CA - Skeena Resources: Robust Eskay Creek Economics Despite Higher Capex

2024-01-08 01:01:25 ET

Summary

- Skeena Resources released an updated Feasibility Study for its Eskay Creek Project in the Golden Triangle.

- While estimated upfront capex (+20%) and sustaining capex (+300%) increased meaningfully year-over-year, the project is de-risked and is still one of the best undeveloped gold assets globally.

- In this update, we'll dig into the updated FS, recent developments, and whether the stock is offering enough of a margin of safety after its recent rally.

It's been a rough past 18 months for the gold developer space, and while there have been a few names that have bucked the trend and some pre-resource developers like New Found Gold ( NFGC ) and Snowline ( OTCQB:SNWGF ) continue to trade at producer-like valuations, returns have been disappointing on balance. This is not overly surprising given the much higher cost of capital, above planned share dilution (low equity prices) and continued inflationary pressures that have weighted on project economics. Worse, developers have had to compete with producers for investment capital given how the highly attractive valuations (and lower risk) among some small-cap producers like K92 Mining ( OTCQX:KNTNF ) at less than 4x FY2026 free cash flow estimates with the potential to become the lowest-cost producer sector-wide in 2026 (sub $700/oz all-in sustaining costs).

Fortunately, although Skeena Resources ( SKE ) has been beaten up just like its peers, the company's project economics have not seen a significant downgrade like other projects, and its After-Tax NPV (5%) actually improved year-over-year (albeit helped by higher metals price assumptions). This was primarily due to additional metallurgical testing that has suggested the possibility to produce a higher-grade gold and silver concentrate with lower concentrate volumes, higher grades from more selective mining, and a longer mine life, more than offsetting higher upfront/sustaining capex. In this update we'll dig into the updated FS, recent developments, and whether the stock is offering enough of a margin of safety after its recent rally.

All figures are in United States Dollars at an exchange rate of 0.80 to 1.0 CAD/USD.

