IONQ - Should You Hold Or Sell IonQ Stock? Here's What You Need To Know

2023-11-21 03:00:02 ET

Summary

- IonQ is making significant progress in developing quantum computing technology, which has the potential to revolutionize various industries.

- The company is potentially ahead of its competitors in developing viable quantum computing solutions and aims to capture a significant portion of the market.

- While IonQ's technology is impressive, new investors may want to avoid buying the stock due to its early-stage status and potential overvaluation.

IonQ ( IONQ ) has become one of the more exciting stocks this year due to its significant progress in developing its quantum computing technology. If you are unaware of quantum computers, the technology can potentially solve problems that classical computers would take too long to figure out. If quantum computers succeed, they could revolutionize Artificial Intelligence ("AI"), drug discovery, financial modeling, materials science, and more. It could become one of the most impactful technologies introduced this decade.

The company has already moved past the proof-of-concept phase and is well into developing Enterprise-grade hardware and applications. Some analysts think IonQ has advanced to the furthest in developing a viable quantum computing solution -- a pure-play first mover. The company believes competing companies and solutions lag far behind, positioning it to grab much of the value created at the beginning of what some believe is the start of the quantum computing era.

While the company's technology is remarkable, there are reasons new investors might want to avoid buying the stock at this time. First, IonQ is still a very early-stage company. Bearish investors argue that there is no clear path to creating profits, and they may be correct. The stock has also risen substantially this year, and some may consider the stock overvalued.

This article will discuss IonQ's position in the quantum computing industry, its latest earnings report, and why existing investors willing to speculate should continue holding the stock.

The company's quantum computing roadmap

Classical computers use bits to represent information as a one or a zero (digitally) and solve problems linearly, meaning they only work on one task at a time. Quantum computers use a basic unit of information in quantum mechanics called a qubit, which can exist as zero and one simultaneously. If you have never studied quantum mechanics, you may have difficulty comprehending how something can be two things at the same time. However, on a subatomic level, particles can exist in a superposition state, meaning particles can exist simultaneously in multiple states. Quantum computers use the ability of qubits to exist in multiple states to solve problems in parallel, meaning they can work on multiple tasks simultaneously to solve problems too complex for classical computers to do in a timely fashion, like optimization problems, data analysis, and simulations.

