SIEGY - Siemens: Very Well-Positioned For The Future But Too Expensive Here

Summary

- Siemens is one of my main industrial holdings, and has been for several years. It's a great company with a substantial upside in several fields and global sectors.

- Since my last article, Siemens has once again outperformed substantially, returning over 30% RoR in a market that's returned 2.5% even with the last few days.

- Siemens remains a must-own, as I see it - and my allocation target is currently almost filled.

Dear readers/followers,

Siemens ( SIEGY ) is one of those companies that I believe that a conservative and long-term investor really "must" own, or should be owning. There is simply too much to like about Siemens. Enough to more or less ignore the momentary dips in share price and a valuation that are endemic to any company with operations of this size.

As I see it, Siemens is like GE ( GE ) - only GE failed to transform its myriad of businesses and former conglomerate sectors, while Siemens, by all accounts, succeeded. That is also why the company has outperformed in the short term and delivered results such as these.

Siemens Article (Seeking Alpha)

Of course, with a 30% climb comes the question if the company is even still in any conservative perspective investable.

Well, here is my view on that.

Revisiting Siemens and its upside

Siemens remains the industrial legacy I've often spoken about, even if it no longer holds everything "directly" in its portfolio. Even if you work for one of the now spun-off companies, you usually say (in Germany), that you work at "Siemens". This is because the company is one of those, like GE, Dow, and others, that "built" entire areas. I was in villages where the entire population, one way or another, worked at a variety of Siemens plants, or offices. In some ways, it's like a company that "is" an entire region or that at least owns the employment (or 90% of it) in an entire area.

Siemens remains my oldest German investment - ever - and one that I'm up triple digits including all the dividends and the RoR I've seen over the years. The company has not yet reached a price where I would view it as rotatable.

It's the largest industrial manufacturing business in all of Europe, with 300,000+ employees across the globe. More importantly, it's very well positioned for the future that's happening in the world at this particular time.

The net result of Siemens spin-offs and portfolio focus is a very positive one. We've lowered our direct risk while increasing or maintaining diversification in the investment. From a large conglomerate with a multitude of segments, Siemens decided to start spinning off its various businesses into their own publicly-listed companies, usually while maintaining some type of stake in them. As I said - it's what GE failed to do, but Siemens succeeded, under the "Kaiser" (Joe Kaeser).

If we want to simply describe what Siemens is, Siemens is a collection of EU-heavy businesses with segments in industrials, communication, health, energy, and infrastructure.

I described in my last article how recent results were all positive for the company, with a book-to-bill ratio above 1.2x, an over €100B backlog that's for the most part contractually protected from inflation and trends, and superb segment trends.

Siemens is one of the best-rated industrials on the planet - so any sort of fundamental concern here in terms of safety is quite unlikely for the time being - and for 2023.

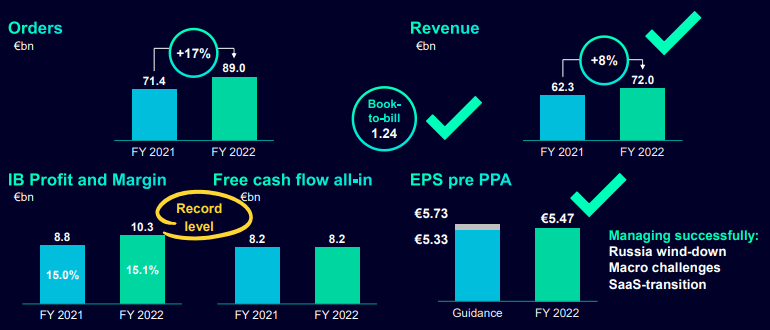

Siemens has already finished its fiscal 2022 - back in November. Results for 4Q22 were absolutely stellar. Siemens delivered on its annual guidance, and operational performance was superb, with double-digit growth in terms of orders, and close to double-digit revenue growth, breaching the €70B mark.