{kind=link}

Golden Triangle, British Columbia - Company Website

Updated Feasibility Study

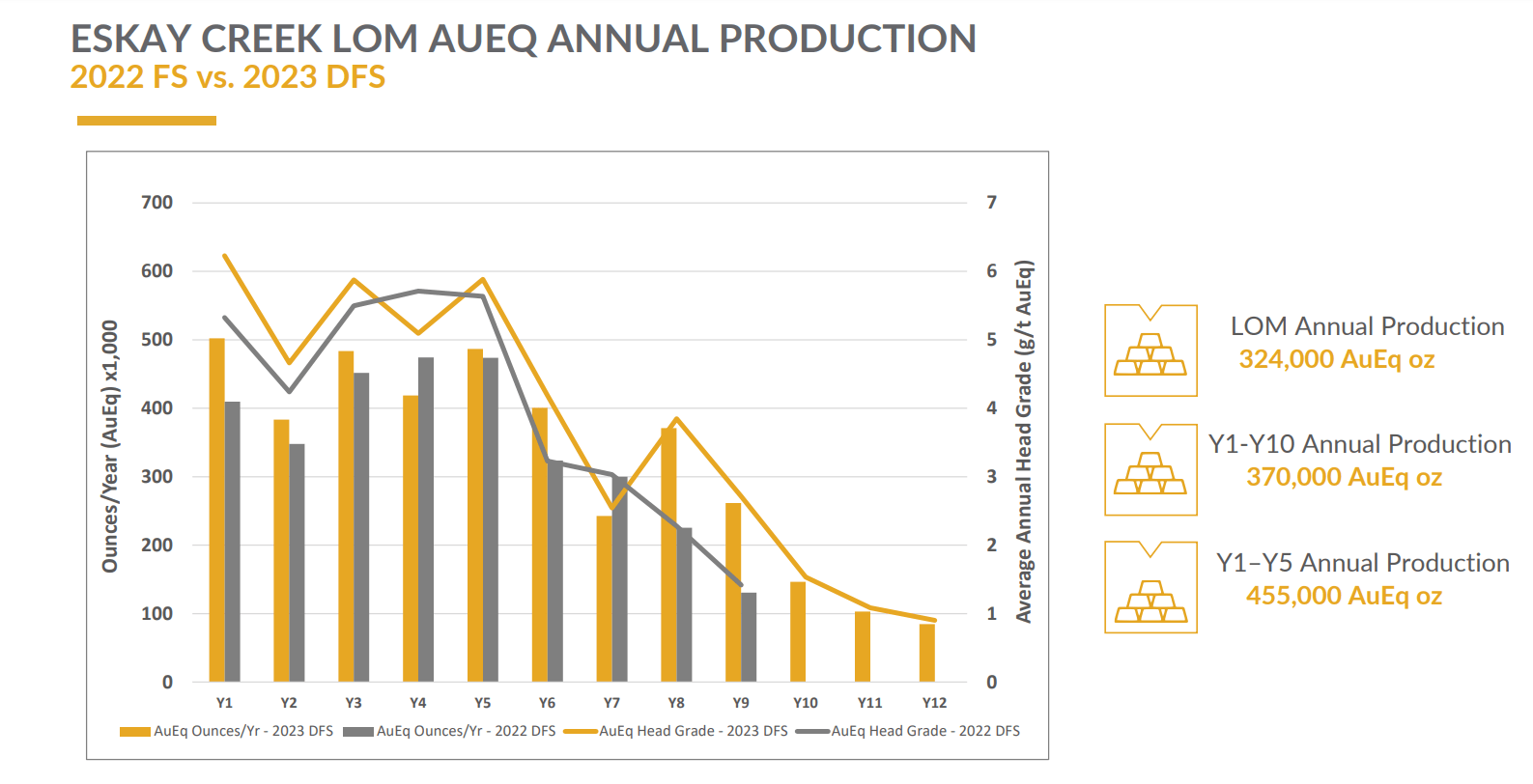

Skeena Resources ("Skeena") released an updated Feasibility Study for its Eskay Creek in the Golden Triangle of British Columbia last month and unveiled a more de-risked project relative to its Q3 2022 iteration. The updated study has seen upfront capex increase by over 20% to ~$570 million which is not surprising (albeit above my estimates of ~$500 million), a significant increase in sustaining capital expenditures ($112 million ---> ~$449 million) which was also to be expected due to persistent inflationary pressures, and higher mining costs of ~$43.20/tonne vs. ~$41.00/tonne in the previous study. On a positive note, first five year production has increased to ~445,000 gold-equivalent ounces [GEOs] vs. ~431,000 GEOs previously (albeit offset by lower LOM GEO production, largely due to the longer mine life with lower production in years 11 and 12), and reserve grades have increased to 4.6 grams per tonne of gold equivalent vs. 4.0 grams per tonne gold-equivalent previously ~40 million tonnes vs. ~30 million tonnes).

{kind=link}

Eskay Creek Gold-Equivalent Production Profile - 2023 FS vs. 2022 FS - Company Website