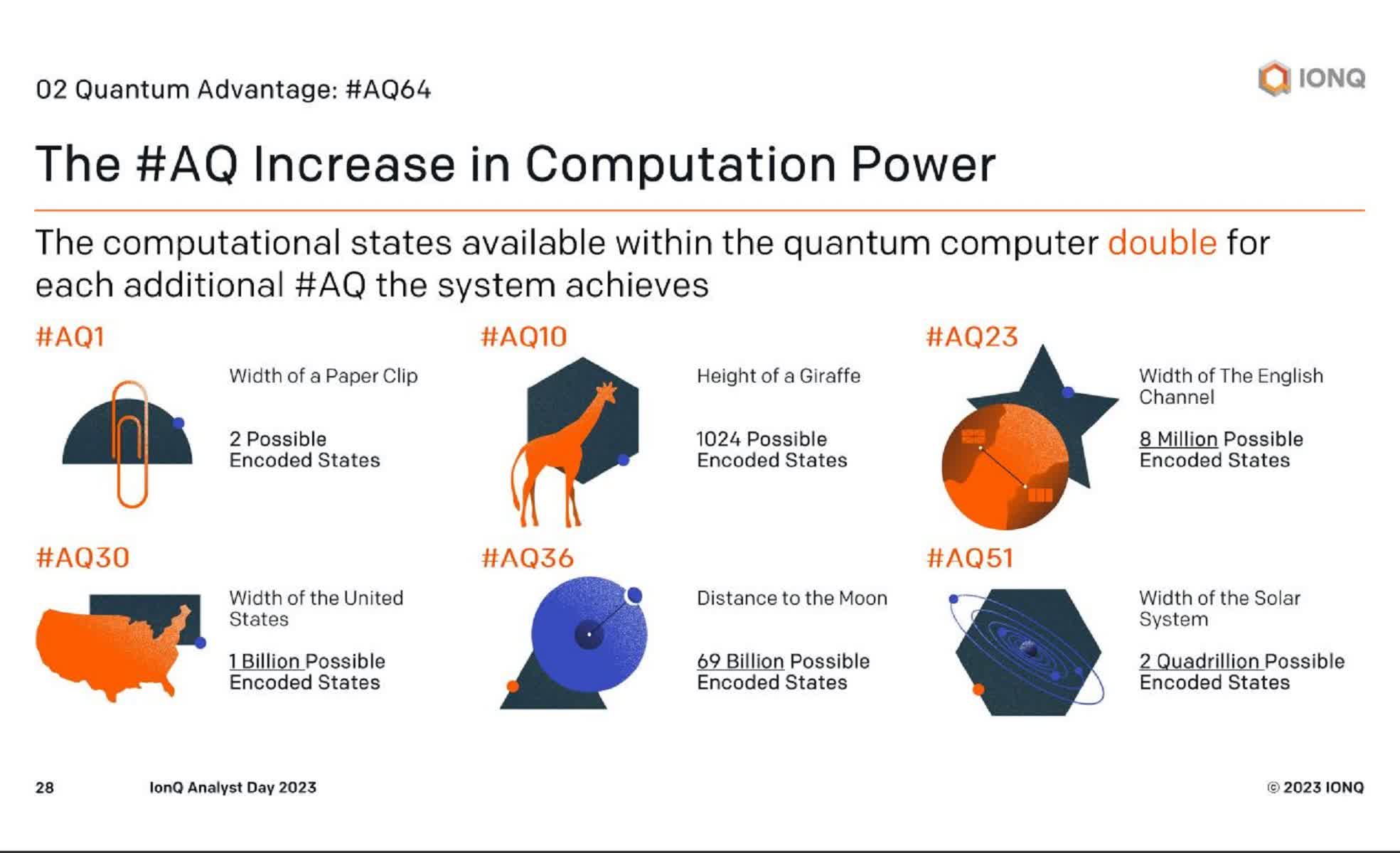

If you watch presentations where IonQ discusses its technology, the term #AQ will sometimes pop up, referencing an algorithmic qubit, a metric used to measure the computational power of a quantum computer. The company defines #AQ as "useable qubits" in a quantum computer. The chart below shows how much computing power IonQ can add to a quantum computer by adding "useable qubits."

