SKE - Skeena Resources: Valuation Improving After The Drop

2023-10-11 17:13:22 ET

Summary

- Skeena Resources has experienced a significant drop in its stock price, down ~68% from its highs, but its fundamentals remain strong.

- Meanwhile, its Snip Project has seen a massive upgrade in its resource base and depending on mining rates and if included as a satellite, it could add 80,000 ounces/year.

- In this update, we'll look at the stock's valuation after the drop, recent developments, and whether the stock has drifted into a low-risk buy zone after two years of underperformance.

It's been a rough two-year stretch for the junior gold sector, and even more advanced-stage developers haven't been spared. This is evidenced by several names being down over 65% from their highs, Skeena Resources ( SKE ) is no exception, down ~68% from its highs, giving up a considerable portion of its gains off the 2020 market low. On a positive note, little has changed from a fundamental standpoint, and things have arguably improved, with a larger resource that's 100% owned by Skeena at Snip, a project that's more de-risked, and a hint of further upside at depth from the NEX Zone with drill-hole 1081 hitting ~4.6 grams per tonne gold-equivalent over 32.2 meters. In this update, we'll look at recent developments below and dig into the valuation to see whether the stock has dropped into a low-risk buy zone yet.

Eskay Creek Project - Company Website

{kind=link}

All figures are in United States Dollars unless otherwise noted. GEOs = gold-equivalent ounces.

Snip Resource & Recent Developments

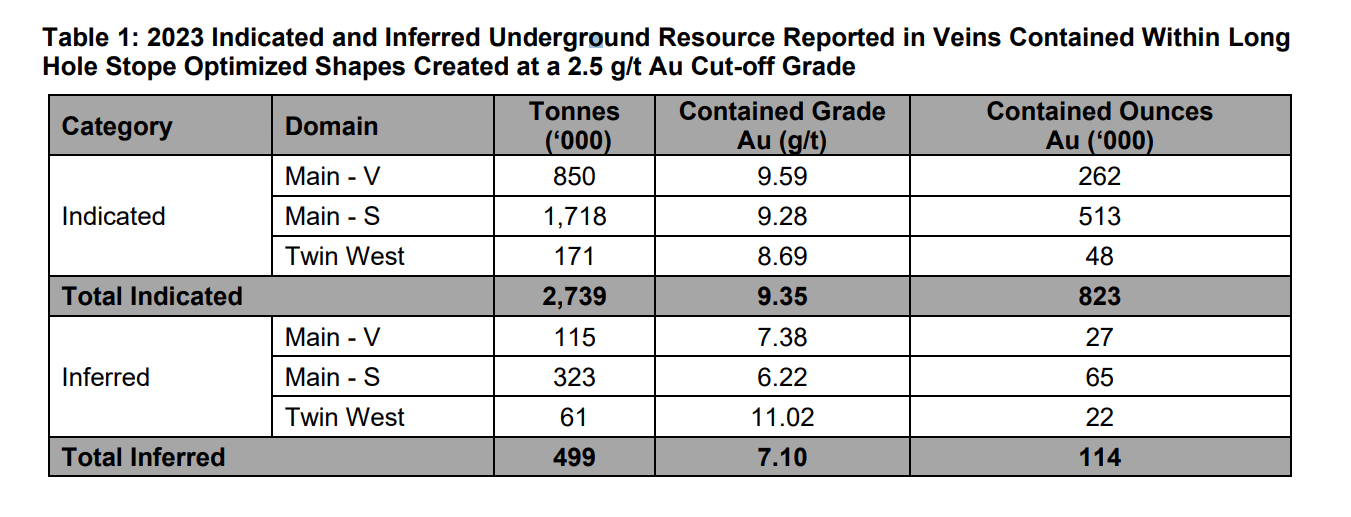

Just last month, Skeena released an update resource estimate for its Snip Project, which lies ~50 kilometers west of its flagship Eskay Creek Project, with a significant upgrade in the resource base. In fact, Snip's indicated ounces increased by 237% to ~823,000 ounces of gold (~2.7 million tonnes at 9.35 grams per tonne of gold) at a conservative gold price of $1,700/oz, and the company noted that the drilling completed by Skeena and Hochschild ( HCHDF ) has increased the confidence of historical drilling data and confidence regarding the continuity of the ore body. This is a very positive development for the company because while its other potential high-grade feed source (Albino Lake) remains under dispute, a ~2.7 million tonne resource or ~2.0 million tonne reserve base could beef up an already impressive production profile (~350,000 GEOs per annum), with the potential for 6+ years assuming a 1,000 tonne per day production rate.

