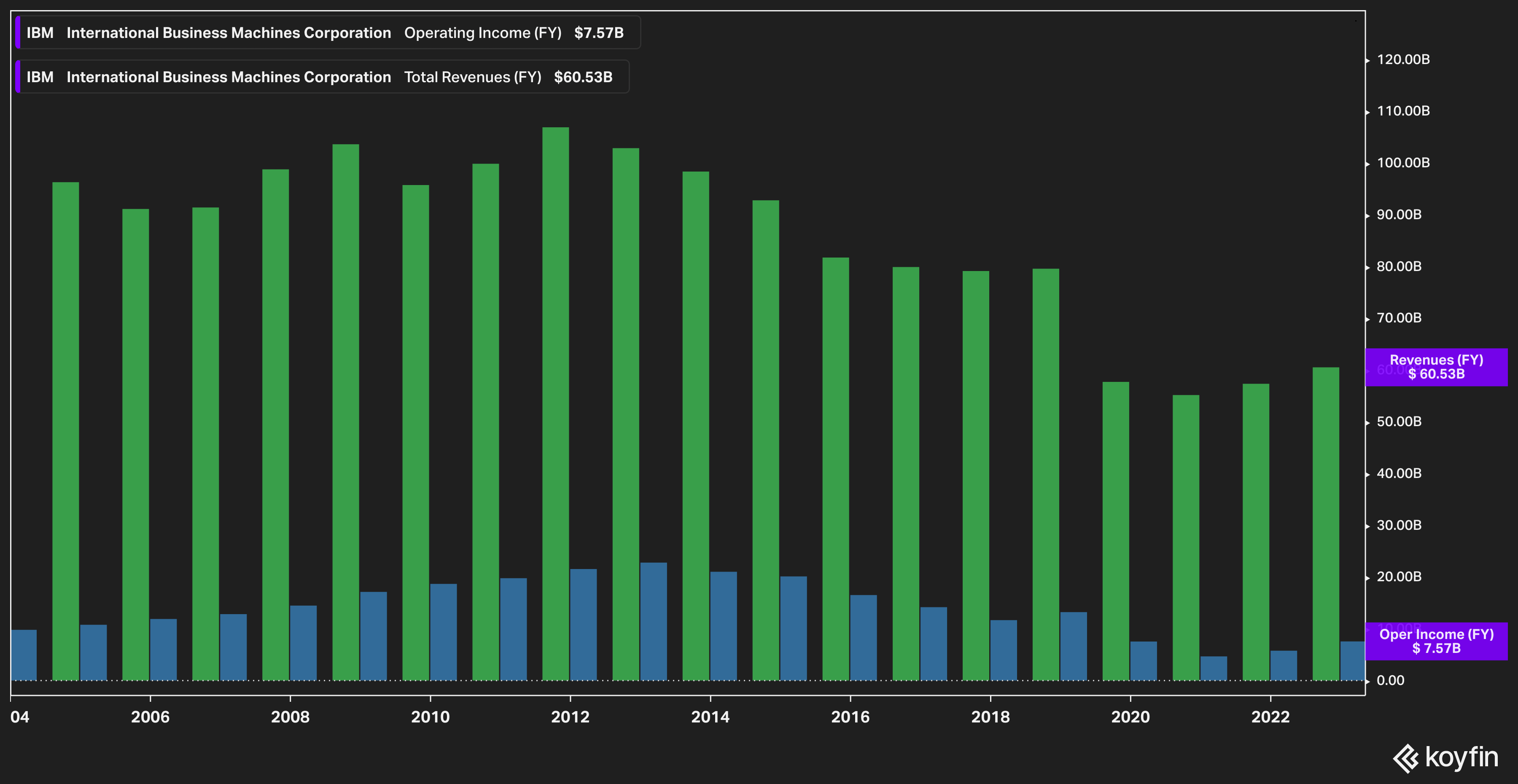

The most obvious reason why IBM stock has failed to keep up with the broader market is the fact that IBM's revenues and operating profits have steadily declined over the same period.

{kind=link}

What the chart above illustrates, in our view, is a company that is perhaps a bit too bloated with acquisitions and operations and in need of streamlining. This, happily, is exactly what management is attempting to do.

A Leaner, Meaner IBM

They say that one man's trash is another man's treasure, and we would opine that the saying seems just as applicable to corporate management teams. Acquisitions that seemed to make all the sense in the world at their time of their closing can age poorly, creating hefty competition for resources within the organization and spreading management thin.

In 2021, IBM completed its spinoff of Kyndryl Holdings, Inc. ( KD ), in which IBM retained a stake. For reference, Kyndryl posted full year 2022 revenue of $18 billion. In 2022, IBM also sold off its Watson Healthcare unit to a private equity firm. The Wall Street Journal also reported that IBM is exploring a potential sale of its Weather Channel unit, which it acquired in 2015.

