SIEGY - Siemens: The Best AI Play Everyone Ignores

2023-07-18 05:22:30 ET

Summary

- In my view, Siemens is the most undervalued industrial conglomerate in the world with a market capitalization of over $100 billion.

- SIEGY stock may be overlooked by AI chasers today due to the company's past struggles, but it's important to recognize that those reasons don't make sense anymore.

- Siemens AG's recent financial results demonstrate a resilient financial position, with significant sales growth, improved gross margin, and a substantial increase in operating income.

- Despite the impressive rally last year [+74%], SIEGY is currently trading at only 14.6 times expected earnings, at the lower limit of the maximum historical range.

- Based on a combination of comparative and fundamental valuation analyses, I conclude that SIEGY is undervalued by 36.6% today. It's the best-undervalued AI play out there, in my view.

The Company

Siemens Aktiengesellschaft ( SIEGY ) is a $134-billion market cap global technology company focused on automation and digitalization. The company offers a wide range of products, solutions, and services in areas such as automation systems, software, sustainable energy, transportation, healthcare technology, and financial services.

Siemens operates in various segments including Digital Industries (31.8% of total sales in 1H FY22 ), Smart Infrastructure (28.3%), Mobility (15.2%), Siemens Healthineers (31.1%), and Siemens Financial Services (<1%). Also, ~4.5% of consolidated sales come from portfolio companies.

Recent Financials

The first half of fiscal 2023 proved to be the best for Siemens. Against the backdrop of a relatively low base in FY2022, the company was able to significantly increase its sales - growth of more than 10% for an industrial group worth billions seems like a significant event to me. Thanks to cost-cutting measures, Siemens was able to significantly increase its gross margin, and further down the operating income statement, we see the positive effect of having operating leverage - the company is now generating 49% more operating income than in FY2013 [ a record year for SIEGY's revenue volume ]. Therefore, the year-over-year momentum we see in the latest income statement does not just reflect growth from a low base - SIEGY is truly showing top results from its historical perspective.

| 1st half results |

|---|

| FY 2023 |

| FY 2022 |

| YoY ch., % |

| Sales |

| 37 486 |

| 33 537 |

| 11.8% |

| COGS |

| (23 321) |

| (21 591) |

| 8.0% |

| GP |

| 14 165 |

| 11 946 |

| 18.6% |

| OPEX + interests |

| (7 802) |

| (7 747) |

| 0.7% |

| EBT |

| 6 363 |

| 4 199 |

| 51.5% |

| Taxes |

| (1 167) |

| (1 177) |

| -0.8% |

| Net income |

| 5 196 |

| 3 022 |

| 71.9% |

Source: Author's work, based on SIEGY's results

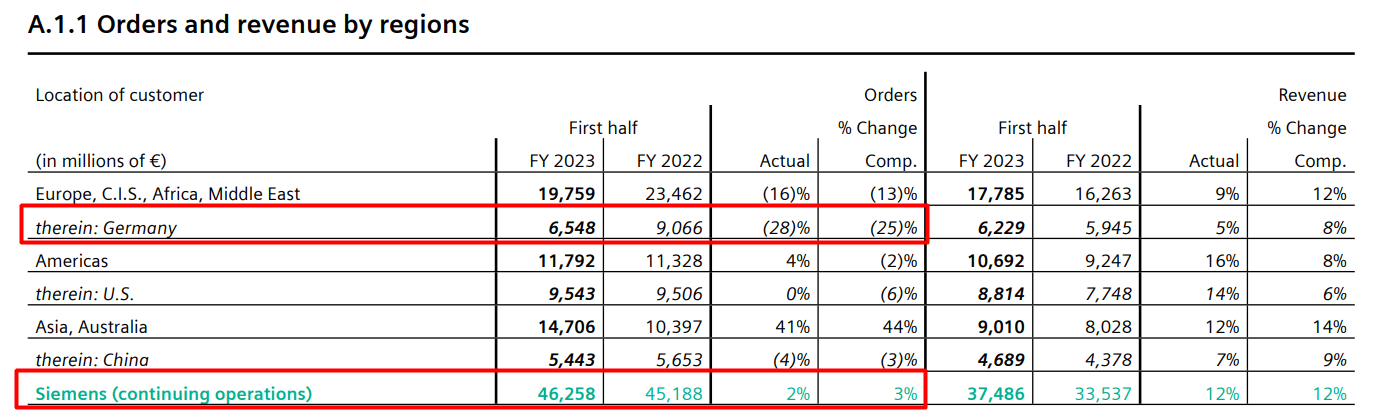

On a quarter basis , Siemens saw a 15% YoY increase in revenue to €19.4 billion in Q2 2023. Orders also rose by 15% YoY to €23.6 billion, driven primarily by a record order intake in the Mobility segment. The profit in the Industrial Business segment surged by 47% to €2.6 billion, with a profit margin of 14.2%. Net income nearly tripled to €3.6 billion, benefiting from a tax-free gain of €1.6 billion from the reversal of an impairment.