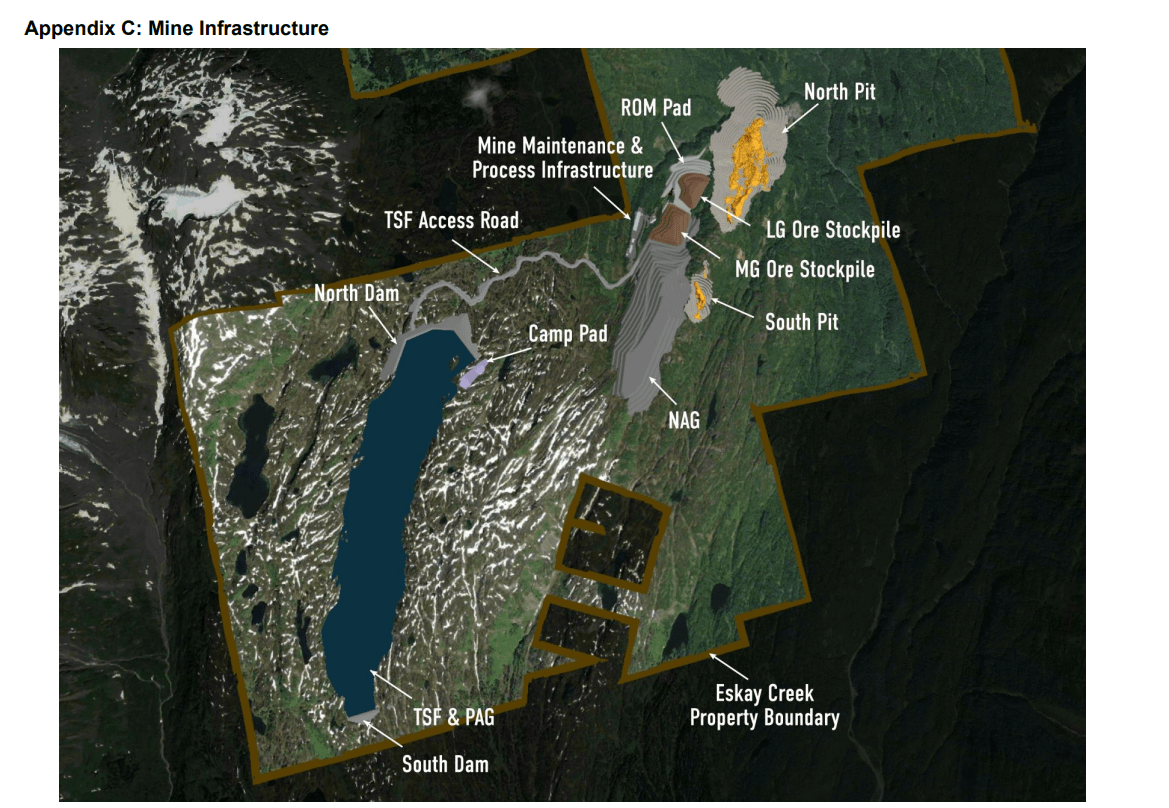

The other positives worth noting are that the company has de-risked the project with pre-production mining accelerated to provide a larger stockpile at start-up, a larger mining fleet has been proposed to increase mining rates in the easier to mine no-snowfall months to offset lower production in the winter, and the company is looking at more selective mining vs. the 2022 FS. Finally, concentrate grades are significantly higher than in the 2022 FS with an optimized flowsheet leading to a 43% lower mass pull and ~1.1 million fewer concentrate tonnes of the life of mine. This is based on grinding ore down to 40 microns under the simplified flow sheet before completing the first rougher flotation, and then re-grind all that concentrate down to 10 microns. Notably, on top of decreasing costs, Skeena noted that the higher-grade concentrate could provide an opportunity for base metals content to be payable and some previous penalty elements to be neutral vs. incurring penalties previously.

{kind=link}

Eskay Creek Planned Mine Infrastructure - Company Website

Overall, this optimization provided a meaningful lift to NPV, with the After-Tax NPV (5%) increasing to ~$1.6 billion vs. ~$1.13 billion previously, albeit with the benefit of higher metals price assumptions ($1,800/oz gold and $23.00/oz silver vs. $1,700/oz gold and $19.00/oz silver in previous study). In fact, these optimizations more than offset the much higher upfront and sustaining capital over the mine life. That being said, I think a $590 million to $600 million upfront capex bill is a safer assumption even when factoring in the benefit of having a permitted TSF already in place vs. other undeveloped projects vs. the current estimate of ~$570 million (0.80 CAD/USD). Hence, I would expect project financing to be closer to $600 to provide a buffer rather than having to go back to market later like some other companies.

As for potential project enhancements, the company has shared that additional opportunities to potentially improve Eskay Creek's NPV include the following:

- improved smelter terms, and the potential for lower operating costs with the potential for deeper mineralization to contribute additional ore tonnes

- the possibility of steepening pit slopes to reduce potential waste movement

- the potential to incorporate Snip into the mine plan and slightly increase overall production levels which could extend the mine life by bringing higher-grade tonnes into the mine plan