Spinning off acquired companies in order to give more focus to IBM's hybrid cloud and AI business, to us, makes all the sense in the world. Given the long potential runway and addressable market that AI could have (CEO Arvind Krishna estimated that AI would be a $16 trillion market by 2030 in the latest earnings call ), we believe that a renewed focus on this market will likely be a smart move for IBM in the mid-term (3-5 years).

Looking To The Future

However, promising a turnaround and delivering on one are two different things, and we are not prone to take management teams at their word.

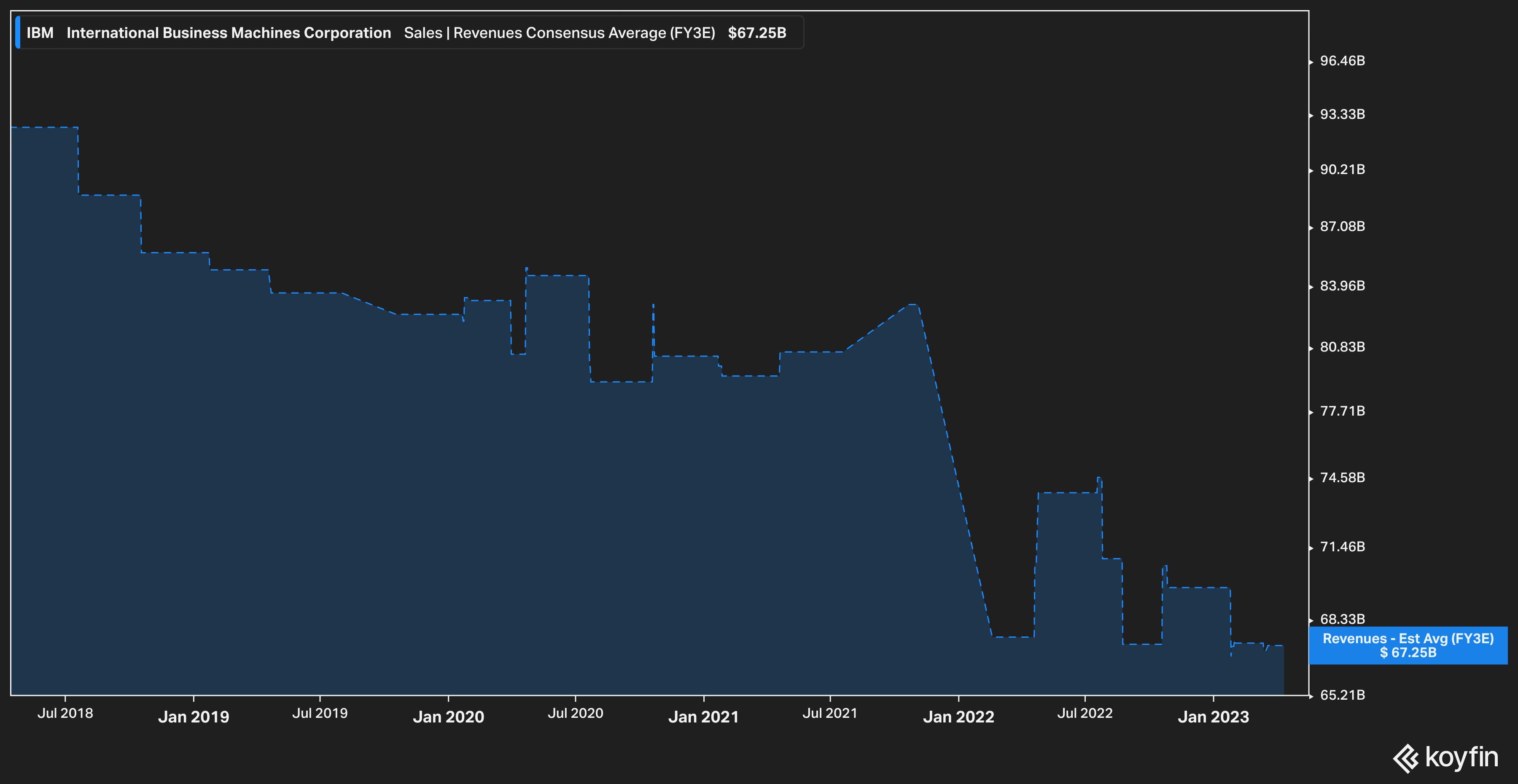

Analysts do not seem to believe it yet, either.

{kind=link}

Looking out to 2025, the current average analyst estimate for IBM's revenue is $67 billion, a little more than 10% over 2022's revenues. While it is good to see that analysts overall expect IBM to grow, 10% top-line growth over three years isn't exactly stellar. These expectations, along with management's guidance, are things we intend to closely monitor over the coming months for any signs of an upside reversal.