{kind=link}

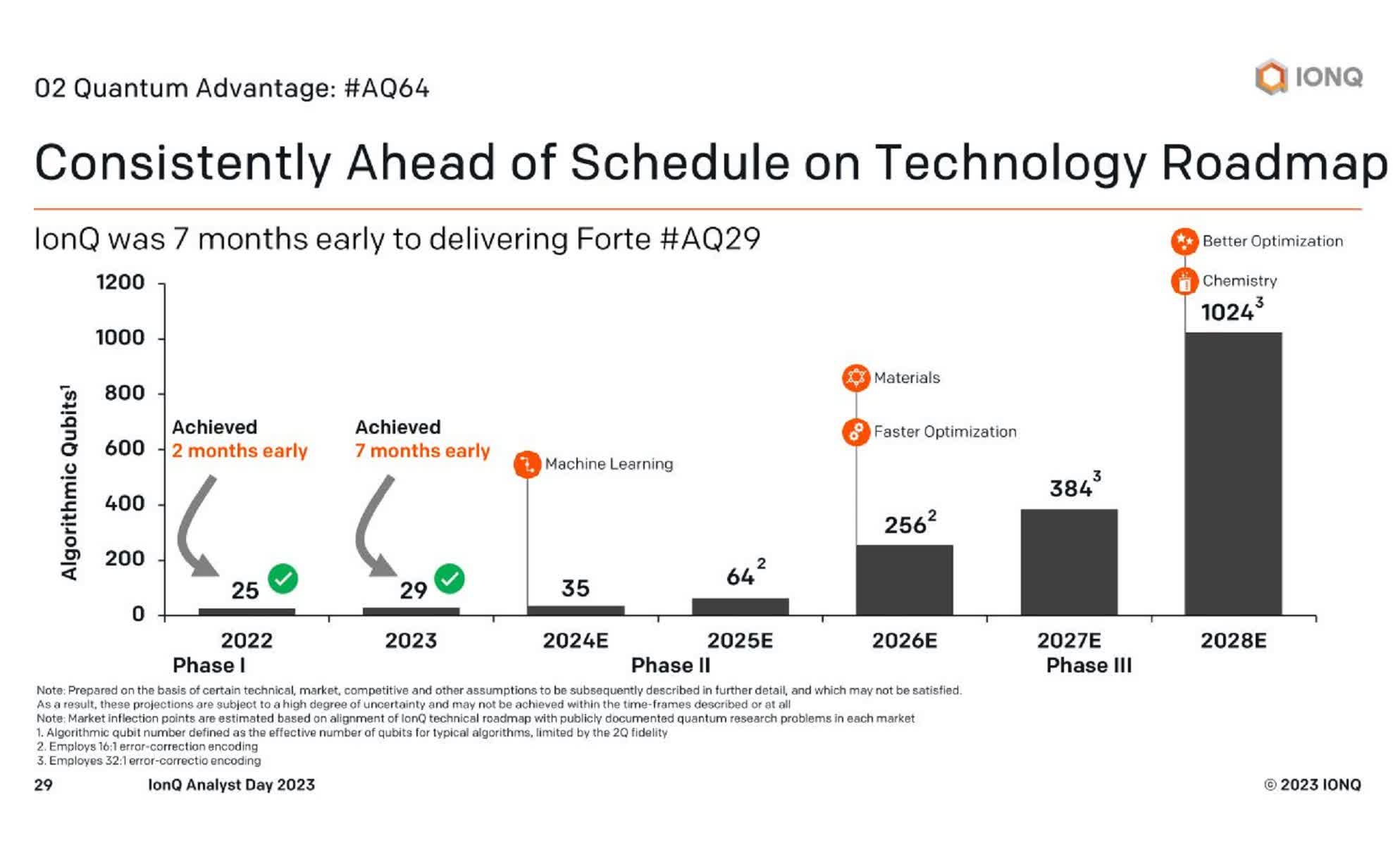

The following chart shows why some investors have grown excited about what this company can potentially do. IonQ achieved #AQ25 last year and has reached #AQ29 this year. Each increase in #AQ means the computer can calculate solutions to more complex problems faster. As seen below, the company expects to reach #AQ35 in 2024, at which it believes it can start using quantum mechanics in machine learning ("ML"). Using quantum computing for ML applications has the potential to revolutionize a wide range of industries, including healthcare, finance, and materials science.