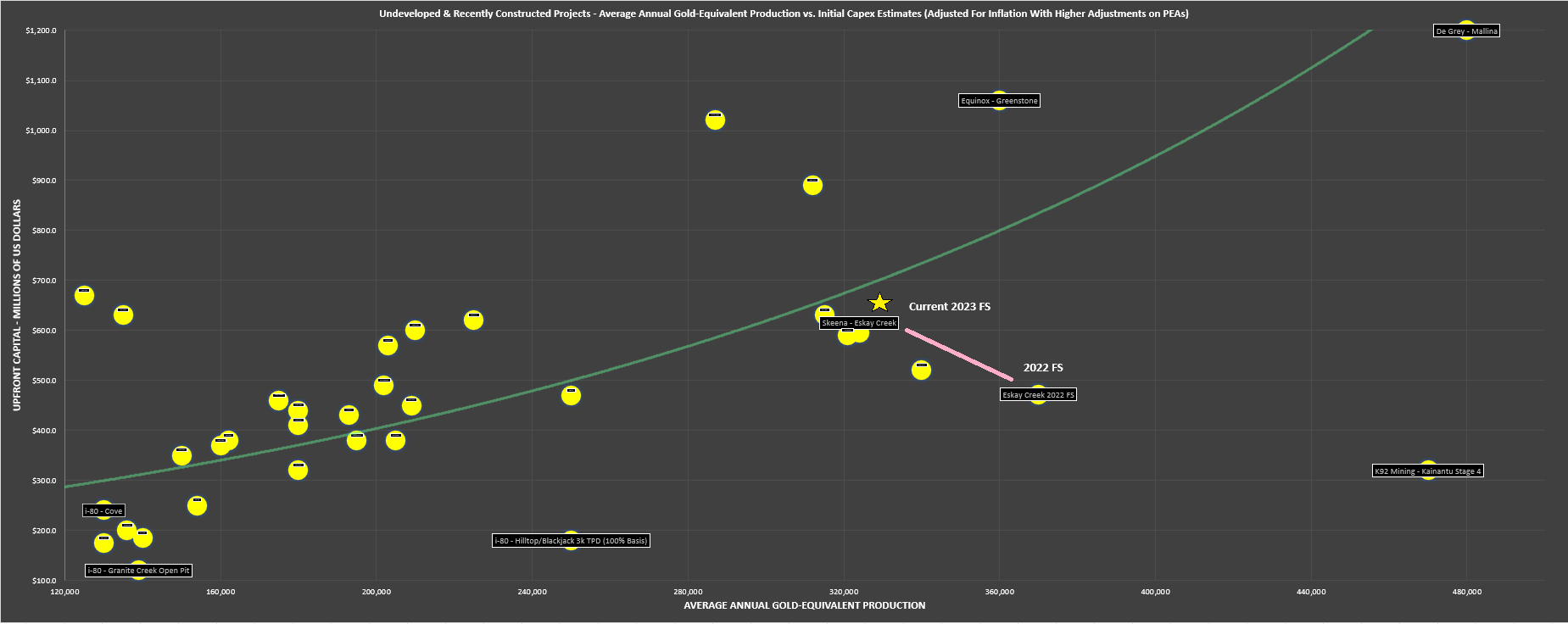

Eskay Creeks Stacks vs. Other Projects

Looking at the below chart, the best projects are located below the green trend line and further right on the chart which indicates high production levels relative to upfront capital expenditures, with the second-best projects being in the bottom to mid left (mid-scale gold projects but well below average upfront capex).

As we can see in the below chart, only a handful of projects have this designation. These projects typically benefit from being brownfields sites with existing processing/tailings infrastructure (Skeena benefits from having a permitted TSF,) and/or extremely high-grade projects that benefit from smaller relative footprints offset by grades to push production higher (like Hod Maden, Windfall, Kainantu Stage 4). Some other examples include i-80 Gold's ( IAUX ) projects in Nevada which benefit from significant sunk costs (autoclave, CIL plants) industry-leading grades above 10.0 grams per tonne gold-equivalent for its underground projects, and a deposit with industry-leading grades for its heap-leach project (Granite Creek Open Pit).