{kind=link}

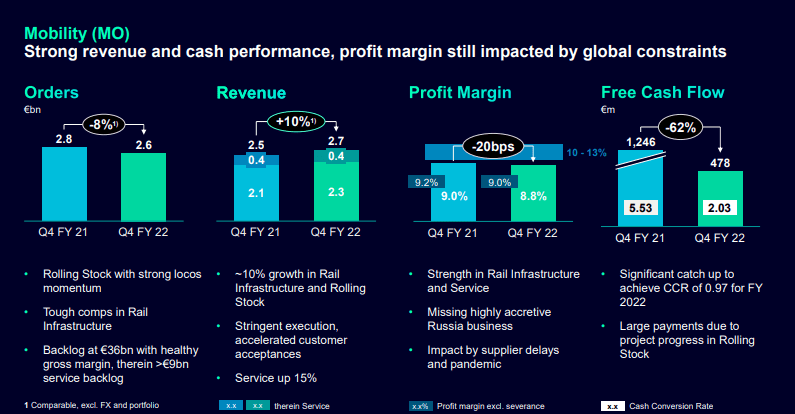

The company's operational segments at this time are DI, SI and MO - and all of these delivered revenue growth and margins according to expectations, with DI at the highest margin close to 20% and MO at around 8.2%, within its target range.

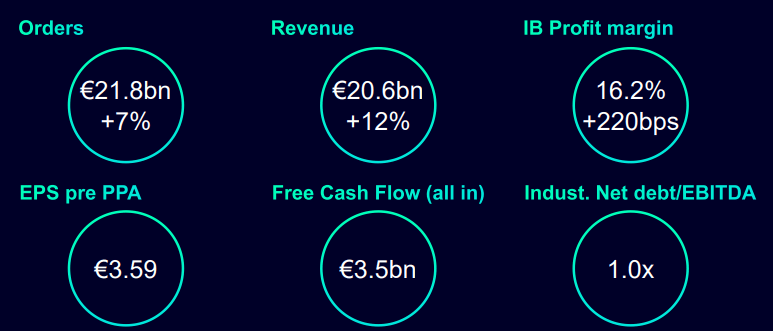

This gives Siemens a superb starting position for 2023. The backlog is up to €102B, and Siemens price improvements are gaining traction in the bottom line. FCF is up to €3.5B for the quarter, with the company's various segments seeing significant improvements over a short time.

The company also retired all, 100%, of its Russia-related risks. Its Finance and leasing are divested, and everything in Russia is wound down in terms of P&L effects.

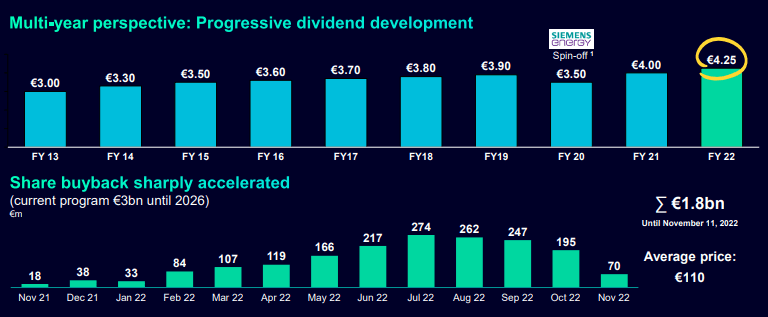

The company boosted the dividend to €4.25, which puts my own YoC at insane levels, and the current yield at the time of writing this article at 3.14%. Low, you might say - but consider what Siemens is before you say that. Because it's not.

{kind=link}

Those metrics spell out to me why you should consider investing heavily in this business. Take a look at the backlog specifics, and the revenue the company is expected to generate from it.

{kind=link}

This showcases the company's fundamental strength. The concept of "streamlining" a conglomerate is one that Siemens, therefore, over the past decade, has perfected. The main differentiator between Siemens and its closest peer GE is that GE is keeping its legacy turbine and other industrial activities while leaving behind the software. Siemens is doing the exact opposite of this, and this is what has driven some of the success here.

This isn't just Siemens doing it this way either - another similar conglomerate I own, Schneider (SBGSY) out of France is doing it the same way, as is ABB (ABB). It's a good example of a "European" model being by far the more effective, turning to tech focus and asset-lighter structures for more flexibility and slowly proving their profitability here.