{kind=link}

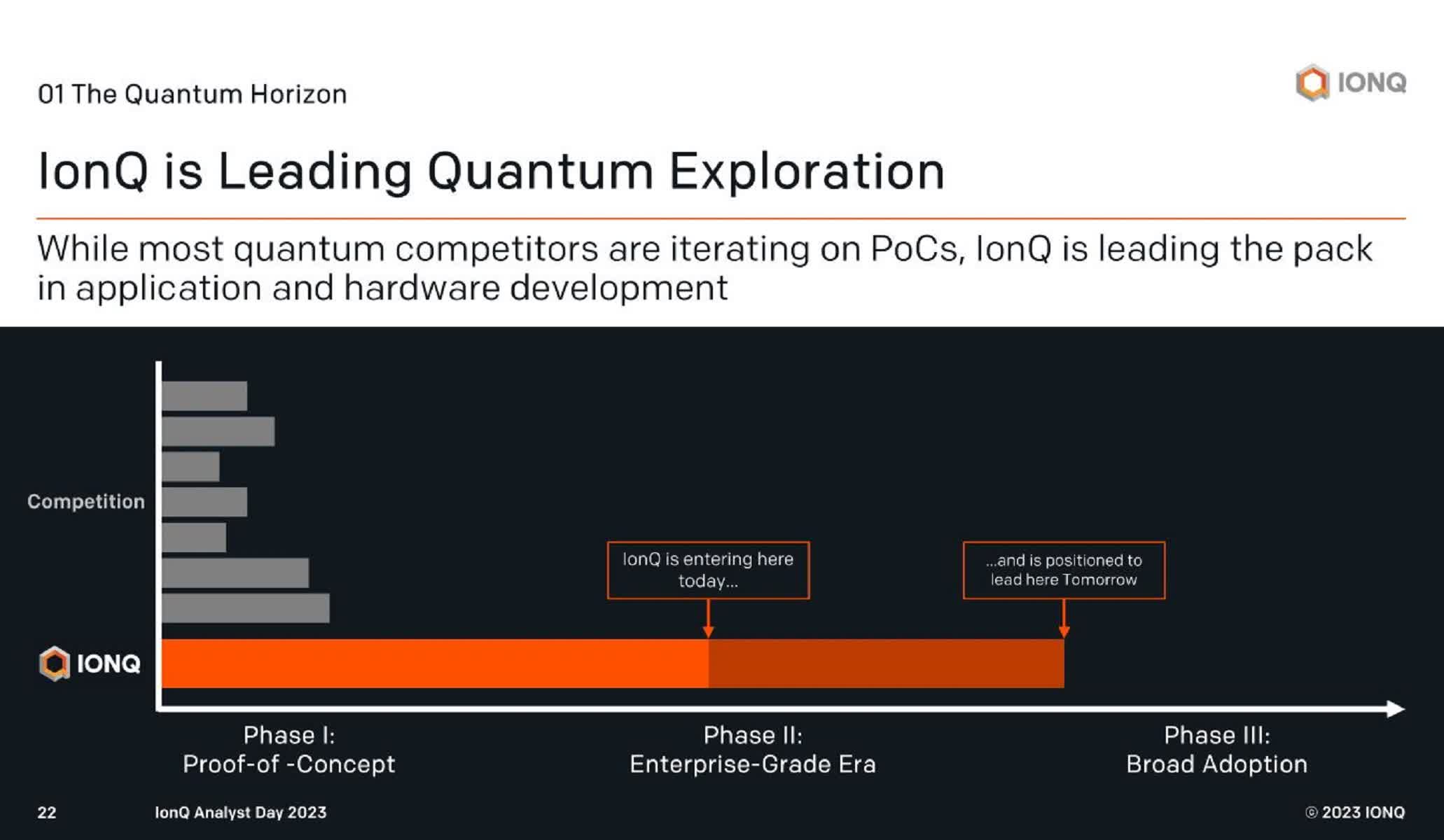

At the Quantum World Congress , it introduced the Forte Enterprise , its #AQ35 computer, and the IonQ Tempo , a #AQ64 computer that the company plans to release in 2025. According to the company, it is far ahead in introducing commercial solutions for the Enterprise. At the same time, most of its competition is stuck in the proof-of-concept phase, as indicated by the gray bars on the following chart.