Eskay Creek 2023 Study vs. 2022 Study & Undeveloped Gold Projects/Recently Constructed Projects - Average GEO Production vs. Upfront Capex - Company Filings, Author's Chart & Author's Estimates

{kind=link}

As for Eskay Creek, the project has gone from being one of the most robust undeveloped projects (2022 FS) to still one of the most robust projects, albeit with a lower average production profile and higher capex. That said, the project is still one of the top-10 best undeveloped precious metals projects globally on an After-Tax NPV to Initial Capex ratio basis and has very manageable capex relative to other projects just shy of Tier-1 scale (500,000 ounces) like Cote, Skouries, and Greenstone. Additionally, it's worth noting that production in the first ten years comes in at 370,000 ounces, so it's actually more robust than it appears on the below chart, but has a lower life-of-mine production due to the added two years of mine life. And if Snip is added to the mine plan at ~1,000 tonnes per day, first ten-year production could come in closer to 400,000 GEOs.

To summarize, Skeena's Eskay Creek Project may look slightly less robust on a LOM production/upfront capex basis, but this is a study that is more de-risked than the 2022 study, and first-five year production is far higher which will result in significant free cash flow generation even assuming a stream is added on the asset.

Recent Developments

Following the release of the Feasibility Study, Skeena has improved its financial flexibility with the sale of an additional 1.0% NSR on the project for ~$45 million, and has secured a convertible debenture (7% interest rate) that matures on the earlier of December 19th, 2028 or on the completion of a Board approved project financing for Eskay Creek with a conversion price of US$6.15. These transactions have increased the company's fully diluted share count to ~102 million shares and increased the total royalty on Eskay Creek to 3.0% (2.0% previously), but these were understandably far better options than selling shares in the company near a valuation of ~0.35x NPV (8%). Hence, I think this was a positive deal for Skeena even if it has led to additional share dilution ahead of what's likely to be another round of 20%+ share dilution to complete project financing.

On the subject of financing, Skeena's Executive Chairman Walter Coles recently shared the following thoughts in an interview, implying that equity will ideally be kept to a minimum as part of the overall financing package and that the preference would be for a gold-equivalent stream vs. solely a silver stream.

"My current thinking is to lean more on the stream than the debt or the equity. In fact, I'd like to keep the equity as low as a percentage of the total financing package as possible. And I feel like if we lean more on the stream, we can probably bring down the equity component to 15% of the total project financing, maybe even a little less. So you know I'm very cognizant of trying to minimize the amount of dilution we have as we go to finance this project."

- Skeena Resources Executive Chairman, Walter Coles

Based on the above comments, we can assume that Skeena is looking at something similar to the financing packages put together for Sabina Gold & Silver (Goose Project) and G Mining Ventures ( OTC:GMINF ) at Tocantinzinho, which included ~30% equity for Sabina and ~25% equity for G Mining. And if we assume a financing of at least $570 million, 20% equity as a portion of the total to be more conservative ($114 million), and a share price of US$4.00, this would translate to an additional 28.5 million shares issued or nearly 30% share dilution from current levels. This would certainly be a much better outcome vs. companies like Marathon Gold that saw 60% share dilution (in addition to warrants) as part of their September 2022 financing, but could still leave Skeena with closer to 130 million fully diluted shares as it graduates to producer status (assuming no issues from a permitting standpoint).

Overall, this decision to focus mostly on a stream will further affect project economics on top of the recent increase in the royalty rate, but past streaming deals have been on quite reasonable terms and certainly more favorable than equity in the current depressed market environment for developers. These have included step downs to 7.5% (12.5% at onset) after 300,000 ounces have been delivered at Tocantinzinho and 1.5% - 2.15% of gold vs. 4.15% at Goose, and buyback options (33% of total gold stream at Goose) under certain conditions. That said, while these financings with a lower equity portion led to better share price performance outcomes vs. Marathon Gold, which was recently picked off by Calibre ( OTCQX:CXBMF ) at fire-sale prices, we still saw a final leg down in Sabina's share price despite a favorable financing deal, meaning that it's hard to rule out a final re-test of the US$3.00 - US$3.50 level for Skeena.