Snip Resource Base - Company Website

{kind=link}

While it's too early to model Snip and a better idea of its true potential combined with Eskay Creek will be available by mid-2024 with a detailed engineering study set to be completed, there looks to be the potential to add an extra ~80,000 ounces per annum to the production profile assuming a ~1,000 tonne per day mining rate, with ore hauled to Eskay Creek. And when combined with better payabilities, because of this being cleaner ore than Eskay Creek (less deleterious elements) and combined with a simplified flow sheet and metallurgical optimization planned to improve Eskay Creek's recoveries in the H2-2023 updated Feasibility Study (plus slightly higher grades mined at Eskay). This leads me to believe we could see average annual production increase to 400,000+ GEOs per annum from Year 1 to Year 10, assuming Snip contributes from Year 3 through 9 (seven years). Meanwhile, first-five year production could improve to ~490,000 GEOs (including two full years of production from Snip).

While this is obviously a significant improvement from an NPV standpoint at a relatively modest cost, I was already modeling at least seven years of production from Snip at 1,000 tonnes per day, so this hasn't done much to change my fair value estimate. That said, it is positive to see that optimization work could lift overall grades with a decision to mine Eskay Creek more selectively according to the company. And while Eskay Creek will likely still have a sub-15 year mine life (depending on mining rate chosen at Snip for satellite feed), this is certainly an asset with room to extend the mine life further given the high hit rates when it comes to exploration drilling near current pits. Hence, while the discovery of further low to mid-grade ounces will be less meaningful as they'll get added onto the back of the mine life, there is room for further growth in NPV at Eskay Creek.