{kind=link}

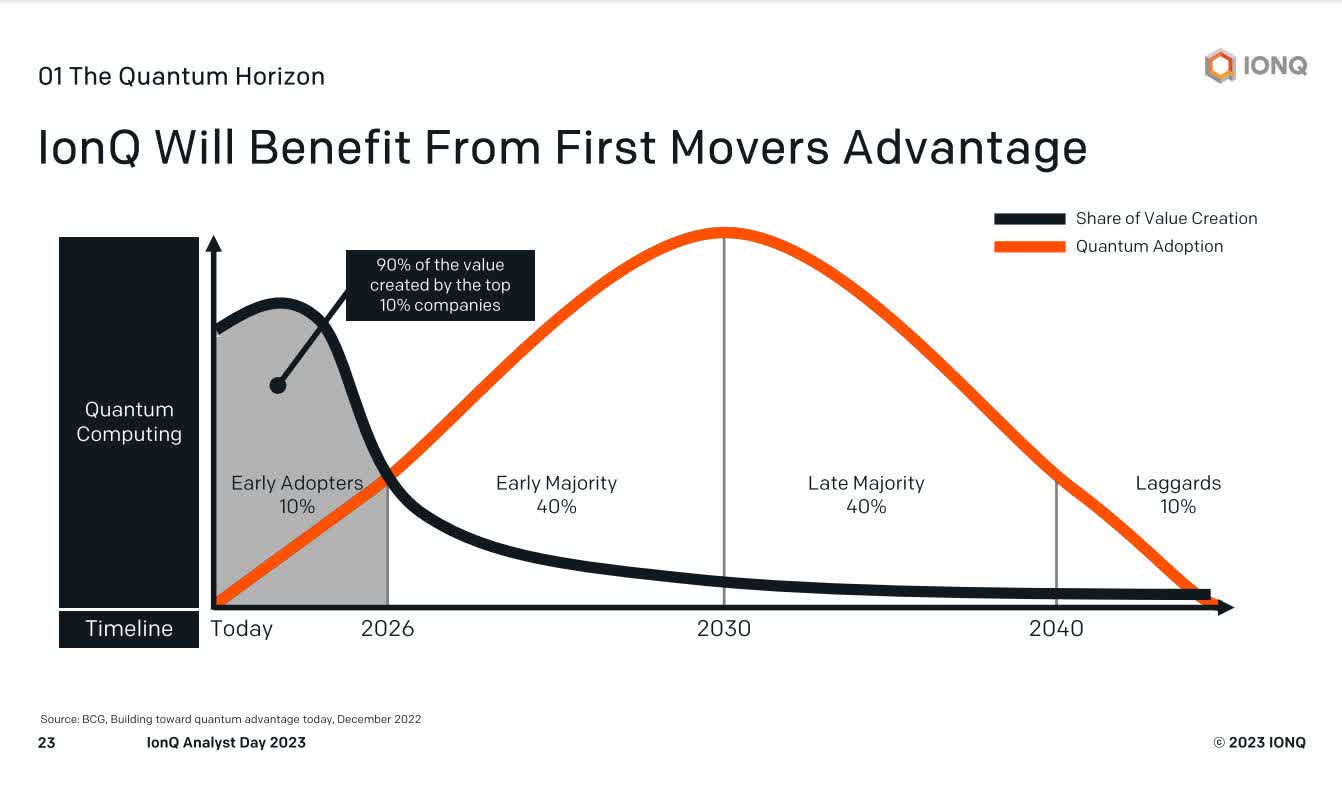

The following chart shows that by becoming a first mover in quantum computing, it expects to garner a significant amount of the potential value of the quantum computing industry by gaining market share among early adopters.

{kind=link}

As Amazon has proven in e-commerce and Alphabet's Google has proven in Search, gaining a first-mover advantage can be lucrative.

The potential of the quantum computing industry

During the company's 2023 Analysts Day, management showed several ways quantum computing could help existing clients solve real-world problems. For example, they showed how quantum computing could help Oak Ridge National Laboratory simulate chemical interactions for drug discovery.