Digital Industries achieved a 23% YoY revenue growth, reaching €5.5 billion, with strong contributions from the automation businesses. However, orders declined by 10% to €5.3 billion, but this was expected due to high levels in the previous year. Smart Infrastructure saw a 9% increase in orders to €5.5 billion, driven by substantial growth in the electrification business. Profit at Smart Infrastructure climbed 75% to €779 million, with a profit margin of 15.9%. Mobility experienced its highest-ever quarterly order intake, and revenue rose by 33% to €2.7 billion.

Although cash and cash equivalents on the balance sheet have declined slightly, it seems to me that the Siemens business is very resilient, as both the current ratio and the quick ratio are above 1. The debt-to-equity is below 0.4 and is declining:

The generous dividends [2.71% FWD] are more than covered by the operating cash flow - and that's amid an earnings yield of 7.04%.

Based on the strong 1H FY23, Siemens raised its outlook: now the firm expects comparable revenue growth for the group to be in the range of 9% to 11%. Digital Industries is forecasted to see revenue growth of 17-20% YoY and a profit margin of 22.5-23.5%. Smart Infrastructure should have revenue growth of 14-16% and a profit margin of 14.5-15.5%. The mobility segment is anticipated to have revenue growth of 10% to 12% and a profit margin of 8% to 10%.

Siemens expects an increase in EPS pre-PPA [the accounting process of allocating the purchase price of acquisition among the acquired assets and liabilities] to a range of €9.60 to €9.90 in FY2023, driven by profitable growth in its industrial businesses. Including the reversal of the impairment on Siemens' stake in Siemens Energy AG, EPS pre-PPA is expected to be in the range of €11.61 to €11.91.

The Opportunity

You have noticed without me that AI is now everywhere, and more and more people are trying to find the coveted "1 share" that has all the characteristics to master this new trend. Siemens seems like an ideal candidate.

The first great advantage of Siemens, in my opinion, is that it has long succeeded in penetrating all the developed markets of Europe, North America, and Asia - it has enabled the firm to cushion the decline of the deteriorating macroeconomic situation in Germany in recent years.

SIEGY's financials, author's notes

{kind=link}

?SIEGY seems to be well diversified and has the scale that most other growth companies aspire to achieve right now.

The second decisive advantage is the possibility of organic growth of the markets which are already addressed by SIEGY. This is not something unique and peculiar to Siemens, no. But given the first advantage - "diversified scale" as I call it - Siemens has every chance of capturing more market share than others [especially so in Europe and Asia].

{kind=link}

The third point in SIEGY's favor among the other AI plays out there are the active attempts by management to transform the company. I will give a brief description of recent corporate events to illustrate what I mean.

Last year Siemens launched Siemens Xcelerator, a digital business platform that combines IoT-enabled hardware and software, a partner ecosystem, and a marketplace to accelerate digital transformation and help businesses achieve their goals. Additionally, the acquisition of Mendix [ from 2018 ] expands Siemens' presence in the low-code development market, enabling more flexible and agile software development.

Also last year , Siemens Digital Industries Software [ SIEGY's American subsidiary ] introduced Capital Electra X, a cloud-native electrical design software as a service. It offers a browser-based solution for creating electrical schematics, targeting small to medium-sized businesses. The software is based on technology from Radica Software, a company acquired by Siemens in October 2022 . It provides a convenient and cost-effective option for designers and engineers, accessible from any device.

Finally, the launch of Siemens MindSphere strengthened the firm's portfolio of open cloud-based platform solutions that enable data collection, analysis, and visualization to enhance operational efficiency and decision-making in industrial businesses.

The most amazing thing about all this is that all this news speaks of the growth prospects of SIEGY's backlog, but at the same time, it seems to have gone unnoticed by the market. Anyway, that is my impression compared to the news about "huge contracts" from the same Palantir ( PLTR ). And at the same time, the dollar amount of PLTR contracts is a drop in the bucket compared to SIEGY [this is not a direct comparison on my part, I just got myself thinking].