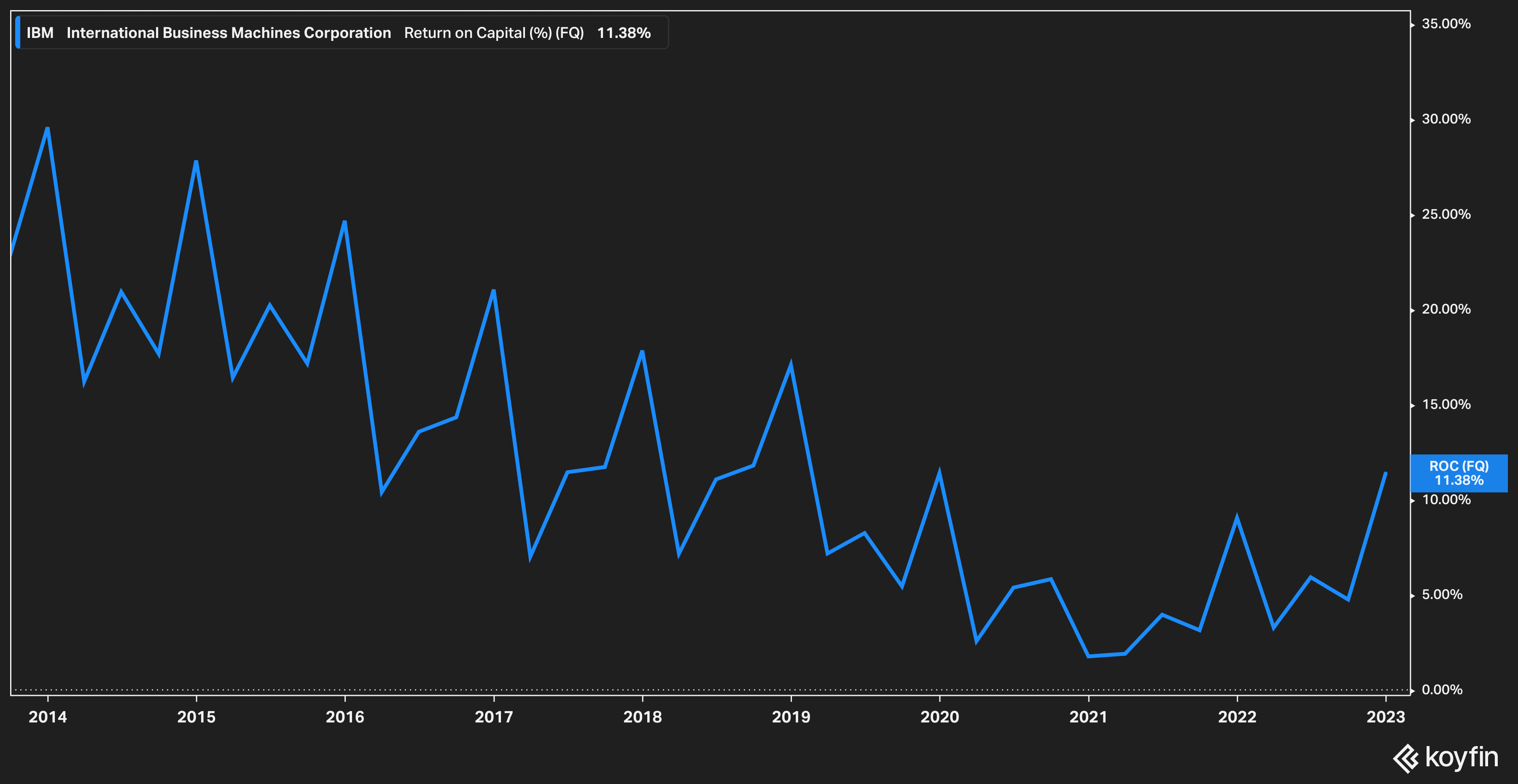

Yet, there are positive signs as well beginning to emerge at IBM.

{kind=link}

IBM has experienced a steadily declining return on capital over the past ten years. We at Ironside Research watch this metric closely, since if a company is not able to generate returns on capital that are above its cost of capital, then things are likely to go poorly long term.

After bottoming out in 2021 at around 5%, returns have begun to tick back up, with IBM turning in a respectable 11% return on capital to close out the fourth quarter of 2022.

Putting It All Together

It has been a difficult few years--a few decades even--for IBM. The company has struggled to find a way to operate efficiently and generate consistent revenue growth. For a while the company aggressively pursued a strategy of acquisitions, but over the years this strategy failed to produce the desired results.

Management seems committed to streamlining IBM and returning it to its former glory. While we believe the IBM turnaround is possible, we think that the time it will take to bear fruit is likely to be 2-3 years from now.

For further details see:

Should You Buy The IBM Turnaround?