Valuation

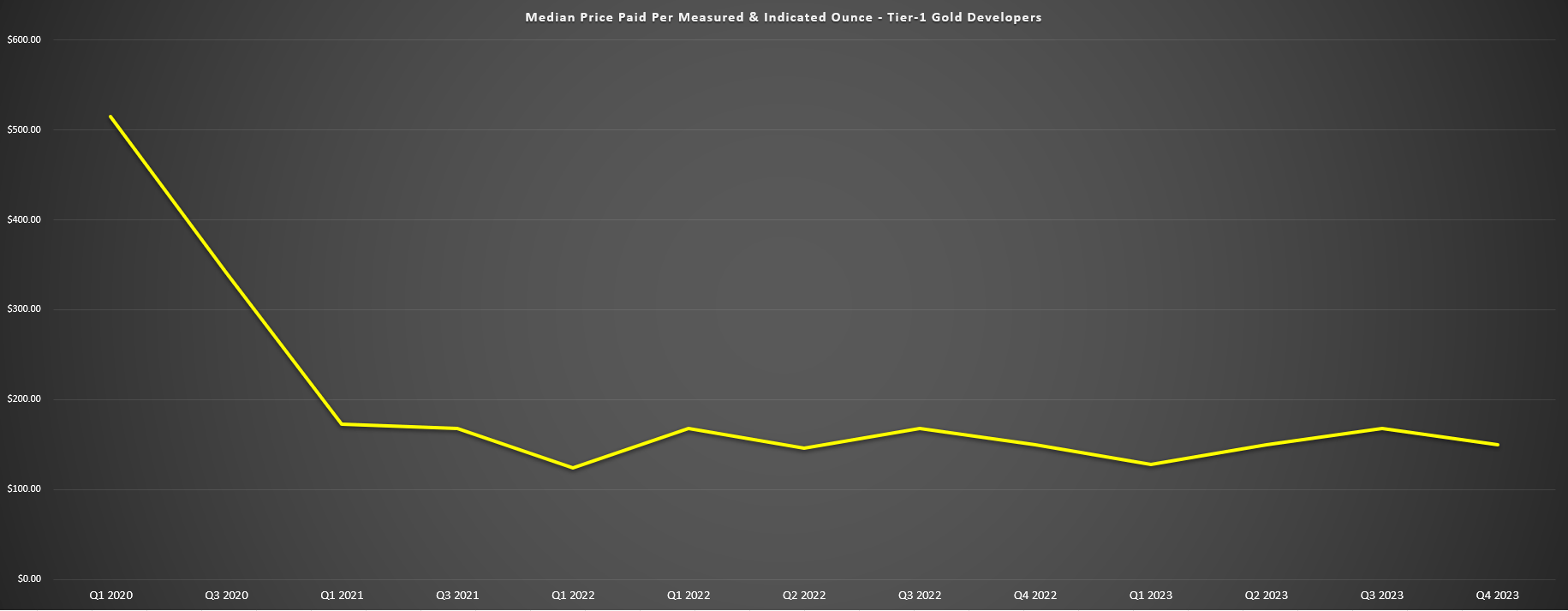

Based on ~102 million fully diluted shares and a share price of US$4.40, Skeena trades at a market cap of ~$450 million, leaving it trading at just ~$71/oz on measured and indicated [M&I] ounces, a discount to the average price paid for M&I ounces in Tier-1 jurisdictions of $132/oz from 2021 through 2023. However, the median price paid across the past five acquisitions for Tier-1 jurisdiction developers has declined to just ~$80/oz, and we've seen acquisitions as low as ~$50/oz with the recent acquisition of Marathon Gold. And while Skeena's Eskay Creek undoubtedly is one of the best undeveloped projects compared to those acquired over the past few years, it's quite clear we've seen meaningful multiple compression when it comes to where developers trade today vs. the 2021/2022 average, and where they've been acquired on a P/NAV standpoint. In fact, the past three North American developers to be acquired came at an average of less than 0.70x P/NAV at an 8% discount rate (SBB, MOZ, GSV).

So, although Skeena certainly screens cheaply, I think a safer assumption for the fair value for Tier-1 jurisdiction ounces for developers is ~$100/oz - $120/oz on M&I ounces vs. the ~$150/oz to ~$300/oz deals that look to be more of outliers especially after several cheaper deals in the past two years (SBB, MOZ, GSV, KOR).