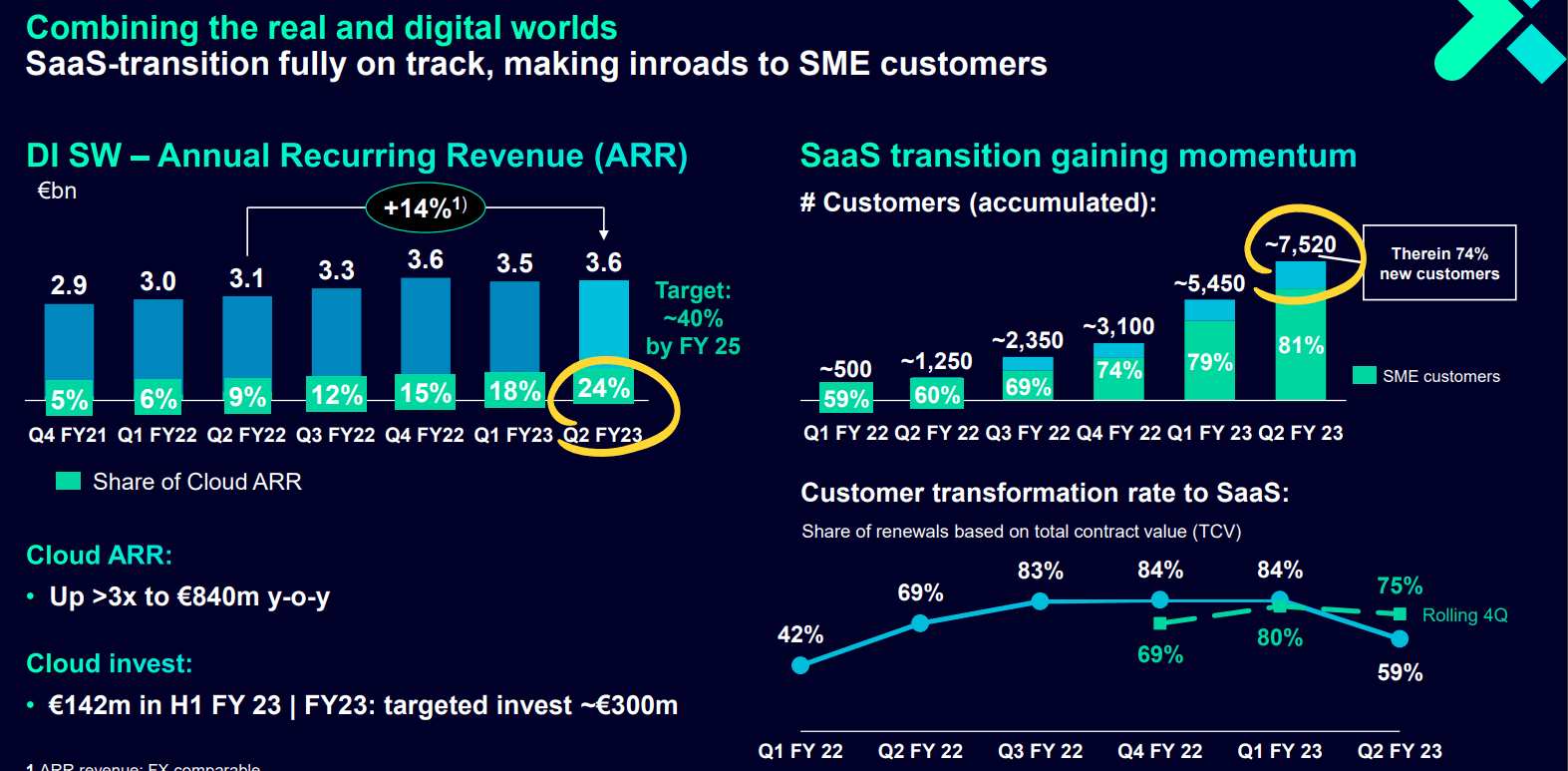

Based on all these and other projects, management plans to move to a SaaS-like revenue model and try to rely more and more on annually recurring revenues [target = 40% of total sales by FY2025], which are more predictable and make it easier to achieve high margins:

{kind=link}

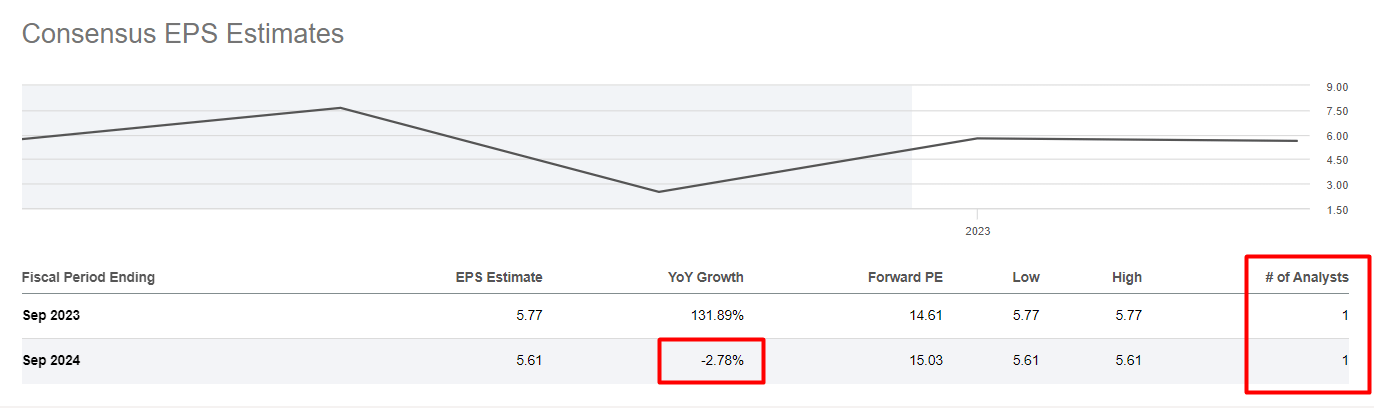

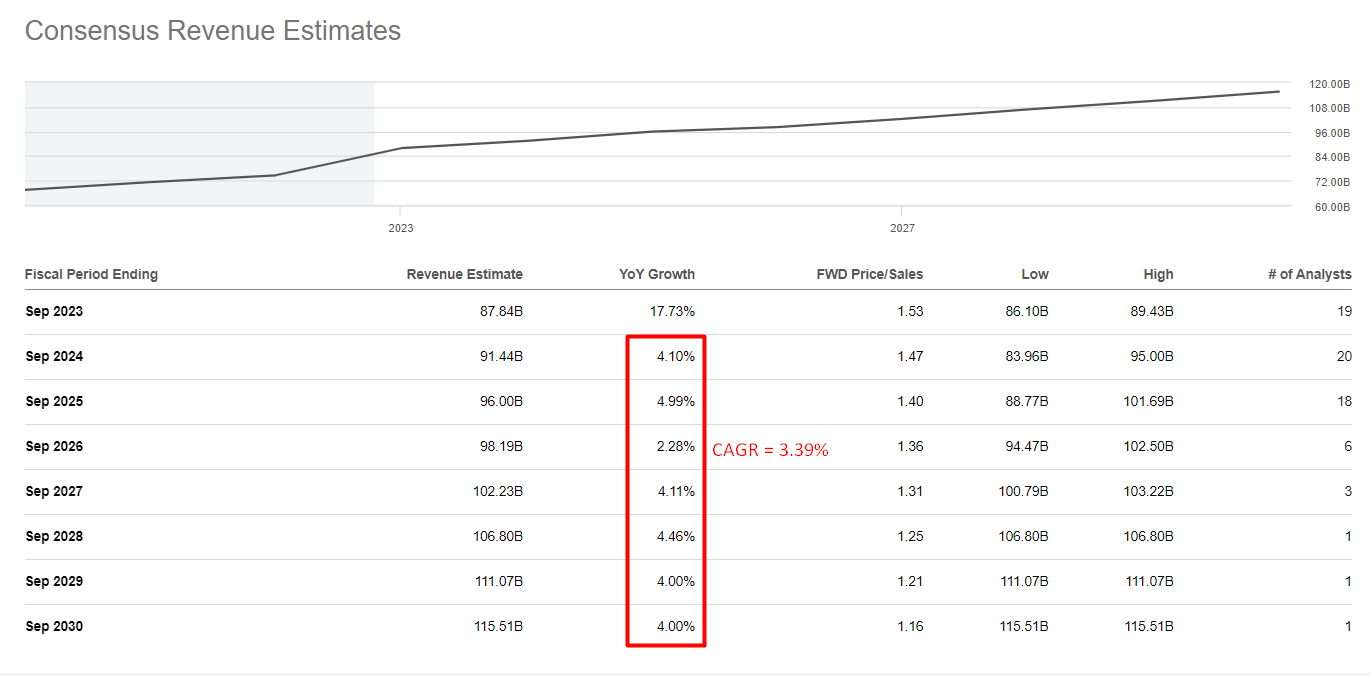

The fourth point follows directly from the third - given the recent launches and partnerships, the potential growth of TAM and thus sales volume appears to be understated due to the company's low visibility in the general market. Thanks to Seeking Alpha Premium's data one can see the sales and EPS consensus estimates. Just think about it - the EPS consensus for a multi-billion dollar global company is based on the opinion of only 1 analyst (isn't this a clear sign of a hidden gem?).

Seeking Alpha Premium, SIEGY, author's notes Seeking Alpha Premium, SIEGY, author's notes

{kind=link}

{kind=link}

The way I see it, the market interprets the company's success in FY23 as a one-off effect followed by an inevitable plateau. I very much doubt this pessimism, because the application of AI in the real world is just getting started. Companies like Siemens, which have made some important mergers and acquisitions in recent years, should have a head start on other players in the industry.