{kind=link}

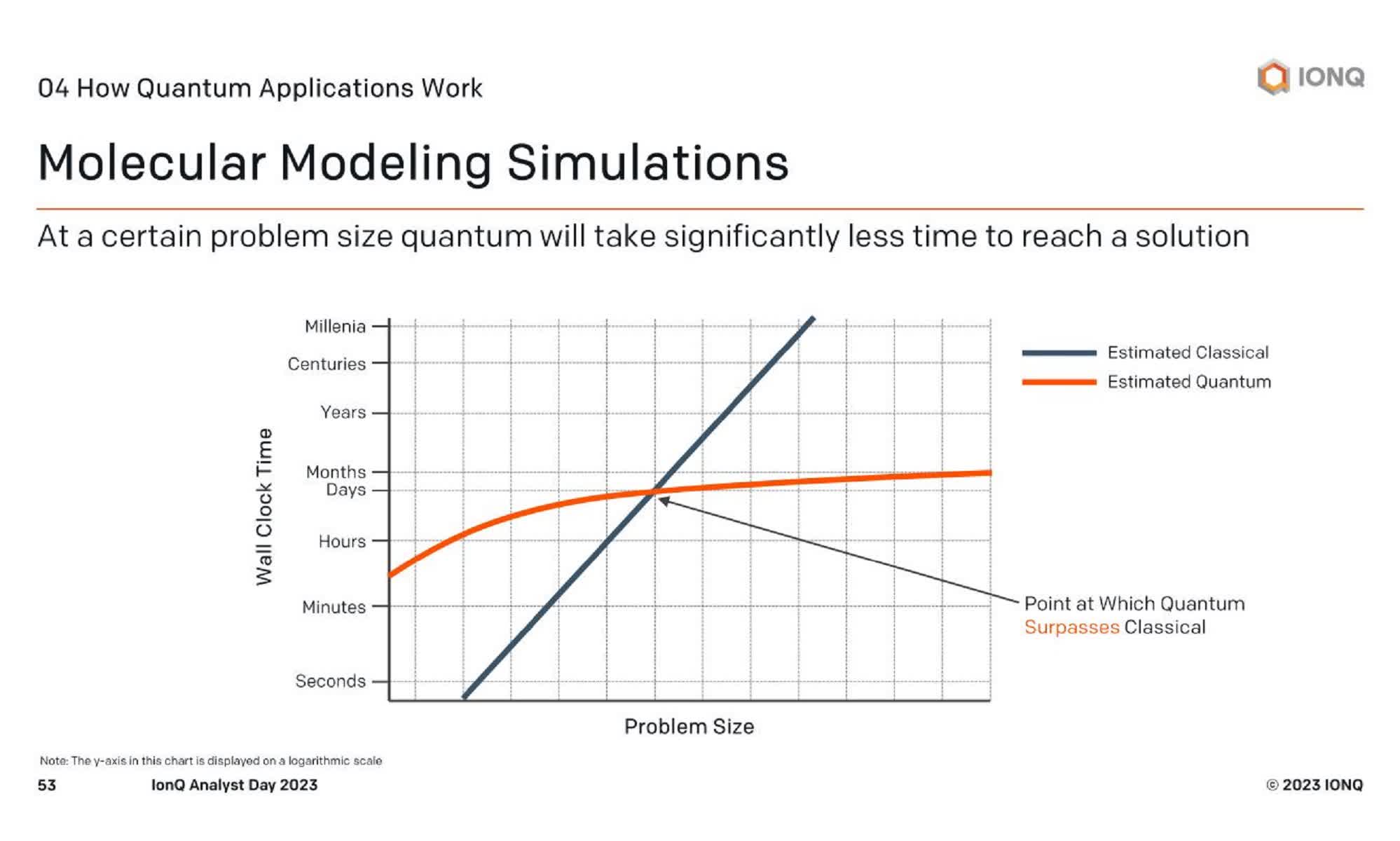

The chart below shows why many industries have become interested in quantum computing -- time. It's not that classical computers can't eventually solve complex problems like molecular modeling simulations; it's that a simulation might require a classical computer over a century to perform what might take a month for a quantum computer.