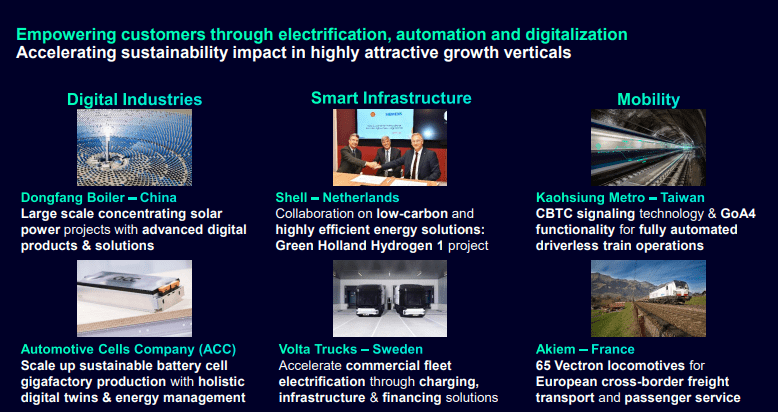

Some concrete examples are possible - including what the company is doing in Egypt, where a modern, sustainable rail system is being developed, or how its divestments and carve-outs are being even further focused on, with the current focus now on LDA. The company is growing across the board with its electrification plans and sustainability targets.

{kind=link}

The company's digital business segment, DI, is a prime example of this. It's expected to grow at 10% CAGR until 2025E, scaling its solutions across businesses, and its SaaS transition is fully on track. Most of the company's SME customers are now switched, and a total of 3,100 customers have gone over to SaaS. Renewals share based on contract value is up from 42% SaaS in 1Q22 to 84% in 4Q22. This marks some of the fastest SaaS turnarounds I have ever seen in any company at any point in time.

My favorite segment that Siemens has though isn't DI - it's MO. I love the mobility and infrastructure pushes based on their massive contract value and their value to their respective customers, usually nations and massive organizations. Yes, margins here are less than half of DI, and yes, these margins are still being constrained. But once things open up here, this segment is going to be a profit driver akin to a locomotive chugging along/forward.

{kind=link}

Company fundamentals, meanwhile, remain absolutely stellar and in no way an argument not to invest in Siemens. The company as some incredible capital efficiency in the form of an improved ROCE now at 24.6%, up from 15.2% in FY21. The company's industrial net debt is now at 1.0x, providing ample room for M&A'ing, if the company feels the need to do this going forward.

And the company's capital returns to shareholders in the form of buybacks and dividends have been stellar, and are rising as well.

{kind=link}

All of this means that Siemens is a truly excellent company that you want to invest in - as I see it - but only at the right price.

So how is that looking today?

Siemens Valuation

Unfortunately my pounding of the table for Siemens did not garner the interest I hoped for. I can only hope that my pointing out this company's upsides and qualities will turn investors onto it so that next time Siemens does take a dive, more people take the opportunity and load up on quality.

Siemens's valuation remains complex in the sense that all of its various portfolio companies and assets need to be properly accounted for in every single model, and my updates in these models are typically a process of a few hours every time the numbers come out.

I went to 3% in my DCF model in terms of EBITDA growth during my last article, and despite these positives, I'm not raising that. It's important not to underestimate the company's potential due to the correlation to infrastructure spending, but it's equally important to not believe the company is immune to downturns - because it isn't.

Typically, we can expect Siemens to yield no higher than a 2-3% yield - the fact that we're now at 3.1% is acceptable but in no way amazing.