Exploration Upside

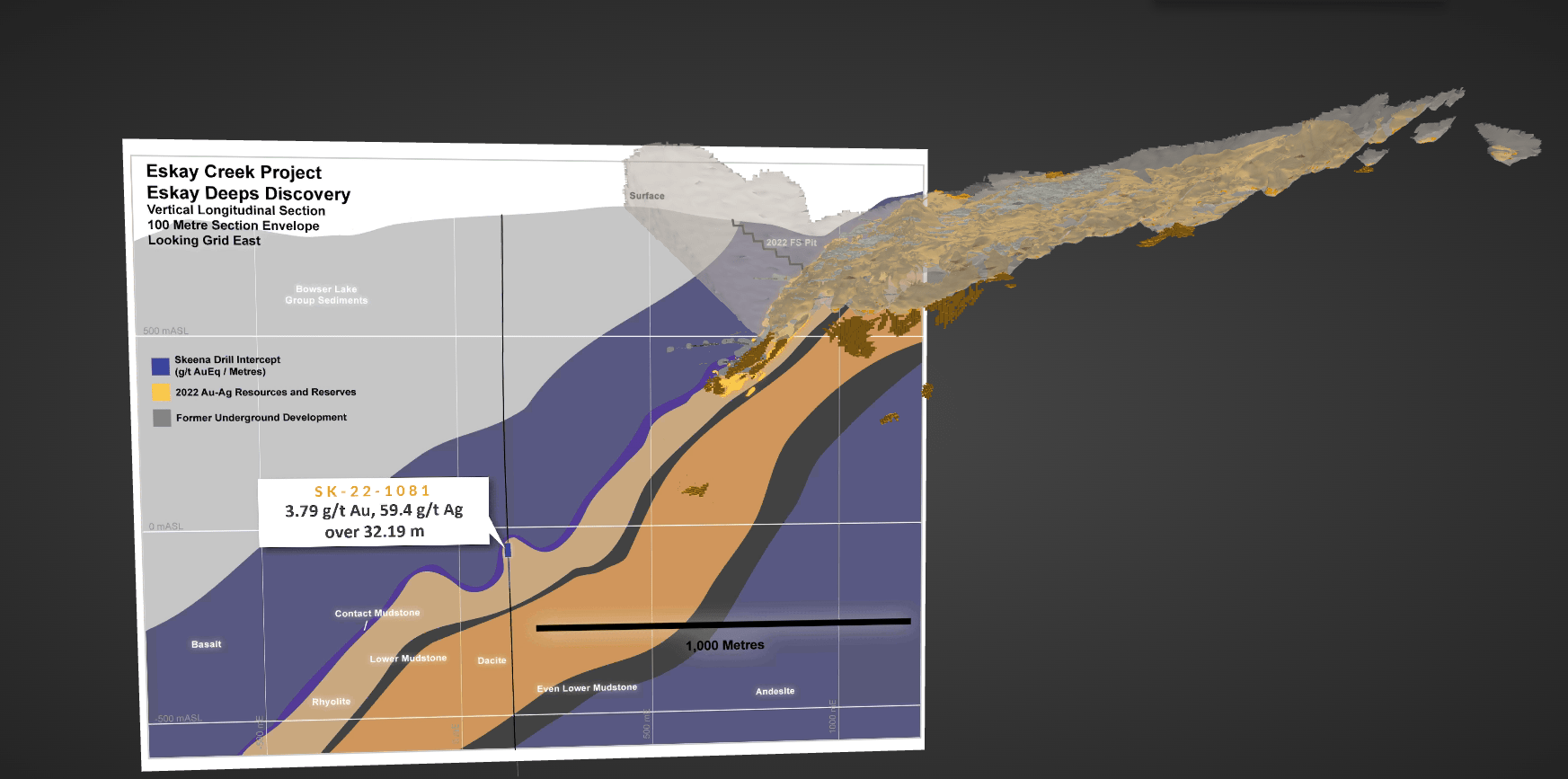

Although Eskay Creek is already one of the best undeveloped assets sector-wide, the exploration upside here is significant, especially following the release of drill-hole 1081, otherwise known as the Eskay Deeps Discovery. When this hole was drilled at this time last year, the company noted that this was an entirely new occurrence of rhyolite-hosted mineralization, and this discovery was important because it suggests that there is considerable exploration upside at depth at the northern end of its mine plan (Northern Extension Zone - NEX). And if the company were able to delineate a decent-sized high-grade resource at depth (recent hole 1081 drilled to ~850 meter vertical depth), it would certainly support a further mine life extension and what could be a future underground operation. The following takeaway related to hole 1081 is also important from President & CEO, Randy Reichert is also important:

"It was in rhyolite - it wasn't you know the main mudstone package that holds the 50, 60 gram material that we're really looking for. But what it was really showing us is that the feeder system is alive out there and just as importantly, the signature that we're seeing of the elements in that hole is very very similar to what we're seeing in the south end of the deposit, so you know, our geologists are excited - they think that we're getting close to where we could see the exhalative event, so this summer we're putting in about 15, 16 holes, really looking for that 50, 60 gram material, that extension of the Eskay Creek high-grade deposit".