{kind=link}

Median Price Paid Per M&I Ounce (Tier-1 Jurisdiction Developers With Deal Price Above $120 Million) - Company Filings, Author's Chart

So, what's a fair value for Skeena today?

Using an estimated ~130 million fully diluted shares at year-end and based on an estimated NPV (8% - $1,875/oz gold, $23.00/oz silver) of ~$1.19 billion and using what I believe to be a more conservative multiple of 0.80x P/NAV ($952 million), I see a fair value for Skeena of US$7.30. Some investors might argue that an 8% discount rate is too high for an advanced stage project in a Tier-1 ranked jurisdiction, but I would argue that it actually might be too low given the current cost of capital for developers and where risk-free rates sit today (and given the fact that Skeena is still not yet fully permitted). However, I have reduced the discount rate from 9.5% to 8.0% previously to factor in a more de-risked study vs. the 2022 study and the fact that there appears to be less upside risk on interest rates. And based on these assumptions (NPV 8% estimate includes a slightly longer mine life, additional conservatism on costs/upfront capex, and higher grades from Years 3 to 8 with the addition of Snip ore), Skeena has a 68% upside from current levels.

While it's quite possible that these metals price assumptions are conservative, I prefer to use three-year average prices as a base case and have bonus upside if prices are higher rather than model higher prices and potentially have too ambitious of assumptions which could result in significant portfolio losses.

Although this represents attractive upside, I am looking for a minimum 50% discount to fair value to justify starting new positions in gold developers, and ideally closer to 60% given that they are very high-risk investments. And after applying the low of this required discount (50%) to fair value, Skeena's low-risk buy zone comes in at US$3.64 or lower. Obviously, there are no guarantees that Skeena trades down to this level, and waiting for these prices may result in a missed opportunity. However, I prefer to buy at the right price or pass entirely when it comes to high-risk names, and this is especially true when there are still opportunities in the producer space at less than 0.50x P/NAV (8%) that carry much lower risk (already financed, in commercial production, fully permitted, and significant available data on how mine plan conforming to assumptions). Hence, with some other names sector-wide still trading at similar P/NAV multiples to Skeena while in production, I continue to focus elsewhere for the time being.

Summary

Skeena Resources recent Feasibility Study has confirmed the robust economics at Eskay Creek, but the company is sitting in a less favorable portion of the Lassonde Curve and ahead of project financing and further share dilution which can often lead to a final leg down in the share price of a developer. In addition, although there is significant free cash flow on the horizon for patient investors, it's best to err on the side of conservative without full permits in hand, and commercial production that could still be over three years away (March 2027). Finally, while the company has presented a de-risked study, this is not an easy environment to operate an open-pit mine and while I have high confidence in the team under the leadership of Randy Reichert (ex-Fekola GM), I'd be less worried about near flawless execution in sunny Mali (~300 millimeters of annual precipitation vs. the Golden Triangle at ~2,800 millimeters, with the bulk of this as snow).

{kind=link}

Eskay Creek Snow Risks & Climate - 2023 TR

Balancing the negatives with the positives (Eskay Creek is a high-grade and fast payback project in a Tier-1 ranked jurisdiction), Skeena continues to be one of the better positioned developers in the market today, and there's no reason the stock can't trade much higher once in commercial production. That said, there are some producers trading at similar P/NAV multiples generating free cash flow today without up to 30% share dilution on the horizon and not having to trudge through a more mixed portion of the Lassonde Curve from a share price return standpoint (pre-financing/permitting/pre-construction), where names like Osisko Mining ( OTCPK:OBNNF ), Marathon, De Grey Mining ( OTCPK:DGMLF ), and Contango Ore ( CTGO ) have seen lifeless returns.

In summary, while Skeena may have upside to offset its higher risk (developer vs. producer), this is a unique period with considerable bifurcation from a valuation standpoint in the producer space with several lower-risk but significant upside opportunities elsewhere. For this reason, I continue to see more attractive reward/risk bets elsewhere and I still don't see enough margin of safety in Skeena's valuation at current levels after its recent ~40% rally.

For further details see:

Skeena Resources: Robust Eskay Creek Economics Despite Higher Capex