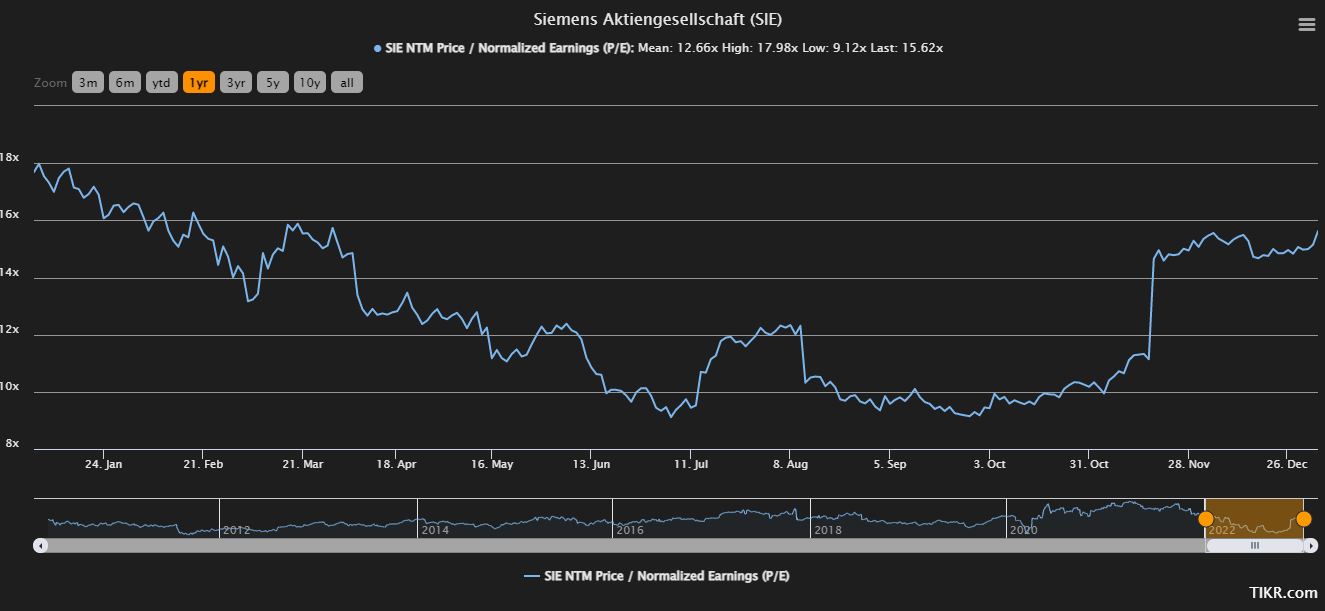

From a peer basis, peers do exist, but none of them really come close to holding a candle to Siemens itself - with maybe 1-2 exceptions. Schneider Electric is one, and ABB is another. Others, like Atlas Copco ( OTCPK:ATLKY ) exist as well, but they're too small to really compare. There's Alstom ( OTCPK:AOMFF ) ( OTCPK:ALSMY ), but where Siemens is safe, Alstom has more volatility, as I see it. Siemens not that long ago traded at a normalized P/E of 10x, in a comp group that comes close to 20x. That is no longer the case here.

The current normalized P/E is around 15x, which is above its native mean of 12-14x. It's reached as high as 22x, and as low as 8x. Last I bought was during 3Q22 when we were staring that 9-10x in the face. That was attractive.

This price? Not so much. I mean, there's still some upside, but at €130+ native, that's when we need to start being careful with this company and its valuation.

{kind=link}

S&P Global calls for a 21-analyst range of €94 on the low side to €190 on the high side, a fairly extreme range. However, 17 out of these analysts have a "Buy" or similar rating at this time. The average PT for Siemens is €152/share here, implying an analyst upside of around 12.8%.

I go more conservatively than this, which should be of little surprise to you if you follow my work. In my last article, I went for a share price of €135. You should also know that my share price targets are set with - if I do say so myself - stringent and meticulous calculations, combining NAV, DCF, Historicals, forecasts, and analyst targets based on real company cash flows and potentials. I don't shift them lightly because the "mood changes".

I won't do so here.

It was, and is €135. I don't see external factors in the past 4 months that cause me to change this target. The company's outperformance was something I was calculating into my model - or at least the potential for it.

This means, as of today and the share price of €135.44 I'm seeing on at the market, I am shifting my stance from "Buy" to "Hold".

Here is my updated thesis for Siemens for this year.

Thesis

My thesis for Siemens is as follows:

- Siemens is a beyond-solid company. It's so far beyond solid that it's one of the 20 companies in my "Buy-and-hold-forever" list, along with businesses like BlackRock ( BLK ), Airbus ( OTCPK:EADSY ), and LVMH ( OTCPK:LVMUY ).

- If you did not buy Siemens when it was below 10x P/E a few months back, you really missed the boat on this business, and missed out on 30% RoR in a short time.

- At the right price, this company becomes a "BUY" strong enough to make me ignore or put second most other investments. I've been pushing capital to work for months now, and my stake is now 3.5%.

- My PT for Siemens is €135 - and it's a "Hold" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Siemens's valuation thesis has changed. It's now a "Hold" going into 2023, though close to fair value.

For further details see:

Siemens: Very Well-Positioned For The Future, But Too Expensive Here