{kind=link}

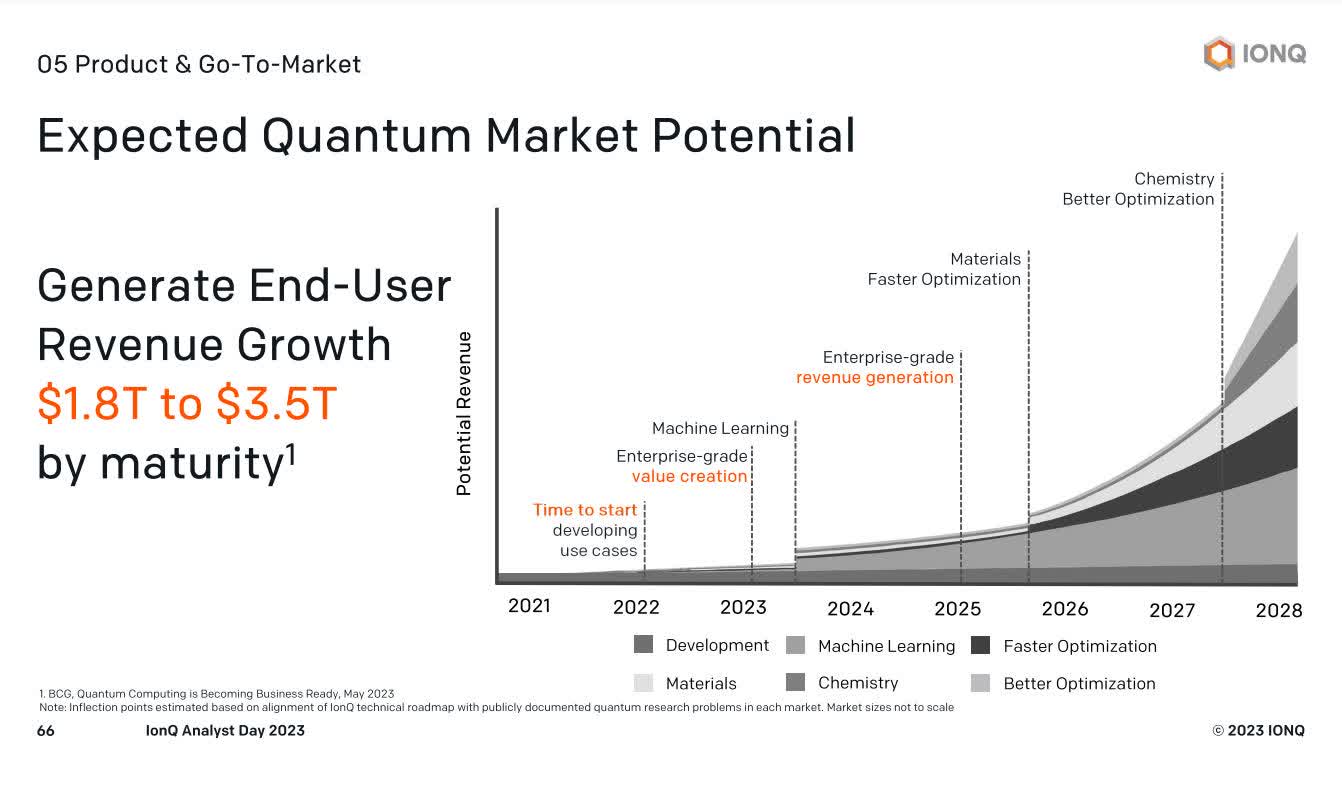

The company also showed how Airbus ( EADSF ) ( EADSY ) uses quantum computing to optimize complex cargo loading to reduce costs, and Hyundai ( HYMTF ) uses Machine Learning for image recognition to enable street sign reading in self-driving cars. There is an emerging demand for quantum computing services from Enterprise early adopters that some analysts believe will snowball. Market research company MarketsAndMarkets projects the total addressable market ("TAM") for quantum computing to grow from $866 million in 2023 at a compound annual growth rate of 38.3% to $4.375 billion in 2028. IonQ cites an article by BCG in the following image titled Quantum Computing Is Becoming Business Ready that projects that quantum computers will grow into a $1.8 trillion to $3.5 trillion market by maturity.

{kind=link}

Suppose you believe the TAM assumptions for the quantum computing market; it has massive upside potential if IonQ can remain a leader.

It has an excellent balance sheet

The company had $384 million in cash and short-term investments with zero long-term debt. On November 9, 2023, IonQ filed a universal shelf offering for $500 million. This Seeking Alpha article states , "The prospectus may include common stock, preferred stock, debt securities, warrants, depositary shares, subscription rights, purchase contracts, and units." The company doesn't need the money at this time. However, the CFO said, "While we continue to believe that our cash on hand is more than sufficient to get the company to cashflow positive and we have no immediate plans to raise additional capital, we also believe that opportunities for strategic M&A may arise in the near to medium term."

The financial fundamentals are poor

IonQ is gaining momentum in signing up new customers with $26.3 million in new bookings for the third quarter, which brings the total booking for the year to $58.4, above its full-year guidance range of between $49 million and $56 million. As a result, management raised the full-year guidance for bookings to between $60.0 million and $63.0 million. It generated revenue of $6.1 million , up 121% year-over-year, above the company's previously provided guidance and beating analysts' estimates by $1.14 million . The company increased its full-year revenue projection from $21.2 million to $22.0 million -- an excellent beat and raise quarter on the top line.

The main worry for this company comes when eyes hit the operating expense line. The company reported that its third-quarter Research and Development (R&D) rose 85% to $24.6 million, a shocking 400% of IonQ's quarterly revenue. Don't expect that number to go down any time soon, as the company needs to invest heavily in R&D to stay on its technology roadmap of increasing computational power. Third-quarter sales and marketing (S&M) costs grew 156% year-over-year to $5.0 million, 82% of its quarterly revenue. The company increased S&M to expand its sales and support team to aid its commercialization efforts. Total operating expenses were $48.33 million, 788% of its quarterly revenue, which is frightening if you think about it. The third quarter loss from operations was $42.194 million.

IonQ reported generally accepted accounting principles ("GAAP") earnings-per-share of -$0.22, missing analysts' estimates by $0.07. Even on an adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) basis, the company shows losses for the third quarter of $22.4 million. The company forecasts an adjusted EBITDA loss of $80.5 million for the year. It burned $28.03 million in cash during the third quarter and lost $79.92 million in trailing 12-month free cash flow ("FCF").

This company will need to continue investing heavily to commercialize its quantum computers. So, don't expect this company to produce bottom-line profits or FCF in the near future. Management predicted a long period of unprofitability since IonQ entered the public markets in 2021. According to the company's S-1 prospectus risk section:

We believe that we will continue to incur operating and net losses each quarter until at least the time we begin significant production of our quantum computers, which is not expected to occur until 2025, at the earliest, and may occur later, or never. Even with significant production, such production may never become profitable.