- Randy Reichert, Skeena Resources President & CEO

Hole 1081 - Eskay Deeps - Company Presentation

{kind=link}

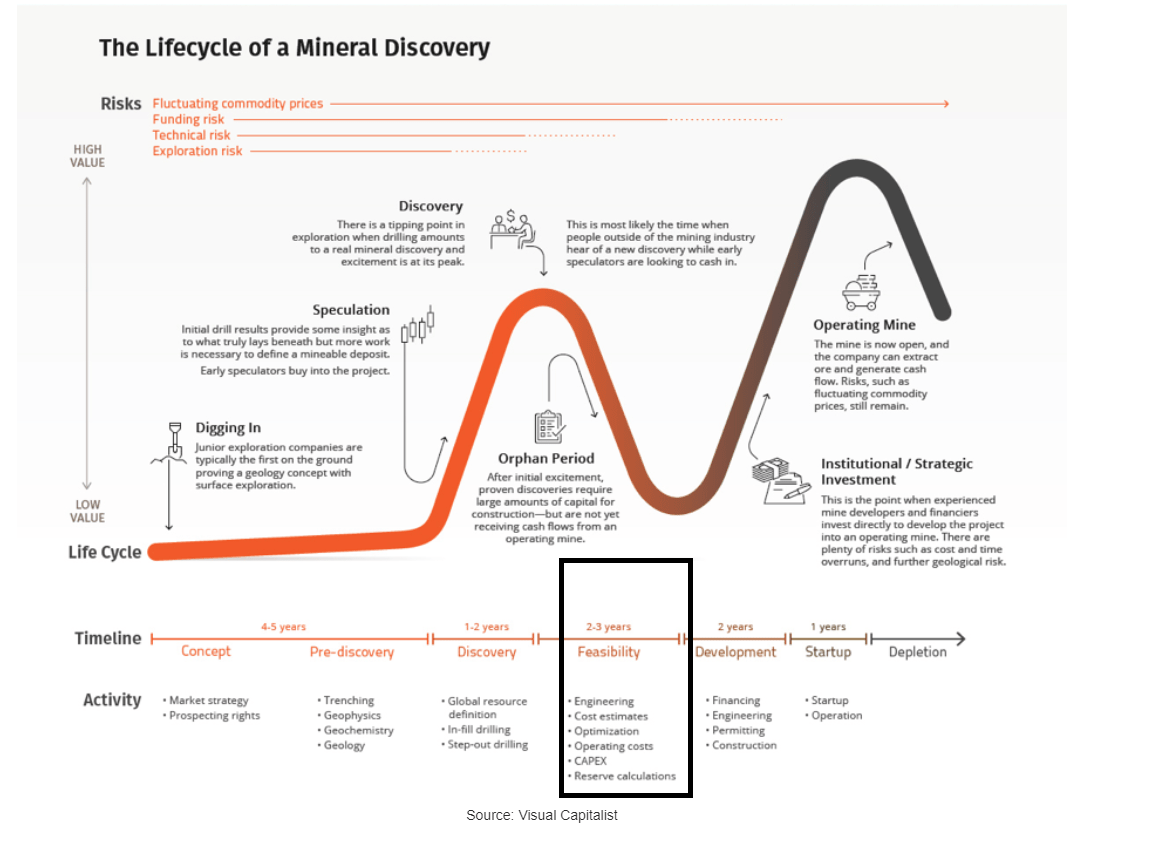

While this is quite exciting and could, in a best-case scenario, mean the potential discovery of an Eskay Creek 2.0, it's still early days to confirming this belief. And while we may get a glimpse of what's down there based on the current drill program, and the focus appears to be on optimizing the current mine plan and getting to construction, which is what it should be. So, although this is a nice kicker to the story, I would expect Skeena to trade off of what it has in resource/reserve inventory and not blue sky exploration upside at least for the time being, and for now, it's locked in the less favorable portion of the Lassonde Curve (Feasibility/Development stage), and at a time when the market is not paying up for future growth, it's possible that the stock will need time to get at least past the halfway mark of construction before it sees the typical Lassonde Curve tailwind and gets close to its first cash flow.