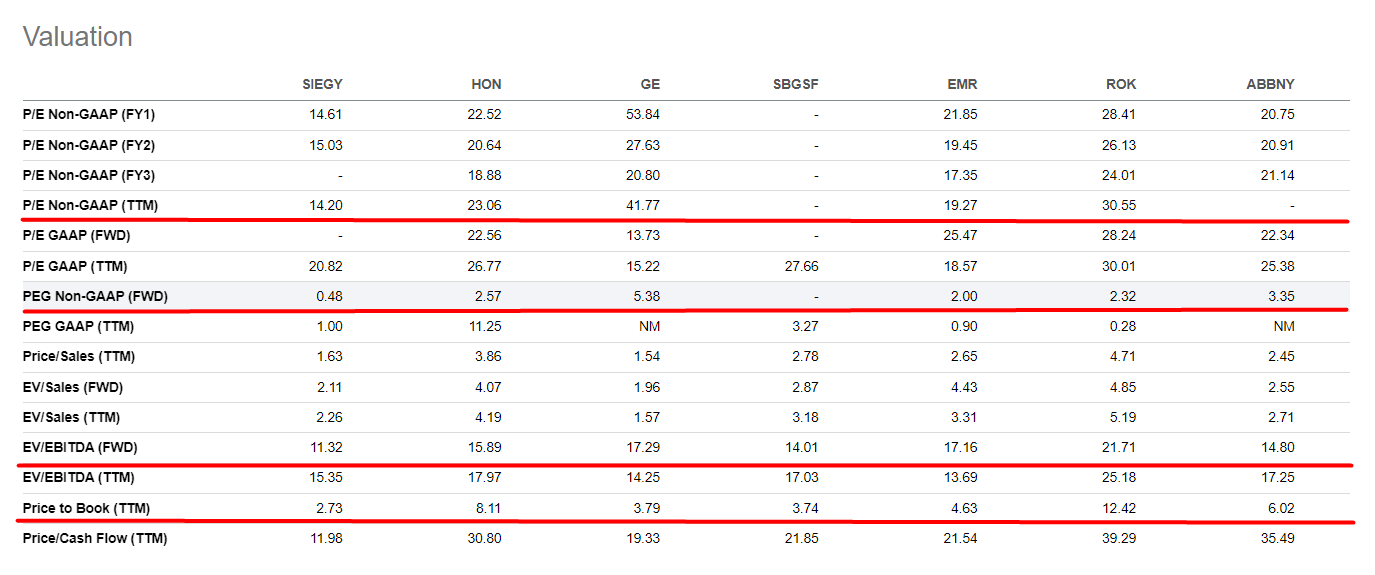

The fifth point why I believe that SIEGY is a top AI pick today is its relative undervaluation. The company has a lot of competitors/peers, and if we focus only on those with similar market caps and business cycle maturities, then among the large caps we should have General Electric Company ( GE ), ABB Ltd ( ABBNY ), Schneider Electric SE ( SBGSF ), Honeywell International Inc. ( HON ), Emerson Electric Co. ( EMR ), and Rockwell Automation, Inc. ( ROK ). Guess which company in this group is the most favorable in terms of P/E, next-year PEG, EV/EBITDA, and even P/B ratios.

Seeking Alpha Premium, author's notes

{kind=link}

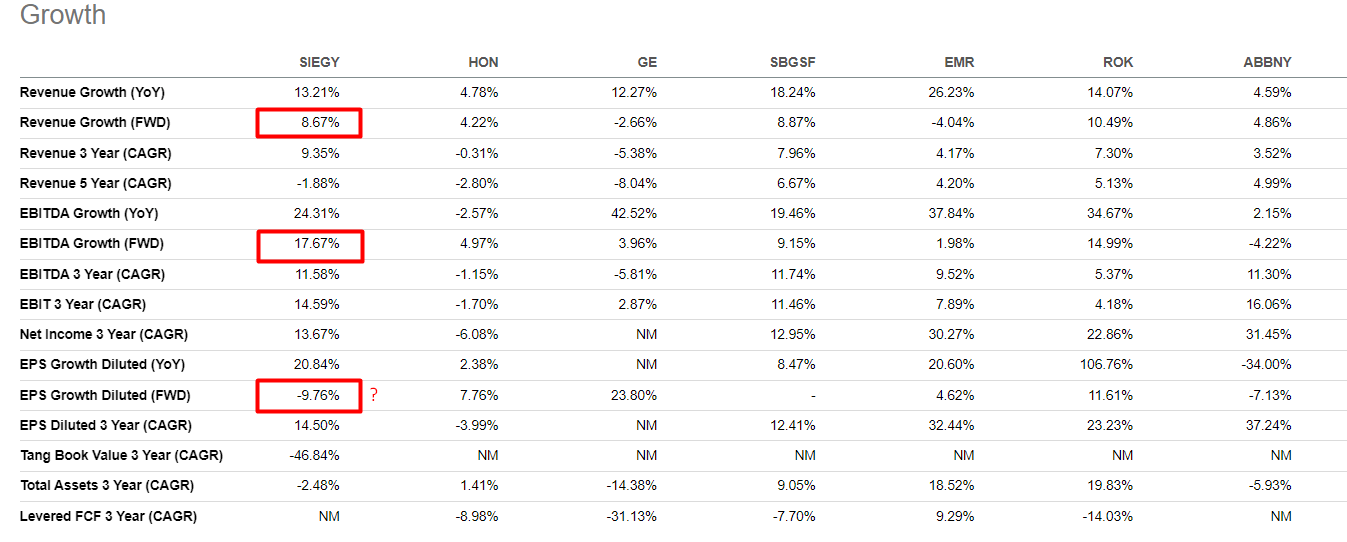

And what is most interesting - SIEGY's growth rates look much better than the other competitors. And the FWD EPS growth rate of negative 9.76% YoY against a backdrop of EBITDA growth of positive 17.67% YoY seems to be further confirmation of how much room SIEGY has to beat earnings estimates:

Seeking Alpha Premium, author's notes

{kind=link}

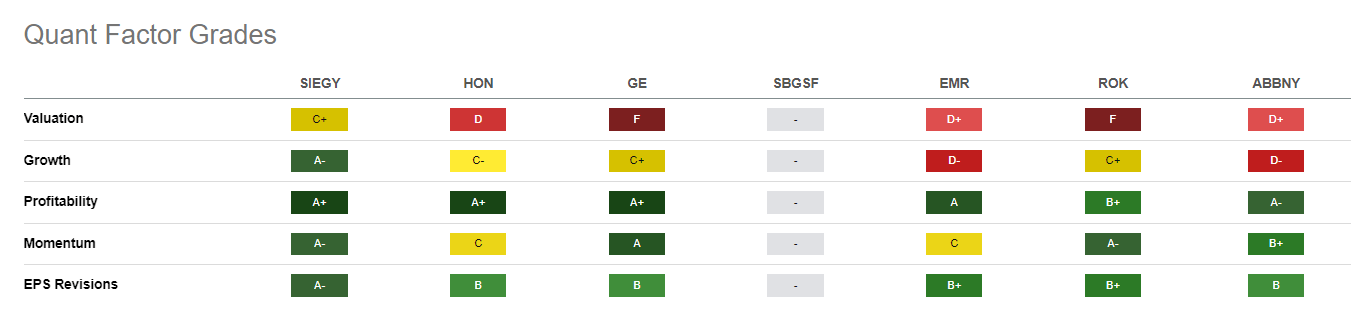

Seeking Alpha's Quant Grades for SIEGY look much better than the other scores - one more reason to think:

{kind=link}

Speaking of the historical backdrop for the valuation of SIEGY stock, despite the impressive rally last year [+74%], SIEGY is currently trading at only 14.6 times expected earnings, at the lower limit of the maximum historical range shown by YCharts. The stock definitely still has room to grow:

SIEGY Is Also Intrinsically Undervalued

In addition to SIEGY's undervaluation relative to its peers and historical norms, it is important for us to understand how the company is able to generate FCF for future distributions in the form of dividends, buybacks, or new projects.

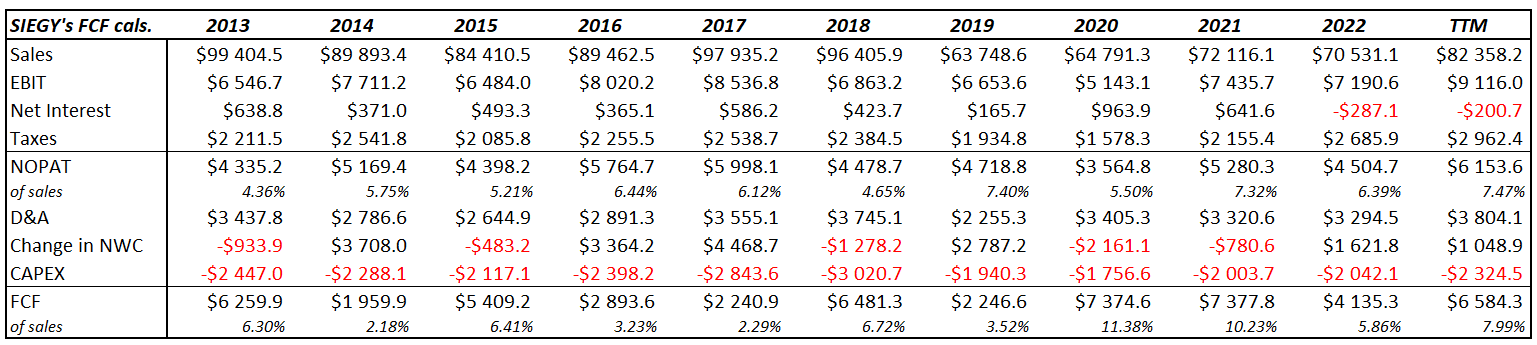

Looking at the company from a historical perspective and deriving its FCFs from NOPAT numbers, we see that regardless of the cycle in its industry, SIEGY has always generated positive FCF ranging from 3.23% [FY2016] to 11.38% [FY2020] to sales:

{kind=link}

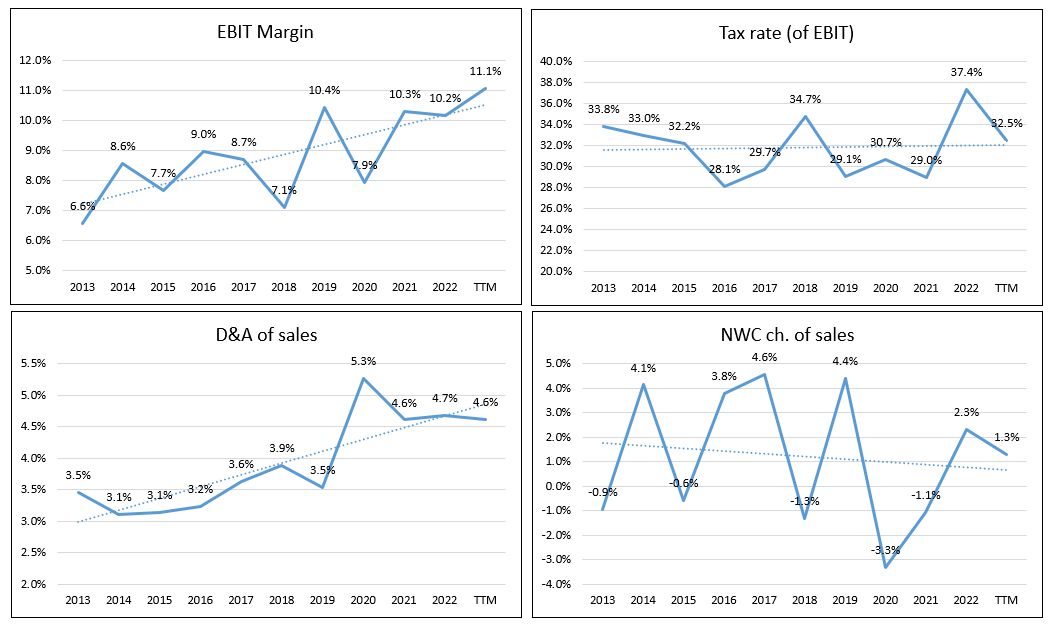

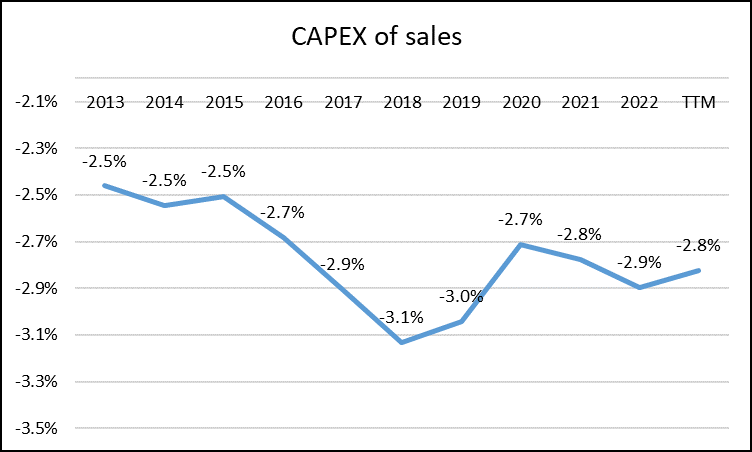

Some of these key metrics are cyclical (changes in net working capital), and others are trending (CAPEX, margins), so one needs to look at the dynamics of the last few years to assess what is happening inside FCFs.

{kind=link}

{kind=link}

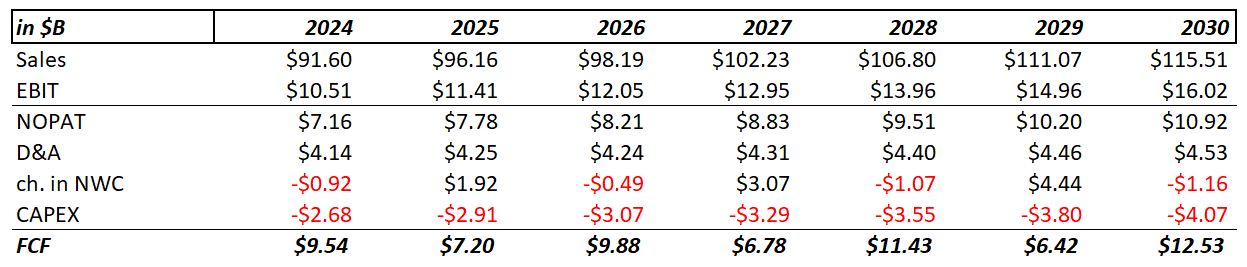

Assuming the stability of SIEGY business processes - this core assumption without which DCF modeling cannot do - I also assume the following inputs:

a) revenues will grow in line with consensus, which seems quite conservative to me (this is an advantage for our model)

b) EBIT margin will gradually improve due to the transition to a SaaS-like ARR-driven revenue model

c) CAPEX as a percentage of revenue will continue to gradually decrease as SIEGY continues to invest in new technologies and projects trying to protect its market share against the backdrop of the growth of a large number of smaller competitors

d) D&A as a percentage of revenue will gradually decline as revenue increases (I do not want to inflate D&A so as not to artificially increase FCFs)

e) NWC changes will follow their usual cycle: Decline to -1% in FY2024, then increase to +2% in FY2025, etc

f) the effective tax rate is expected to remain stable at 31.8%

{kind=link}

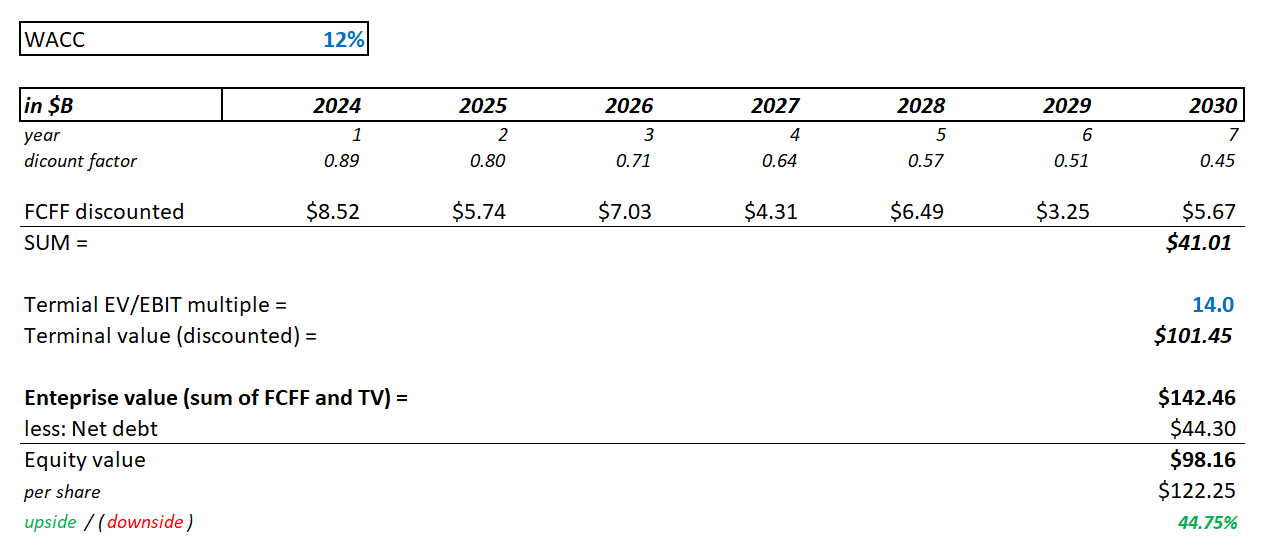

Here is what I get from these metrics in absolute terms:

{kind=link}

In trying to determine a discount rate for SIEGY, I went to Google and found a range of 5.8-10.8% based on information on various finance-related websites. I will go further in my conservatism and assume a WACC of 11%. Let us not forget that this is a large conglomerate, some of whose businesses are cyclical in nature, so I want to play it safe in my assumptions.