Source: IonQ S-1

So, if you ever see massive top-line growth from this company in the future, it is wise to temper your upside expectations for the stock. While the top line is important, remember that it is equally important to see IonQ progress toward profitability at some point. Right now, investors are giving it a pass, understanding that the company is in the first stages of commercialization. However, eventually, investors will want to see progress toward profitability.

Risks

IonQ entered the public markets through a special purpose acquisition company ("SPAC") on October 1, 2021 . Usually, companies brought public via a SPAC have a limited operating history, are unprofitable, and are very risky. Additionally, technology SPACs have a history of doing poorly compared to companies that faced more stringent compliance and regulatory requirements in an initial public offering. So, buyer beware.

Next, quantum computing is an extraordinarily complex field. Unless you are a quantum physicist or an engineer, it may be difficult to understand and assess the technology enough to determine IonQ's chances of succeeding or whether a competitor has a better mousetrap. If you are an " Invest in what you know " investor, consider whether you understand the technology enough to make a good investing decision with this company.

Another risk investors should consider is whether the company can eventually build a scalable quantum computer. Despite management talking glowingly about the company's technology prowess during investing conferences and earnings calls, the company still faces considerable challenges in building scalable quantum computers. Scalability means a manufacturer can increase the number of qubits without significantly decreasing performance. IonQ lists the following risk in its latest 10-K , "We have not produced a scalable quantum computer and face significant barriers in our attempts to produce quantum computers." IonQ may never build a scalable quantum computer, or it could take the investment of significant funds in R&D for far longer than Wall Street or investors may be comfortable with.

IonQ also has significant competition in developing a scalable quantum computer. Although the company has found customers for its initial quantum computers, and management believes it's a first mover in commercializing the technology with enterprises, other companies with far more resources also have big plans for commercializing quantum computers. For instance, IBM ( IBM ) plans to sell thousands of 4000 qubits quantum computers by 2025. Contrary to IonQ management's assertions about being a quantum computing first mover, IBM considers itself the quantum computing leader .

Additionally, there is another publicly traded company called Rigetti Computing ( RGTI ) that some consider a leading pure-play company in quantum computing. This company recently received a contract with the U.S. Air Force for quantum foundry services. In August 2023, it achieved an 84-qubit quantum computer, far larger than IonQ's current 29-qubit quantum computer. Plus, a few other companies are developing quantum computers using various technologies. No matter which company currently "leads," the industry is so early that no one can predict which companies will be the ultimate winners.

Last, company co-founder and Chief Science Officer Chris Monroe recently left the company. IonQ gave no reason for his departure beyond saying, "Dr. Monroe will be returning to his academic, research, and policy pursuits." The company announced the news on October 23, and in a knee-jerk reaction, the stock dropped 27% to an intraday low of $9.23 on October 31. How will this impact the company in the long term? No one knows yet.

Should you buy, sell, or hold it?

IonQ is a complex stock to value for multiple reasons. At this point in its development, it barely generates sales, is unprofitable and burning cash, has a minimal operating history, and little certainty that it can develop a scalable quantum computer. It has a price-to-sales (P/S) ratio of 129.31 compared to a competing quantum company, Rigetti Computing, with a P/S ratio of 9.53.

An investor could argue that IonQ deserves a much higher valuation than Rigetti because it grows revenue faster. However, both these companies are in such an early stage of commercialization that year-over-year growth rates could be meaningless. One or two contracts of a few million dollars could make quarterly year-over-year growth rates look impressive.

The few valuation ratios IonQ has are well above its sector median. For instance, it has a price-to-book (P/B) ratio of 5.20 compared to a sector median of 2.74. Trying to value the company using a discounted cash flow model is impossible, as the company may not generate cash flow for quite a while.

This company's stock price has risen mainly on the promise of what quantum computing can theoretically do and the company's initial progress in commercializing the technology. However, there are significant hurdles to realizing the promise of quantum computing. As investors begin to understand this company's risks, they may become disenchanted with the stock. Risk-averse investors should stay far away from IonQ.

Considering the risk that IonQ might never become profitable, I don't recommend buying it after the stock's massive move up this year. However, suppose you are a speculative investor that already owns shares. In that case, the stock has enough potential upside that it may be worth it to hold a few shares in the speculative portion of your portfolio. I recommend a Hold.

For further details see:

Should You Hold Or Sell IonQ Stock? Here's What You Need To Know