Lassonde Curve - Visual Capitalist, SmallCapInvestor.Ca

{kind=link}

Valuation

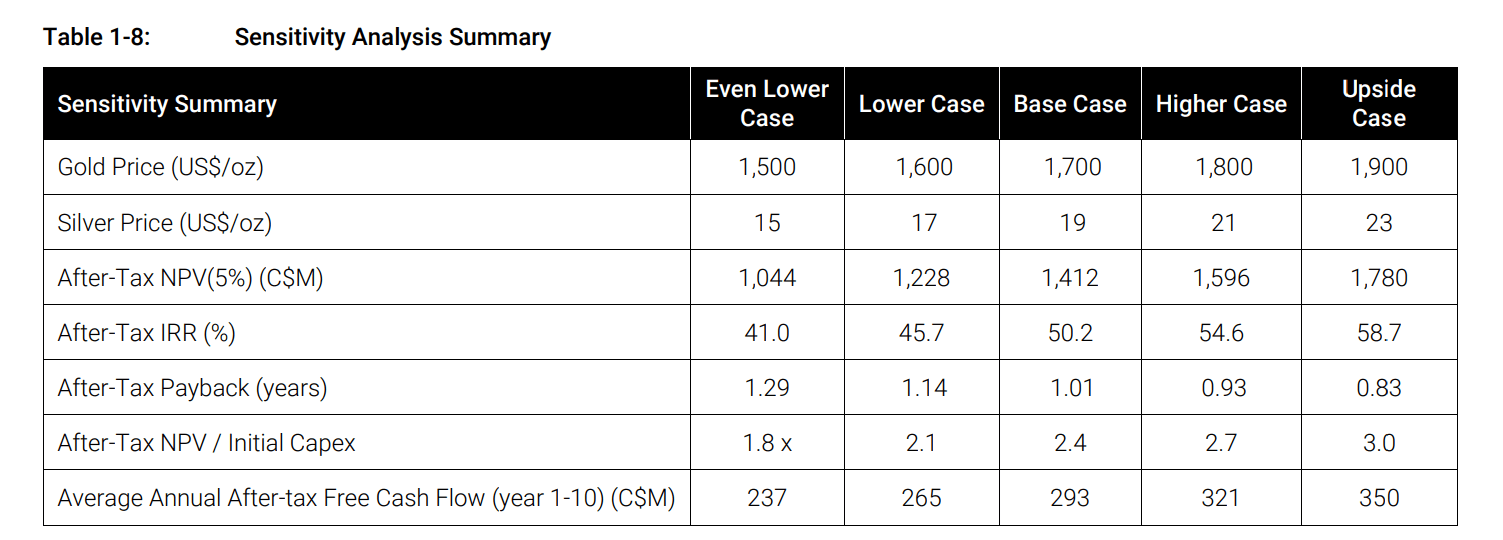

Based on ~96 million fully diluted shares and a share price of US$4.40, Skeena trades at a market cap of ~$420 million, making it one of the lowest capitalization names in junior gold sector among companies with projects capable of producing over 300,000 gold-equivalent ounces per annum. If we compare this figure to an estimated After-Tax NPV (5%) of ~$1.2 billion in the 2022 FS ($1,800/oz gold price and $21.00/oz silver price), this would appear to be a massive discount, with it trading at just 0.35x P/NPV. However, I don't see any way to justify using a 5% discount rate when the Federal Funds Rate is sitting above 4.5%, and even an 8% discount rate doesn't look conservative enough when the cost of capital for most juniors is north of 10%. And if we use a more conservative discount rate of 9.5% to adjust for Skeena not yet being fully funded, permitted, or in construction and the higher rate environment, offset by NPV gains from adding Snip and extending the mine life to 13 years, I see an estimated NPV (9.5%) of ~$815 million [US$8.50].