As a basis for calculating the terminal value, I will focus on the EV / EBIT ratio, because, unlike some other conglomerates, SIEGY's operating profit has been consistently positive in recent years. I use 14x as the exit multiple, which is roughly in line with the long-term average.

So, here's what I got as an output of my model:

{kind=link}

As you see, the intrinsic valuation suggests an even bigger upside potential for SIEGY stock.

Risk Factors

Even though I am quite optimistic about the future of Siemens Aktiengesellschaft, some risk factors are well worth mentioning.

First , SIEGY is an ADR that trades on the over-the-counter market ((OTC)) in the United States. ADRs typically have less liquidity than stocks listed on major U.S. exchanges. This can result in wider bid-ask spreads and potentially lower trading volumes, which can make it more difficult to buy or sell SIEGY at desired prices. In addition, ADRs carry currency risks. As long as the dollar ( DXY ) is weak, this is an advantage for SIEGY, but when it strengthens again, this may slow the stock's rally.

Second , one cannot but mention the fierceness of competition in the market where SIEGY operates. As you can see from the companies I have listed as direct competitors, SIEGY has to fight desperately every year for a place under the sun, and as attention to the AI trend increases, it's becoming increasingly difficult to do so.

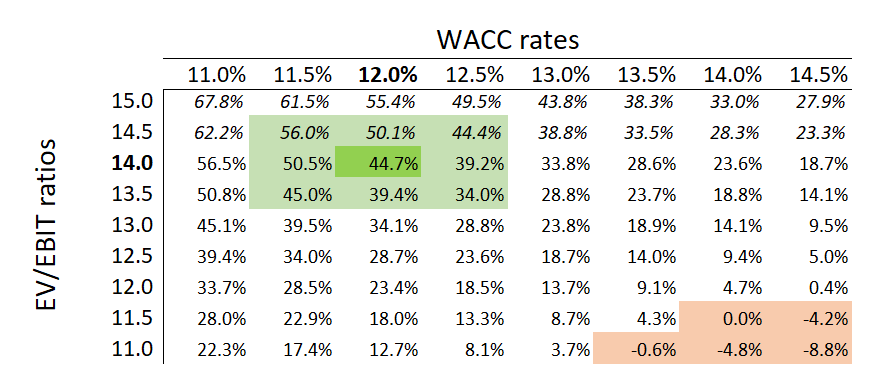

Third, my conclusion that SIEGY's valuation is fair and that there is a significant discount to its valuation is based on a number of important assumptions that must occur in the next few years. They will be wrong anyway - a DCF cannot correctly predict the future. The extent to which the fact deviates from my forecast will strongly influence today's fair price, as the following sensitivity analysis shows:

{kind=link}

Fourth , I would not be surprised if SIEGY stock cools down again at some point after the overwhelming recovery rally of the last few months - the current entry points for this stock seem quite high from a technical analysis perspective.

The Bottom Line

In my opinion, SIEGY stock is ignored by AI chasers because the company has struggled in recent years: sales volumes have been relatively volatile and there has been no obvious reason for improvement; EBIT has been declining since peaking in FY 2017.

An old memory and relatively low investor awareness - that's the reason for the discount on the company's valuation. However, things are now starting to change. SIEGY has not only fully recovered from a difficult FY2022, but it has also set a multi-year EBIT record and is in the active phase of transformation with a focus on a SaaS-like revenue model that should eventually lead to a valuation premium, not a discount, over its peers. If this assumption is correct, SIEGY is now the most undervalued industrial conglomerate in the world with a market capitalization of over $100 billion. And as a large cap, it's way more stable than small and mid-cap peers.

Based on relative valuation, I see a fair price at ~$118/ADR at a P/E of 21x and a consensus FY2024 EPS of $5.61 per ADR. With this assumption, which I believe is quite conservative, SIEGY has an upside potential of 28.4% - and that's excluding the dividend yield of over 2.7%.

Speaking of SIEGY's intrinsic valuation: a number of conservative assumptions have led me to conclude that SIEGY is undervalued by 44.75% in the base case. The prospects of EBIT margin expansion due to the continuation of business transitioning are not yet priced-in, in my view, which gives significant headroom for future high-quality growth.

Based on the comparative and fundamental valuations, I conclude that SIEGY is undervalued by 36.6% today.

I rate the SIEGY share as a Buy this time around.

Thank you for reading!

Editor's Note: This article was submitted as part of Seeking Alpha's Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Siemens: The Best AI Play Everyone Ignores