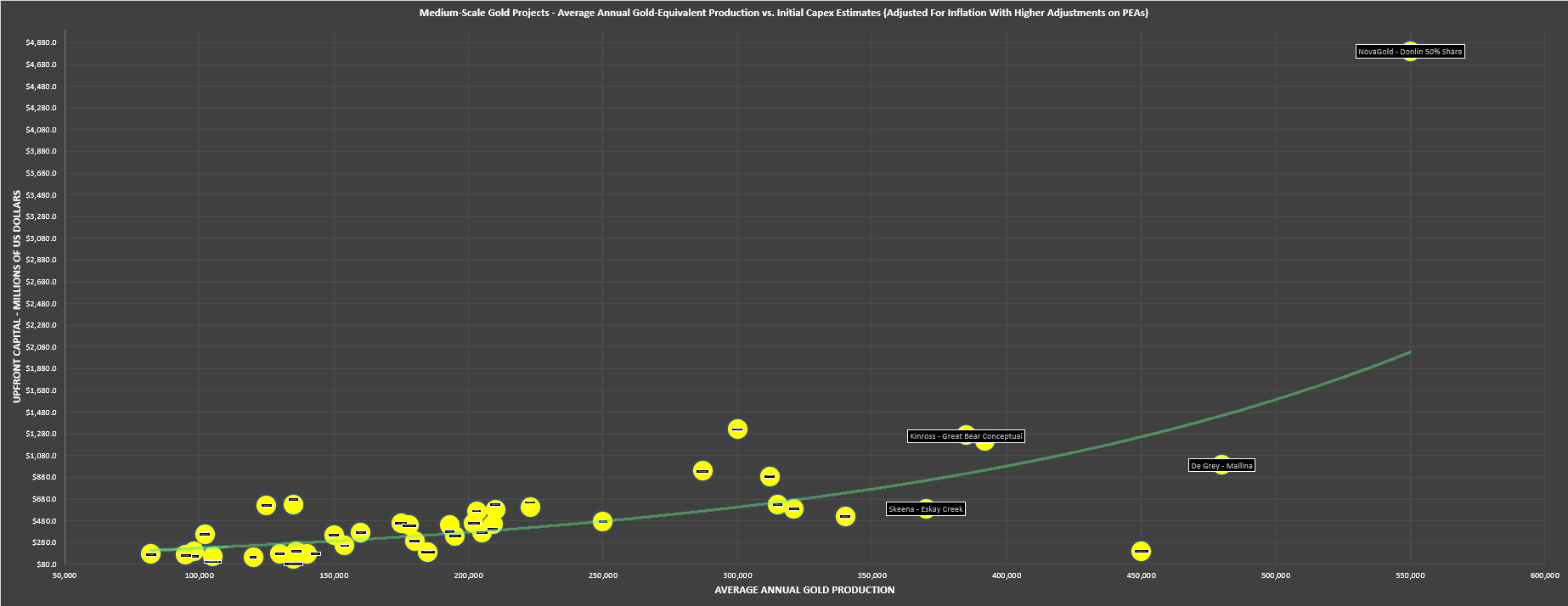

Skeena - Eskay Creek - Average Annual GEO Production & Initial Capex Estimates Adjusted for Inflation - Company Filings, Author's Chart & Estimates

{kind=link}

This estimated NPV (9.5%) incorporates more conservative estimates for mining and processing costs because of sticky inflation pressures on consumables and higher pressure on labor costs, especially in prolific mining jurisdictions, as well as a higher upfront capex bill of $490 million vs. the ~$450 million estimate in the 2022 FS.

Eskay Creek - 2022 FS Sensitivity Analysis Summary - 2022 TR

{kind=link}

If we measure from a current share price of US$4.40, a price target of US$8.50 translates to an impressive 93% upside from current levels, making Skeena one of the most undervalued Tier-1 juniors in the market today. That said, I am looking for a minimum 50% discount to fair value to justify buying gold developers given that they are quite volatile, are more prone to negative surprises, and carry much higher risk overall than producers. If we apply this discount, Skeena's updated low-risk buy zone comes in at US$4.25 or lower, with it trading just outside of this area following its current relief rally. So, while the stock has certainly seen a material improvement in its reward/risk ratio following its ~70% correction, I remain focused on what I believe to be more attractive bets elsewhere, like Marathon Gold ( MGDPF ) which trades at just ~0.25x NPV (8%) yet is over one year closer to first cash flow, with a Q1 2025 gold pour vs. my estimates of Q3 2026 for Skeena to be more conservative.

I have used an 8.0% discount rate for Marathon Gold given that it is 95% funded, already nearly halfway through construction, and nearly fully permitted (two of three pits permitted, with Berry permits pending).

Obviously, I could be wrong, and Skeena could bottom out here without providing an entry into the stock closer to US$4.00. However, with financing on deck, and the company still being at least 30 months away from first concentrate sales under a more conservative permitting timeline, I don't see any urgency to rush into the stock. This is especially true given that developers on balance have not been responding well at all to the typical Lassonde Curve over the past two years, and even with relatively favorable financing terms like for Sabina (equity, stream debt, which is similar what Skeena will look for), we've typically seen significant share-price weakness following the announcement of project financing. Therefore, while I think the worst of the correction is over, I don't see the catalyst for higher prices just yet, outside of a consistent trend higher in gold which is not a company-specific catalyst as it benefits all gold juniors/producers.

Summary

Skeena has seen a significant fall from grace since its 2021 peak, affected by inflationary pressures that have weighed on project economics for mines (opex) and especially pre-construction developers (opex+capex), an acquisition that can often end up killing share-price momentum, and the worst sentiment in the sector we've seen in years. Adding insult to injury, some junior producers have found themselves at even more attractive valuations than September 2022, creating a relative value issue for names like Skeena given that investors can get cash-flowing names with no capex blowout risk for only a moderately higher multiple. Finally, while the company is certainly a potential takeover target, it hasn't helped that the companies that might have typically been logical suitors have been busier swallowing bigger fish (Yamana, Newcrest, Pretium).

That said, Skeena is unique relative to other developers in the sense that its capex blowout risk is quite low because of having an already constructed tailings facility, having a less-stale study in place and benefiting from having a brownfields site and a relatively small plant (~3.7 million tonnes per annum) compared to larger projects like Cote and Magino which went way over-budget. And while Skeena packs a punch from a production profile standpoint, it's also somewhat of a unicorn from a future margin standpoint and has the right team in place with Randy Reichert at the helm [former Fekola Mine GM and VP Operations at B2Gold ( BTG )] to ensure the mine plan is optimized and runs as smoothly as possible. To summarize, given Skeena's massive and growing resource in a Tier-1 jurisdiction, its potential for industry-leading margins, and its untapped exploration upside at depth, I would view any pullbacks below US$4.25 as buying opportunities.

For further details see:

Skeena Resources: Valuation Improving After The Drop